Notice of Changes to Companion Policy 24-102 Clearing Agency Requirements

Notice of Changes to Companion Policy 24-102 Clearing Agency Requirements

Notice of Changes to Companion Policy 24-102 Clearing Agency Requirements

June 3, 2016

Introduction

On December 3, 2015, the Canadian Securities Administrators (the CSA or we) published National Instrument 24-102 Clearing Agency Requirements (Instrument) and Companion Policy 24-102CP to National Instrument 24-102 Clearing Agency Requirements (Companion Policy) in final adopted form. Subject to certain transition provisions, the Instrument and Companion Policy became effective in most CSA jurisdictions on February 17, 2016.{1}

The main objective of the Instrument is to impose requirements on recognized clearing agencies that operate as a central counterparty (CCP), central securities depository (CSD) or securities settlement system (SSS). The requirements are based on international standards applicable to a financial market infrastructure (FMI), which are described in the April 2012 report Principles for financial market infrastructures (as the context requires, the "PFMIs" or "PFMI Report") published by the Committee on Payments and Market Infrastructures (CPMI){2} and the International Organization of Securities Commissions (IOSCO).{3} Implementation of the international standards is intended to enhance the safety and efficiency of clearing agencies, limit systemic risk, and foster financial stability.

The CSA also published on December 3, 2015, for a 60-day comment period, proposed amendments to the final adopted Companion Policy. The proposed amendments consist of new supplementary guidance (Recovery Guidance) jointly developed by the Bank of Canada and CSA (collectively, the Canadian authorities) on FMI recovery and orderly wind-down planning. The Recovery Guidance is intended to provide additional clarity regarding recovery and orderly wind-down plans for domestically-based, recognized clearing agencies that are also overseen by the Bank of Canada. Canadian authorities expect such clearing agencies to meet the standards related to recovery and orderly wind-down outlined in the PFMI Report. The PFMI Report is supplemented by the October 2014 CPMI-IOSCO report Recovery of financial market infrastructures (Recovery Report), which further interprets the standards and guidance in the PFMI Report on the subject matter.{4}

The comment period for the Recovery Guidance closed on February 1, 2016. The Canadian authorities have made some modifications to the Recovery Guidance, as a result of both the comments received and emerging international trends in FMI recovery planning and FMI resolution frameworks. None of the modifications are considered material changes. Consequently, we are adopting the Recovery Guidance today as part of the Joint Supplementary Guidance (JSG) set forth in Annex 1 to the Companion Policy. In addition, further non-material revisions are being made to other aspects of the JSG, which are intended to simplify and enhance consistency among all the JSG. We have included a blacklined version of the revised Companion Policy in Annex C to this Notice, as well as a clean version of the Companion Policy in Annex D to this Notice.{5} The material is also available on websites of CSA jurisdictions, including:

www.lautorite.qc.cawww.albertasecurities.comwww.bcsc.bc.cawww.gov.ns.ca/nsscwww.fcnb.cawww.osc.gov.on.cawww.fcaa.gov.sk.cawww.msc.gov.mb.ca

This Notice includes the following Annexes:

• Annex A: List of commenters on the Recovery Guidance

• Annex B: Summary of comments and CSA responses

• Annex C: Blacklined version of Annex 1 to final Companion Policy 24-102 Clearing Agency Requirements

• Annex D: Clean version of Annex 1 to final Companion Policy 24-102 Clearing Agency Requirements

Substance and purpose of Recovery Guidance

The Recovery Guidance is intended to provide additional clarity to the PFMIs and the Recovery Report regarding recovery and orderly wind-down plans in the Canadian context. It clarifies the expectations of the Canadian authorities regarding key components of recovery plans; the selection and application of recovery tools; additional considerations for recovery planning; implementation of recovery plans; review of recovery plans; orderly wind-down; and practical aspects of designing a recovery plan, such as the organization and structure of content.

Comments received on Recovery Guidance and responses

The Canadian authorities received four comment letters. We have considered these comments and thank all the commenters. We have set out the names of the commenters in Annex A, and summarized their comments, together with our responses, in Annex B to this Notice.{6} Certain commenters suggested delaying the finalization of the Recovery Guidance. The Canadian authorities do not believe that delaying the Recovery Guidance is appropriate. The Recovery Guidance being published today is intended to help clearing agencies develop recovery plans before the end of 2016.

In developing the Recovery Guidance, the Canadian authorities have been influenced by the comments received through the consultation, the evolving international interpretations of the standards and guidance on FMI recovery planning set out in the PFMIs and Recovery Report, and ongoing international policy work related to FMIs and financial stability.

Developments in these areas are having, and will continue to have, a significant global impact on FMI recovery planning and resolution frameworks. To ensure that recovery planning in the Canadian context remains in step with this evolving landscape, Canadian authorities have relaxed some of the previously restrictive language of the Recovery Guidance. Nonetheless, the principled intent of the guidance, in particular its strong emphasis on systemic stability, has not changed and is reinforced by the adjustments made. Specifically:

• references to caps on participant exposures are replaced with language echoing existing Canadian requirements that exposures be limited to fixed or determinable amounts;

• additional emphasis is added to stress the need for measureable, manageable and controllable exposures for participants;

• language is added to stress that Canadian authorities will consider the impact of each successive round of recovery tool application with increasing focus on systemic stability; and

• where certain types of tools were not recommended in the draft Recovery Guidance, language has been adjusted to instead place the onus on the FMIs to justify their use in recovery, where applicable.

It is important to note that these and other proposed changes are not intended to be a departure from the principled approach to recovery, nor do they represent a lesser focus on financial stability on the part of the Recovery Guidance or Canadian authorities. Rather they adapt the Recovery Guidance to be flexible in the fast-evolving area of FMI financial stability, and provide the FMIs, their stakeholders, and Canadian authorities the ability to respond within the principled approach that has been adopted.

Effective Date

The revised Companion Policy, which includes the Recovery Guidance, is effective immediately.

Questions

Please refer any of your questions to the CSA staff listed below:

Antoinette LeungManager, Market RegulationOntario Securities CommissionTel: 416-593-8901Email: [email protected]Maxime ParéSenior Legal Counsel, Market RegulationOntario Securities CommissionTel: 416-593-3650Email: [email protected]Oren WinerLegal Counsel, Market RegulationOntario Securities CommissionTel: 416-593-8250Email: [email protected]Michael BradySenior Legal CounselBritish Columbia Securities CommissionTel: 604-899-6561Email: [email protected]Doug MacKayManager, Market and SRO OversightCapital Markets RegulationBritish Columbia Securities CommissionTel: 604-899-6609Email: [email protected]Kathleen BlevinsSenior Legal CounselAlberta Securities CommissionTel: 403-297-4072Email: [email protected]Paula WhiteDeputy Director, Compliance and OversightManitoba Securities CommissionTel: 204-945-5195Email: [email protected]Claude GatienDirector, Clearing HousesAutorité des marchés financiersTel: 514-395-0337, ext. 4341Toll free: 1-877-525-0337Email: [email protected]Martin PicardSenior Policy Advisor, Clearing HousesAutorité des marchés financiersTel: 514-395-0337, ext. 4347Toll free: 1-877-525-0337Email: [email protected]Liz KutarnaDeputy Director, Capital Markets, Securities DivisionFinancial and Consumer Affairs Authority of SaskatchewanTel: 306-787-5871Email: [email protected]Ella-Jane LoomisSenior Legal Counsel, SecuritiesFinancial and Consumer Services Commission (New Brunswick)Tel: 506-658-2602Email: [email protected]

{1} In Saskatchewan, the effective date was February 19, 2016.

{2} Prior to September 2014, CPMI was known as the Committee on Payment and Settlement Systems (CPSS).

{3} The PFMI Report is available on the Bank for International Settlements' website (www.bis.org) and the IOSCO website (www.iosco.org).

{4} The Recovery Report is available on the Bank for International Settlements' website (www.bis.org) and the IOSCO website (www.iosco.org).

{5} To clarify, the revisions made to the Companion Policy with this Notice are strictly to the JSG set forth in Annex 1 to the Companion Policy. Therefore, Annexes C and D to this Notice reproduce the JSG in Annex 1 to the Companion Policy, but not the entirety of the Companion Policy. In addition, while the Recovery Guidance is new text added today to the JSG (new Box 3.1), we have only blacklined in Annex C the changes made to the proposed Recovery Guidance published for comment on December 3, 2015. Other blacklined changes in Annex C made to other aspects of the JSG reflect the non-material revisions that were made to such JSG (i.e., changes to Boxes 2.1, 2.2, 5.1, 7.1, 15.1, 16.1, and 23.1 -- also please note that Boxes 2.1 and 2.2 are merged into a single Box 2.1).

{6} We note, however, that comments that were not reasonably within scope of the consultation on the Recovery Guidance are not included in Annex B.

ANNEX A

List of Commenters on Recovery Guidance (as published for comment on December 3, 2015)

Commenters:

Canadian Bankers AssociationCLS BankTMX Group LimitedIGM Financial Group

ANNEX B

Summary of Comments on Proposed Changes to Companion Policy 24-102 Clearing Agency Requirements and CSA Responses

|

1. Theme/question |

2. Summary of comments |

3. Responses |

|

|

|

|||

|

General Issues |

|||

|

|

|||

|

Principles-based approach |

One commenter expresses support for a principles-based approach to adopting the PFMIs, but views the proposed guidance -- with prescriptive language and scope -- as a departure from this approach. |

The Canadian authorities have amended the language regarding the use of certain recovery tools. The overarching purpose of the guidance is to provide additional clarity in the Canadian context to the PFMIs and the Recovery Report regarding a clearing agency's recovery and orderly wind-down plans. The guidance clarifies the expectations of the Canadian authorities regarding key aspects of recovery plans. |

|

|

|

|||

|

International consistency |

Two commenters express the need to maintain international consistency with recovery guidance, and encourage Canadian regulators to consult with the international community and to review the proposed guidance in light of other regulators implementing their recovery regimes. |

While being mindful of the purpose described above, we agree that we should maintain international consistency in this area. See also the cover Notice. |

|

|

|

|||

|

|

One commenter further suggests delaying implementation until U.S. and EU regulators have finalized their guidance on the issue. |

With respect to delaying the guidance, we disagree. See the cover Notice. |

|

|

|

|||

|

Application and level playing field concerns |

A commenter seeks clarity with respect to the meaning and implications of the term "designated domestic FMI" used to describe the scope of application of the guidance. In particular, the commenter seeks clarification as to whether foreign-based FMIs designated by the Bank of Canada as systemically important are, or should be, exempt from compliance. |

Section 3.1 of the Companion Policy states that the JSG in Annex 1 is applicable only to "recognized domestic clearing agencies that are also overseen by the [Bank of Canada]". By domestic, we mean based in Canada. |

|

|

|

|||

|

|

One commenter argues that applying the guidance only to designated domestic FMIs would lead to an unlevel playing field with designated foreign FMIs. |

While the JSG in Annex 1 to the Companion Policy is applicable only to recognized domestic clearing agencies that are also overseen by the Bank of Canada, we would expect a foreign-based recognized clearing agency that is also designated by the Bank of Canada to be subject to home-jurisdiction requirements that achieve an equivalent "outcome". If, hypothetically, a foreign-based clearing agency carrying on business in a local jurisdiction were based in a home jurisdiction that did not have similar regulatory expectations with respect to clearing agency recovery planning and we felt there was a "gap" in this area, CSA regulators could impose requirements analogous to the JSG through terms and conditions in a recognition order. |

|

|

|

|||

|

Communication and escalation |

One commenter agrees that setting a recovery scenario communication plan in advance may be appropriate, but emphasizes that a contextual approach is required to achieve balance between communication and maintaining public confidence in the markets. The commenter concludes that, while communication between regulators and an FMI's Boards of Directors is appropriate, plans ought not to require communications with any particular stakeholder. |

We are of the view that the current wording of the guidance strikes an appropriate balance between transparency and public confidence. Therefore, we have not modified the text on this matter. A communications protocol between a clearing agency and its overseers can be separately agreed-upon. |

|

|

|

|||

|

|

Another commenter expresses concern that the language in the guidance suggests that an FMI should obtain prior approval before implementing its recovery plan or a particular tool, which could hinder the quick response that a crisis may require. The commenter proposes that consultation with regulatory authorities regarding recovery plans should be required only where reasonably practicable, and that the guidance should only refer to a communication protocol to be agreed upon separately. |

The guidance is clear that a clearing agency should inform or consult with Canadian authorities when taking recovery actions. We consider it critical to be informed to ensure that the clearing agency's decisions take account of potential systemic risk consequences. The guidance does not require prior regulatory approval before triggering the recovery plan and applying a particular recovery tool. |

|

|

|

|||

|

Transparency |

One commenter argues that FMIs should be required to make their recovery plans fully available to members. An FMI wishing to keep any part of a plan confidential should be required to justify the non-disclosure. Similarly, the commenter advocates that legal opinions on the application of recovery tools solicited by the FMI be made available to its participants. |

Recovery plans would normally be adopted through changes to the clearing agency's rulebook, and therefore be subject to a transparent comment and approval process. Thus, a clearing agency's recovery actions taken under its recovery plan should not surprise participants. In addition, the guidance already stresses that recovery plans must be drafted with a high degree of legal certainty, but it should be left to the clearing agency and its participants to decide how best to ensure this certainty is communicated and ensured. |

|

|

|

|||

|

Categorization and choice of recovery tools |

One commenter believes that the guidance ought to define "recovery tool" in a way that accounts for the heterogeneity of FMIs. This commenter also emphasizes the importance of distinguishing between recovery and business continuity management so that recovery plans address the correct objectives. |

The guidance provides flexibility in the selection of recovery tools to account for the heterogeneity of clearing agencies in terms of structure and service offering. We have amended the guidance to clarify that a recovery plan aims to facilitate recovery from threats to a clearing agency's viability and financial strength, while a business continuity plan (BCP) facilitates recovery mainly from operational events, but the two are complementary. For example, when an operational incident results in financial losses that threaten the clearing agency's viability, both the BCP and the (financial) recovery plan should be triggered so that they complement each other. |

|

|

|

|||

|

|

One commenter criticizes the "recommended" / "non-recommended" binary, citing its inconsistency with international guidance, and suggests softening "non-recommended tools" to "other tools." By discouraging certain tools, the commenter argues that Canadian FMIs may end up worse equipped to manage recovery. |

We have amended the language in the guidance by replacing the description of tools that are "not recommended" with "tools requiring further justification". |

|

|

|

|||

|

|

The same commenter further argues that the guidance should appreciate that continued use of pre-recovery tools in combination with recovery tools may be necessary. |

We agree that the continued use of pre-recovery tools in combination with recovery tools may be necessary, but the text in the guidance already encourages clearing agencies to do so: the guidance states that "tools are often already found in the pre-recovery risk-management frameworks of clearing agencies. Canadian authorities encourage their use for recovery as well, provided they are in keeping with the criteria for effective recovery tools as found in the Recovery Report and in this guidance." |

|

|

|

|||

|

Effectiveness of recovery tools |

One commenter offers support for the adoption of measurable, manageable, controllable and capped recovery tools, and the discouragement of destabilizing tools, but suggests that FMI recovery plans should include criteria that measure the effectiveness of each tool so that it can be determined whether the recovery process is effective. |

The guidance already establishes the following mechanisms to limit the risks of ineffective plans and undue risk to clearing agency participants: |

|

|

|

|||

|

|

|

1) |

Recovery plans should be reviewed, including an assessment of recovery tools, at least annually and following certain events, such as significant changes to market conditions, the clearing agency's business model, or risk exposures; |

|

|

|||

|

|

|

2) |

We note the importance of consulting with regulators when applying recovery tools; and |

|

|

|||

|

|

|

3) |

Clearing agencies should keep in mind the objective of minimizing the tools' negative impacts on participants, the clearing agency, and the broader financial system. |

|

|

|||

|

Application of recovery tools to tiered participants |

A commenter states that ensuring recovery tool inclusiveness of all types and tiers of participants is imperative and that, where inclusiveness cannot be attained, that compensation to participating members is essential. |

We see the lack of a direct contractual relationship between an indirect participant and the clearing agency as a challenge. Since indirect participant involvement depends on such contractual relationship (as well as, in the case of a CCP, the segregation and portability arrangements of the CCP), the guidance cannot expressly recommend the involvement of indirect participants. To this end, the guidance has been adjusted to note that recovery plans should respect the clearing agency's frameworks for tiered participation, segregation and portability. Also, the guidance notes that, to the extent that the costs of recovery are shared less equally under some tools (e.g., VMGH), clearing agencies could, if it is financially feasible, consider post-recovery actions to restore fairness where participants have been disproportionately affected. |

|

|

|

|||

|

Approval vs. endorsement of recovery plan by Board of Directors |

A commenter notes inconsistent language between the guidance and the Recovery Report. The latter requires recovery plans to be only endorsed by an FMI's Board of Directors or equivalent body. The guidance requires formal approval by the Board. |

Consistent with the Recovery Report (para. 2.3.3), we view recovery planning as an extension of the clearing agency's regular risk management. As a result, the Canadian authorities believe that there is high value in requiring that recovery plans be approved, rather than just endorsed, by the clearing agency's Board of Directors, in order to incentivize responsible recovery planning. |

|

|

|

|||

|

Stress testing |

One commenter encourages establishing minimum stress testing standards and scenarios across CCPs, the results of which ought to be shared with members as part of the FMI's recovery plan. |

We note that standardized stress testing is out of scope of this guidance. Currently, the CPMI-IOSCO is examining stress testing as part of its stock-take exercise related to CCP resilience. We will monitor this work and any related developments, and assess if any Canadian specific guidance would be necessary. |

|

|

|

|||

|

Recovery tools and related issues |

|||

|

|

|||

|

Cash calls |

One commenter argues that limiting the maximum cumulative value of rounds for mandatory cash calls per default event and per successive default within a period of time would allow members to prepare in advance and increase predictability. |

The draft guidance noted that caps on dollar amounts should be applied and the number of rounds limited. While our position on cash calls has not changed, we believe the guidance needs to be aligned with international guidance on, and interpretations of, full allocation of losses and shortfalls for clearing agencies. As a result, we have softened the language by emphasizing the need to have measurable, manageable and controllable exposures. Clearing agencies should ensure that participant exposures to cash calls must be determinable, if not fixed, while respecting the requirements of the PFMIs to permit full allocation in recovery. The guidance has been further revised to emphasize that authorities will monitor the application of each successive round of cash calls with increased focus on systemic stability. |

|

|

|

|||

|

Variation margin gains haircutting (VMGH) |

One commenter views limiting the number of rounds of VMGH available to a recovering FMI as overly restrictive. The commenter argues these limits may lead to larger cash calls, which could increase uncertainty at times of crisis. Further, this commenter argues that implementing a cap (on either time or amount) may undermine the effectiveness of this tool, and is inconsistent with international practice. Another commenter suggests that VMGH should apply to all tiers of participants, and that (contrary to the comment above) a dollar limit would be more effective than a time limit in enabling members to prepare for a major default event. |

We recognize a need to acknowledge the international interpretation of the PFMI definition of full allocation while balancing participant concerns regarding predictable and manageable recovery tools. While unfettered application of VMGH is not recommended, lifting caps on VMGH is not prohibited as participant exposures to each round can be measured with reasonable confidence. In this context, cautionary language has been added to the guidance to signal to clearing agencies that participant exposures must be manageable, measurable and controllable. Moreover, the guidance highlights the need for authorities to be kept informed to allow them to monitor the application of each successive round of VMGH with increased focus on systemic stability. See also our response above regarding applying tools to all tiers of participants. |

|

|

|

|||

|

Payment haircutting |

Two commenters felt that the guidance did not provide an exhaustive compendium of recovery tools-for example, there are few tools described for non-CCPs other than cash calls and contract tear-up. One commenter recommends considering "payment haircutting" more broadly than VMGH, pointing to Canadian and Australian precedents for use of payment haircutting in recovery situations. |

The guidance welcomes clearing agencies to include other recovery tools, where applicable, in their recovery plans, provided that they are in keeping with the criteria for the recommended tools. Language has been added to clarify that clearing agencies can also design recovery tools not explicitly listed in the guidance, where system-specific recovery needs necessitate. We consider the concept of "payment haircutting" as too vague to be explicitly included in the guidance. |

|

|

|

|||

|

Voluntary contract allocation/tear up |

One commenter supports voluntary contract allocation or tear-ups but notes that it may be difficult or impossible to apply to indirect participants. The commenter also wishes to ensure that, for tear ups, corresponding accounting/netting and capital criteria will be consistent with the Canadian bank capital framework. |

With regard to indirect participants, the guidance notes the allocation of losses and shortfalls in recovery should respect the clearing agency's frameworks for tiered participation, segregation and portability. The guidance also requires recovery plans to have a strong legal basis for the relevant processes and procedures with voluntary tools to manage participant expectations. |

|

|

|

|||

|

Recovery from non-default losses |

One commenter encourages Canadian authorities to strengthen the language surrounding the principle that FMIs should rely on FMI-funded resources to address recovery from non-default-related losses. The commenter proposes that the guidance explicitly state that shareholders and not members should bear all of the non-default-related losses unless members voluntarily contribute (e.g. in exchange for creditor/shareholder rights). A second commenter cautioned that unprofitable business and investment lines should always be promptly addressed by FMIs, regardless of whether or not recovery has been triggered. |

We believe the guidance on non-default losses is adequate. |

|

|

|

|||

|

Orderly wind down |

One commenter requests more detail on the role of wind-down plans and how they differ from an FMI resolution plan. This commenter also opines that FMIs exempted from wind down requirements should be required to disclose this exemption, and that principles of defined and limited losses to surviving participants should continue to be observed. A second commenter agrees that developing a wind-down plan may not be appropriate or feasible for some critical services. It concludes that no wind-down plan should be required in those scenarios. |

We note that the guidance, together with the Recovery Report, adequately cover these points. The guidance states that "developing an orderly wind-down plan may not be appropriate or operationally feasible for some critical services". While not obligatory, the guidance further notes that clearing agencies may consider developing wind-down plans for non-critical services where this could benefit a clearing agency in recovery. |

|

|

|

|||

|

Link to resolution frameworks and resolution authority, including "no-creditor-worse-off" (NCWO) policy |

One commenter suggests that due to the connections between recovery and resolution, additional comments on the guidance may be necessary once more details on FMI resolution become available. |

While not within the scope of the guidance, we have briefly addressed some of these comments. See also the cover Notice. |

|

|

|

|||

|

|

The commenter argues that the listed "non-recommended tools," with the exception of forced contract tear up, should also be seen as inappropriate for a resolution scenario. |

We note that the text of the guidance allows clearing agencies to justify to authorities the inclusion of certain types of tools that we characterize as "requiring further justification" (previously described as "not-recommended" tools) in recovery plans. See also our response above. |

|

|

|

|||

|

|

The commenter further suggests that FMI recovery plans should include criteria that, not only measure the effectiveness of each tool so that it can be determined whether the recovery process is effective, but also when a resolution should begin. The commenter also proposes that when recovery is ineffective, FMIs should not utilize loss allocation tools to their prescribed limits. To this end, the commenter highlights that evaluative tools could be implemented, citing criteria for non-viability of financial institutions maintained by OSFI. The commenter also notes that recovery tools should have a high likelihood of success if their use is to respect the NCWO standard (see below), and that in certain circumstances, some recovery tools will not be appropriate. |

The Canadian authorities believe that these comments (particularly, criteria for the non-viability of a clearing agency) are best addressed in the context of resolution and not in recovery, where determining many of these issues would be subject to a framework separate from the recovery process. The development of a clearing agency resolution framework is out of scope of this consultation process. |

|

|

|

|||

|

|

One commenter believes that NCWO protection is fundamental not only to FMI resolution but also at the recovery stage because of the ability for an FMI to allocate losses from failure in recovery. It suggests that the guidance should contain provisions stating that no FMI members should be worse off during recovery than with service closure, using this as the counterfactual for the NCWO safeguard. |

We note that, while NCWO considerations are mostly applicable to gone-concern, rather than going-concern, entities, we have softened language around caps on recovery tools so that recovery does not necessarily result in a mechanistic transition to resolution (e.g., when all recovery tools have been exhausted). |

|

|

|

|||

|

Mandatory clearing suspension |

One commenter notes the need to consider the link between mandatory central clearing requirements and the recovery and resolution of CCPs. The commenter argues that authorities should have the ability to suspend central clearing mandates for a product in the event of a crisis involving an important CCP that clears that product. |

While suspending central clearing requirements in a CCP recovery phase is unlikely, the CSA will work with the Bank of Canada and federal authorities, as well as monitor the development of international guidance, on this topic in the context of CCP resolution frameworks. |

|

ANNEX C

ANNEX I TO COMPANION POLICY 24-102 CLEARING AGENCY REQUIREMENTS [BLACKLINED VERSION -- please see footnote 5 of the Notice]

Annex I to Companion Policy 24-102 Clearing Agency Requirements is amended by replacing the Annex in its entirety with the following:

Annex I to Companion Policy 24-102 Clearing Agency Requirements

Joint Supplementary Guidance Developed by the Bank of Canada and Canadian Securities Administrators

-- PFMI Principle 2: Governance

Box 2.1: Joint Supplementary Guidance -- Governance

Context

The PFMIs define governance as the set of relationships between an FMI's owners, board of directors (or equivalent), management, and other relevant parties, including participants, authorities, and other stakeholders (such as participants' customers, other interdependent FMIs, and the broader market). Governance provides the processes through which an organization sets its objectives, determines the means for achieving those objectives, and monitors performance against those objectives.

This note provides supplementary regulatory guidance for Canadian FMIs that either belong to an integrated entity or are considering consolidating with another entity to form one. It also provides additional context and clarity for Canadian FMIs on certain aspects of the PFMIs expectations pertaining to how their governance arrangements are expected to support relevant public interest considerations.

(i) Vertical and horizontal integration in the context of FMIs

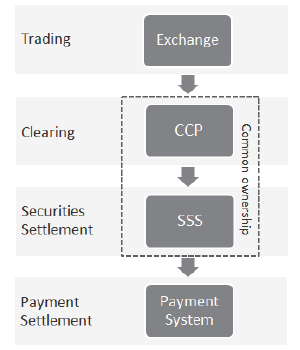

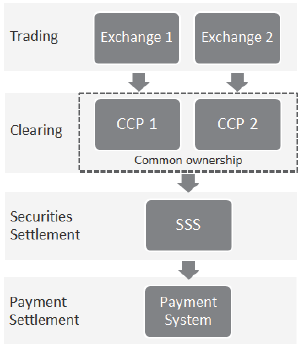

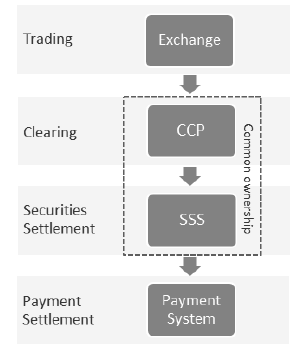

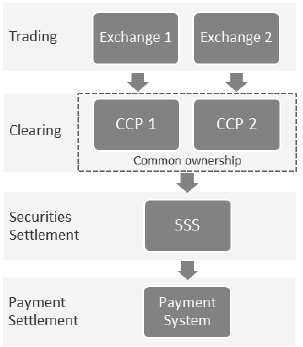

The PFMIs define a vertically integrated FMI group as one that brings together post-trade infrastructure providers under common ownership with providers of other parts of the value chain (for example, one entity owning and operating an exchange, CCP and SSS) and a horizontally integrated group as one that provides the same post-trade service offerings across a number of different products (for example, one entity offering CCP services for derivatives and cash markets).{1} Examples are shown in Figure 1.

(a) Figure 1: Examples of FMI integration in the value chain

Consolidation, or integration, of FMI services may bring about benefits for merging FMIs; however it may also create new governance challenges. The PFMIs contain some general guidance regarding how FMIs should manage governance issues that arise in integrated entities.

(b) Guidance within the PFMIs

The following text has been extracted directly from the PFMIs. The pertinent information is in bold.

PFMI paragraph 3.2.5:

Depending on its ownership structure and organisational form, an FMI may need to focus particular attention on certain aspects of its governance arrangements. An FMI that is part of a larger organisation, for example, should place particular emphasis on the clarity of its governance arrangements, including in relation to any conflicts of interests and outsourcing issues that may arise because of the parent or other affiliated organisation's structure. The FMI's governance arrangements should also be adequate to ensure that decisions of affiliated organisations are not detrimental to the FMI.{2} An FMI that is, or is part of, a for-profit entity may need to place particular emphasis on managing any conflicts between income generation and safety.

PFMI paragraph 3.2.6:

An FMI may also need to focus particular attention on certain aspects of its risk-management arrangements as a result of its ownership structure or organisational form. If an FMI provides services that present a distinct risk profile from, and potentially pose significant additional risks to, its payment, clearing, settlement, or recording function, the FMI needs to manage those additional risks adequately. This may include separating the additional services that the FMI provides from its payment, clearing, settlement, and recording function legally, or taking equivalent action. The ownership structure and organisational form may also need to be considered in the preparation and implementation of the FMI's recovery or wind-down plans or in assessments of the FMI's resolvability.

(c) Supplementary guidance for designated Canadian FMIs

An FMI that is part of a larger entity faces additional risk considerations compared to stand-alone FMIs. While there are potential benefits from integrating services into one large entity, including potential risk reduction benefits, integrated entities could face additional risks such as a greater degree of general business risk. Examples of how this could occur include the following:

• losses in one function may spill-over to the entity's other functions;

• the consolidated entity may face high combined exposures across its functions; and

• the consolidated entity may face exposures to the same participants across its functions.

For a more extensive discussion of potentially heightened risks that integrated FMIs may face, see CPMI-IOSCO, "Market structure developments in the clearing industry: implications for financial stability" (2010).

If an FMI belongs to a larger entity, or is considering consolidating with another entity, it should consider how its risk profile differs as part of the consolidated entity, and take appropriate measures to mitigate these risks.

In addition, FMIs that either belong to an integrated entity or are considering merging to form one should meet the following conditions.

Measures to protect critical FMI functions

FMIs may be part of a larger consolidated entity. These FMIs must either:

• legally separate FMI-related functions{3} from non-FMI-related functions performed by the consolidated entity in order to maximize bankruptcy remoteness of the FMI-related functions; or

• have satisfactory policies and procedures in place to manage additional risks resulting from the non-FMI-related functions appropriately to ensure the FMI's financial and operational viability.

If an FMI performs multiple FMI-related functions with distinct risk profiles within the same entity, the operator should effectively manage the additional risks that may result. The FMI should hold sufficient financial resources to manage the risks in all services it offers, including the combined or compounded risks that would be associated with offering the services through a single legal entity. If the FMI provides multiple services, it should disclose information about the risks of the combined services to existing and prospective participants to give an accurate understanding of the risks they incur by participating in the FMI. The FMI should carefully consider the benefits of offering critical services with distinct risk profiles through separate legal entities.

If an FMI offers CCP services as part of its FMI-related functions, further conditions apply. CCPs take on more risk than other FMIs, and are inherently at higher risk of failure. Therefore, the FMI must either legally separate its CCP functions from other critical (non-CCP) FMI-related functions, or have satisfactory policies and procedures in place to manage additional risks appropriately to ensure the FMI's financial and operational viability.

Legal separation of critical functions is intended to maximize their bankruptcy remoteness and would not necessarily preclude integration of common organizational management activities such as IT and legal services across functions as long as any related risks are appropriately identified and mitigated.

Independence of governance and risk management

FMIs and non-FMIs may have different corporate objectives and risk management appetites which could conflict at the parent level. For example, non-FMI-related functions, such as trading venues, are generally more focused on profit generation than risk management and do not have the same risk profile as FMI-related functions. A trading venue in a vertically integrated entity may benefit from increased participation in its service if its associated clearing function lessens its participation requirements.

To mitigate potential conflicts, in particular the ability of other functions to negatively influence the FMI's risk controls, each FMI subsidiary should have a governance structure and risk management decision-making process that is separate and independent from the other functions and should maintain an appropriate level of autonomy from the parent and other functions to ensure efficient decision making and effective management of any potential conflicts of interest. In addition, the consolidated entity's broad governance arrangements should be reviewed to ensure they do not impede the FMI-related function's observance of the PFMI Principle on governance.

Comprehensive management of risks

Although risk management governance and decision-making should remain independent, it is nonetheless necessary that the consolidated entity is able to manage risk appropriately across the entity. At a consolidated level, the entity should have an appropriate risk management framework that considers the risks of each subsidiary and the additional risks related to their interdependencies.

An FMI should identify and manage the risks it bears from and poses to other entities as a result of interdependencies. Consolidated FMIs should also identify and manage the risks they pose to one another as a result of their interdependencies. Consolidated FMIs may have exposures to the same participants, liquidity providers, and other critical service providers across products, markets and/or functions. This may increase the entity's dependence on these providers and may heighten the systemic risk associated with the consolidated entity compared to a stand-alone FMI. Where possible, the consolidated entity and its FMIs should consider ways to mitigate risks arising from shared dependencies. The consolidated entity and its FMIs should also consider conducting entity-wide operational risk testing related to identifying and mitigating these risks.

Sufficient capital to cover potential losses

Consolidated entities face the risk that a single participant defaults in more than one subsidiary simultaneously. This could result in substantial losses for the consolidated entity which will then also need to replenish resources for the FMIs to continue to operate. FMIs should consider such risks in developing their resource replenishment plan.

Consolidated entities may face higher or lower business risk than individual FMIs depending on size, complexity and diversification across affiliates. Consolidated entities should consider these impacts in their general business risk profiles and in determining the appropriate level of liquid assets needed to cover their potential general business losses.{4}

(ii) Public interest considerations in the context of the PFMIs

The PFMIs indicate that FMIs should "explicitly support financial stability and other relevant public interests." However, there may be circumstances where providing explicit support of relevant public interests conflict with other FMI objectives and therefore require appropriate prioritization and balancing. For example, addressing the potential trade-offs between protecting the participants and the FMI while ensuring the financial stability interests are upheld.

(a) Guidance within the PFMIs

The following text has been extracted directly from the PFMIs. The pertinent information is in bold.

PFMI paragraph 3.2.2:

Given the importance of FMIs and the fact that their decisions can have widespread impact, affecting multiple financial institutions, markets, and jurisdictions, it is essential for each FMI to place a high priority on the safety and efficiency of its operations and explicitly support financial stability and other relevant public interests. Supporting the public interest is a broad concept that includes, for example, fostering fair and efficient markets. For example, in certain over the counter derivatives markets, industry standards and market protocols have been developed to increase certainty, transparency, and stability in the market. If a CCP in such markets were to diverge from these practices, it could, in some cases, undermine the market's efforts to develop common processes to help reduce uncertainty. An FMI's governance arrangements should also include appropriate consideration of the interests of participants, participants' customers, relevant authorities, and other stakeholders. (...) For all types of FMIs, governance arrangements should provide for fair and open access (see Principle 18 on access and participation requirements) and for effective implementation of recovery or wind-down plans, or resolution.

PFMI paragraph 3.2.8:

An FMI's board has multiple roles and responsibilities that should be clearly specified. These roles and responsibilities should include (a) establishing clear strategic aims for the entity; (b) ensuring effective monitoring of senior management (including selecting its senior managers, setting their objectives, evaluating their performance, and, where appropriate, removing them); (c) establishing appropriate compensation policies (which should be consistent with best practices and based on long-term achievements, in particular, the safety and efficiency of the FMI); (d) establishing and overseeing the risk-management function and material risk decisions; (e) overseeing internal control functions (including ensuring independence and adequate resources); (f) ensuring compliance with all supervisory and oversight requirements; (g) ensuring consideration of financial stability and other relevant public interests; and (h) providing accountability to the owners, participants, and other relevant stakeholders.

The CPMI-IOSCO PFMI Disclosure framework and Assessment methodology provides questions to guide the assessment of the FMI against the PFMIs. Questions related to public interest considerations are focused on ensuring that the FMI's objectives are clearly defined, giving a high priority to safety, financial stability and efficiency while also ensuring all other public interest considerations are identified and reflected in the FMI's objectives.

(b) Supplementary Guidance for designated Canadian FMIs

By definition the PFMIs apply to systemically important FMIs, so safety and financial stability objectives should be given a high priority.

Efficiency is also a high priority that should contribute to (but not supersede) the safety and financial stability objectives.

Other public interest considerations such as competition and fair and open access should also be considered in the broader safety and financial stability context.

A framework (objectives, policies and procedures) should be in place for default and other emergency situations. The framework should articulate explicit principles to ensure financial stability and other relevant public interests are considered as part of the decision making process. For example, it should provide guidance on discretionary management decisions, consider the trade-offs between protecting the participants and the FMI while also ensuring the financial stability interests are upheld, and articulate a communication protocol with the board and regulators.

Practical questions/approaches to assessing the appropriateness of the framework include:

• Does the enabling legislation, articles of incorporation, corporate by-laws, corporate mission, vision statements, corporate risk statements/frameworks/methodology clearly articulate the objectives and are they appropriately aligned and communicated (transparent)?

• Do the objectives give appropriate priority to safety, financial stability, efficiency and other public interest considerations?

• Does the Board structure ensure the right mix of skills/experience and interests are in place to ensure the objectives are clear, appropriately prioritized, achieved and measured?

• What is the training provided to the Board and management to support the objectives?

• Do the service offerings and business plans support the objectives?

• Do the system design, rules, procedures support the objectives?

• Are the inter-dependencies and key dependencies considered and managed in the context of the broader financial stability objectives? For instance, do problem and default management policies and procedures appropriately provide for consideration of the broader financial stability interests and do they engage the key stakeholders and regulators?

• Are there procedures in place to get timely engagement of the Board to discuss emerging/current issues, consider scenarios, provide guidance and make decision?

Does the framework ensure that the broader financial stability issues are considered in any actions relating to a participant suspension?

-- PFMI Principle 3: Framework for the comprehensive management of risks

Box 3.1: Joint Supplementary Guidance -- Recovery Plans

Context

In 2012, to enhance the safety and efficiency of payment, clearing and settlement systems, the Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions (CPMI-IOSCO) released a set of international risk-management standards for FMIs, known as the Principles for Financial Market Infrastructures (PFMIs).{1} The PFMIs provide standards regarding FMI recovery planning and orderly wind-down, which were adopted by the Bank of Canada as Standard 24 of the Bank's Risk-Management Standards for Systemic FMIs{2} and by the CSA as part of National Instrument 24-102 (NI-24-102).{5} In the context of recovery planning,

An FMI is expected to identify scenarios that may potentially prevent it from being able to provide its critical operations and services as a going concern and assess the effectiveness of a full range of options for recovery or orderly wind-down. This entails preparing appropriate plans for its recovery or orderly wind-down based on the results of that assessment.

In October 2014, the CPMI-IOSCO released its report, "Recovery of Financial Market Infrastructures" (the Recovery Report), providing additional guidance specific to the recovery of FMIs.{6} The Recovery Report explains the required structure and components of an FMI recovery plan and provides guidance on FMI critical services and recovery tools at a level sufficient to accommodate possible differences in the legal and institutional environments of each jurisdiction.

For the purpose of this guidance, FMI recovery is defined as the set of actions that an FMI can take, consistent with its rules, procedures and other ex ante contractual agreements, to address any uncovered loss, liquidity shortfall or capital inadequacy, whether arising from participant default or other causes (such as business, operational or other structural weakness), including actions to replenish any depleted pre-funded financial resources and liquidity arrangements, as necessary, to maintain the FMI's viability as a going concern and the continued provision of critical services.{7},{8}

Recovery planning is not intended as a substitute for robust day-to-day risk management or for business continuity planning. Rather, it serves to extend and strengthen an FMI's risk-management framework, enhancing the resilience of the FMI against financial risks and bolstering confidence in the FMI's ability to function effectively even under extreme but plausible market conditions and operating environments.

Key Components of Recovery Plans

Overview of existing risk-management and legal structures

As part of their recovery plans, FMIs should include overviews of their legal entity structure and capital structure to provide context for stress scenarios and recovery activities.

FMIs should also include an overview of their existing risk-management frameworks-i.e., their pre-recovery risk-management frameworks and activities. As part of this overview, and to determine the relevant point(s) where standard pre-recovery risk-management frameworks are exhausted, FMIs should identify all the material risks they are exposed to and explain how they use their existing pre-recovery risk-management tools to manage these risks to a high degree of confidence.

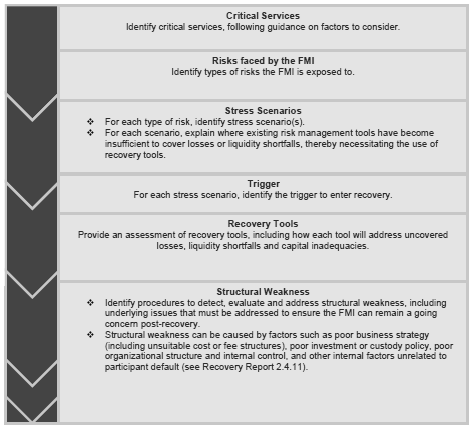

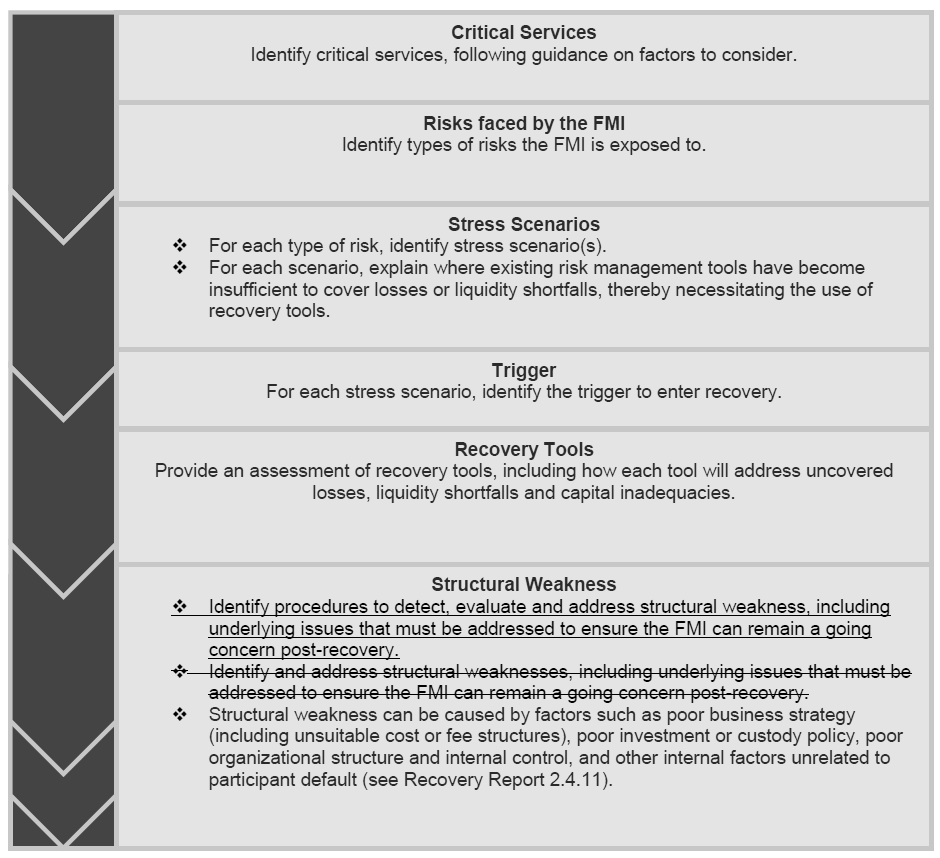

Critical services{9}

In their recovery plans, FMIs should identify, in consultation with Canadian authorities and stakeholders, the services they provide that are critical to the smooth functioning of the markets that they serve and to the maintenance of financial stability. FMIs may find it useful to consider the degree of substitutability and interconnectedness of each of these critical services, specifically

• The degree of criticality of an FMI's service is likely to be high if there are no, or only a small number of, alternative service providers. Factors related to the substitutability of a service could include (i) the size of a service's market share, (ii) the existence of alternative providers that have the capacity to absorb the number of customers and transactions the FMI maintains, and (iii) the FMI participants' capability to transfer positions to the alternative provider(s).

• The degree of criticality of an FMI's service may be high if the service is significantly interconnected with other market participants, both in terms of breadth and depth, thereby increasing the likelihood of contagion if the service were to be discontinued. Potential factors to consider when determining an FMI's interconnectedness are (i) what services it provides to other entities and (ii) which of those services are critical for other entities to function.

Stress scenarios{10}

In their recovery plans, FMIs should identify scenarios that may prevent them from being able to provide their critical services as a going concern. Stress scenarios should be focused on the risks an FMI faces from its payment, clearing and settlement activity. An FMI should then consider stress scenarios that cause financial stress in excess of the capacity of its existing pre-recovery risk controls, thereby placing the FMI into recovery. An FMI should organize stress scenarios by the types of risk it faces; for each stress scenario, the FMI should clearly explain the following:

• the assumptions regarding market conditions and the state of the FMI within the stress scenario, accounting for the differences that may exist depending on whether the stress scenario is systemic or idiosyncratic;

• the estimated impact of a stress scenario on the FMI, its participants, participants' clients and other stakeholders; and

• the extent to which an FMI's existing pre-recovery risk-management tools are insufficient to withstand the impacts of realized risks in a recovery stress scenario and the value of the loss and/or of the negative shock required to generate a gap between existing risk-management tools and the losses associated with the realized risks.

Triggers for recovery

For each stress scenario, FMIs should identify the triggers that would move them from their pre-recovery risk-management activities (e.g., those found in a CCP's default waterfall) to recovery. These triggers should be both qualified (i.e., outlined) and, where relevant, quantified to demonstrate a point at which recovery plans will be implemented without ambiguity or delay. While the boundary between pre-recovery risk-management activities and recovery can be clear (for example, when pre-funded resources are fully depleted), judgment may be needed in some cases. When this boundary is not clear, FMIs should lay out in their recovery plans how they will make decisions.{11} This includes detailing in advance their communication plans, as well as the escalation process associated with their decision-making procedures. They should also specify the decision-makers responsible for each step of the escalation process to ensure that there is adequate time for recovery tools to be implemented if required.

More generally, it is important to identify and place the triggers for recovery early enough in a stress scenario to allow for sufficient time to implement recovery tools described in the recovery plan. Triggers placed too late in a scenario will impede the effective rollout of these tools and hamper recovery efforts. Overall, in determining the moment when recovery should commence, and especially where there is uncertainty around this juncture, an FMI should be prudent in its actions and err on the side of caution.

Selection and Application of Recovery Tools{12}

A comprehensive plan for recovery

The success of a recovery plan relies on a comprehensive set of tools that can be effectively applied during recovery. The applicability of these tools and their contribution to recovery varies by system, stress event and the order in which they are applied.

A robust recovery plan relies on a range of tools to form an adequate response to realized risks. Canadian authorities will provide feedback on the comprehensiveness of selected recovery tools when reviewing an FMI's complete recovery plan.

Characteristics of recovery tools

In providing this guidance, Canadian authorities used a broad set of criteria (described below), including those from the Recovery Report, to determine the characteristics of effective recovery tools.{13} FMIs should aim for consistency with these criteria in the selection and application of tools. In this context, recovery tools should be

• Reliable and timely in their application and have a strong legal and regulatory basis. This includes the need for FMIs to mitigate the risk that a participant may be unable or unwilling to meet a call for financial resources in a timely manner, or at all (i.e., performance risk), and to ensure that all recovery activities have a strong legal and regulatory basis.

• Measurable, manageable and controllable to ensure that they can be applied effectively while keeping in mind the objective of minimizing their negative effects on participants and the broader financial system. To this end, using tools in a manner that results in participant exposures that are determinable and fixed provides better certainty of the tools' impacts on FMI participants and their contribution to recovery. Fairness in the allocation of uncovered losses and shortfalls, and the capacity to manage the associated costs, should also be considered.

• Transparent to participants: this should include a predefined description of each recovery tool, its purpose and the responsibilities and procedures of participants and the FMIs subject to the recovery tool's application to effectively manage participants' expectations. Transparency also mitigates performance risk by detailing the obligations and procedures of FMIs and participants beforehand to support the timely and effective rollout of recovery tools.

• Designed to create appropriate incentives for sound risk management and encourage voluntary participation in recovery to the greatest extent possible. This may include distributing post-recovery proceeds to participants that supported the FMI through the recovery process.

Systemic stability

Certain tools may have serious consequences for participants and for the stability of financial markets more generally. FMIs should use prudence and judgment in the selection of appropriate tools. Canadian authorities are of the view that FMIs should be cautious in using tools that can create uncapped, unpredictable or ill-defined participant exposures, and which could create uncertainty and disincentives to participate in an FMI. Any such use would need to be carefully justified. Participants' ability to predict and manage their exposures to recovery tools is important, both for their own stability and for the stability of the indirect participants of an FMI.

In assessing FMI recovery plans, Canadian authorities are concerned with the possibility of systemic disruptions from the use of certain tools or tools that pose unquantifiable risks to participants. When determining which recovery tools should be included in a recovery plan, and selecting and applying such tools during the recovery phase, FMIs should keep in mind the objective of minimizing their negative impacts on participants, the FMI and the broader financial system.

Recommended recovery tools

This section outlines recommended recovery tools for use in FMI recovery plans. Not all tools are applicable for the different types of FMIs (e.g., a payment system versus a central counterparty), nor is this an exhaustive list of tools that may be available for recovery. Each FMI should use discretion when determining the most appropriate tools for inclusion in its recovery plan, consistent with the considerations discussed above.

• Cash calls

Cash calls are recommended for recovery plans to the extent that the exposures they generate are fixed and determinable; for example, capped and limited to a maximum number of rounds over a specified period, established in advance. In this context, participant exposures should be linked to each participant's risk-weighted level of FMI activity.

By providing predictable exposures pro-rated to a participant's risk-weighted level of activity, FMIs create incentives for better risk management on the part of participants, while giving the FMI greater certainty over the amount of resources that can be made available during recovery.

Since cash calls rely on contingent resources held by FMI participants, there is a risk that they may not be honoured, reducing their effectiveness as a recovery tool. The management of participants' expectations, especially through the placement of clear limits on participant exposure, can mitigate this concern.

Cash calls can be designed in multiple ways to structure incentives, vary their impacts on participants and respond to different stress scenarios. When designing cash calls, FMIs should, to the greatest extent possible, seek to minimize the negative consequences of the tool's use.

• Variation margin gains haircutting (VMGH)

VMGH is recommended for recovery plans because participant exposure under this tool can be measured with reasonable confidence, as it is tied to the level of risk held in the variation margin (VM) fund and the potential for gains. Where recovery plans allow for multiple rounds of VMGH, Canadian authorities will consider the impact of each successive round of haircutting with increasing focus on systemic stability.

VMGH relies on participant resources posted at the FMI as variation margin (VM). Where the price movements of underlying instruments create sufficient VM gains for use in recovery, VMGH provides an FMI with a reliable and timely source of financial resources without the performance risk that is associated with tools reliant on resources held by participants.

VMGH assigns losses and shortfalls only to participants with net position gains; as a result, the pro rata financial burden is higher for these participants. The negative effects of VMGH can also be compounded for participants who rely on variation margin gains to honour obligations outside the FMI.

FMIs should seek to minimize these negative effects to the greatest extent possible.

• Voluntary contract allocation

To recover from an unmatched book caused by a participant default, a CCP can use its powers to allocate unmatched contracts.{14} In the context of recovery, contract allocation is encouraged on a voluntary basis for example, by auction. Voluntary contract allocation addresses unmatched positions while taking participant welfare into account, since only participants who are willing to take on positions will participate.

The reliance on a voluntary process, such as an auction, introduces the risk that not all positions will be matched or that the auction process is not carried out in a timely manner. Defining the responsibilities and procedures for voluntary contract allocation (e.g., the auction rules) in advance will mitigate this risk and increase the reliability of the tool. To ensure that there is adequate participation in an auction process, FMIs should create incentives for participants to take on unmatched positions. FMIs may also wish to consider expanding the auction beyond direct participants to increase the chances that all positions will be matched.

• Voluntary contract tear-up

Since eliminating positions can help re-establish a matched book, Canadian authorities view voluntary contract tear-up as a potentially effective tool for FMI recovery. To this end, FMIs may want to consider using incentives to encourage voluntary tear-up during recovery.{15} While contract tear-up undertaken on a voluntary basis is a recommended tool, the forced termination of an incomplete trade may represent a disruption of a critical FMI service, and can be intrusive to apply (see the section "Tools requiring further justification" for a discussion of forced contract tear-up).

To the extent that voluntary contract tear-up may disrupt critical FMI services, it can produce disincentives to participate in an FMI. There should be a strong legal basis for the relevant processes and procedures when voluntary contract tear-up is included in a recovery plan. This will help to manage participant expectations for this tool and ensure that confidence in the FMI is maintained.

Other tools available for FMI recovery include standing third-party liquidity lines, contractual liquidity arrangements with participants, insurance against financial loss, increased contributions to pre-funded resources, and use of an FMI's own capital beyond the default waterfall. These and other tools are often already found in the pre-recovery risk-management frameworks of FMIs. Canadian authorities encourage their use for recovery as well, provided they are in keeping with the criteria for effective recovery tools as found in the Recovery Report and in this guidance.{16} Where system-specific recovery needs necessitate, FMIs can also design recovery tools not explicitly listed in this guidance. The applicability of such tools will be examined by the Canadian authorities when they review the proposed recovery plan.

To the extent that the costs of recovery are shared less equally under some tools (e.g., VMGH), if it is financially feasible, FMIs could consider post-recovery actions to restore fairness where participants have been disproportionately affected. Such actions may include the repayment of participant contributions used to address liquidity shortfalls and other instruments that aim to redistribute the burden of losses allocated during recovery. It is important to note that these actions in the post-recovery period should not impair the financial viability of the FMI as a going concern.

Tools requiring further justification

Due to their uncertain and potentially negative effects on the broader financial system, tools that are more intrusive or result in participant exposures that are difficult to measure, manage or control, must be carefully considered and justified with strong rationale by the FMI when they are included in a recovery plan. Canadian authorities will provide their views on the suitability of any such tools as part of cash calls, unlimited rounds their review of recovery plans.

For example, uncapped and unlimited cash calls and unlimited rounds of VMGH can create ambiguous participant exposures, the negative effects of which must be prudently considered when including them in a recovery plan. In addition, when applied during the recovery process, Canadian authorities will monitor the application of each successive round of cash calls and VMGH with increased focus on systemic stability.

Tools such as involuntary (forced) contract allocation and involuntary (forced) contract tear-up create exposures that are difficult to manage, measure and control. To the extent that these tools are even more intrusive, they have the ability to pose greater risk to systemic stability. Canadian authorities acknowledge that such tools have potential utility when other recovery options are ineffective, and could possibly be used by a resolution authority, but expect FMIs to carefully assess the potential impact of such tools on participants and the stability of the broader financial system.

Canadian authorities do not encourage the use of non-defaulting participants' initial margin in FMI recovery plans considering the potential for significant negative impacts.{17} Similarly, a recovery plan should not assume any extraordinary form of public or central bank support.{18}

Recovery from non-default-related losses and structural weaknesses

Consistent with a defaulter-pays principle, an FMI should rely on FMI-funded resources to address recovery from non-default-related losses (i.e., operational and business losses on the part of an FMI), including losses arising from structural weakness.{19} To this end, FMIs should examine ways to increase the loss absorbency between the FMI's pre-recovery risk-management activities and participant-funded resources (e.g., by using FMI-funded insurance against operational risks).

Structural weakness can be an impediment to the effective rollout of recovery tools and may itself result in non-default-related losses that are a trigger for recovery. An FMI recovery plan should identify procedures detailing how to promptly detect, evaluate and address the sources of underlying structural weakness on a continuous basis (e.g., unprofitable business lines, investment losses).

The use of participant-funded resources to recover from non-default-related losses can lessen incentives for robust risk management within an FMI and provide disincentives to participate. If, despite these concerns, participants consider it in their interest to keep the FMI as a going concern, an FMI and its participants may agree to include a certain amount of participant-funded recovery tools to address some non-default-related losses. Under these circumstances, the FMI should clearly explain under what conditions participant resources would be used and how costs would be distributed.

Defining full allocation of uncovered losses and liquidity shortfalls

Principles 4 (credit risk){20} and 7 (liquidity risk){21} of the PFMIs require that FMIs should specify rules and procedures to fully allocate both uncovered losses and liquidity shortfalls caused by stress even. To be consistent with this requirement, Canadian FMIs should consider various stress scenarios and have rules and procedures that allow them to fully allocate any losses or liquidity shortfalls arising from these stress scenarios in excess of the capacity of existing pre-recovery risk controls. Tools used to address full allocation should reflect the Recovery Report's characteristics of effective recovery tools, including the need to have them measurable, manageable and controllable to those who will bear the losses and liquidity shortfalls in recovery, and for their negative impacts to be minimized to the greatest extent possible.

Legal consideration for full allocation

An FMI's rules for allocating losses and liquidity shortfalls should be supported by relevant laws and regulations. There should be a high level of certainty that rules and procedures to fully allocate all uncovered losses and liquidity shortfalls are enforceable and will not be voided, reversed or stayed.{22} This requires that Canadian FMIs design their recovery tools in compliance with Canadian laws. For example, if the FMI's loss-allocation rules involve a guarantee, Canadian law generally requires that the guaranteed amount be determinable and preferably capped by a fixed amount.{23}

FMIs should consider whether it is appropriate to involve indirect participants in the allocation of losses and shortfalls during recovery. To the extent that it is permitted, such arrangements should have a strong legal and regulatory basis; respect the FMI's frameworks for tiered participation, segregation and portability; and involve consultation with indirect participants to ensure that all relevant concerns are taken into account.

Overall, FMIs are responsible for seeking appropriate legal advice on how their recovery tools can be designed and for ensuring that all recovery tools and activities are in compliance with the relevant laws and regulations.

Additional Considerations in Recovery Planning

Transparency and coherence{24}

An FMI should ensure that its recovery plan is coherent and transparent to all relevant levels of management within the FMI, as well as to its regulators and overseers. To do so, a recovery plan should

• contain information at the appropriate level and detail; and

• be sufficiently coherent to relevant parties within the FMI, as well as to the regulators and overseers of the FMI, to effectively support the application of the recovery tools.

An FMI should ensure that the assumptions, preconditions, key dependencies and decision-making processes in a recovery plan are transparent and clearly identified.

Relevance and flexibility{25}

An FMI's recovery plan should thoroughly cover the information and actions relevant to extreme but plausible market conditions and other situations that would call for the use of recovery tools. An FMI should take into account the following elements when developing its recovery plan:

• the nature, size and complexity of its operations;

• its interconnectedness with other entities;

• operational functions, processes and/or infrastructure that may affect the FMI's ability to implement its recovery plan; and

• any upcoming regulatory reforms that may have the potential to affect the recovery plan.

Recovery plans should be sufficiently flexible to address a range of FMI-specific and market-wide stress events. Recovery plans should also be structured and written at a level that enables the FMI's management to assess the recovery scenario and initiate appropriate recovery procedures. As part of this expectation, the recovery plan should demonstrate that senior management has assessed the potential two-way interaction between recovery tools and the FMI's business model, legal entity structure, and business and risk-management practices.

Implementation of Recovery Plan{26}

An FMI should have credible and operationally feasible approaches to recovery planning in place and be able to act upon them in a timely manner, under both idiosyncratic and market-wide stress scenarios. To this end, recovery plans should describe

• potential impediments to applying recovery tools effectively and strategies to address them; and

• the impact of a major operational disruption.{27}

This information is important to strengthen a recovery plan's resilience to shocks and ensure that the recovery tools are actionable.

A recovery plan should also include an escalation process and the associated communication procedures that an FMI would take in a recovery situation. Such a process should define the associated timelines, objectives and key messages of each communication step, as well as the decision-makers who are responsible for it.

Consulting Canadian authorities when taking recovery actions

While the responsibility for implementing the recovery plan rests with the FMI, Canadian authorities consider it critical to be informed when an FMI triggers its recovery plan and before the application of recovery tools and other recovery actions. To the extent an FMI intends to use a tool or take a recovery action that might have significant impact on its participants (e.g. tools requiring further justification), the FMI should consult Canadian authorities before using such tools or taking such actions to demonstrate how it has taken into account potential financial stability implications and other relevant public interest considerations. Authorities include those responsible for the regulation, supervision and oversight of the FMI, as well as any authorities who would be responsible for the FMI if it were to be put into resolution.

Relevant Canadian authorities should be informed (or consulted as appropriate) early on and interaction with authorities should be explicitly identified in the escalation process of a recovery plan. Acknowledging the speed at which an FMI may enter recovery, FMIs are encouraged to develop formal communications protocols with authorities in the event that recovery is triggered and immediate action is required.

Review of Recovery Plan{28}

An FMI should include in its recovery plan a robust assessment of the recovery tools presented and detail the key factors that may affect their application. It should recognize that, while some recovery tools may be effective in returning the FMI to viability, these tools may not have a desirable effect on its participants or the broader financial system.

A framework for testing the recovery plan (for example, through scenario exercises, periodic simulations, back-testing and other mechanisms) should be presented either in the plan itself or linked to a separate document. This impact assessment should include an analysis of the effect of applying recovery tools on financial stability and other relevant public interest considerations.{29} Furthermore, an FMI should demonstrate that the appropriate business units and levels of management have assessed the potential consequences of recovery tools on FMI participants and entities linked to the FMI.

Annual review of recovery plan

An FMI should review and, if necessary, update its recovery plan on an annual basis. The recovery plan should be subject to approval by the FMI's Board of Directors.{30} Under the following circumstances, an FMI is expected to review its recovery plan more frequently:

• if there is a significant change to market conditions or to an FMI's business model, corporate structure, services provided, risk exposures or any other element of the firm that could have a relevant impact on the recovery plan;

• if an FMI encounters a severe stress situation that requires appropriate updates to the recovery plan to address the changes in the FMI's environment or lessons learned through the stress period; and

• if the Canadian authorities request that the FMI update the recovery plan to address specific concerns or for additional clarity.