Report on Staff’s Review of Insider Reporting

and User Guides for Insiders and Issuers

OSC Staff Notice 51-726 -- Report on Staff's Review of Insider Reporting and User Guides for Insiders and Issuers is reproduced on the following internally numbered pages. Bulletin pagination resumes at the end of the Staff Notice.

OSC Staff Notice 51-726

Report on Staff's Review of Insider Reporting and User Guides for Insiders and Issuers

February 18, 2016

1. Introduction

This notice reports the findings and comments of staff (collectively, staff or we) of the Ontario Securities Commission (OSC) arising from an issue-oriented review of the continuous disclosure (CD) records and insider filings of 100 reporting issuers whose principal regulator (PR) is Ontario. The purpose of the review was to assess compliance and assist reporting insiders with meeting insider reporting requirements.

The 100 Ontario PR reporting issuers selected for the review resulted in a corresponding review of approximately 1,500 reporting insiders. While approximately 85% of the reporting insiders we reviewed were materially compliant, we found material insider reporting deficiencies{1} in approximately 15% which resulted in approximately 200 reporting insiders filing new insider reports on the System for Electronic Disclosure by Insiders (SEDI) to address these deficiencies. Generally, these reporting insiders were charged late filing fees as contemplated in section 10.1(2) of Companion Policy 55-104CP Insider Reporting Requirements and Exemptions (55-104CP).

- - - - - - - - - - - - - - - - - - - -

Reporting insiders of issuers of all sizes need to improve the quality of their insider reporting for accuracy, completeness and timeliness.

- - - - - - - - - - - - - - - - - - - -

The compliance rate for insider reporting can be substantially improved, and this improvement needs to happen across all reporting issuers. We found material insider reporting deficiencies in approximately 70% of the issuers we reviewed. There was minimal correlation between the size of the reporting issuer and the occurrence of material insider reporting deficiencies. Our findings suggest that reporting insiders of issuers of all sizes need to improve the quality of their insider reporting for accuracy, completeness and timeliness.

To assist issuers and reporting insiders in meeting their reporting obligations, staff strongly recommend that issuers and insiders take note of the guidance provided in this notice including the user guides for reporting insiders and reporting issuers attached as Appendix B and Appendix C, respectively. We will continue to monitor and review insider reporting as part of our normal course CD review program, with an emphasis on:

• educating issuers and their reporting insiders; and

• identifying reporting insiders who are failing to report and thereby compromising the integrity of our insider reporting regime.

2. Background

The insider reporting requirements serve a number of functions, including deterring improper insider trading based on material undisclosed information and increasing market efficiency by providing investors with information concerning the trading activities of insiders, and, by inference, the insiders' views of the respective issuer's future prospects.

Insider reporting also discourages illegal or otherwise improper activities involving stock options and similar equity-based instruments, including stock option backdating, option repricing and opportunistic timing of grants since the requirement for timely disclosure and public scrutiny of such disclosure will generally limit opportunities for insiders to engage in such improper practices.

When insiders fail to comply with insider reporting requirements, this affects the integrity, reliability and effectiveness of the insider reporting regime, which in turn has a negative impact on market efficiency. As such, it is crucial for investors to have access to reliable trading information of insiders. All instances of inaccurate reporting can negatively impact the insider reporting regime. However, when an insider fails to file any report in connection with a trade in a security, our regime is significantly impacted.

3. Regulatory Requirements and Guidance

The following represents a summary of the key regulatory requirements and guidance on insider reporting.

National Instrument 55-104

In Ontario, the general insider reporting requirements are found in the Securities Act (Ontario) (the Act). Certain insider reporting requirements in the Act have been varied by National Instrument 55-104 Insider Reporting Requirements and Exemptions (NI 55-104) which consolidated the principal insider reporting requirements and exemptions available in various Canadian jurisdictions in a single national instrument to make it easier for reporting issuers and reporting insiders to understand their obligations.

Reporting insiders are generally required to file an initial insider report within 10 calendar days of becoming a reporting insider. Any subsequent insider reports reflecting changes in their holdings must be filed within 5 calendar days of such change. "Reporting insider" is defined in NI 55-104, and generally includes persons who have routine access to material undisclosed information concerning a reporting issuer and/or significant influence over the reporting issuer.

National Instrument 55-102

National Instrument 55-102 System for Electronic Disclosure by Insiders (SEDI) (NI 55-102) sets out the process for filing insider reports. Reporting insiders are required to file insider reports containing securities trading information in electronic format at www.sedi.ca for public dissemination.

National Policy 51-201

National Policy 51-201 Disclosure Standards (NP 51-201) provides guidance on "best disclosure" practices for issuers to promote good disclosure, enhance their credibility with investors and minimize the risk of non-compliance with securities legislation. As part of the guidance, NP 51-201 includes a provision on insider trading policies and blackout periods.

Additional Guidance

There are numerous Canadian Securities Administrators (CSA) and CSA staff notices{2} which remind reporting issuers and their reporting insiders of their filing obligations and provide guidance on the process by which to file their insider reports.

4. Review Objectives

The objectives of our review were as follows:

• to assess insider reporting compliance;

• to raise awareness for issuers and insiders on insider filing requirements; and

• to gather information about insider trading policies.

5. Review Scope

For the purpose of this review, we selected 100 reporting issuers whose PR is Ontario. The issuers were randomly selected from across all industries in proportion to the total number of Ontario PR reporting issuers in each industry.{3} Sixty-five percent of the reporting issuers selected for review were non-venture issuers and the remaining 35% were venture issuers.{4} Each selected issuer had, on average, 15 active reporting insiders at the beginning of the review, for a combined total of approximately 1,500 reporting insiders.

We compared the insider information contained in public CD documents of the issuers available on the System for Electronic Document Analysis and Retrieval (SEDAR) (including management information circulars, annual information forms, annual financial statements and prospectuses) with the insider information reported on SEDI to identify any discrepancies. We also reviewed insider trading policies requested from issuers to determine whether issuers have developed these policies in accordance with the best practices set out in NP 51-201.

As part of the review, we corresponded with all 100 reporting issuers. In addition, in order to address the matters noted during our review, we corresponded with approximately 530 reporting insiders or their filing agents about the reporting insiders' SEDI filings.

6. Findings

Based on our review, we identified two main areas where improvement is needed:

- - - - - - - - - - - - - - - - - - - -

Issues

1. The quality of insider reporting

2. Insider trading policies

- - - - - - - - - - - - - - - - - - - -

Improvement in the Quality of Insider Reporting is Required

We found deficiencies in insider reports filed by reporting insiders of issuers of all sizes which resulted in reporting insiders or issuers, as applicable, having to make either remedial or correctional filings or other amendments on SEDI as described below.

a) Material deficiencies leading to remedial filings

• We found material insider reporting deficiencies in approximately 15% of the reporting insiders we reviewed, which resulted in approximately 200 reporting insiders making one or more remedial filings on SEDI to address these deficiencies.

• In approximately 70% of the issuers reviewed, at least one insider was required to file a remedial filing to address a material deficiency.

These reporting insiders were generally charged late filing fees as contemplated in 55-104CP.

In general, we found material insider reporting deficiencies where there were:

i. Missing reporting insider profiles

• Approximately 30% of the issuers had at least one reporting insider that did not have an insider profile and failed to file insider reports on SEDI.

The majority of these reporting insiders were either directors or senior officers of reporting issuers or significant shareholders of reporting issuers. In certain cases, the reporting insiders who failed to file were the issuers themselves (e.g., for acquisitions under a normal course issuer bid (NCIB)). In most cases, these reporting insiders failed to report their holdings in the respective issuers' common shares.

ii. Balance discrepancy in SEDI filings vs. CD records

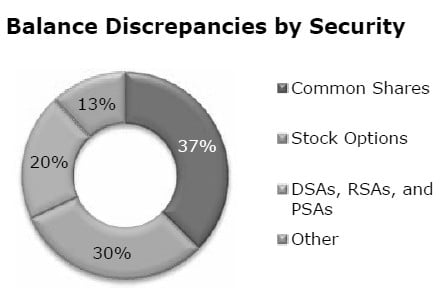

• Approximately 65% of the issuers had at least one reporting insider that had a variance equal to or greater than 5% between the balances of securities holdings as reported on SEDI versus CD records of the respective issuer.

The majority of these reporting insiders were directors or senior officers of reporting issuers. The variances were most common for holdings of common shares and stock options, followed by deferred share awards (DSAs), restricted share awards (RSAs) and performance share awards (PSAs) as shown in the chart below.

Image

Some of the common reasons we noted in our review for the material discrepancies discussed above leading to remedial filings were as follows:

Unfamiliarity with definition of "reporting insider"

Some reporting insiders were not aware that they had reporting obligations under NI 55-104.{6}

Unfamiliarity with definition of "significant shareholder" in NI 55-104

Some reporting insiders were not aware that when an individual holds more than 10% of the outstanding shares of an issuer through a holding company, that holding company is also a "significant shareholder" under NI 55-104, which is required to have its own insider profile and file its own insider reports.{7}

Failure to file reports for acquisitions under a NCIB

Some issuers failed to file insider reports for acquisitions of a security of its own issue under a NCIB in accordance with Part 7 of NI 55-104, which requires issuers to file an insider report disclosing each acquisition under a NCIB within 10 days of the end of the month in which the acquisition was completed.{8}

Failure to report expiration of securities

Many insiders failed to report expiration of certain issuer derivative securities such as options or warrants within the required 5 day period.{9}

Late reporting due to issuer delays

Some insiders failed to file insider reports on time because they did not receive certain key information from issuers on a timely basis. In some cases, this was due to the fact that issuers failed to file issuer event reports as required under NI 55-102 to alert insiders to changes affecting all holdings of a class of securities.{10}

Reliance on third parties

Some reporting insiders relied on third parties to make their filings and had genuinely believed that such filings had been made.

{6} See definition of "reporting insider" in NI 55-104 and Part 3 of NI 55-104 for primary insider reporting requirements.

{7} See definition of "significant shareholder" in NI 55-104 which includes a person or company that has beneficial ownership of, or control or direction over, whether direct or indirect, securities of an issuer carrying more than 10% of the voting rights attached to all the issuer's outstanding voting securities. In general, there is no reporting exemption available for a holding company that is a significant shareholder and whose share holdings are only reported by the ultimate individual shareholder.

{8} See Part 7 of NI 55-104 and item 4.5.1 of Staff Notice 55-316.

{9} See section 3.3 of NI 55-104 which requires a reporting insider to file a report to disclose any change in the reporting insider's beneficial ownership of, or control or direction over, whether direct or indirect, securities of the reporting issuer.

{10} See section 2.4 of NI 55-102 as well as Form 55-102F4 Issuer Event Report and Part 8 of NI 55-104.

- - - - - - - - - - - - - - - - - - - -

Staff Recommendation:

As responsibility to file insider reports remains with the reporting insider regardless of whether they use a third party agent, reporting insiders should periodically review SEDI to make sure their reports are being filed correctly.

- - - - - - - - - - - - - - - - - - - -

b) Non-material deficiencies leading to correctional filings

• In approximately 45% of issuers reviewed, at least one insider filed inaccurate insider reports on SEDI (with one or more non-material deficiencies (as described below)) which resulted in approximately 150 reporting insiders making correctional filings to address the non-material deficiencies.

These reporting insiders were not subjected to late fees or other penalties.

Some of the non-material deficiencies resulting in correctional filings were as follows:

• inaccurate transaction codes;

• inaccurate transaction dates;

• inaccurate reporting with respect to type of ownership (direct, indirect or control or direction);

• not reporting the name of the registered holder; and

• use of incorrect security designations by issuers, precluding their insiders from correctly reporting their transactions (see discussion below under the heading "Use of incorrect security designations").

c) Other common findings

In addition to the above, staff observed the following:

i. Unfamiliarity with requirement to update insider profiles and issuer profile supplements on SEDI

Reporting insider profiles

Some reporting insiders were not aware that when they cease to be a reporting insider of a reporting issuer, their insider profile on SEDI must be amended to reflect this fact within 10 calendar days of the change.

• Approximately 500 insiders were asked to update their profile on SEDI to disclose that they had ceased to be reporting insiders of reporting issuers.

Some reporting insiders were also not aware that their contact information was out of date.

• Approximately 300 insiders were required to update their profile on SEDI as their contact information was out of date.

- - - - - - - - - - - - - - - - - - - -

Staff Recommendation:

Reporting insiders should be proactive and periodically review their insider profiles on SEDI to determine whether they continue to be shown as reporting insiders of issuers and whether their contact information is current.

- - - - - - - - - - - - - - - - - - - -

Issuer profile supplements

Some reporting issuers were not aware that they are required to file an amended issuer profile supplement on SEDI immediately if there is a change in the information disclosed in their issuer profile supplement.

• Approximately 60% of issuers had out of date issuer profile supplements which required updating.

Some of the common issues noted were as follows:

• the insider affairs contact was out of date; and

• security designations needed to be updated (see below).

- - - - - - - - - - - - - - - - - - - -

Staff Recommendation:

Issuers should be proactive and periodically review their issuer profile supplement to see if any updates are required and remind their insiders to review their insider profiles for accuracy and completeness.

- - - - - - - - - - - - - - - - - - - -

ii. Use of incorrect security designations by issuers

In their issuer profile supplements, reporting issuers are required to designate all types of securities and related financial instruments that are held by insiders.

• Security designations were required to be updated for approximately 40% of reporting issuers reviewed.

Security designations needed to be updated for the following reasons:

• security designations were omitted;

• security designations were set up incorrectly; or

• security designations needed to be archived.

The majority of security designations that required updating were issuer derivative securities (e.g., stock options, rights, RSAs, DSAs and PSAs). Incorrect designation of issuer derivative securities as simple equity securities precluded insiders from properly reporting the characteristics of these securities (e.g., exercise price and vesting or expiration date) and transactions in these securities (e.g., the exercise or vesting of such securities).

- - - - - - - - - - - - - - - - - - - -

Staff Recommendation:

Guidance on creating security designations can be found in Staff Notice 55-316. However, issuers should contact the OSC if they have further questions to ensure new securities designations are set up properly in SEDI.

- - - - - - - - - - - - - - - - - - - -

iii. Limited use of issuer grant reports by issuers

• Only 10% of issuers filed one or more issuer grant reports since January 2014.{11}

An issuer grant report is a report that may be voluntarily filed by a reporting issuer on SEDI which discloses the details of a grant of stock options or similar instruments to its insiders under a compensation arrangement which has already been described in a public document filed on SEDAR.

While there is no obligation for an issuer to file issuer grant reports, staff believe that increased use of issuer grant reports by issuers would be beneficial to all stakeholders as it would provide the market with timely information about the existence and material terms of a grant and provide insiders with relief from having to report the grant within the ordinary reporting time periods.{12}

- - - - - - - - - - - - - - - - - - - -

Staff Recommendation:

To communicate information about a grant in a timely manner and to help avoid late fees being charged against its insiders, issuers should consider filing an issuer grant report within 5 days of a grant.

- - - - - - - - - - - - - - - - - - - -

iv. Lack of internal processes to reconcile insider reports on SEDI with issuers' CD records on SEDAR

As mentioned above, we observed that in many cases, information contained in SEDI filings did not reconcile to the related issuer's CD records available on SEDAR. Some issuers noted that the information contained in CD documents was incorrect as the issuer relied solely on the information communicated by insiders and did not compare such information to the insiders' SEDI filings.

• Staff issued comments to approximately 20% of the reporting issuers reviewed requesting that they implement, on a going-forward basis, an internal process to reconcile insiders' reported holdings in CD documents to SEDI filings.

Staff believe that such internal processes are an important element in the design and operation of issuers' internal control over financial reporting and disclosure controls and procedures.

- - - - - - - - - - - - - - - - - - - -

Staff Recommendation:

Issuers should implement a process to annually verify the securities holdings communicated to them by insiders in order to avoid variances in the public records filed by the issuer on SEDAR versus the reports filed by insiders on SEDI.

Reporting insiders should be proactive and review information circulars annually and other CD records of the issuer on a regular basis to ensure their security holdings are properly reflected.

- - - - - - - - - - - - - - - - - - - -

Improvement of Insider Trading Policies is Recommended

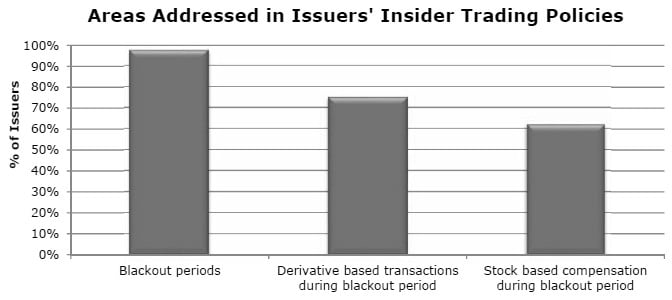

Most issuers had a written insider trading policy that was in accordance with the best practices set out in NP 51-201 and provided for "blackout periods" around regularly scheduled earnings announcements.

• Approximately 85% of the issuers had written insider trading policies in place.

However, as demonstrated in the chart below, certain policies reviewed by staff did not restrict derivative-based transactions or the grant of stock options or similar forms of stock-based compensation during blackout periods.

While these types of transactions are not specifically addressed in NP 51-201, staff believe that having a written insider trading policy which prohibits such transactions during blackout periods is essential to avoid public and regulatory scrutiny relating to the opportunistic timing of such actions taken on the basis of market prices which do not reflect material undisclosed information.

Image

- - - - - - - - - - - - - - - - - - - -

Staff Recommendation:

Issuers should annually review their insider trading policies to ensure they align with current Canadian securities legislation.

Issuers should also adopt a written policy which, among other things, specifically prohibits derivative-based transactions, the grant of options and the setting of the exercise price during blackout periods. The written policy should also provide for a senior officer to approve and monitor the trading activity of all insiders, officers, and senior employees.

- - - - - - - - - - - - - - - - - - - -

7. Examples

For examples of common deficiencies noted by staff during this review, please see Appendix A.

8. Conclusion

Our findings suggest that many reporting insiders need to improve the quality of their insider reporting for accuracy, completeness and timeliness. Staff strongly recommend that issuers and reporting insiders take note of the recommendations made in this notice and consider other processes that can be put in place to increase the rate of compliance with insider reporting obligations.

To assist issuers and their reporting insiders, we have included as Appendix B and Appendix C, checklists which highlight some of the key points that reporting insiders and issuers, respectively, should consider in complying with insider reporting requirements.

Staff remind issuers and reporting insiders of their responsibility to ensure that their filing obligations under NI 55-102 and NI 55-104 are satisfied. We also remind issuers and reporting insiders that regulatory action may be taken against issuers and reporting insiders who have not fulfilled their insider reporting requirements.

We will continue to monitor and review insider reporting as part of our normal course CD review program with an emphasis on continuing to educate issuers and reporting insiders on their obligations. We will also focus on identifying those reporting insiders who fail to file reports given the negative impact this non-compliance has on our insider reporting regime and market efficiency.

9. Questions

If you have any questions, please feel free to contact any of the following individuals:

Inquiries and Contact Centre, Strategy and Operations Branch

{1} "Material insider reporting deficiency" or "material deficiency" means a compliance deficiency with insider reporting requirements which requires a reporting insider to file one or more new insider reports on SEDI (remedial filings) in order to correct the deficiency.

{2} CSA Staff Notice 55-312 Insider Reporting Guidelines for Certain Derivative Transactions (Equity Monetization)(Revised); CSA Staff Notice 55-315 Frequently Asked Questions about National Instrument 55-104 Insider Reporting Requirements and Exemptions; CSA Staff Notice 55-316 Questions and Answers on Insider Reporting and the System for Electronic Disclosure by Insiders (SEDI) (Staff Notice 55-316); OSC Staff Notice 55-701 Automatic Securities Disposition Plans and Automatic Securities Purchase Plans.

{11} While it is possible that other issuers did not have a reason to file issuer grant reports since January 2014, staff believe that this is highly unlikely given that many reporting issuers have compensation plans which contemplate granting of stock options or similar instruments.

{12} See section 6.2 of NI 55-104 for the terms of the insider reporting exemption for certain issuer grants.

APPENDIX A

EXAMPLES

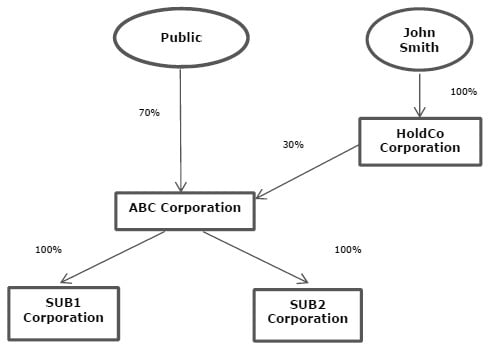

Refer to the following diagram for Examples 1 and 2.

Image

Example 1:

Q. ABC Corporation is a reporting issuer. It has two subsidiaries, SUB1 Corporation and SUB2 Corporation, each of which is wholly owned and considered a "major subsidiary" for purposes of NI 55-104. Each of the directors and senior officers of SUB1 Corporation and SUB2 Corporation holds common shares of ABC Corporation. Do these directors and senior officers need to file insider reports?

A. Yes, the directors and senior officers{1} of SUB1 Corporation and SUB 2 Corporation need to file insider reports in respect of their holdings in the common shares of ABC Corporation.

We note that senior officers and directors of major subsidiaries of an issuer are "reporting insiders" under NI 55-104. "Major subsidiary" is defined in NI 55-104 as a subsidiary of an issuer if the assets or revenue of the subsidiary are 30 percent or more of the consolidated assets or revenue of the issuer, as applicable.

Example 2:

Q. Holdco Corporation is a private holding company. Mr. John Smith owns all of the common shares of Holdco Corporation. Holdco Corporation owns 30% of the shares in ABC Corporation. Mr. John Smith has a SEDI insider profile and reports his indirect ownership in ABC Corporation through Holdco Corporation. Is Holdco Corporation required to have its own insider profile and file its own insider reports in respect of the common shares it holds in ABC Corporation?

A. Yes, Holdco Corporation is required to have its own insider profile and file its own insider reports. The definition of "significant shareholder" means a person or company that has beneficial ownership of, or control or direction over, whether direct or indirect, securities of an issuer carrying more than 10 percent of the voting rights. As Holdco Corporation has control or direction over the securities that are held in its name representing 30% of the shares of ABC Corporation, and it does not otherwise qualify for a reporting exemption under NI 55-104, it should have its own filings on SEDI.

Example 3:

Q. Effective January 1, 2016, ABC Corporation enters into a new compensation plan which contemplates grants of restricted share awards (RSAs) and performance share awards (PSAs) as long term incentives for its senior officers. The RSAs and PSAs entitle the holder to common shares of ABC Corporation after a specified period. On May 31, 2016, ABC Corporation awards RSAs and PSAs to its senior officers. What actions could ABC Corporation take to encourage reporting insiders to comply with their insider reporting obligations?

A. We recommend ABC Corporation take the following steps:

1. Prior to the first grants of RSAs and PSAs, publicly disclose the existence and material terms of the compensation arrangement in an information circular or other public document filed on SEDAR.

2. Prior to the first grants of RSAs and PSAs, create new security designations for RSAs and PSAs on SEDI as contemplated under section 3.2.7 of Staff Notice 55-316:

A brief description of the security can be added to the name of the security (e.g., vesting date and/or conversion details).

3. File an issuer grant report within 5 days of the grant (i.e., within 5 days of May 31, 2016) on SEDI in accordance with section 6.3 of NI 55-104 to allow its reporting insiders to take advantage of the delayed reporting exemption in section 6.2 of NI 55-104.

Example 4:

Q. ABC Corporation announces the launch of a NCIB by way of a press release on April 1, 2016. On May 14, 2016 and May 28, 2016, ABC Corporation purchases for cancellation 1000 common shares and 3000 common shares respectively under the NCIB. The common shares purchased are cancelled on June 13, 2016. What actions should ABC Corporation take to comply with its insider reporting obligations?

A. ABC Corporation should take the following steps:

1. Create an insider profile on SEDI (if it has not done so already) to reflect that it is a reporting insider.

2. File two separate insider reports on or prior to June 10, 2016 to report the May acquisitions under the NCIB -- one for the 1000 common shares purchased on May 14, 2016 and one for the 3000 common shares purchased on May 28, 2016.

3. File two separate insider reports on or prior to July 10, 2016 to report the cancellation of common shares purchased on May 14, 2016 (1000 common shares) and May 28, 2016 (3000 common shares), respectively.

For more information, see section 4.5.1 of Staff Notice 55-316.

{1} "Senior officer" refers to persons acting as the CEO, CFO and COO of an issuer. See the definitions of CEO, CFO and COO in NI 55-104.

APPENDIX B

USER GUIDE FOR REPORTING INSIDERS

This user guide is provided to assist reporting insiders with their insider reporting obligations. This guide is not meant to be exhaustive and we remind reporting insiders that responsibility for complying with the insider reporting requirements under Ontario securities laws rests with the reporting insiders themselves.

Yes

No

N/A

Part A: Reporting Insider Profile on SEDI

1

I have reviewed the definition of "reporting insider" under NI 55-104 and I am considered a reporting insider of the reporting issuer.

_____

_____

_____

Note: You may need to seek advice about this item. You should also determine whether you qualify for an insider reporting exemption under NI 55-104 or otherwise under Ontario securities laws.

If "yes" to items 1 and 2, within 10 calendar days of becoming a reporting insider, I have registered as a SEDI user and filed my insider profile on SEDI identifying my relationship with the reporting issuer.

_____

_____

_____

4

I periodically review my SEDI insider profile and make updates to my profile where required.

_____

_____

_____

5

I am no longer a reporting insider of the reporting issuer and I have amended my SEDI insider profile within 10 calendar days of that change in status to indicate that I have ceased to be a reporting insider of the reporting issuer.

_____

_____

_____

Part B: Insider Reports on SEDI

6

I have filed insider reports on SEDI that reflect all of my securities holdings and related transactions.

_____

_____

_____

7

I periodically review records of my securities holdings and compare those records to the filings I have made on SEDI for purposes of accuracy and completeness.

_____

_____

_____

Note: This should include a review of:

_____

_____

_____

--

balances in securities holdings

_____

_____

_____

--

transaction dates

_____

_____

_____

--

transaction codes

_____

_____

_____

--

type of ownership (direct, indirect or control or direction)

_____

_____

_____

8

I use a filing agent or other third party for my reporting insider filings on SEDI.

_____

_____

_____

9

If "yes" to item 8, I review my SEDI filings on a periodic basis to ensure all requested filings are accurate and complete.

_____

_____

_____

10

I hold issuer derivatives with expiration dates (e.g., stock options).

_____

_____

_____

11

If "yes" to item 10, I have reported the expiration of any issuer derivative securities on SEDI within 5 days of the expiration date.

_____

_____

_____

Part C: Holding Companies that are Significant Shareholders

12

I hold more than 10% of the outstanding shares of the reporting issuer through a holding company that I control.

_____

_____

_____

13

If "yes" to item 12, I have reported on SEDI that I have control or direction over those shares through my holding company.

_____

_____

_____

14

If "yes" to item 13, my holding company has filed its own insider reports on SEDI for the shares that it directly owns.

_____

_____

_____

Part D: Grants of Stock Options and Other Forms of Compensation

15

I have received stock options or other forms of compensation under the reporting issuer's compensation plans.

_____

_____

_____

16

If "yes" to item 15, I have checked the reporting issuer's SEDI profile to determine if the reporting issuer has filed an issuer grant report within 5 days of each grant.

_____

_____

_____

Note: If an issuer grant report has been filed by the issuer within 5 days of the grant in accordance with Part 6 of NI 55-104, you have until March 31 of the next calendar year to report the grant, unless you transfer or dispose of the granted securities before such date (in which case the grant needs to be reported within 5 days of the transfer or disposition).{2}

_____

_____

_____

17

If an issuer grant report has not been filed by the reporting issuer, I have reported each grant on SEDI within 5 days of the grant.

_____

_____

_____

Part E: Continuous Disclosure Filings of the Reporting Issuer

18

I have reviewed the continuous disclosure filings of the reporting issuer (e.g., management information circulars) that include my securities holdings for accuracy and completeness and reported any discrepancies to the reporting issuer.

_____

_____

_____

{1} In this guide, "hold" or "holdings" refer to beneficial ownership of, or control or direction over, whether direct or indirect, securities of the reporting issuer.

{2} There are certain exceptions for "specified dispositions". See Part 6 of NI 55-104.

APPENDIX C

USER GUIDE FOR REPORTING ISSUERS

This user guide is provided to assist reporting issuers with their insider reporting obligations as well as the reporting obligations of their reporting insiders. This guide is not meant to be exhaustive and we remind reporting issuers that responsibility for complying with the insider reporting requirements under Ontario securities laws rests with the issuers themselves (if applicable) and their reporting insiders.

Yes

No

N/A

Part A: Issuer Profile Supplement on SEDI

1

The reporting issuer periodically reviews the insider affairs contact information on its issuer supplement on SEDI and makes updates where required.

_____

_____

_____

2

The reporting issuer periodically reviews its security designations on its issuer supplement on SEDI to ensure that all securities have been designated and archived as appropriate.

_____

_____

_____

Note: The reporting issuer should ensure that "issuer derivative securities" such as stock options, restricted share awards, deferred share awards and performance share awards have been categorized as issuer derivative securities.

_____

_____

_____

Part B: Insider Reports on SEDI

3

The reporting issuer engages in NCIBs.

_____

_____

_____

4

If "yes" to item 3, the issuer has created an insider profile on SEDI so that it can report acquisitions under a NCIB.

_____

_____

_____

5

If "yes" to item 3, the reporting issuer has reviewed its filings on SEDI to ensure that all transactions related to NCIBs have been reported on SEDI within 10 days of the end of the month in which the transaction was completed.

_____

_____

_____

6

The reporting issuer has recently announced an "issuer event" that affects all holdings of an entire class of its securities in the same manner.

_____

_____

_____

Note: An "issuer event" includes:

_____

_____

_____

--

stock dividend

_____

_____

_____

--

stock split

_____

_____

_____

--

consolidation

_____

_____

_____

--

amalgamation

_____

_____

_____

--

reorganization

_____

_____

_____

--

merger

_____

_____

_____

--

other similar event

_____

_____

_____

7

If "yes" to item 6, the reporting issuer has filed an issuer event report on SEDI no later than one business day following the occurrence of the issuer event.

_____

_____

_____

Part C: Grants of Stock Options and Other Forms of Compensation

8

The reporting issuer has compensation arrangements under which grants of stock options and similar instruments may be made to reporting insiders.

_____

_____

_____

Note: The reporting issuer should consider filing an issuer grant report within 5 days of a grant to provide the market with timely information about the existence and material terms of a grant and allow reporting insiders to take advantage of the delayed reporting exemption in section 6.2 of NI 55-104.

_____

_____

_____

9

If "yes" to item 8, the reporting issuer notifies its reporting insiders of such grants in a timely manner (by filing an issuer grant report or otherwise).

_____

_____

_____

Part D: Continuous Disclosure Filings of the Reporting Issuer

10

The reporting issuer relies on information communicated by its reporting insiders to prepare its continuous disclosure records (e.g., management information circulars).

_____

_____

_____

Note: To avoid discrepancies in public records, the reporting issuer should consider implementing a process to compare securities holdings disclosed by its reporting insiders on SEDI to the balances communicated to the reporting issuer.