Notice of Proposed Change and Request for Comment – Change to the MATCHNow Trading System – TriAct Canada Marketplace LP

TriAct Canada Marketplace LP (operating as MATCHNow) hereby announces plans to implement the change described below, following approval by the Ontario Securities Commission (the OSC). MATCHNow is publishing this Notice of Proposed Change in accordance with the "Process for the Review and Approval of Rules and the Information Contained in Form 21-101F2 and the Exhibits Thereto." Market participants are invited to provide the OSC with comments on the proposed change.

Comments on the proposed change should be in writing and submitted by August 23, 2021 to:

Market Regulation Branch

Ontario Securities Commission

20 Queen Street West, 22nd Floor

Toronto, Ontario M5H 3S8

Email: [email protected]

A copy should also be provided to:

David Nolan

Chief Compliance Officer

MATCHNow

Equinix TR2, 45 Parliament Street, Suite 13155, c/o Cboe Flex Office #13155

Toronto, Ontario, M5A 0G7

Email: [email protected]

Comments received will be made public on the OSC website. Upon completion of the review by OSC staff, and in the absence of any regulatory concerns, notice will be published to confirm the completion of OSC staff's review and to specify the intended implementation date of the change.

Any questions concerning the information below should be addressed to Vince Poil, Head of Products for MATCHNow, at (416) 861-1010 or at [email protected].

Cboe LIS Powered by BIDS (the "New Conditionals Offering")

MATCHNow proposes to implement a "Significant Change subject to Public Comment" to its Form 21-101F2 (the Form F2), to replace the existing technology underlying the entering and processing of MATCHNow's existing conditional orders (Conditionals) with a new "large-in-scale" (LIS) trading technology, developed by MATCHNow's corporate affiliate, BIDS Trading L.P.{1} and to introduce certain related changes to how Conditionals will be entered and processed on the MATCHNow ATS (the Cboe LIS Powered by BIDS Offering or simply the New Conditionals Offering).{2}

The New Conditionals Offering can be broken down into six individual, but related components, each of which is described in detail in Section A. below, in order of relative significance.{3}

A. Detailed description of the proposed change

1. The New "Sponsored Access Model"

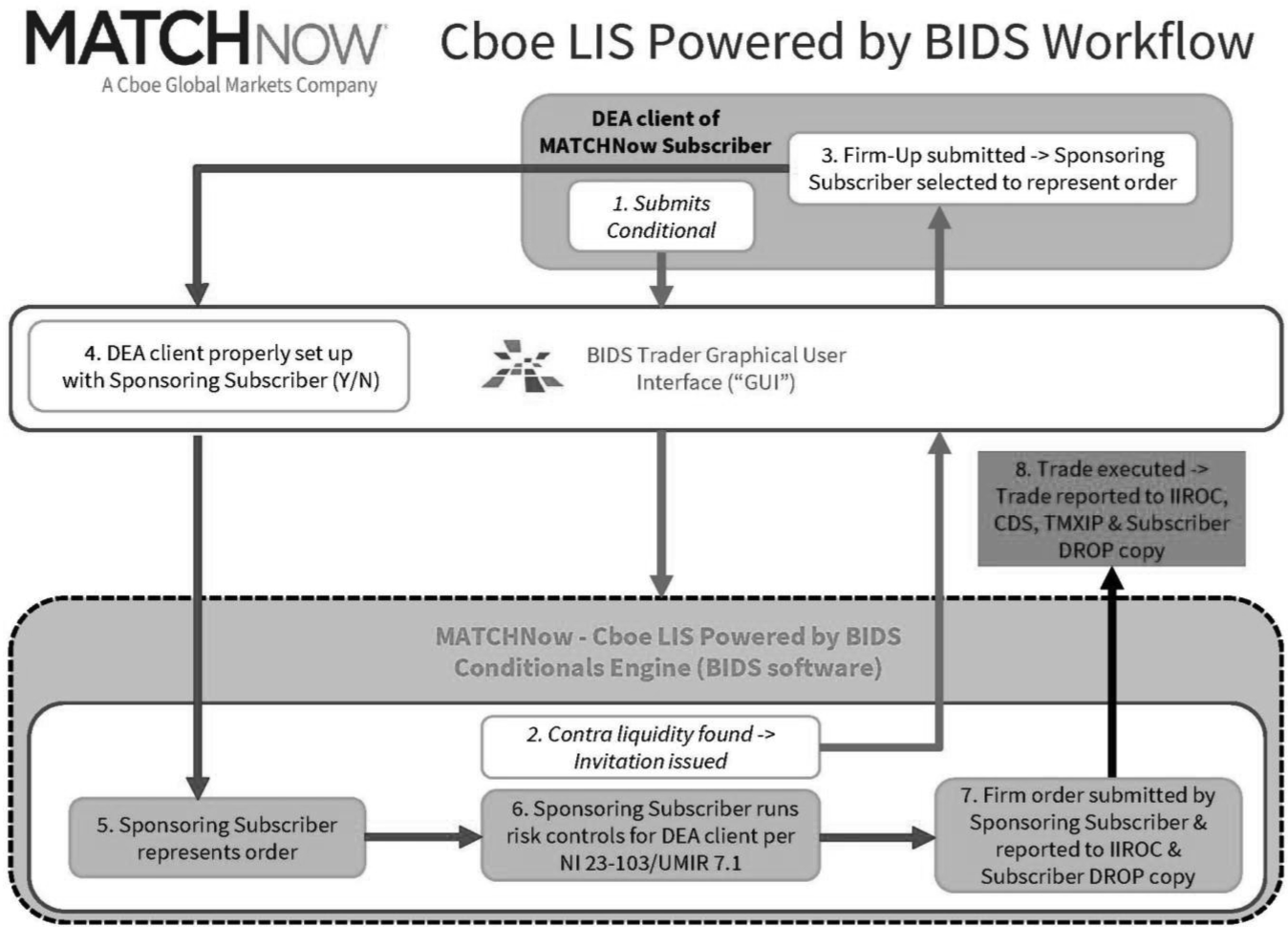

MATCHNow is proposing to expand Conditionals to allow eligible institutional investors (often colloquially referred to as "buy-side firms") that have taken the appropriate steps to be granted direct electronic access (DEA) by a MATCHNow Subscriber (each, colloquially referred to as a "sell-side firm") to send Conditionals to the MATCHNow ATS, using the Participating Organization number of the Subscriber that they have designated as their sponsor for such purposes. This expanded functionality may be referred to as MATCHNow's "Sponsored Access Model" for Conditionals.

With the proposed change, MATCHNow will offer both Subscribers and eligible institutional investors (including, but not limited to, Canadian buy-side firms, such as pension funds, private equity funds, and asset management firms, as well as exempt foreign dealer equivalents and, where appropriate, their institutional investor clients) (collectively, DEA Clients or, where properly set up in the MATCHNow system, Sponsored Users) a new BIDS front-end interface (in the case of Subscribers, the Subscriber Interface, and, in the case of Sponsored Users, the Sponsored User Interface), which will allow each Sponsored User to enter and, where contra liquidity is found, firm up Conditionals through a direct FIX connection to MATCHNow.{4}

MATCHNow will take reasonable measures to verify that all DEA Clients of its Subscribers are properly set up before being granted access, as Sponsored Users, to enter Conditionals through the Sponsored User Interface, and will require that all Sponsored Users be appropriately supervised at all times by their sponsoring MATCHNow Subscriber(s).{5} Most notably, each sponsoring MATCHNow Subscriber will need to execute the new "Sponsored Access Addendum" to the MATCHNow Subscriber Agreement (the Addendum). The Addendum includes several new contractual obligations for each Subscriber that signs it, including:

• an obligation, in connection with each trade that originates as a Conditional, to represent (and be responsible for) the resulting trade and, in particular, to ensure that it is reported and settled in the normal course by the Subscriber as a Participant of CDS (or through an agent that is a CDS Participant);

• an obligation to ensure that the Subscriber has entered into all requisite agreements with its prospective Sponsored User (DEA Client), has in place all required policies and procedures to establish proper relationship(s), account(s), and risk controls with or for each such prospective Sponsored User, and that all requirements pursuant to section 3 of National Instrument 23-103 Electronic Trading and Direct Electronic Access to Marketplaces (NI 23-103), applicable rules of the Investment Industry Regulatory Organization of Canada (including, in particular, Rules 6.2, 7.1, 7.13, 10.15, and 10.18 of its Universal Market Integrity Rules or UMIR), and other applicable regulatory requirements are complied with at all times; and

• an obligation to make proper use of the Subscriber Interface to set up the appropriate pre-trade, automated risk controls for each Sponsored User and to take reasonable measures to monitor those risk controls (which includes monitoring risk control-related threshold alerts), and if necessary, adjusting those risk controls, in accordance with the Subscriber's obligations under NI 23-103, UMIR 7.1, and any other applicable regulatory requirements.

MATCHNow will also require each Subscriber to identify and provide certain basic information for each DEA Client that it intends to have as a Sponsored User in the New Conditionals Offering and to update that list at least once annually. This contractual framework will provide that every Sponsored User is, at all times, in a proper (DEA Client) relationship with at least one MATCHNow Subscriber, either directly or indirectly,{6} or else its access will not be granted or, if already granted, will be promptly suspended.

The new process for the "Sponsored Access" aspect of the New Conditionals Offering may be illustrated as follows:

The Subscriber Interface will provide the following new features for Subscribers to set for their own trading and for that of their Sponsored Users:

• fat-finger checks;

• single order limits;

• daily open orders plus traded value limits for buys;

• daily open orders plus traded value limits for sells; and

• gross daily orders plus traded value limits for buys and sells.

As noted above, and as will be spelled out in the Addendum, the responsibility for setting and supervising all risk controls will remain with the Subscriber, even though it will have the flexibility to configure risk controls in a unique manner for each of its Sponsored Users, as it sees fit, and then to conduct its supervision programmatically (i.e., in an automated manner). Nevertheless, at a minimum, MATCHNow will verify that, before granting "Sponsored User" access to any DEA Client, the latter has at least one sponsoring Subscriber that:

• has set static limits for that DEA Client; and

• has the ability to shut off that DEA Client at any time.

MATCHNow personnel will leverage best practices developed by BIDS and will work with BIDS personnel in an integrated and seamless manner to verify that all required set-up is completed before access to the new functionality is turned on for any prospective Sponsored User, and to address any issues that may arise once Sponsored Users are sending and firming up Conditionals through the new platform.

2. Invitation Sequencing, Time Limits, and Minimum Size

If the proposed change is approved, MATCHNow will offer three types of Conditional interactions:

• Subscriber-to-Subscriber (which currently exists);

• Subscriber-to-Sponsored User/Sponsored User-to-Subscriber (which is new); and

• Sponsored User-to-Sponsored User (which is also new).

With respect to Subscriber-to-Sponsored User (and vice-versa) interactions, the Sponsored User's trading will normally be conducted by a human trader; in that circumstance, the system is designed to send the invitation to firm up to the Sponsored User first-i.e., before the invitation to firm up is sent to the Subscriber (which is always an electronic user). In such cases, the Sponsored User (human trader) will have up to 30 seconds to firm up the invitation. This is necessary to give human traders the practical ability to make a deliberate, conscious decision to firm up and/or adjust (i.e., modify or cancel) their Conditional (or firmed-up Conditional), in light of any similar conditional or firm orders that the trader has submitted on behalf of his or her firm to MATCHNow or other marketplaces. That said, the Conditionals Compliance Mechanism (which is discussed in greater detail below) will mitigate any potential information leakage and prevent human traders from abusing their 30-second window.

With respect to Subscriber-to-Subscriber (often algorithm-to-algorithm) interactions, the process will include the following characteristics:

• Invitations will be synchronous (i.e., simultaneous); and

• The time limit for firming up will continue to be one second (as it exists today, in the current Conditionals offering);

As for Sponsored User-to-Sponsored User interactions (where the interaction is human-to-human), the process will include the following characteristics:

• Invitations will be synchronous; and

• The time limit for firming up will be 30 seconds for both sides.

As regards minimum size thresholds, all three types of interactions, should the proposed change be approved, will be subject to the same minimums that will apply to all existing Conditionals once the recently-approved "Opt-In Feature" (see In re TriAct Canada Marketplace LP -- Proposed Change to the MATCHNow Trading System -- Notice of Approval, (2021), 44 OSCB 4986 (June 10)) is implemented-namely, the requirements set out in UMIR 6.6 (i.e., greater than 50 standard trading units and greater than $30,000 in nominal value or greater than $100,000 in nominal value).

3. Pro-Rata Allocation Replaced by Price/Broker/Size/Time Priority

MATCHNow proposes to replace the existing one-to-many matching process for its Conditionals with a primarily one-to-one matching process for all Conditionals in the New Conditionals Offering.{7} This change will enhance the user experience, as it will yield fewer fall-downs and shorter wait times for firm-ups. (In fact, this is how the BIDS technology is already configured for existing U.S. and European equivalents of the New Conditionals Offering; it has thus far worked well in those other jurisdictions, and we believe it will have a similar positive impact in Canada.) As a result, allocations will no longer follow pro-rata logic, but instead, will be done based on priority of firmed-up orders, using the following criteria, in this order:

• Price;

• Broker;

• Size; and

• Time.

This type of prioritization will enhance the efficiency of trading that originates through the Conditionals matching engine, without harming the liquidity or pricing of smaller orders on MATCHNow or other marketplaces (including lit marketplaces). Indeed, Conditionals are purposely designed to encourage large, block-sized trades, and this shift away from pro-rata allocation to prioritized matching is logically and appropriately aligned with, and fully supportive of, that purposeful design.

4. Execution Anywhere within the Protected National Best Bid or Offer

As part of the New Conditionals Offering, MATCHNow is proposing to replace its existing mid-point-only executions for firmed-up Conditionals with a new feature that will allow executions at a price that is anywhere within the range of prices created by the current Protected National Best Bid or Offer (the PNBBO).{8} This will be achieved through a new optional pegged order functionality.

If the proposed change is approved, Subscribers will have the ability to enter Conditionals with an optional pegged price, with or without an "offset". This pegged functionality would work as follows:

A peg is designed to maintain a purchase or sale price relative to the PNBBO.

There are 3 types of supported peg types as part of our New Conditionals Offering:

• Peg mid;

• Near-side Peg (Peg to Bid when buying or the Offer when selling); and

• Far-side Peg (Peg to the Offer when buying or to the Bid when selling)

A peg offset will also be supported. This will allow a level of discretion to set a peg on a Conditional-by-Conditional basis. Peg discretion is measured in dollar-value increments of $0.005, and it is added to the result of the peg calculations.

We expect that moving away from mid-point-only executions to executions anywhere within the PNBBO will increase the number of matches and facilitate more activity in the MATCHNow Conditionals book, with the potential of increasing liquidity for Canadian market participants as a whole.

For illustrative purposes, as an Appendix to this Notice, we have provided examples of Conditionals matching in different scenarios, including in the context of differing peg selections.

5. Conditionals Compliance Mechanism Will Evolve

For the reasons explained in MATCHNow's original Form F2 amendment filing for Conditionals (see In re TriAct Canada Marketplace LP -- Change to the MATCHNow Trading System -- Notice of Proposed Change and Request for Comment, (2018), 41 OSCB 3936 (May 10) at 3937), MATCHNow views its compliance mechanism for Conditionals (the Conditionals Compliance Mechanism) as an integral part of the offering, as it provides that information leakage is mitigated and any potential abusive conduct is discouraged and minimized, without undermining fair access to the Conditionals destination. Nevertheless, over time, MATCHNow has made minor tweaks to the Conditionals Compliance Mechanism-in some cases, in response to feedback from its Subscribers and other stakeholders, and in other cases, as a result of its own analysis of its Conditionals-related data and what its competitors and counterparts are doing in the conditional order space in Canada and around the world.

With that in mind, MATCHNow is proposing to replace the existing full trading suspension for the duration of the trading day that applies today whenever a Subscriber crosses below the 70% threshold of firms-up for the day (provided that at least 20 invitations have been received) with a more targeted symbol-by-symbol suspension. Specifically, in the New Conditionals Offering, Subscribers that receive 20 or more invitations to firm up a Conditional for a given security will need to avoid crossing below the 70% threshold of firm-ups for that security, failing which the Subscriber will be suspended from receiving invitations for any new Conditionals that it enters for that security for the rest of that trading day.

A symbol-by-symbol suspension is logical and appropriate because the risk of information leakage only arises when a market participant is repeatedly falling down on invitations to firm up its Conditionals for a specific security. In other words, suspending a Subscriber for falling down on twenty invitations to firm up where each firm-up pertains to just one of twenty different equity securities does not, in our view, serve a regulatory (market integrity) purpose. A symbol-by-symbol approach is not only more effective, it is more equitable, as the penalty (a symbol-by-symbol suspension) is more proportional.

That being said, the basic parameters of the Conditionals Compliance Mechanism will remain the same, namely, the mechanism will only be engaged from the moment 20 invitations have been sent to a given market participant, and a suspension will be imposed for the duration of the trading day (for the affected symbol) if the rate of firm-ups for that participant falls below 70% within that trading day. Moreover, in the new offering, those parameters will apply equally to both Subscribers and Sponsored Users.{9} MATCHNow will continue to report daily suspensions of Subscribers (including which symbols were affected by the suspension) to IIROC and to each affected Subscriber in real time via email. The existing one-second "lookback" will be eliminated, however, as it will no longer be necessary (in addition to not being a feasible feature for Sponsored Users).

6. Improved reporting for Subscribers

The New Conditionals Offering will provide enhanced daily reporting for Subscribers, which will help them assess their Conditional firm-up and trade performance, including summary information regarding:

• Number of invitations;

• Number of firm-ups;

• Firm-up rate (percentage);

• Shares traded;

• Value traded;

• Number of trades;

• Average trade size;

• Detailed invitation and firm-up data on a per-order basis, including:

• Trader ID;

• Symbol;

• Invitation time;

• Response time (from invitation to firm-up);

• Result (e.g., traded, failed to respond, PNBBO moved, contra cancelled);

• Conditional resting time;

• Event type (e.g., aggressive order, passive order, PNBBO event).

This BIDS technology-based reporting is already well-regarded in the United States and Europe, and we believe it will be highly informative and will benefit the Canadian market as well.

B. Expected implementation date

The proposed change is expected to be implemented on February 1, 2022 (provided that approval by the OSC has been granted prior to that date).

C. Rationale for the proposed change and any supporting analysis

As a result of the features described in detail in Section A. above, the New Conditionals Offering will promote liquidity and fair access by allowing MATCHNow to unlock certain untapped liquidity for large-size orders, without disturbing the pricing mechanism of existing dark and lit markets in Canada. It will treat all Subscribers equally. Moreover, it will leverage the technology and many years of client satisfaction, regulatory scrutiny, and business growth that BIDS and Cboe have had in Europe and the United States with similar offerings, thus providing a Canadian version of the functionality already offered by these marketplaces outside of Canada.

D. The expected impact, including the quantitative impact, of the proposed change on market structure, subscribers, and, if applicable, investors and capital markets

The impact on market structure, Subscribers, investors, and capital markets is expected to be positive, through the resulting expansion of liquidity and increased matching and price improvement opportunities for large-sized orders. With the enhanced functionality of the New Conditionals Offering, we anticipate further electronification and growth of the block market in Canada, which presently represents approximately 5% to 10% of overall volume.

E. Expected impact of the proposed change on MATCHNow's compliance with Ontario securities law requirements and in particular requirements for fair access and maintenance of fair and orderly markets

The proposed change will have no impact on MATCHNow's continuing compliance with Ontario securities law, including requirements for fair access and the maintenance of fair and orderly markets.

In particular, MATCHNow respectfully submits that the shift away from pro-rata allocation for Conditionals is fully compliant with the "fair access" requirements of sections 5.1 and 5.7 of National Instrument 21-101 Marketplace Operation for the following reasons:

• the Cboe LIS Powered by BIDS technology is purposely and exclusively designed to facilitate block (large-in-scale) trading, in particular, by requiring a minimum size-threshold that parallels the requirements of UMIR 6.6;

• as a block-only book, it can only truly function as such by moving away from a pro-rata fill allocation to a one-to-one matching model, which favors block liquidity;

• By prioritizing size over arrival time, the New Conditionals Offering emphasizes the block-only nature of this functionality, and by rewarding larger-sized orders, it ensures a higher average trade (execution) size, which in turn attracts and incentivizes higher quantity orders from all participants.

MATCHNow's regular book, which can facilitate trades of any size, including those stemming from very small orders, will continue to allocate matches on a pro-rata basis, which is important for treating small orders fairly.

F. Summary of consultations undertaken in formulating the proposed change and the internal governance process followed to approve it

MATCHNow has conducted informal consultations with several Subscribers and vendors and a handful of buy-side firms; we also conducted a conference call on June 22, 2021 to announce and explain the New Conditionals Offering in detail to all clients and other stakeholders. The reaction to the proposed New Conditionals Offering has been uniformly positive.

The proposed change was also fully reviewed, discussed, and approved by MATCHNow's senior management in or around early 2021.

G. If the proposed change will require subscribers or service vendors to modify their systems after implementation, the expected impact on the systems of subscribers and service vendors together with an estimate of the amount of time needed to perform the necessary work and how the estimated amount of time was deemed reasonable in light of the expected impact of the proposed change on MATCHNow, its market structure, subscribers, investors or the Canadian capital markets

For Subscribers and vendors, the work that will be needed to access the New Conditionals Offering is not insignificant. However, MATCHNow has provided-and will continue to provide-information and technical support for Subscribers and vendors throughout the migration process to make it is as smooth and as seamless as possible for them. In particular, in addition to numerous informal one-on-one consultations with clients, MATCHNow conducted a publicly-accessible conference call on June 22, 2021, focusing specifically on the New Conditionals Offering; this was in addition to two other conference calls (on February 17, 2021 and May 11, 2021, respectively) in which general technology migration matters were explained in great detail. Furthermore, transcripts of all three calls, as well as presentation materials used during the calls, are now available on the Cboe Technology Migration microsite (https://matchnow.cboe.com).

Moreover, MATCHNow plans to open a certification environment for Subscribers and vendors in early September 2021, which will continue to be available through January 2022. This will provide ample time, as well as the necessary technological support, to allow Subscribers and vendors to complete all necessary coding and testing of all new FIX connections and any other technological infrastructure necessary for the New Conditionals Offering prior to the planned launch date (February 1, 2022).

MATCHNow believes that a reasonable estimate of the time needed for Subscribers and vendors to modify their own systems in this way is approximately 90 days, including the certification (testing) process. We believe this estimate is reasonable based on MATCHNow's past experiences with technological changes to its ATS, as well as the experience of its corporate affiliates in the context of similar technological migrations.

H. Where the proposed change is not a Significant Change subject to Public Comment, the rationale for why the proposed Significant Change is not considered a Significant Change subject to Public Comment

Not applicable.

I. Alternatives considered

None.

J. If applicable, whether the proposed Significant Change would introduce a feature that currently exists in other markets or jurisdictions

As mentioned above, the New Conditionals Offering would introduce functionality and features that Cboe and BIDS currently offer market participants in the United States and Europe. This is true with regard to all six of the components of the proposed change described above, which all have parallels in the BIDS ATS (in the United States){10} and the existing Cboe LIS offering (in Europe).

In addition, we would submit that the Sponsored Access Model is not unlike the DEA model in a general sense, insofar as it is based on marketplace-provided automated risk controls, which are a feature of several marketplaces in Canada and around the world. A similar note applies to pegged orders in general, which exist in several marketplaces in Canada and internationally.

{1} BIDS Trading L.P. (BIDS) is an American ATS, registered with the U.S. Securities and Exchange Commission, and a corporate affiliate of MATCHNow (i.e., a wholly-owned subsidiary of Cboe).

{2} MATCHNow is also in the process of replacing its existing technology (the Legacy Technology) for all orders (not just Conditionals) with technology developed by Cboe and/or its corporate affiliates (the Cboe Technology) as part of MATCHNow's full integration into the Cboe family of global marketplaces (the Cboe Technology Migration). Additional information is available on the Cboe Technology Migration microsite (https://matchnow.cboe.com/). Please note, however, that this Notice of Proposed Change and Request for Comment focuses exclusively on the New Conditionals Offering.

{3} In the interests of efficiency, we are treating all six components as a single "Significant Change subject to Public Comment" to MATCHNow's Form F2 and, accordingly, each of Sections B. through J. below shall address all six components of the proposed change on a consolidated basis.

{4} MATCHNow will continue to offer its existing Conditionals functionality to Subscribers (i.e., its existing sell-side-to-sell-side interactions); however, if this proposed change is approved, MATCHNow will also offer buy-side-to-buy-side interactions, as well as mixed (buy-side-to-sell-side and sell-side-to-buy-side) interactions. The new platform will incorporate and support all of these types of interactions, as is explained in greater detail below. Moreover, while Sponsored Users will use the new Sponsored User Interface to enter and firm up Conditionals, Subscribers will continue to send and firm up Conditionals through a FIX connection, as is the case today. In addition, the MATCHNow ATS will continue to have separate books for receiving and processing Conditionals and firm orders, respectively; however, just as is the case today, these two books will have some limited degree of inter-connectedness (including with respect to firm orders that have been "opted-in" to match with Conditionals). For greater certainty, we would note that, to the extent that any particular feature or aspect of Conditionals is not expressly addressed herein, it is because that particular feature or aspect will undergo no change whatsoever as part of the proposed change.

{5} As is currently the case, every MATCHNow Subscriber will be required to be a Canadian registered, IIROC-approved securities dealer. That will not change if and when the New Conditionals Offering is approved and implemented.

{6} For example, U.S. asset managers (e.g., managers of registered mutual funds) could be granted access to the Sponsored User Interface by maintaining a proper client relationship with a U.S. registered broker-dealer, which is, in accordance with UMIR 1.1, a "foreign dealer equivalent" (or FDE), where that FDE is itself a client of a MATCHNow Subscriber (e.g., Merrill Lynch Canada Inc.). In such a scenario, the Subscriber would need to arrange for appropriate transparency through its own books and records, as well as in its set-up on the Subscriber Interface, such that the Conditionals that originate with an eligible U.S. asset manager are separately attributed to that firm for reporting and record-keeping purposes (even though the Legal Entity Identifier, or LEI, that would be reported to IIROC would be that of the FDE itself, in such a scenario). The Subscriber could accomplish this by establishing separate accounts for each of the individual Sponsored User clients that it wishes to sponsor by using the FDE as the intermediary and assigning a simple nomenclature for the FDE's eligible clients (e.g., one asset manager could be "USBD 1," and another could be "USBD 2," etc.). Such an arrangement would allow MATCHNow and its regulators to easily trace trading activity to the correct (foreign) Sponsored User ex post facto, should the need arise, without overcomplicating the day-to-day LEI reporting to IIROC that MATCHNow and its Subscribers will carry out in accordance with IIROC's upcoming "Client Identifier" rule amendments.

{7} Technically, one-to-one matching, as designed for the New Conditionals Offering, could involve more than one Conditional on one side-namely, where the Conditional on the other side could satisfy all of the contra liquidity sought on the first side. For example, two Conditionals to sell 50,000 shares of XYZ could match "one-to-one" with a Conditional to buy 100,000 shares of XYZ. This is different than the one-to-many matching that occurs on MATCHNow today, using the Legacy Technology, where one side need not be large enough to satisfy the totality of the contra side as a condition for engaging the (potential) matching (firm-up) process in the Conditionals book.

{8} Since the new minimum size thresholds for Conditionals (which will continue as is in the New Conditionals Offering) are the equivalent of the "large" thresholds for "dark" orders set out in UMIR 6.6, minimum price improvement is not required; hence, execution anywhere within the PNBBO range is permitted.

{9} For purposes of calculating the daily rate of firm-ups in connection with the application of the Conditionals Compliance Mechanism, a fall-down caused by a Sponsored User's decision not to firm up (or failure to firm up in time) will not be attributed to the sponsoring Subscriber, but rather, only to the Sponsored User in question. To put it another way, a Subscriber's firm-up (fall-down) rate will be based exclusively on its firm-up behaviour with respect to Conditionals entered by the Subscriber directly on the system (either on its own behalf or on behalf of a client, other than a client that is a Sponsored User accessing the Sponsored User Interface and entering Conditionals directly). Moreover, in the event the proposed change is approved, MATCHNow plans to study the firm-up behavior of Sponsored Users during the first 6 to 12 months following launch of the New Conditionals Offering and will propose future adjustments to the Conditionals Compliance Mechanism (including possibly lowering the number of firm-ups necessary to engage the mechanism for Sponsored Users), if warranted.

{10} See e.g., the latest BIDS Form ATS-N (available on the SEC website here).

Appendix: MATCHNow -- Conditionals Matching -- Examples

Example 1: no fall-down, no change in quantity, size priority

PNBBO: 10 x 10.02

|

Order |

Quantity |

Side |

Type |

Limit |

Time |

Broker |

Human/Electronic/Standing Liquidity |

|

|

|||||||

|

Conditional 1 |

50,000 |

SELL |

P Mid |

10.01 |

10:00 AM |

Broker A |

Electronic |

|

|

|||||||

|

Conditional 2 |

100,000 |

SELL |

P Mid |

10.01 |

11:00 AM |

Broker B |

Electronic |

|

|

|||||||

|

Conditional 3 |

75,000 |

BUY |

P Mid |

10.02 |

11:15 AM |

Broker C |

Electronic |

Result, step i:

Conditionals 2 and 3 each receive an invitation to firm up

Result, step ii:

Conditional 2 sends a Firm Order back to sell 100,000 shares @ 10.01

Conditional 3 sends a Firm Order back to buy 75,000 shares @ 10.02

Result, step iii:

Firm Order 2 gets a partial fill for 75,000 shares at 10.01

Firm Order 3 gets fully filled for 75,000 shares at 10.01

Example 2: no fall-down, no change in quantity, price priority

PNBBO: 10 x 10.02

|

Order |

Quantity |

Side |

Type |

Limit |

Time |

Broker |

Human/Electronic/Standing Liquidity |

|

|

|||||||

|

Conditional 1 |

50,000 |

SELL |

P Mid |

10.01 |

10:00 AM |

Broker A |

Electronic |

|

|

|||||||

|

Conditional 2 |

100,000 |

SELL |

P Mid |

10.02 |

11:00 AM |

Broker B |

Electronic |

|

|

|||||||

|

Conditional 3 |

75,000 |

BUY |

P Far |

10.02 |

11:15 AM |

Broker C |

Electronic |

Result, step i:

Conditionals 1 and 3 each receive an invitation to firm up

Result, step ii:

Conditional 1 sends a Firm Order back to sell 50,000 shares @ 10.01

Conditional 3 sends a Firm Order back to buy 75,000 shares @ 10.02

Result, step iii:

Firm Order 1 gets fully filled for 50,000 shares at 10.01

Firm Order 3 gets a partial fill for 50,000 shares at 10.01

Example 3: no fall-down, change in quantity, price priority, human vs. electronic

PNBBO: 10 x 10.02

|

Order |

Quantity |

Side |

Type |

Limit |

Time |

Broker |

Human/Electronic/Standing Liquidity |

|

|

|||||||

|

Conditional 1 |

50,000 |

SELL |

P Far |

None |

10:00 AM |

Broker A |

Electronic |

|

|

|||||||

|

Conditional 2 |

100,000 |

SELL |

P Mid |

10.02 |

11:00 AM |

Broker B |

Electronic |

|

|

|||||||

|

Conditional 3 |

75,000 |

BUY |

P Near +1 |

None |

11:15 AM |

Not yet selected |

Human |

Result, step i:

Conditional 3 receives an invitation to firm up first (30s max)

Result, step ii:

Conditional 3 sends a Firm Order back to buy 50,000 shares (selecting Broker C) @ Peg Near +1

Result, step iii:

Conditional 1 receives an invitation to firm up second (1s max)

Result step iv:

Conditional 1 sends a Firm Order back to sell 40,000 shares @ Peg Mid

Result, step v:

Firm Order 1 gets fully filled for 40,000 shares at 10.01

Firm Order 3 gets a partial fill for 40,000 shares at 10.01

Example 4: no fall-down, no change in quantity, broker priority, standing liquidity vs. electronic

PNBBO: 10 x 10.02

|

Order |

Quantity |

Side |

Type |

Limit |

Time |

Broker |

Human/Electronic/Standing Liquidity |

|

|

|||||||

|

Conditional 1 |

50,000 |

SELL |

P Mid |

None |

10:00 AM |

Broker A |

Electronic |

|

|

|||||||

|

Conditional 2 |

100,000 |

SELL |

P Mid |

None |

11:00 AM |

Broker B |

Electronic |

|

|

|||||||

|

Firm Order 3 (Opt-In Active) |

75,000 |

BUY |

P Mid |

None |

11:15 AM |

Broker A |

Opted-In Standing Liquidity |

Result, step i:

Conditional 1 receives an invitation to firm up

Result, step ii:

Conditional 1 sends a Firm Order back to sell 50,000 shares @ Peg Mid

Result, step iii:

Firm Order 1 gets fully filled for 50,000 shares at 10.01

Firm Order 3 gets a partial fill for 50,000 shares at 10.01

Example 5: fall-down, no change in quantity, price priority

PNBBO: 10 x 10.02

|

Order |

Quantity |

Side |

Type |

Limit |

Time |

Broker |

Human/Electronic/Standing Liquidity |

|

|

|||||||

|

Conditional 1 |

50,000 |

SELL |

P Mid |

10.00 |

10:00 AM |

Broker A |

Electronic |

|

|

|||||||

|

Conditional 2 |

100,000 |

SELL |

P Mid |

10.02 |

11:00 AM |

Broker B |

Electronic |

|

|

|||||||

|

Conditional 3 |

75,000 |

BUY |

P Far |

10.01 |

11:15 AM |

Broker C |

Electronic |

Result, step i:

Conditional 1 receives an invitation to firm up

Conditional 3 receives an invitation to firm up

Result, step ii:

Conditional 1 sends a Firm Order back to sell 50,000 shares @ 10.02

Conditional 3 does not send in a Firm Order

Result, step iii:

No trade occurs

Broker C has a fall-down registered against it in the Conditionals Compliance Mechanism

Example 6: no fall-down, no changes in quantity, multiple contra invites

PNBBO: 10 x 10.02

|

Order |

Quantity |

Side |

Type |

Limit |

Time |

Broker |

Human/Electronic/Standing Liquidity |

|

|

|||||||

|

Conditional 1 |

50,000 |

SELL |

P Mid |

10.01 |

10:00 AM |

Broker A |

Electronic |

|

|

|||||||

|

Conditional 2 |

100,000 |

SELL |

P Mid |

10.01 |

11:00 AM |

Broker B |

Electronic |

|

|

|||||||

|

Conditional 3 |

150,000 |

BUY |

P Mid |

10.02 |

11:15 AM |

Broker C |

Electronic |

Result, step i:

Conditionals 1, 2, and 3 each receive an invitation to firm-up

Result, step ii:

Conditional 1 sends a Firm Order back to sell 50,000 shares @ 10.01

Conditional 2 sends a Firm Order back to sell 100,000 shares @ 10.01

Conditional 3 sends a Firm Order back to buy 150,000 shares @ 10.02

Result, step iii:

Firm Order 1 gets fully filled for 50,000 shares at 10.01

Firm Order 2 gets fully filled for 100,000 shares at 10.01

Firm Order 3 gets a partial fill for 100,000 shares and a complete fill for 50,000 shares, both at 10.01

Example 7: no fall-down, change in quantity, multiple contra invites, size priority

PNBBO: 10 x 10.02

|

Order |

Quantity |

Side |

Type |

Limit |

Time |

Broker |

Human/Electronic/Standing Liquidity |

|

|

|||||||

|

Conditional 1 |

50,000 |

SELL |

P Mid |

10.01 |

10:00 AM |

Broker A |

Electronic |

|

|

|||||||

|

Conditional 2 |

100,000 |

SELL |

P Mid |

10.01 |

11:00 AM |

Broker B |

Electronic |

|

|

|||||||

|

Conditional 3 |

150,000 |

BUY |

P Mid |

10.02 |

11:15 AM |

Broker C |

Electronic |

Result, step i:

Conditionals 1, 2, and 3 each receive an invitation to firm-up

Result, step ii -- Brokers A and B both firm up before Broker C:

Conditional 1 sends a Firm Order back to sell 50,000 shares @ 10.01

Conditional 2 sends a Firm Order back to sell 100,000 shares @ 10.01

Conditional 3 sends a Firm Order back to buy 100,000 shares @ 10.02

Result, step iii:

Firm Order 1 gets no fill

Firm Order 2 gets fully filled for 100,000 shares at 10.01

Firm Order 3 gets fully filled for 100,000 shares at 10.01

Example 8: no fall-down, change in quantity, multiple contra invites, time priority

PNBBO: 10 x 10.02

|

Order |

Quantity |

Side |

Type |

Limit |

Time |

Broker |

Human/Electronic/Standing Liquidity |

|

|

|||||||

|

Conditional 1 |

50,000 |

SELL |

P Mid |

10.01 |

10:00 AM |

Broker A |

Electronic |

|

|

|||||||

|

Conditional 2 |

100,000 |

SELL |

P Mid |

10.01 |

11:00 AM |

Broker B |

Electronic |

|

|

|||||||

|

Conditional 3 |

150,000 |

BUY |

P Mid |

10.02 |

11:15 AM |

Broker C |

Electronic |

Result, step i:

Conditionals 1, 2, and 3 each receive an invitation to firm-up

Result, step ii -- Broker C firms up first, then Broker A, then Broker B:

Conditional 1 sends a Firm Order back to sell 50,000 shares @ 10.01

Conditional 2 sends a Firm Order back to sell 100,000 shares @ 10.01

Conditional 3 sends a Firm Order back to buy 100,000 shares @ 10.02

Result, step iii:

Firm Order 1 gets fully filled for 50,000 shares at 10.01

Firm Order 2 gets a partial filled for 50,000 shares at 10.01

Firm Order 3 gets fully filled for 100,000 shares at 10.01