OSC Staff Notice 11-793 Hierarchy of Regulatory Instruments in Securities Law

OSC Staff Notice 11-793 Hierarchy of Regulatory Instruments in Securities Law

OSC STAFF NOTICE 11-793 HIERARCHY OF REGULATORY INSTRUMENTS IN SECURITIES LAW

In November 2018 the Ontario Securities Commission (the Commission) created a burden reduction task force to refocus our efforts on reducing unnecessary regulatory burden. Consultations were launched on January 14, 2019, with the publication of OSC Staff Notice 11-784 Burden Reduction.

During the public consultations, several market participants expressed a concern that the difference between rules, or legal requirements, and guidance is not always clear. This staff notice clarifies the differences between each regulatory instrument and serves as an informational resource for Commission regulatory staff and market participants.

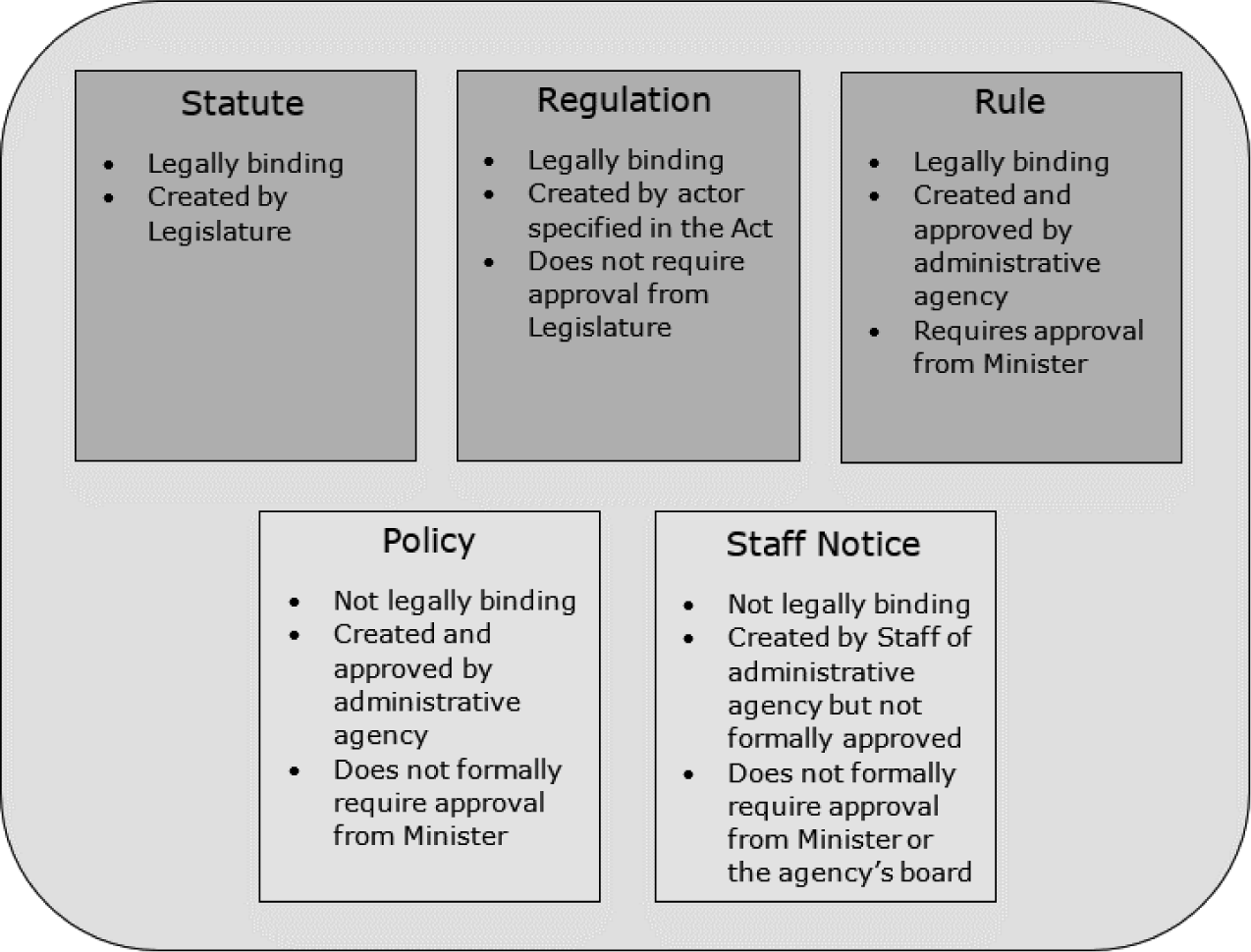

Securities regulators deploy several different types of instruments to govern the conduct of regulated persons and entities. However, not all regulatory instruments have the same legal authority. As illustrated in the diagram below, statutes, regulations, and rules are all legally binding. The requirements set out in these instruments are mandatory and failure to comply may result in enforcement action. Conversely, guidance published by the Commission or staff of the Commission (Staff) is instructive in nature and is not legally binding.

Statutes & Regulations

The Commission administers the Securities Act (Ontario) and its General Regulation, as well as the Commodity Futures Act (Ontario) and its General Regulation. These provincial statutes and regulations are legally binding.

Statute

A statute or "Act" is a law passed by the provincial Legislature. The legislative process in Ontario generally requires:

• a first reading where a bill is introduced, and its purpose is explained;

• a second reading where members of the Legislature debate and vote on the bill;

• a committee examination of the bill clause-by-clause;

• a report to the House and order for a third reading;

• a third reading where members vote on whether the bill will be passed; and

• royal assent where the Lieutenant Governor signs the bill.

A bill's provisions can come into force on royal assent, on a specified date, or on proclamation. Some bills are never proclaimed and therefore never become law.

Regulation

A regulation is a law that is made by a person or body whose authority to make such law is set out in a statute. The authority to make regulations is typically provided to the Lieutenant Governor in Council. However, in some statutes, this authority is given to a Minister or to another government official or body.

Regulations are created by the Ontario government ministry that is responsible for administering the parent statute, and are passed by Order in Council. Approval from the Legislature is not required for the creation of a new regulation.

Rules

The Legislature has given the Commission explicit authority to make rules in subject areas enumerated in the Securities Act.{1} Rules are drafted by the Commission, are often required to be published for public comment, and require Ministerial approval.{2}

Because securities regulation is provincial, rules are made under each province or territory's Securities Act or equivalent. In the rare instance where only the Commission makes a rule, this is called a local rule.

More commonly, Canadian securities regulators harmonize rules. As a result, most rules appear as national instruments, which apply to all Canadian jurisdictions uniformly, subject to local carveouts. There are also multilateral instruments, which apply only in the subscribing jurisdictions. National instruments and multilateral instruments are essentially consolidations of local rules.

Before the Commission publishes for comment a new rule (or an amendment to an existing rule) dealing with a novel or complex issue, it may publish a consultation paper and request comments. This initial consultation enables the Commission to better understand the need for the new rule or amendment and the potential market impacts.

Following the consultation period, Staff drafts the proposed rule or amendment and the Commission publishes it for comment, unless an exception to the publication requirement applies.{3} In Ontario, the publication must include:

• the proposed rule;

• a statement of the substance and purpose of the proposed rule;

• a summary of the rule;

• a discussion of all alternatives to the proposed rule that were considered and reasons for not proposing their adoption;

• a qualitative and quantitative analysis of the anticipated costs and benefits of the rule; and

• a reference to the authority under which the rule is to be made.{4}

The public is provided at least 90 days to consider a proposed rule and to submit comments to the Commission. If the Commission makes material amendments to a proposed rule after the initial comment period, the Commission must republish the proposed rule for a second comment period.{5}

For a rule to come into force, the Commission must approve the rule in its final form and deliver it to the Minister of Finance for review.{6} Within 60 days after a rule is delivered to the Minister, the Minister may approve or reject the rule, or return it to the Commission for further consideration.{7} If the Minister does not approve, reject or return the rule, it becomes effective 15 days following the conclusion of the 60-day period unless there is a later effective date specified in the rule.{8} The Commission must publish every rule that comes into force in The Ontario Gazette and in its Bulletin.

Guidance

The Commission produces two types of non-binding guidance: policies and staff notices. These are intended to be instructive and to provide regulated persons and entities with insight into how the requirements are applied.

Like rules, policies and staff notices may apply at the national or local level. National policies and companion policies to a national instrument apply to all Canadian jurisdictions. The Commission can issue local policies that apply only within Ontario.

Regulated persons and entities may also be guided by decisions of the OSC Tribunal, although these decisions are not formally binding on persons or entities who were not parties to the proceeding before the Tribunal.

Policies

The Securities Act authorizes the Commission to adopt policies of a non-binding nature, including the Commission's interpretations of rules.{9} A policy is generally used to address issues that occur frequently or have a broad impact on market participants.

Unlike staff notices, policies must be approved by the Commission and must be published for comment. Publication is not required if the proposed policy would make no material substantive change to an existing policy.{10} Following the notice and comment process, if applicable, the Commission may adopt a proposed policy. While policies do not formally require Ministerial approval, the Commission may consult the Minister when a new policy is proposed.

Unlike rules, policies cannot be prohibitive or mandatory in character. Policies inform market participants of: (a) how the Commission may exercise its discretionary authority, (b) how the Commission interprets Ontario securities law, (c) the practices followed by the Commission in performing its duties under Ontario securities law, and (d) other matters that are not legislative in nature.{11} Policies are also used to communicate the Commission's views of what may be in the public interest regarding a given issue.{12}

Staff Notices

Staff notices are documents issued by the Commission that communicate Staff's views and expectations of operational reviews, emerging issues and trends, and market participant conduct. Staff views are subject to change as Staff are confronted with different factual circumstances. Accordingly, views expressed in a staff notice do not necessarily represent the views of the Commission.

Staff notices are not approved by the Commission and need not be published for public comment. However, Staff notices are often discussed with the Commission and may incorporate feedback from Commissioners. Like policies, staff notices do not require Ministerial approval.

Staff notices generally describe: (a) factors relevant to the exercise of a discretion by Staff, (b) the manner in which statutes, regulations, rules or policies are interpreted by Staff, or (c) the practices generally followed by Staff in the performance of their responsibilities.

The annual Corporate Finance Branch Report is an example of a staff notice that provides issuers with guidance on trends and issues identified during compliance reviews. Branch reports also articulate Staff's expectations and interpretation of regulatory requirements and outline the Branch's operational and policy work.

Contact Information

If you have questions about this notice, please contact:

Robert Galea

Acting Associate General Counsel

General Counsel's Office

Tegan Raco

Legal Counsel

General Counsel's Office

{1} Securities Act, RSO 1990, c S.5, s 143(1) [Securities Act]. Note, the Commodity Futures Act provides the Commission with similar rule-making authority and process requirements.

{2} Securities Act, ss 143.2-143.6.

{3} Securities Act, s 143.2(5).

{4} Securities Act, s 143.2(2).

{5} Securities Act, s 143.2(7).

{6} Securities Act, s 143.3(1).

{7} Securities Act, s 143.3(3).

{8} Securities Act, s 143.4.

{9} Securities Act, s 143.8.

{10} Securities Act, s 143.8(6).

{11} Securities Act, s 143.8(1). Ontario Securities Commission Policy 11-601 is an example of a policy that addresses matters that are not legislative in nature. This local policy outlines organizational and procedural practices of the Securities Advisory Committee (a group of practicing securities lawyers who provide advice to the Commission and Staff).

{12} National Policy 62-202 is an example of how securities regulators communicate public interest considerations. This policy recognizes that, during a take-over bid, the interests of management may differ from those of shareholders of the target company and provides guidance on when defensive tactics may be subject to scrutiny by securities regulators.