CSA Staff Notice 25-303 – 2021 CSA Annual Activities Report on the Oversight of Self-Regulatory Organizations and Investor Protection Funds

CSA Staff Notice 25-303 – 2021 CSA Annual Activities Report on the Oversight of Self-Regulatory Organizations and Investor Protection Funds

INTRODUCTION

Self-regulatory organizations

Self-regulatory organizations (SROs) are entities that have been given the responsibility by securities regulators to govern the operations and business conduct of certain players in the investment industry, with a view to promoting the protection of investors and the public interest. In Canada, SROs operate under the authority and supervision of the Canadian Securities Administrators (CSA or statutory regulators). Applicable legislation in each province and territory provides each securities regulator within the CSA with the power to recognize an SRO through a Recognition Order. The Recognition Order also sets out the authority of an SRO to carry out certain regulatory functions and the terms and conditions that each SRO must comply with in carrying out their regulatory functions.

In Canada, the two SROs are the Investment Industry Regulatory Organization of Canada (IIROC) and the Mutual Fund Dealers Association of Canada (MFDA). IIROC is recognized by all thirteen provinces and territories, while the MFDA is recognized by eight provinces and three territories.{1}

The oversight of the SROs is coordinated through two separate memoranda of understanding (MOUs). Each MOU describes how the Recognizing Regulators (RRs) will oversee the SRO's performance of its self-regulatory activities and services to ensure that the SRO is acting in accordance with the public interest and complying with the terms and conditions of its Recognition Orders.{2}

Investor protection funds

Investor protection funds (IPFs) are authorized to provide coverage within prescribed limits for financial losses suffered by eligible clients in the event of the insolvency of an investment dealer or a mutual fund dealer. Analogous to the recognition and oversight of SROs, the statutory regulators have the power to approve an IPF through an Approval Order, and separate MOUs coordinate the oversight of the IPFs among the Approving Regulators (ARs). Currently, there are two approved or accepted IPFs -- the Canadian Investor Protection Fund (CIPF) and the MFDA Investor Protection Corporation (MFDA IPC).{3} {4} {5}

Annual Activities Report

This report summarizes the key oversight activities of CSA staff (Staff) and their assessment of SRO and IPF compliance with securities legislation requirements, including the terms and conditions of recognition or approval/acceptance. As part of our continuing efforts to be transparent and foster public confidence in the regulatory framework, Staff intend to publish an activities report on the CSA's oversight of the new SRO and new IPF{6} on an annual basis, going forward.

This report covers the period of January 1 -- December 31, 2021 (the Reporting Period).

The remainder of this report follows the below structure:

• Section 1 -- Executive Summary

• Section 2 -- Oversight Committees

• Section 3 -- Overview of CSA Oversight Program

• Section 4 -- Summary of Key Information, Oversight Activities and Observations

(A) IIROC

(B) MFDA

(C) CIPF

(D) MFDA IPC

• Appendix 1 -- Composition of the SRO Oversight Committees

• Appendix 2 -- Rule/By-law/Policy and Procedures Amendments

• Appendix 3 -- Other Materials Filed

1. EXECUTIVE SUMMARY

Staff are of the view that, based on the oversight activities performed by Staff during the Reporting Period, the CSA continues to fulfill its obligations in overseeing SRO and IPF compliance with securities legislation and the Recognition/Approval Orders. Set out below are key highlights from CSA oversight activities performed during the Reporting Period.

• New SRO Framework: On June 25, 2020, the CSA working group published CSA Consultation Paper 25-402 Consultation on the Self-Regulatory Organization Framework. The paper sought public input on seven key issues identified through informal consultations conducted by the CSA working group in late 2019 and early 2020. During the public comment period, 67 letters were received from a broad range of stakeholders. The information and views provided by stakeholders were considered -- along with other data and analysis, including dozens of academic publications pertaining to SRO design, operation and best practices, and their applicability to the Canadian capital markets -- for the CSA working group to arrive at its recommendation.

The overall recommendation for a new single enhanced SRO and, separately, a combined protection fund is described in CSA Position Paper 25-404 New Self-Regulatory Organization Framework, published on August 3, 2021 (CSA Position Paper). The new SRO will consolidate the functions of IIROC and the MFDA, while the new IPF will combine CIPF and the MFDA IPC into an integrated fund independent of the new SRO. The corporate transactions necessary for amalgamation (including obtaining the ministerial approvals) are expected to be completed by the end of 2022. All work is progressing on track in accordance with the timeline.

A Special Joint Committee (SJC) has been formed, comprised of representatives from IIROC, the MFDA and the CSA. The mandate of the SJC is to identify and recommend candidates for the new SRO's chief executive officer, who would also be a voting member of the board, as well as six industry directors and eight independent directors, with one of the independent directors serving as the SRO's Chair. The SJC has retained Russell Reynolds, a global leadership advisory and search firm, to assist with recruitment.

Since the publication of the CSA Position Paper, Staff have organized nine specific workstreams to lead and manage different aspects of the integration project. Comment letters about the framework have been reviewed by Staff and have been considered as the process moves forward, which includes continuing stakeholder engagement.

To address the specific regulatory landscape in force in Québec to facilitate the transition, the Autorité des marchés financiers (AMF) has put together a forum with senior representatives of the Chambre de la sécurité financière, IIROC's Montreal Office and the Conseil des fonds d'investissement du Québec, which is the Investment Funds Institute of Canada's voice in Québec.

IIROC and MFDA staff are also working together on the necessary operational components needed to combine their respective organizations and have retained an outside consultant, Deloitte, to serve as an integration manager.

The integration of the IPFs continues on a separate track, with the same completion date and subject to the same CSA oversight.

• COVID-19 Update: In response to the risks associated with the COVID-19 pandemic, the SROs and IPFs triggered business continuity plans in March 2020 and moved their staff to working remotely from the office. During the Reporting Period, the entities continued to operate with staff working from home and functions primarily being carried on remotely. Plans are being made for a return to the office in Spring 2022, in accordance with public health measures, and proposed pilots are being developed for expanded work-from-home arrangements after office re-openings. CSA staff have been receiving regular updates from the SROs and IPFs in terms of their own operations and their oversight of member operations. Other COVID-19 related information is contained within the body of this report.

• Project to Streamline and Modernize Orders and MOUs: In the first quarter of the Reporting Period, Staff completed a three-phased multi-year project, intended to improve harmonization and CSA oversight of SROs and IPFs to ultimately enhance investor protection. Brief details of each of the three phases are provided below:

• Phase 1 project helped modernize reporting requirements for IIROC and the MFDA and was completed in April 2018.

• Phase 2 project eliminated the regulatory gaps that existed with respect to the IPF approvals and oversight. Specifically, all jurisdictions recognizing IIROC have now also approved the CIPF as an IPF for investment dealers. Analogously, all jurisdictions recognizing the MFDA have now approved the MFDA IPC as an IPF for mutual fund dealers. As part of this project, IPF Approval Orders have been updated and harmonized and appropriate MOUs signed to better reflect CSA oversight expectations. All the proposed changes were published for comment; no comments were received, following which subsequent CSA approvals were obtained. This phase was completed in January 2021 when the amended Approval Orders and MOUs came into effect.

• Phase 3 project harmonized, streamlined and modernized IIROC and MFDA Recognition Orders and MOUs to better reflect current CSA expectations and oversight practices. In addition, as part of Phase 3, the three territories recognized the MFDA in addition to eight provinces.{7} Analogous to Phase 2, the proposed changes to the Recognition Orders and MOUs were published; no comments were received, following which subsequent CSA approvals were obtained. Phase 3 was completed in April 2021 when the amended Recognition Orders and MOUs came into effect.

• The SROs and IPFs were actively consulted by Staff throughout the applicable phases.

This three-phased project was important not only for immediate enhancement of SRO and IPF oversight, but the project will also assist in the creation of a new single SRO and independent new IPF, which will require the consolidation of the existing Recognition/Approval Orders and MOUs. Having these documents largely harmonized and modernized will ease the continuing work related to the new SRO Framework.

• Enhanced Methodology Project: The purpose of the Enhanced Methodology Project was to identify and implement improvements to the CSA methodology for coordinated oversight of SROs and IPFs, while also formalizing many of the practices and processes already being followed by Staff. The main changes to the methodology included:

• updates to the CSA risk assessment framework for SROs and IPFs to account for applicable advancements in best practices;

• the introduction of different levels of participation (full, limited, and reliant) which define a jurisdiction's involvement in an oversight activity;

• the introduction of the concept of "regulatory activities" that are core to the mandate of an SRO or IPF. The revised methodology recommends that each regulatory activity of an entity be examined at least once in a 5-year cycle, regardless of its net risk score;

• the inclusion of a complaint handling process which sets out the manner by which RRs should receive, process and assess legitimate complaints made against an SRO or IPF; and

• the inclusion of a process for Enforcement referrals, developed in consultation with CSA Enforcement staff and the SROs, and which sets out the key elements to define and administer enforcement referrals by SROs.

The enhanced methodology was implemented by Staff on April 1, 2021.

• Oversight Reviews: Staff conducted a risk-based desk review of IIROC during the Reporting Period, targeting specific processes within IIROC's Equity Market Surveillance and Debt Market Surveillance functions. Although Staff did not identify overall concerns with IIROC's compliance with the relevant terms and conditions of the Recognition Order, one low priority finding was noted. The final CSA report discussing the results of the review was published on June 25, 2021.

Based on the annual CSA risk assessments of the MFDA, CIPF and MFDA IPC, a determination was made that oversight reviews of these entities during the Reporting Period were not warranted, and that action items resulting from the risk assessments could be addressed by other oversight mechanisms. Staff continued to review filing requirements, hold meetings with the entities, review applicable rule proposals in the normal course, and follow-up with queries as necessary.

2. OVERSIGHT COMMITTEES

The CSA Market Regulation Steering Committee{8} is the forum for coordination and providing updates where issues relate to more than one SRO or IPF. There are also oversight sub-committees for each SRO and IPF to act as a forum to discuss issues, concerns and proposals related to the oversight of each SRO or IPF. The oversight sub-committees include representatives from each of the RRs and ARs, with the Principal Regulator serving as the lead.{9} The committees held scheduled quarterly meetings with each SRO and semi-annual meetings with each IPF during the Reporting Period.{10} The respective committees also held numerous ad hoc meetings with the respective entities throughout the Reporting Period as part of their oversight of specific issues, primarily related to the oversight review, proposed rule amendments and filing requirements.

3. OVERVIEW OF CSA OVERSIGHT PROGRAM

While the Enhanced Methodology Project made some improvements to the CSA oversight framework and methodology for SROs and IPFs, the core elements of the program remain the same. The RRs' oversight program for SROs, and the ARs' oversight program for IPFs include:

• Annual Risk Assessment -- an evaluation of potential inherent risks and mitigating controls for each entity, to identify specific risks and control factors in each functional area of the entity. The evaluation can become the basis of future oversight activities as determined by the net adjusted risk attributed to each functional area.

• Oversight Reviews -- a more in-depth process for Staff to make an independent assessment of whether and how the entity meets its regulatory obligations. For example, oversight reviews{11} provide an opportunity to validate the information received from the entity through interviewing staff, obtaining an understanding of the systems and processes in place, reviewing written policies, and examining files on a sample basis. The scope of an oversight review is determined by the results of the annual risk assessment and/or specific issues that arise on a periodic basis. During the Reporting Period, Staff conducted a desk review of IIROC and the final report was published on June 25, 2021.

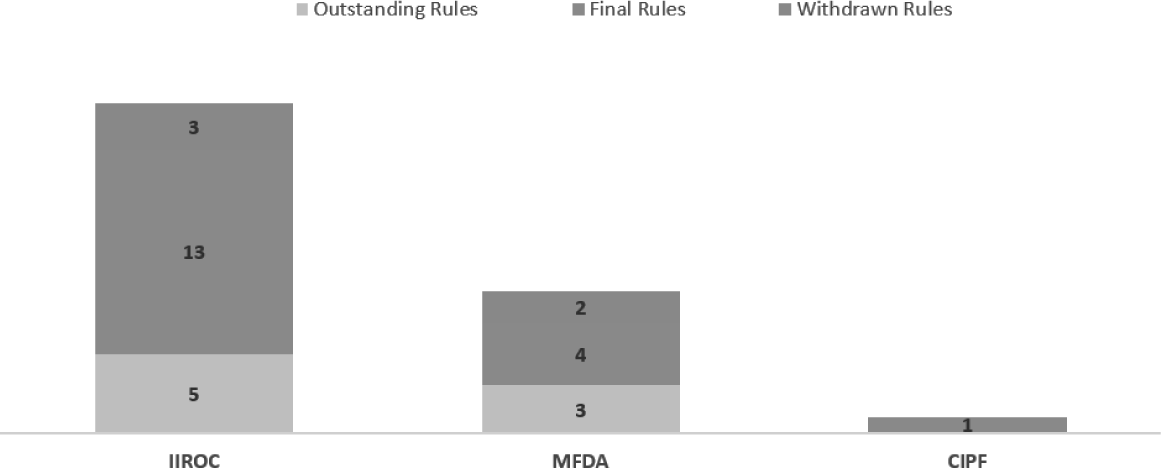

• Review and Approval of Proposed New and Amended Rules, Policies and Constating Documents (collectively, rules) -- Under their respective Recognition Orders and MOUs, SROs are required to seek RR approval for proposed new rules and by-laws, and any changes to existing rules and by-laws. Similarly, under their respective Approval Orders and MOUs, IPFs are required to seek AR approval or non-objection for any changes to certain policies (e.g. coverage policy) and their by-laws. Staff of all RRs/ARs are involved in the rule review process with the Principal Regulator coordinating communication with the entity. Staff coordinate their review of rule proposals and amendments, provide consolidated comments, and assess the entity's responses. Staff also consider if the entity's responses to public comments are adequate and reasonable. Only when satisfied that the public interest has been met, Staff recommend rule proposals and amendments for approval or non-objection to their decision makers. If Staff of all RRs/ARs are not prepared to support approval or non-objection, the entity generally withdraws the rule proposal or amendment, or makes revisions to address issues raised. The chart below reflects the number of rules approved or withdrawn during the Reporting Period and outstanding as of December 31, 2021.{12}

Rules{13} Approved or Withdrawn During the Reporting Period, and Outstanding as of December 31, 2021{14}

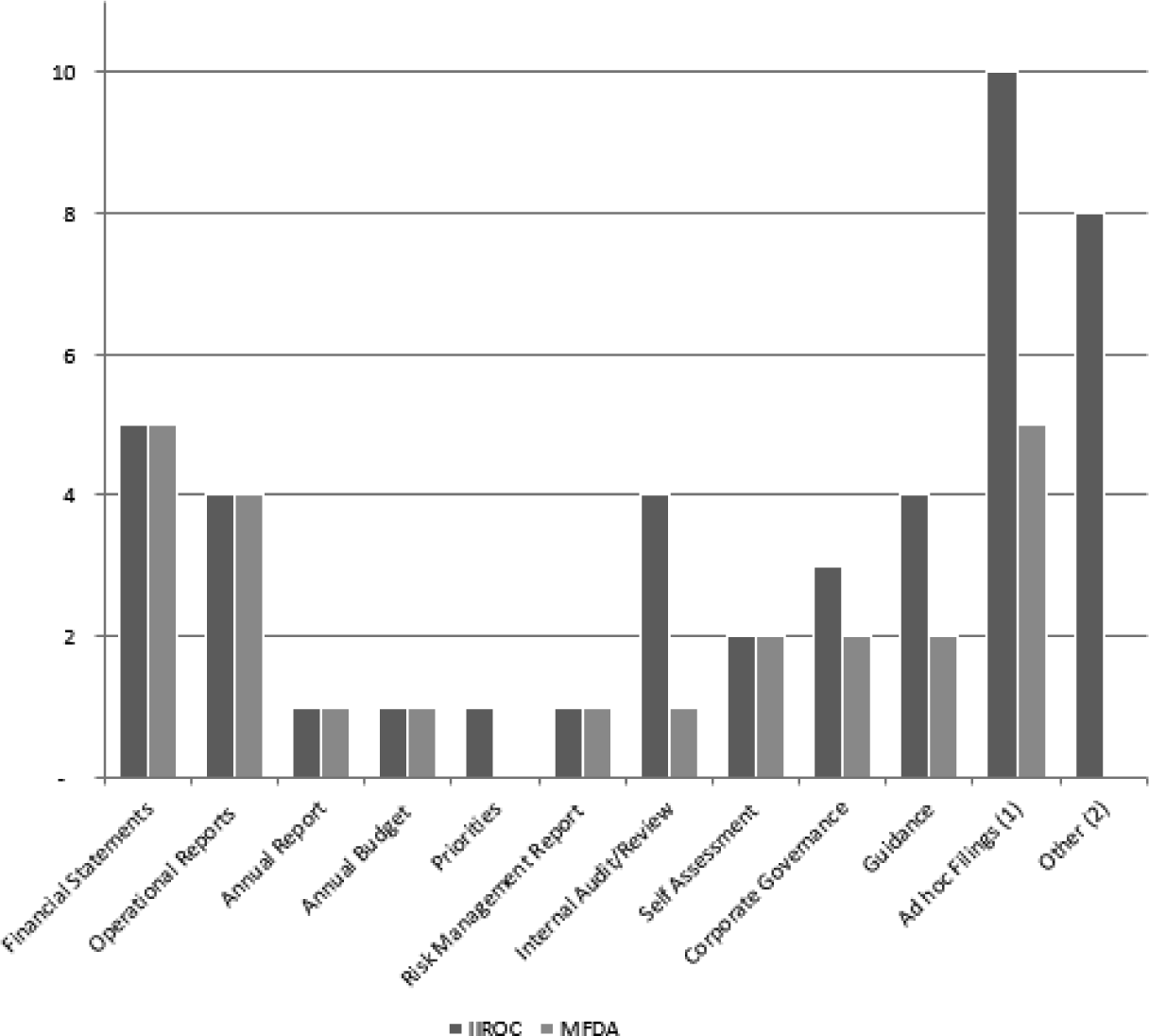

• Review of Materials Filed -- SROs and IPFs are responsible for filing certain information (other than proposed rules or by-laws) with each RR/AR, as required by the Recognition/Approval Orders. This information includes, but is not limited to, reports on financial condition, regulatory self-assessments, risk management scorecards, systems integrity, market surveillance, internal audit, progress on compliance examination results and enforcement matters. Staff review the materials filed, and the Principal Regulator coordinates the necessary follow-up with the SRO or IPF on significant issues identified. Staff's review of issues and materials filed inform the annual risk assessment process.{15}

• Meetings and Other Discussions with Entities

• SROs -- Staff meet with IIROC and, separately, with the MFDA on a scheduled quarterly basis to discuss issues relating to each SRO's regulatory activities, the RRs oversight process, and to share information about emerging and/or ongoing regulatory issues and trends. In addition, Staff of certain RRs hold regular meetings with management of the SROs at regional offices to discuss regional issues. Staff also discuss key or escalated issues with each SRO's management as they arise.

• IPFs -- Staff meet with each IPF on a scheduled semi-annual basis to discuss issues relating to the IPFs' activities, the ARs oversight process, and to share information about emerging and/or ongoing regulatory issues and trends. Staff also discuss issues with each IPF's management as they arise.

4. SUMMARY OF KEY INFORMATION, OVERSIGHT ACTIVITIES AND OBSERVATIONS

(A) IIROC

i. Regulatory Status

IIROC as an SRO oversees all investment dealers and trading activity on debt and equity marketplaces in Canada{16} and has been approved as an information processor for corporate and government debt securities. IIROC's head office is in Toronto with regional offices in Montréal, Calgary and Vancouver.

ii. Member Firm Statistics

|

As at December 31 |

2021 |

2020 |

Change |

% Change |

|

|

||||

|

Assets Under Management |

$4.1 Trillion |

$3.4 Trillion |

$0.7 Trillion |

20.6% |

|

|

||||

|

Approved Persons |

30,747 |

29,441 |

1,306 |

4.4% |

|

|

||||

|

Firms |

172 |

169 |

3 |

1.8% |

(Source: IIROC and National Registration Database (NRD))

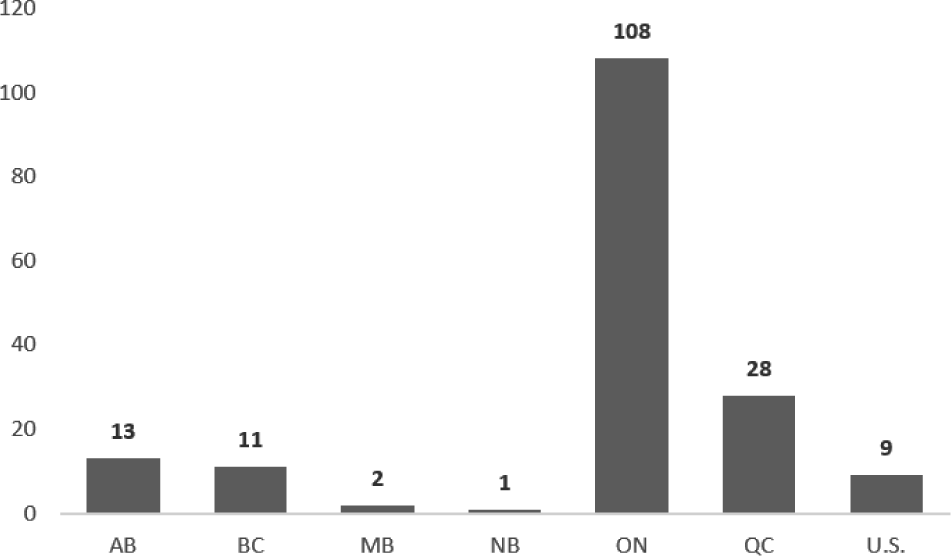

iii. IIROC Member Firms by Head Office Location

(Source: NRD)

iv. Oversight Review

IIROC implemented an enhanced software for market surveillance (SMARTS) in March 2019. Using SMARTS, IIROC's Market Surveillance teams have improved their ability to: (i) quickly detect trading anomalies across multiple products, individual traders and firms; and (ii) identify and respond to emerging trends -- for example, by monitoring daily message and trade volumes in a more efficient manner.

During the Review Period, Staff completed a risk-based desk review of IIROC. Based on the results of the annual risk assessment and in order to follow up on the implementation of the new market surveillance system, Staff determined that the following areas within IIROC's Equity and Debt Market Surveillance function would form the focus of the oversight review to assess the adequacy of those identified areas:

• Equity Market Surveillance

• Development and review of equity market surveillance alerts

• The Market Wide Circuit Breaker (MWCB) process

• Debt Market Surveillance

• Development and review of debt market surveillance alerts

• IIROC's review of triggered debt market surveillance alerts

• Data integrity review of reported debt transaction data

Based on the work performed, Staff were satisfied that IIROC had adequate processes and procedures in place in the identified areas, except for a low priority finding pertaining to certain processes and procedures not being integrated into the Equity and Debt Market Surveillance written policies and procedures manuals. Staff have since reviewed the relevant manuals and are satisfied that they have been adequately updated to address the finding.

Staff acknowledge that IIROC has made recent enhancements to the MWCB process and, as part of IIROC's outreach to Canadian marketplaces, IIROC is currently assessing the need for any additional enhancements to the MWCB process (e.g., desirability to automate the MWCB process). Staff have continued to follow up with IIROC regarding the development of any potential enhancement to the MWCB process.

The final report was published on June 25, 2021.

v. Rule Reviews

During the Reporting Period, thirteen IIROC rule amendments were approved or non-objected to by the IIROC RRs and three rule amendments were withdrawn by IIROC. Five rule amendments continue to be under CSA review as of December 31, 2021.{17}

vi. Materials Filed

IIROC is responsible for filing certain information with Staff on a regular or ad hoc basis. Required filings are outlined under the Recognition Orders and include, but are not limited to, items such as quarterly regulatory activities reports, quarterly and annual financial statements, internal audit and enterprise risk management reports, independent systems review reports, market activity statistics, exemptions granted from Universal Market Integrity Rules (UMIR), disclosure of members in financial difficulty, and terms and conditions on members.{18}

vii. Meetings and Other Discussions

During regular meetings held with IIROC, among other varied topics, the following key subjects were discussed and followed up on by CSA oversight staff:

• COVID-19 Response -- IIROC continued to function primarily on a remote basis as its staff have the tools, equipment and support necessary to execute IIROC's regulatory responsibilities. Compliance examinations continued on a fully remote basis with no significant delays regarding timing to complete the examinations. Within Enforcement, hearings and investigative interviews continued to be held by teleconference or video conference.

IIROC's market surveillance infrastructure continued to operate effectively. Pre-pandemic, system capacity and processing capability was set at 1 billion messages. In response to unprecedented market activity during the pandemic, which resulted in a significant increase in the daily average volume of trades and messages, and to ensure excess capacity during spikes in market activity, server and storage upgrades to the market surveillance system were completed. At the end of the Reporting Period, IIROC's SMARTS surveillance system had the ability to handle approximately 3 billion real-time messages per day and approximately 2 billion messages per day in the end-of-day processing.

During the pandemic, IIROC also received applications for exemptive relief relating to hardships experienced by dealers due to pandemic measures in place. Working with the CSA, IIROC operationalized a delegated authority model which enabled IIROC dealers to obtain specific relief from a sub-set of rules with set terms. An oversight mechanism was put in place for IIROC to provide timely information to the CSA to ensure proper oversight for as long as relief was provided under the model. The IIROC Board of Directors authorized staff to provide extensions of existing exemptive relief until March 31, 2022, provided that the Dealer Member was able to demonstrate that continued relief was warranted in the particular circumstances. A special section of the IIROC website was created to maintain all COVID-19 pandemic related information for stakeholders, which includes summaries of the exemptive relief applications and the exemptions granted.

• Order Execution Only (OEO) Service Levels -- As noted, there was a significant increase in trading volumes during the pandemic, including retail specific trading, partially attributable to the work-from-home environment and the ease of opening new trading accounts. Within the OEO platform, the impact of higher trading volumes and new account openings resulted in a corresponding increase in service level complaints from clients (e.g., delays in opening new accounts, system response times and service disruptions). Given the increasing importance of online trading services, IIROC collected quantitative and qualitative information from dealers with OEO trading platforms. A working group comprised of industry representatives and IIROC staff was also established to provide insight into key factors that could be considered as part of an appropriate regulatory response to this growing sector highly reliant on technology.

• Crypto / Digital Assets - A number of novel issues were identified during the review of applications for: (i) new membership from crypto-asset trading platforms; and (ii) business change from existing IIROC dealers planning on expanding into the distribution of crypto asset products and/or provision of service offerings. To better address these issues from an efficiency standpoint and to leverage knowledge and expertise of staff, IIROC created a Member Intake group in Summer 2021. This group is to be primarily responsible for the review and assessment of applications which are expected to increase in number. On November 17, 2021, Fidelity Clearing Canada ULC became the first IIROC dealer to be approved to offer trading and custody of crypto assets, based on specific terms and conditions. Reviews continue of other applications and business change notices. New IIROC rules and guidance, as well as standardized compliance procedures, are expected to be developed in the future. In the interim, IIROC continues to be engaged with staff at various levels on how IIROC rules and securities legislation apply to crypto-asset trading platforms, enabling targeted applications for exemption to be considered based on customized terms and conditions for each business model. A joint CSA/IIROC notice was published on March 29, 2021 providing guidance to crypto-asset trading platforms.

• Cybersecurity Incidents -- Pre-pandemic, IIROC conducted dealer cybersecurity self-assessment surveys, hosted table-top exercises to help small and medium sized firms with cybersecurity preparedness and risk management practices, and engaged cybersecurity consultants to visit selected dealers whose cybersecurity self-assessments revealed maturity levels below the expected target of their industry peer group. Furthermore, IIROC established a specific cybersecurity section on its website and provided webinars and published guidance to help dealers protect themselves and their clients against cyber threats. In November 2019, amendments to IIROC's reporting requirements were approved and implemented, requiring dealer members to report certain cybersecurity incidents to IIROC.{19} During the pandemic, cyber attacks increased across all industries, including the financial sector. In response, IIROC issued further guidance on how to prevent, detect, respond to and recover from ransomware attacks, and the Board approved future table-top exercises to discuss plans in the event of a ransomware attack. CSA staff were kept apprised of the IIROC initiatives and engaged with IIROC staff to ensure proper oversight.

• IIROC Information Processor Order - During the Reporting Period, in conjunction with the CSA, a long-standing project to provide post-trade transparency to the Canadian debt markets was finally achieved. On September 1, 2020, the CSA expanded IIROC's role as debt information processor to include government debt securities, in addition to corporate debt securities. The implementation of the expanded requirements took place in two phases. The first phase took effect on September 1, 2020, when IIROC started publishing post-trade information for trades in corporate and government debt securities executed the day prior by: (i) dealers subject to the requirements in current IIROC Rule 7200 Transaction Reporting for Debt Securities; and (ii) banks that are already reporting their corporate and government debt securities to IIROC. The second phase commenced during the Reporting Period on May 31, 2021, when IIROC started publishing information about all trades in corporate and government debt securities executed by those banks that were not already reporting such trades to IIROC.

• IIROC's Plain Language Rules (PLR) - Several years ago, IIROC started a project to rewrite, reformat, rationalize, and reorganize its Dealer Member Rules in plain language. Subsequent to public comments, CSA review and necessary approvals, the implementation of PLR took place on December 31, 2021, coinciding with the effective date of the implementation of the CSA's Client Focused Reforms (CFR){20}. As a result of the PLR project, the existing Dealer Member Rules, many of which originated in predecessor organizations{21}, were rewritten in plain language resulting in rules that are more clear, concise, and organized. The new rules are now referred to as the IIROC Rules.

• Client Focused Reforms - With the implementation of the CFR conflicts of interest requirements on June 30, 2021, the CSA, IIROC and the MFDA discussed a CFR conflicts of interest coordinated review. As part of these discussions, the CSA and both SROs harmonized their compliance modules specific to the CFR conflicts of interest requirements. IIROC added specific questions to the annual request of information from firms, a mechanism used by IIROC for data collection to assist in the assessment of compliance risk. IIROC also incorporated the CFR conflicts of interest review into its regularly scheduled business conduct compliance exams, and fieldwork began in the Reporting Period. In parallel with IIROC's and the MFDA's examination of its members, the CSA will be conducting a targeted CFR conflicts of interest sweep of other registrants. Together, the CSA, IIROC and the MFDA plan to publish findings from the coordinated review and provide additional implementation guidance to the industry on the enhanced conflict requirements.

• Other Initiatives - Over the Reporting Period, Staff also engaged IIROC staff on other specific matters of regulatory concern such as:

• the IIROC-sponsored test of the industry business continuity plan in October 2021;

• IIROC staff's participation in the CIPF insolvency simulation exercise (discussed further in the CIPF section below); and

• IIROC's specific investor protection initiatives, such as:

• proposed changes to IIROC's arbitration program;

• IIROC's research with past complainants;

• the return of disgorged funds to investors; and

• the development of the proposed Expert Investor Issues Panel.

(B) MFDA

i. Regulatory Status

The MFDA is the SRO that oversees mutual fund dealers in Canada, except in Québec where mutual fund dealers operating only in the province are directly regulated by the AMF.{22} The MFDA head office is in Toronto, with regional offices in Calgary and Vancouver.

ii. Member Firm Statistics

|

As at December 31 |

2021 |

2020 |

Change |

% Change |

|

|

||||

|

Total Mutual Fund Assets Under Administration |

$729B |

$627B |

$102B |

16.3% |

|

|

||||

|

Approved Persons |

77,383 |

77,195 |

188 |

0.2% |

|

|

||||

|

Members |

86 |

88 |

-2 |

-2.3% |

(Source: MFDA and NRD)

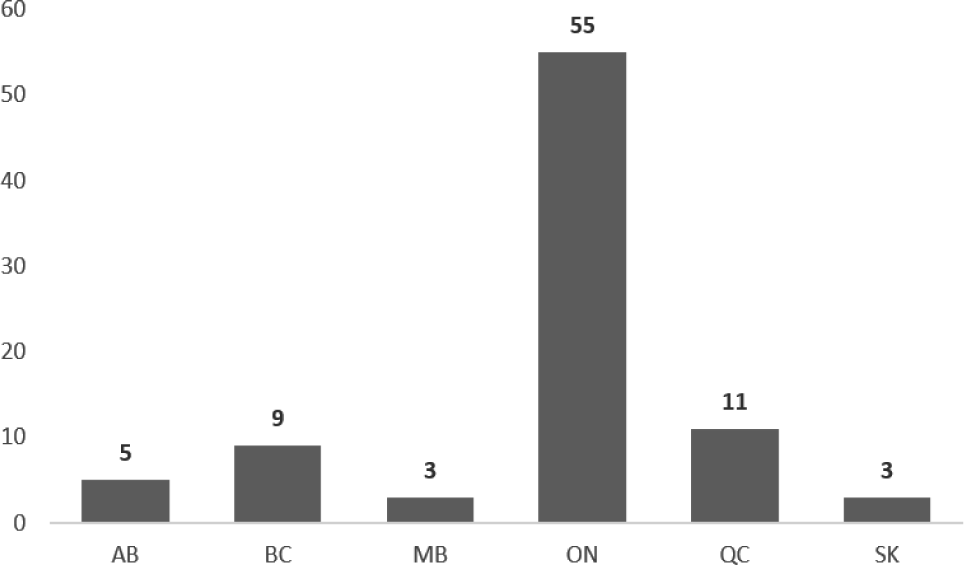

iii. MFDA Member Firms by Head Office Location

(Source: NRD)

iv. Rule Approvals

During the Reporting Period, four MFDA rule amendments were approved or non-objected to by the RRs that recognized the MFDA at the time of approval and two rule amendments were withdrawn by the MFDA. Three rule amendments continue to be under CSA review as of December 31, 2021.{23}

v. Materials Filed

The MFDA is also responsible for filing information with Staff on a regular and ad hoc basis. Required filings are outlined in the MFDA Recognition Orders and include (but are not limited to) annual and quarterly financial statements, disclosure of members in financial difficulty, and quarterly operations reports.{24}

vi. Oversight Review

Based on the annual risk assessment of the MFDA, Staff did not conduct an oversight review during the Reporting Period. Other CSA oversight activities are described below.

vii. Meetings and Other Discussions

During regular meetings with the MFDA, the following key topics, among other varied subjects, were discussed and followed up on:

• COVID-19 Response -- Near the outset of the pandemic, Staff became aware of a process followed by the MFDA of granting regulatory relief to members as a result of disruptions in business operations caused by the COVID-19 pandemic. In reviewing the process, Staff focused their assessment on the MFDA's process in granting such relief, rather than questioning whether the particular relief granted was appropriate or necessary in the circumstances. In particular, Staff queried the MFDA's (i) characterization of the relief as an "administrative accommodation"; (ii) the delegation to MFDA staff of the ability to grant such relief; and (iii) the lack of public transparency regarding the availability or details of the relief. During the Reporting Period, Staff continued to follow up with the MFDA in terms of internal processes and procedures in place to ensure that, when MFDA staff engage in discussions with member(s) that result in the exercise of discretion on MFDA staff's part, those discussions and decisions are within the scope of their authority (i.e. not exercising exemptive relief), and that MFDA staff's reasons for providing administrative accommodations are properly documented.

With respect to the impact of COVID-19 on operations, during the Reporting Period, the MFDA continued to primarily carry on its functions remotely, including its core compliance and enforcement functions. While the MFDA suspended its onsite compliance fieldwork during the Reporting Period, it continued to perform compliance examinations remotely. The MFDA also continued to conduct its enforcement activities remotely using virtual technologies and other means to facilitate the participation of relevant parties in the MFDA's enforcement processes, but it has indicated a willingness to facilitate in-person processes, as necessary and appropriate. The MFDA continued to accept, review and respond to complaints or inquiries from the public. The level of complaints received by the MFDA has returned to pre-pandemic levels after a temporary spike in late March and April 2020. The MFDA continued to monitor the pandemic and act in accordance with local government instructions to guide its plan for returning staff to the office.

• Cybersecurity -- Cybersecurity for both the MFDA and its members continues to be an area of focus. The MFDA engaged external IT consultants to perform various tests of its own security controls and assess the maturity of its cybersecurity framework. The results of these tests were provided to Staff. In May 2021, the MFDA issued a mandatory cybersecurity survey to all its members. Preliminary results demonstrated that smaller members tended to have resource issues in dealing with cybersecurity; however, due to regulatory requirements and the high threat pressure on the financial services industry, even smaller MFDA members were deemed to be more prepared and invested in cyber protection than similar-sized entities in other sectors. The survey identified some key areas for which the MFDA intends to provide additional guidance and resources.

• Client Research Project -- The 2016 and 2019 MFDA Client Research Project provided the MFDA with information and insight into members' business models, their approved persons and their clients. In the beginning of the Reporting Period, the MFDA, in collaboration with the AMF, issued a mandatory data request to all its members, requiring that client data be provided by June 30, 2021. The MFDA has assessed the accuracy and completeness of the data, and is now working with research consultants to perform an analysis and summarize the results in a report.

• Client Focused Reforms -- As part of regular member examinations, the MFDA commenced its review of member firms' compliance with the enhanced CFR conflicts of interest requirements. As discussed above, the MFDA will use the information gathered from its examinations to participate with the CSA and IIROC in a coordinated review of the implementation of the new conflict requirements by firms. The group plans to publish its findings and provide additional implementation guidance to the industry.

• Performance Reporting Targeted Review -- In 2020, the MFDA commenced a targeted review focused on performance data reported to clients by MFDA members. While the MFDA regularly tests performance reporting as part of routine compliance examinations, data obtained from the 2019 Client Research Project allowed the MFDA to conduct a targeted review of performance reporting, specifically focused on accounts with highly unusual positive or negative returns. A report was issued in July 2021. Among the key recommendations in the report were: (i) for members to carefully review and test their annual performance reporting, as inaccurate reporting can impact their clients' investment decisions; and (ii) where members identify inaccurately reported performance returns, members should provide each affected client with a restated performance report for the time periods that were incorrectly reported.

• Continuing Education - In 2019, the CSA approved or non-objected to the introduction of Continuing Education (CE) requirements for mutual fund approved persons. In July 2021, the CSA also approved or non-objected to amendments to establish a CE accreditation process. The CE cycle commenced in December 2021. During the Reporting Period, to ensure the stability and adequacy of the CE system, the MFDA contracted third-party specialists to successively review, test, identify and remedy potential concerns with the new MFDA CE reporting and tracking system (CERTS) prior to launch. A separate section relating to Continuing Education has been added to the MFDA website to consolidate information for ease of reference.

(C) CIPF

i. Regulatory Status

CIPF is approved as an IPF to provide protection within prescribed limits to eligible clients of IIROC dealer member firms suffering losses, if client property held by a member firm is unavailable as a result of the insolvency of a dealer member.{25} CIPF's head office is in Toronto.

ii. Fund Statistics

|

As at December 31 |

2021 |

2020 |

Change |

% Change |

|

|

||||

|

General Fund |

$540M |

$544M |

-$4M |

-0.7% |

|

|

||||

|

Insurance |

$440M |

$440M |

- |

- |

|

|

||||

|

Lines of Credit |

$125M |

$125M |

- |

- |

|

|

||||

|

Total |

$1,105M |

$1,109M |

$4M |

-0.4% |

(Source: 2021 CIPF Audited Annual Financial Statements)

iii. Oversight Review

Based on the 2021 annual risk assessment, Staff did not conduct a risk-based oversight review of CIPF during the Reporting Period. Other CSA oversight activities are described below.

iv. Policy and Procedures Amendments

During the Reporting Period, the CIPF ARs did not object to amendments to the CIPF Claims Procedures.

v. Meetings and Other Discussions

During the semi-annual meetings held with CIPF, the following key topics were discussed and followed up on:

• COVID-19 Response - During the Reporting Period, CIPF's office continued to operate remotely, and meetings of the CIPF Board and its Committees were carried on virtually.

• Statement of Member Assets by Location (SMAL) - While the filing of the annual SMAL was suspended in 2020 to accommodate the management and operational challenges faced by member firms due to the COVID-19 pandemic, the requirement to file resumed during the Reporting Period.

• SRO Structure - On March 31, 2021, CIPF published its discussion paper The Independence of Compensation Funds, which considered whether CIPF should remain an independent body or be integrated with a future SRO. Subsequently, the CSA Position Paper recommended the creation of a combined protection fund, separate from the new SRO. CIPF and MFDA IPC staff are working through the integration process and, given that many aspects of their operations are similar such as how liquidity resources are structured, CSA staff expect that this will facilitate the combination of the two entities into the new IPF.

• Review of Adequacy of Level of Assets, Assessment Amounts and Assessment Methodology - CIPF uses a credit-risk based fund model to project its liquidity resource requirement and assist in the setting of its fund size. During the Reporting Period, CIPF's Board reviewed the adequacy of the level of resources available in relation to the risk exposure of member firms. CIPF continued to implement enhancements to its model with: (i) the recalibration of a stress multiplier; and (ii) implementation of a five-year weighted average methodology, in order to mitigate potential volatility to the liquidity resource requirements.

• Crypto Assets - During the Reporting Period, staff from IIROC, CIPF and the CSA met regularly to discuss crypto asset developments, including the review by the CSA and IIROC of applications from crypto asset trading platforms for registration and membership and for exemptive relief from certain requirements in securities legislation and IIROC's rules. The primary areas of interest for CIPF were the custody, control and pricing of crypto assets.

• Simulation Exercises -- Three simulation exercises were held during the Reporting Period. Two simulation exercises were held with regulatory and clearinghouse staff in February and October 2021. These simulations focused on the manner in which operational strategies, tools and regulatory processes changed during the pandemic (e.g., the use of virtual hearing panels), and how these changes could impact the handling of a member firm insolvency. The third simulation was organized by CIPF for trustees in April 2021. Since the pool of trustees and lawyers who specialize in financial institution bankruptcies is limited, the goal of this simulation was to expand industry knowledge. Future simulation exercises are being scheduled.

• Insolvencies -- During the Reporting Period, there were no IIROC member insolvencies whereby CIPF was actively involved.

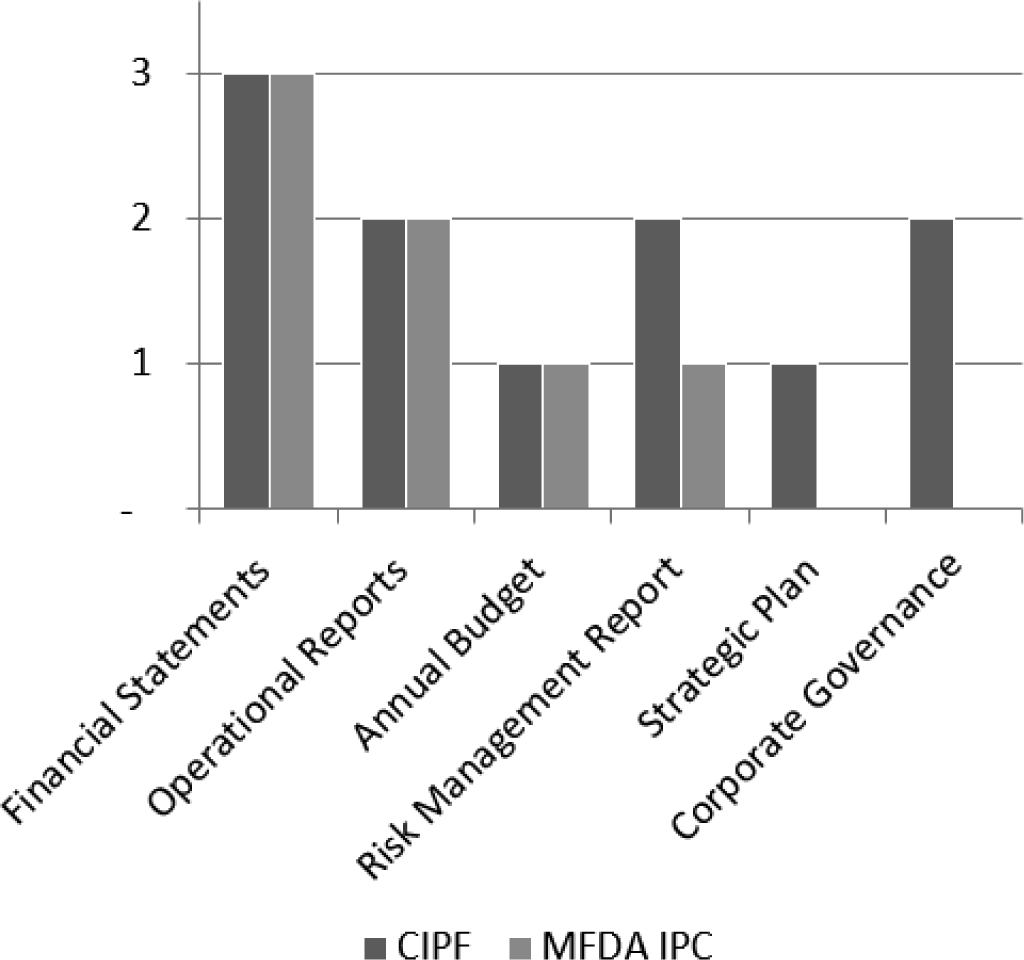

• New Reporting Requirements - As of January 2021, the new updated CIPF Approval Orders came into effect. Filings received under the new Approval Orders for the Reporting Period included the unaudited semi-annual financial statements as at June 30, 2021 and December 31, 2021, the annual and semi-annual operational reports, and 2022 financial budget.{26} Staff worked with CIPF staff to ensure a smooth transition to the updated reporting requirements.

(D) MFDA IPC

i. Regulatory Status

The MFDA IPC is approved as an IPF to provide protection within prescribed limits to eligible clients of MFDA mutual fund dealer member firms suffering losses as a result of the insolvency of a mutual fund dealer member.{27} The MFDA IPC's head office is in Toronto.

ii. Fund Statistics

|

As at June 30 |

2021 |

2020 |

Change |

% Change |

|

|

||||

|

General Fund |

$53M |

$51M |

$2M |

3.9% |

|

|

||||

|

Insurance |

$40M |

$20M |

$20M |

100.0% |

|

|

||||

|

Lines of Credit |

$30M |

$30M |

- |

- |

|

|

||||

|

Total |

$123M |

$101M |

$22M |

21.8% |

(Source: 2021 MFDA IPC Audited Annual Financial Statements)

iii. Oversight Review

Based on the 2021 annual risk assessment, Staff did not conduct a risk-based oversight review of the MFDA IPC during the Reporting Period. Other CSA oversight activities are described below.

iv. Meetings and Other Discussions

During semi-annual meetings held with the MFDA IPC, the following key topics were discussed:

• COVID-19 Response - MFDA IPC staff continued to work and hold Board meetings remotely and remain equipped with the necessary access and tools to do so. The MFDA IPC relies on the MFDA (through the Services Agreement) for its continued support of certain MFDA IPC services and thus was in close coordination with MFDA during COVID-19.

• Fund Size Target -- The Board of the MFDA IPC oversees the enhancement of the annual review of the general fund size and monitors the ongoing stability of this fund. The MFDA IPC has reached its general fund size target of $50 million. In 2021, the MFDA IPC added a secondary layer of insurance in the amount of $20M in respect of any losses to be paid by the MFDA IPC in excess of $50M. This is in addition to the original layer of insurance of $20M in respect of any losses to be paid by the MFDA IPC in excess of $30M.

• Insolvencies -- There were no MFDA member insolvencies during the Reporting Period whereby the MFDA IPC was actively involved. Information related to the W.H. Stuart insolvency (2013) is still available on the MFDA IPC website as MFDA IPC staff received some queries during the Reporting Period.

• Simulation Exercise - During the Reporting Period, MFDA IPC staff conducted a simulation exercise for its Board to go through the key events that would take place in an insolvency and the key decisions requiring Board involvement. External legal counsel and third-party consultants helped to facilitate the exercise.

• Governance -- Following the risk assessment in 2020 and with a view to further strengthen MFDA IPC's governance controls, Staff recommended and the MFDA IPC agreed to implement a code of conduct for the MFDA IPC staff, aimed to help mitigate any potential conflicts of interest. This is important given the MFDA IPC's integration with the MFDA (e.g., shared accounting resource). The new code of conduct was implemented during the Reporting Period.

• New Reporting Requirements - As of January 2021, the new updated MFDA IPC Approval Orders came into effect. Staff worked with the MFDA IPC to ensure a smooth transition to the updated reporting requirements.{28}

{1} Recognition Orders set out the authority of IIROC and the MFDA.

{2} Two separate MOUs describe how the RRs will oversee IIROC and the MFDA.

{3} Approval Orders provide CIPF and the MFDA IPC with the authority to carry out their mandates.

{4} In Québec, CIPF is an accepted investor protection fund.

{5} Two separate MOUs describe how the ARs will oversee CIPF and the MFDA IPC.

{6} As described in CSA Position Paper 25-404 New Self-Regulatory Organization Framework

{7} In Québec, mutual fund dealers are directly regulated by the AMF and registered individuals in the category of mutual fund representatives must also be members the Chambre de la sécurité financière. Newfoundland and Labrador is considering the recognition of the MFDA.

{8} More information about the current membership of the Committee and sub-committees (IIROC and MFDA) is provided in Appendix 2.

{9} The British Columbia Securities Commission (BCSC) is the Principal Regulator for the MFDA, and the Ontario Securities Commission (OSC) is the Principal Regulator for IIROC, CIPF and the MFDA IPC.

{10} The 2021 annual in-person meetings have been postponed due to the ongoing COVID-19 pandemic.

{11} Pre-pandemic oversight reviews could be desk or onsite reviews. Upon the return to the office, we expect oversight reviews to integrate both desk and onsite features (hybrid), leveraging technology as needed.

{12} Details of the approved/withdrawn/outstanding rules are provided in Appendix 2.

{13} "Rules" in this chart also refers to amendments to IIROC and MFDA by-laws, and CIPF policies and procedures.

{14} There were no outstanding or new proposed policies or by-law amendments pertaining to the MFDA IPC during the Reporting Period.

{15} Further details of these materials filed are provided in Appendix 3.

{16} IIROC is recognized by the Alberta Securities Commission (ASC), the AMF, the BCSC, the Financial and Consumer Affairs Authority of Saskatchewan (FCAA), the Financial and Consumer Services Commission of New Brunswick (FCNB), the Manitoba Securities Commission (MSC), the Nova Scotia Securities Commission (NSSC), the Office of the Superintendent of Securities Service Newfoundland and Labrador (NL), the OSC, the Prince Edward Island Office of the Superintendent of Securities Office (PEI), the Northwest Territories Office of the Superintendent of Securities, the Nunavut Securities Office, and the Office of the Yukon Superintendent of Securities (collectively, the IIROC RRs).

{17} More information about IIROC rule approvals is provided in Appendix 2.

{18} Further details about materials filed by IIROC (other than rule amendments) is provided in Appendix 3.

{19} In February 2022, IIROC issued further guidance to Dealer Members on how to demonstrate compliance with the cybersecurity incident reporting requirements.

{20} The new requirements under the Client Focused Reforms came into effect on December 31, 2021 (know your client, know your product, suitability, relationship disclosure information, and all other reforms). Amendments relating to the conflicts of interest requirements came into effect earlier on June 30, 2021.

{21} IIROC was recognized as an SRO effective June 1, 2008, combining the operations of the Investment Dealers Association and Market Regulation Services Inc.

{22} The MFDA is currently recognized by ASC, AMF, BCSC, FCAA, FCNB, MSC, NSSC, OSC, PEI, the Northwest Territories Office of the Superintendent of Securities, the Nunavut Securities Office, and the Office of the Yukon Superintendent of Securities.

{23} More information about MFDA rule approvals is provided in Appendix 2.

{24} Further details about the materials filed by the MFDA (other than rule amendments) are provided in Appendix 3

{25} CIPF is deemed acceptable or approved as an IPF by the AMF, ASC, BCSC, FCAA, FCNB, MSC, NL, NSSC, OSC, PEI, the Northwest Territories Office of the Superintendent of Securities, the Nunavut Securities Office, and the Office of the Yukon Superintendent of Securities (collectively, the CIPF ARs).

{26} Further details about materials filed by CIPF (other than rule amendments) are provided in Appendix 3.

{27} The MFDA IPC is currently approved as an IPF by the ASC, BCSC, FCAA, FCNB, MSC, NSSC, OSC, PEI, the Northwest Territories Office of the Superintendent of Securities, the Nunavut Securities Office, and the Office of the Yukon Superintendent of Securities. The MFDA IPC operates in all provinces except Québec, which has its own compensation fund.

{28} Further details of the materials filed by the MFDA IPC is provided in Appendix 3.

APPENDIX 1 -- COMPOSITION OF THE SRO OVERSIGHT COMMITTEES

MARKET REGULATION STEERING COMMITTEE

|

AMF |

Elaine Lanouette |

FCNB |

David Shore |

|

|

|||

|

ASC |

Lynn Tsutsumi |

NL |

Scott Jones |

|

|

|||

|

BCSC |

Mark Wang |

NSSC |

Chris Pottie |

|

|

|||

|

FCAA |

Liz Kutarna |

OSC |

Susan Greenglass |

|

|

|||

|

MSC |

Paula White |

PEI |

Steve Dowling |

IIROC OVERSIGHT COMMITTEE

|

AMF |

Dominique Martin |

Serge Boisvert |

Jean-Simon Lemieux |

|

|

|||

|

|

Catherine Lefebvre |

Lucie Prince |

Herman Tan |

|

|

|||

|

ASC |

Rose Rotondo |

Gerald Romanzin |

|

|

|

|||

|

BCSC |

Mark Wang |

Michael Brady |

Liz Coape-Arnold |

|

|

|||

|

|

Michael Grecoff |

Sylvia Lee |

Joseph Lo |

|

|

|||

|

|

Zach Masum |

Meg Tassie |

|

|

|

|||

|

FCAA |

Liz Kutarna |

Curtis Brezinski |

|

|

|

|||

|

FCNB |

David Shore |

Amelie McDonald |

|

|

|

|||

|

MSC |

Paula White |

Angela Duong |

|

|

|

|||

|

NL |

Scott Jones |

|

|

|

|

|||

|

NSSC |

Chris Pottie |

Angela Scott |

|

|

|

|||

|

NT |

Matthew Yap |

|

|

|

|

|||

|

NU |

Shamus Armstrong |

|

|

|

|

|||

|

OSC |

Joseph Della Manna |

Karin Hui |

Stacey Barker |

|

|

|||

|

|

Yuliya Khraplyva |

Ruxandra Smith |

Bryana Lee |

|

|

|||

|

|

Felicia Tedesco |

|

|

|

|

|||

|

PEI |

Steve Dowling |

Curtis Toombs |

|

|

|

|||

|

YK |

Rhonda Horte |

|

|

MFDA OVERSIGHT COMMITTEE

|

ASC |

Rose Rotondo |

Gerald Romanzin |

|

|

|

|||

|

BCSC |

Mark Wang |

Michael Brady |

Joseph Lo |

|

|

|||

|

|

Liz-Coape-Arnold |

Anne Hamilton |

Lenworth Haye |

|

|

|||

|

|

Zach Masum |

|

|

|

|

|||

|

FCAA |

Liz Kutarna |

Curtis Brezinski |

|

|

|

|||

|

FCNB |

David Shore |

Amelie McDonald |

|

|

|

|||

|

MSC |

Paula White |

Angela Duong |

|

|

|

|||

|

NSSC |

Chris Pottie |

Brian Murphy |

|

|

|

|||

|

NT |

Matthew Yap |

|

|

|

|

|||

|

NU |

Shamus Armstrong |

|

|

|

|

|||

|

OSC |

Joseph Della Manna |

Yuliya Khraplyva |

Karin Hui |

|

|

|||

|

|

Stacey Barker |

Felicia Tedesco |

Dimitri Bollegala |

|

|

|||

|

PEI |

Steve Dowling |

Curtis Toombs |

|

|

|

|||

|

YK |

Fred Pretorius |

Rhonda Horte |

|

CIPF OVERSIGHT COMMITTEE

|

AMF |

Dominique Martin |

Lucie Prince |

|

|

|

|||

|

ASC |

Rose Rotondo |

Gerald Romanzin |

|

|

|

|||

|

BCSC |

Michael Brady |

Sylvia Lee |

Joseph Lo |

|

|

|||

|

|

Meg Tassie |

|

|

|

|

|||

|

FCAA |

Liz Kutarna |

Curtis Brezinski |

|

|

|

|||

|

FCNB |

David Shore |

|

|

|

|

|||

|

MSC |

Paula White |

Angela Duong |

|

|

|

|||

|

NL |

Scott Jones |

|

|

|

|

|||

|

NSSC |

Chris Pottie |

Angela Scott |

|

|

|

|||

|

NT |

Matthew Yap |

|

|

|

|

|||

|

NU |

Shamus Armstrong |

|

|

|

|

|||

|

OSC |

Joseph Della Manna |

Stacey Barker |

Karin Hui |

|

|

|||

|

|

Yuliya Khraplyva |

|

|

|

|

|||

|

PEI |

Steve Dowling |

Curtis Toombs |

|

|

|

|||

|

YK |

Fred Pretorius |

Rhonda Horte |

|

MFDA IPC OVERSIGHT COMMITTEE

|

ASC |

Rose Rotondo |

Gerald Romanzin |

|

|

|

|||

|

BCSC |

Mark Wang |

Michael Brady |

Anne Hamilton |

|

|

|||

|

|

Joseph Lo |

Zach Masum |

Meg Tassie |

|

|

|||

|

FCAA |

Liz Kutarna |

Curtis Brezinski |

|

|

|

|||

|

FCNB |

David Shore |

|

|

|

|

|||

|

MSC |

Paula White |

Angela Duong |

|

|

|

|||

|

NL |

Scott Jones |

|

|

|

|

|||

|

NSSC |

Chris Pottie |

Brian Murphy |

|

|

|

|||

|

NT |

Matthew Yap |

|

|

|

|

|||

|

NU |

Shamus Armstrong |

|

|

|

|

|||

|

OSC |

Joseph Della Manna |

Stacey Barker |

Karin Hui |

|

|

|||

|

|

Yuliya Khraplyva |

|

|

|

|

|||

|

PEI |

Steve Dowling |

Curtis Toombs |

|

|

|

|||

|

YK |

Fred Pretorius |

Rhonda Horte |

|

APPENDIX 2 -- RULE/BY-LAW/POLICY AND PROCEDURES AMENDMENTS

IIROC Rule/By-Law Amendments

Completed

1. Amendments to Dealer Member Rules and Form 1 Regarding the Securities Concentration Test and Designated Rating Organizations

2. Amendments to the Risk Component of IIROC's Dealer Member Fee Model

3. Amendments Regarding Exemptions for Bulk Account Movements

4. Housekeeping Amendments to Form 1 for Use In, and Consistency With, the IIROC Rules

5. Amendment to IIROC By-law No. 1 Regarding the Definition of "Marketplace"

6. Housekeeping Amendments to Dealer Member Rules and IIROC Rules as Related to IIROC Notices 19-0071 and 19-0101

7. Amendments to Swap Counterparty Margin Requirements

8. Client Focused Reforms Rule Amendments

9. Housekeeping Amendments to IIROC Rules to Enhance Protection of Older and Vulnerable Clients

10. Amendments to Form 1 and Corollary Amendments to the IIROC Rules

11. Housekeeping Rule Changes to the IIROC Rules

12. Housekeeping Amendments to the Universal Market Integrity Rules (UMIR) Regarding the Definition of "Marketplace"

13. Housekeeping Amendments to the Universal Market Integrity Rules (UMIR) to Update Reference to IIROC Rules

Withdrawn

1. Proposed Amendments Respecting Non-Clients

2. Proposed Amendments Respecting the Minor Contravention Program and Early Resolution Offers

3. Proposed Amendments Respecting Disclosure of Information by Ombudsman Service to IIROC

In Progress

1. Proposed Derivatives Rule Modernization, Stage 1

2. Proposed Amendments Respecting the Trading of Derivatives on a Marketplace

3. Proposed Margin Requirements for Structured Products

4. Proposed Amendments to the IIROC Rules and Form 1 Relating to the Futures Segregation and Portability Customer Protection Regime

5. Proposed Amendments Respecting Reporting, Internal Investigation and Client Complaint Requirements

MFDA Rule/By-Law Amendments

Completed

1. Amendments to MFDA Rule 1.1.1(a) (Business Structures -- Members)

2. Amendments to MFDA Policy No. 9 Continuing Education ("CE") Requirements

3. Client Focused Reforms Rule Amendments

4. Housekeeping Amendments to MFDA Rules to Enhance Protection of Older and Vulnerable Clients

Withdrawn

1. Proposed Amendments to MFDA Rule 1.2.5 (Misleading Business Titles Prohibited)

2. Proposed Amendments to MFDA Rule 2.3.1(b) (Discretionary Trading) and Rule 2.2.5 (Relationship Disclosure)

In Progress

1. Proposed Amendments to MFDA Rule 1.1.2 (Compliance by Approved Persons)

2. Proposed Amendments to MFDA Rule 2.3.2 (Limited Trading Authorization) and Rule 2.3.3 (Designation)

3. Proposed New MFDA Policy No. 11 Proficiency Standards for the Sale of Alternative Mutual Funds

CIPF Policies and Procedures/By- Law Amendments

Completed

1. Housekeeping Amendments to CIPF Claims Procedures.

APPENDIX 3 -- OTHER MATERIALS FILED

SRO Filings During the Reporting Period

(1) Ad hoc filings include, for example, notifications about dealer members in financial distress, cybersecurity breaches and significant exemption requests.

(2) Other filings include, for example, publications and miscellaneous reports.

IPF Filings During the Reporting Period

Questions

If you have any questions or comments about this CSA Staff Notice, please contact any of the following:

Sasha Cekerevac

Dominique Martin

Manager, Market Oversight

Director, Oversight of Trading Activities

Alberta Securities Commission

Autorité des marchés financiers

403-297-7764

514-395-0337, ext. 4351 or 1-877-395-0337, ext. 4351

Jean-Simon Lemieux

Michael Brady

Senior Analyst

Deputy Director, Capital Markets Regulation

Autorité des marchés financiers

British Columbia Securities Commission

514-395-0337, ext. 4366 or 1-877-395-0337, ext. 4366

604-899-6561

Curtis Brezinski

David Shore

Compliance Auditor, Capital Markets Securities Division

Senior Legal Counsel

Financial and Consumer Affairs Authority of Saskatchewan

Financial and Consumer Services Commission (New Brunswick)

306-787-5876

506-658-3038

Paula White

Chris Pottie

Deputy Director, Compliance and Oversight

Deputy Director, Registration & Compliance

Manitoba Securities Commission

Nova Scotia Securities Commission

204-945-5195

902-424-5393

Joseph Della Manna

Stacey Barker

Manager, Market Regulation

Senior Accountant, Market Regulation

Ontario Securities Commission

Ontario Securities Commission

416-204-8984

416-593-2391