CSA Staff Notice 25-306 Activist Short Selling Update

CSA Staff Notice 25-306 Activist Short Selling Update

Part 1. Introduction

On December 3, 2020, the Canadian Securities Administrators (CSA or we) published CSA Consultation Paper 25-403 Activist Short Selling (Consultation Paper) for a 90-day consultation period. The purpose of the Consultation Paper was to facilitate discussion relating to activist short selling and its potential impact on Canadian capital markets. We received 23 comment letters and thank all those who provided comments. A summary of comments and responses is attached at Appendix A. Since the Consultation Paper was published, we have also conducted informal discussions and consultations with various regulatory advisory committees and industry groups. We have actively monitored international developments related to short selling, including those directly relevant to activist short selling.

Part 2. Executive Summary

Our consultations and comments received in response to the Consultation Paper show that there continue to be negative views associated with activist short selling and, in general, with short selling. This perception is primarily held by issuers targeted in recent campaigns. Some stakeholders believe that changes to the regulatory requirements should be considered to address perceived problems with short selling, including activist short selling. Some commenters acknowledge there are positive aspects of activist short selling, particularly its contribution to price discovery.

We acknowledge the continued and persistent negative perception of short selling and the concerns some stakeholders have with the existing regulatory regime for short selling. Today, we are also publishing Joint CSA-IIROC Staff Notice 23-329 Short Selling in Canada (Joint CSA-IIROC Staff Notice 23-329) to seek feedback on general short selling issues and the existing regulatory framework. We encourage market participants and other stakeholders to provide comments on this notice. The feedback we receive will inform any future regulatory initiatives in this area.

At the same time, CSA staff, through its existing committees, continues to monitor and analyze activist short selling initiatives, and short selling in general, to understand whether there are gaps in the regulatory regime that need to be addressed to ensure investor protection and foster fair and efficient capital markets. In particular, we:

• continue to enforce securities legislation provisions relevant to activities of dishonest activist short sellers, including misrepresentation, fraud and market manipulation;

• monitor the number of activist short selling campaigns and review trends and campaign statistics;

• review complaints regarding activist short selling and possible manipulation in the regular course;

• monitor other domestic initiatives including, most importantly, the ongoing failed trades study conducted by the Investment Industry Regulatory Organization of Canada (IIROC) to see whether the findings support regulatory initiatives that may impact activist short selling; and

• monitor international short selling initiatives.

Part 3. Recent Developments

Since the publication of the Consultation Paper, there have been several developments that are relevant to short selling and activist short selling. We outlined them below and discussed them in more detail in Joint CSA-IIROC Staff Notice 23-329.

a. IIROC's Failed Trades Study

As highlighted in its public priorities,{1} IIROC conducted a failed trades study which analyzed data provided by the Canadian Depository for Securities (CDS) to take an in-depth look at the settlement process and the handling of fails to identify whether any systemic issues exist. IIROC last studied settlement fails in 2007, but this was done using limited data. IIROC updated this study with recent data covering a five-year period, in part to reassess the results of their previous study and to determine whether there is a connection between failed trades and short selling or other administrative causes. Joint CSA-IIROC Staff Notice 23-329 includes a high-level overview of the findings from this study. IIROC Notice 22-0190, also published today, provides additional detail.

b. Recent Activist Short Selling Activity

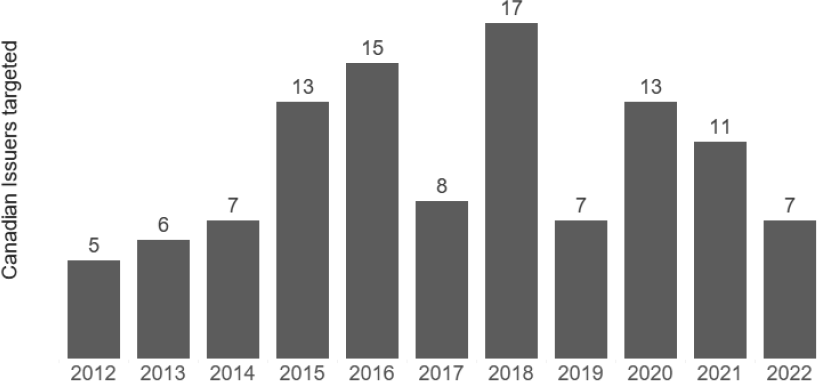

Figure 1 below shows the annual number of Canadian issuers that have been targeted by prominent activist short sellers between 2012 and 2021.{2} As of October 7th, 2022, seven Canadian issuers have been the target of activist short seller campaigns since the start of the year. Over the same period, 50 US issuers have also been targeted by activist short sellers.

Figure 1 -- Annual Number of Canadian Issuers targeted by Activist Short Sellers (Note: the count for 2022 is as of October 7, 2022)

Contrasting these statistics with the total number of listed issuers in Canada, we observe that annually, less than 1% of all Canadian issuers have been the target of activist short selling campaigns.{3} In comparison, 3% of all U.S issuers and less than 0.5% of Australian issuers have been the target of similar activist short selling campaigns.

Part 4. Themes from the Consultation Paper

a. Commenters

We received 23 comment letters on the Consultation Paper from stakeholders that included:

• Seven issuers;{4}

• Four full-service business law firms;

• Seven industry groups;

• One exchange;

• One asset management company;

• One investment dealer;

• One financial advisory firm; and

• One individual.

We attached the summary of comments and the CSA's responses at Appendix A. We did not receive, through the public comment process or through outreach to retail investor groups, feedback from retail investor representatives.{5} Similarly, we did not receive comments from activist short sellers, although the asset management company that commented indicated that it had, in the past, participated in activist short selling campaigns.

b. Themes from comments received

The Consultation Paper focused on issues identified through CSA staff's research and solicited feedback from stakeholders, supported by evidence, whenever possible, on specific questions. The purpose was to further inform our analysis of the issues and to ensure that the CSA had all the relevant information before determining whether regulatory intervention is required. The topics in the Consultation Paper included:

• the nature and extent of activist short selling activity in Canada;

• the Canadian and international regulatory framework; and

• issues related to enforcement and other potential remedial actions.

Several themes emerged from the comments on the Consultation Paper:

(i) use of social media;

(ii) perception versus evidence;

(iii) the short selling regulatory regime; and

(iv) need for regulatory change.

Each of these themes will be further discussed below.

(i) Use of Social Media

While the Consultation Paper did not specifically focus on the impact of social media or other shared information platforms on capital markets, commenters raised many concerns related to the use of social media.

We acknowledge that social media has created an environment for investors, companies, dealers, advisers and other intermediaries to have access to an unprecedented amount of information and disinformation. The speed at which this information is conveyed and responded to, as well as questions about the accuracy and reliability of the information, are of significant concern. The CSA recognizes that social media can present challenges when used for sharing information with the market{6} and has cautioned investors to consider the source of information and advice when making investments decisions.{7}

These concerns were reiterated by commenters, particularly with respect to the speed of today's communication technologies which can cause damage to an issuer's reputation and valuation before the issuer has an opportunity to respond. Some commenters also focussed on the need for laws to ensure social media platforms preserve evidence for review and identification, particularly where the activist short seller relies on a pseudonym.{8} It should also be noted that commenters who had a negative perception towards activist short sellers did not distinguish the actions of anonymous activists as being more problematic than named ones.

We acknowledge that social media platforms are a significant data source in today's markets. We also note that there are current challenges with accessing data from some platforms and with parsing unstructured social media data to clearly identify activist short sellers from other users that may only be expressing a negative opinion. We see that industry participants are planning to monitor online platforms more closely, including for risk management and investor relation purposes. Off-the-shelf and custom-built surveillance tools are in development that would parse through social media. Issuers are starting to actively monitor social media platforms for comments, including those made by activist short sellers, and may respond to negative statements.{9} IIROC has also indicated that their surveillance alert workflow includes basic social media scans, including in circumstances when there is no relevant news to explain any unusual market activity.{10}

The problematic conduct observed in connection with the use of social media or other online platforms is not unique to activist short selling, but rather it can be seen as part of a broader trend in the market. Issuers, investors and activists (both long and short) increasingly rely on online platforms to promote their views. Unlike issuers and certain shareholders who are subject to specific securities law requirements on the long side, activist short sellers are not subject to any specific regulatory framework. The regulatory requirements applicable to activist short selling are limited to the general provisions applicable to all market participants, including prohibitions against fraud and market manipulation, the dissemination of false and misleading statements, and trading with knowledge of undisclosed material information. We acknowledge that this may create a perception of imbalance from a regulatory framework perspective. We note, however, that the purpose of regulation of public disclosure by issuers is to address the information asymmetry that may exist between an issuer's insiders and the market and to help price securities accurately. Activist short sellers do not generally have access to non-public information.

That said, there are initiatives such as the recent B.C. Securities Act amendments and proposed section 94(1) False or misleading statements, information about reporting issuers of the proposed Capital Markets Act (Ontario) which could help address the risk of dissemination of false and misleading statements and would capture those made through social media and would apply to statements made by activist short sellers. These are discussed in more detail below.

(ii) Perception versus Evidence

In the Consultation Paper, we published the results of CSA staff's research on activist short selling. We did not identify widespread market abuse related to activist short selling through our research and requested that commenters provide new sources of information or data that we could consider in determining whether there is evidence of systemic abusive related to activist short selling activities.

Based on the comments received, we are of the view that we considered all relevant sources of information when conducting our research. However, the comments highlighted that stakeholders such as issuers, law firms and related industry groups continued to see activist short selling in a negative light, with many believing that problematic conduct permeates this type of activity and that additional regulatory measures are necessary. Other market participants, however, noted the beneficial aspects of activist short selling. This latter group recognized that activist short sellers can play an important check and balance on the higher propensity for promotional information that exists in the market and may be the only voice expressing a "sell" recommendation where their research warrants. These stakeholders cited the lack of evidence of problematic activity as a reason against the introduction of regulatory measures and cautioned that new measures could potentially curtail or deter legitimate activity and negatively impact markets.

We agree that, to the extent any regulatory measures are considered, such measures should be tied to evidence of problematic conduct with activist short selling and consideration be given to potential impacts on the activity, including any unintended consequences on market efficiency and the price discovery process. The CSA have access to information regarding activist short selling campaigns. Should we see evidence that regulatory changes are needed, they would be considered.

(iii) The Short Selling Regulatory Regime

Many of the comment letters focussed on the short selling regime in general and raised some concerns that were not specific to the activist short selling issues raised in the Consultation Paper.{11} The views expressed by commenters included:

• concerns with perceived "naked" short selling and the need to impose pre-borrow requirements;

• potential harm caused by short selling in connection with prospectus offerings and private placements;

• a perceived negative impact that resulted from the removal of the tick test{12} in 2012 and a recommendation to consider adopting a regulation similar to the modified uptick rule of the Securities and Exchange Commission (SEC);{13} and

• inadequate frequency and disclosure of short selling positions and identities (unlike the European Union or Australia).

We acknowledge the concerns raised. As we noted above, the CSA and IIROC are publishing the Joint CSA-IIROC Staff Notice 23-329 to seek feedback on broader short selling issues and the existing regulatory regime. Any regulatory proposals that may emerge, either from IIROC or from the CSA, would be subject to the regular public comment and approval processes.

(iv) Need for Regulatory Change

The comments on the Consultation Paper provided a range of views on whether regulatory change was necessary. Some advocated for sweeping reforms to short selling regulation (as discussed above), while others were of the view that incremental and targeted changes are more appropriate when supported by evidence. Some commenters were of the view that no change was necessary at all. We found that certain market participants (mainly issuers, related industry associations and some law firms) were more supportive of regulatory change. The suggested changes are described below.

In the Consultation Paper, we asked whether:

• there are market developments that warrant revisiting the regulatory framework;

• there is a connection between failed trades and activist short selling; and

• there are relevant regulatory requirements in other jurisdictions that should be considered.

On the issue of market developments, the influence of social media figured prominently in responses received. We acknowledge the need to monitor the impact of social media on the capital markets.

Many commenters were also of the view that a comprehensive study on failed trades should be conducted but did not indicate that there was a connection between failed trades and problematic activist short selling activity. As we noted in Part 3 a above, IIROC conducted a new study of failed trades and the findings are outlined in the Joint CSA-IIROC Staff Notice 23-329 and in IIROC Notice 22-0190, published today.

We set out below the proposals that were put forward or addressed in the comment letters received on the Consultation Paper related to activist short selling concerns and we also identify some challenges or areas for further consideration.

a. Guidelines

Some commenters, including some who view activist short selling favourably, suggested that guidelines or best practices would benefit the market with respect to what may be considered problematic activity. This is similar to the approach taken by the Australian Securities and Investment Commission (ASIC), which published INFO 255 Activist short selling campaigns in Australia, an information sheet which, among others, described the existing Australian regulatory framework for short selling and recommended "better practices" for activist short sellers.{14}

With respect to issuing guidance regarding activist short selling, we note that typically guidelines are tied to a national instrument or rule and we do not presently have any rules which govern the conduct of activist short sellers (as noted above, there is no regulatory requirement specifically targeting activist short sellers). Should any regulatory requirements implemented in the future, we would consider what additional guidance is needed to complement such requirements.

b. Reporting and Disclosure Requirements

Comments received on this topic varied. For example:

• some commenters supported regulatory changes requiring that activist short sellers disclose their opening, changes in and closing positions, as well as their identity either to the regulator, the public, or both;{15}

• some noted that requiring additional disclosure should only be done once there has been focus on studying the Canadian liquidity environment, underlying data and the potential impact of new disclosure obligations;

• some cautioned that introducing public disclosure requirements could potentially lead to Reddit-type message board traders inciting short squeezes;

• it was noted that public disclosure and reporting, especially by activist short sellers could also have the unintended consequence of promoting herd behavior to further drive down the target's stock price;{16} and

• some commenters raised the issue of whether there should be symmetry for reporting obligations between activists on the long and short side.

Regulators in some foreign jurisdictions already impose reporting and disclosure requirements on short sellers with short positions above certain thresholds. International regulatory developments in this area are discussed in Joint CSA-IIROC Staff Notice 23-329. We are monitoring these developments and will consider whether additional disclosure of short selling activities, which may include those of activist short sellers, is needed. As noted above, however, imposing disclosure requirements on activist short sellers would first require defining who the activist short sellers are, creating a regulatory framework over them and determining whether that framework should include reporting of synthetic short positions. The creation of such a framework would likely require a change in securities legislation.

c. Implementation of a Hold Period

Some commenters proposed imposing a brief trading moratorium or minimum holding period on any stock promoter or short seller who opens a large position and disseminates market-moving information, irrespective of the medium.{17} The rationale is that a holding period could provide the market with an opportunity to evaluate the quality and credibility of the information. We are not aware of any securities regulators who have implemented such a measure at this time.

While we agree that the introduction of a hold period may give more time for the market to absorb information disseminated from an activist short seller's report, we note that it could also disincentivize activist short sellers from publishing short reports, resulting in less informationally efficient markets. Moreover, any hold period would need to be implemented equally on both the short and long sides of trades to be fair and would also need to consider synthetically held positions. A hold period could further raise practical challenges, such as identifying the duration of this hold period and imposing them on non-regulated entities.

The impact of such measures would have to be carefully studied and examined to determine whether the potential benefit outweighs the risks this measure introduces.

d. Advance Notice to Issuers

The proposal was for a requirement that the activist short seller provide their report to the issuer in advance of publishing. This would give the issuer an opportunity to review the report, identify factual errors and have the means to provide their own rebuttal before it is released into the public. The proposal recognizes that issuers may face practical impediments, such as the fact that they are constrained by disclosure rules and that there are practical difficulties in responding quickly to sometimes broad allegations in a timely manner to avoid or minimize the negative price impact of a short seller's report.

We acknowledge that issuers may find it difficult to respond on a timely basis to activist short seller campaigns spread through social media or other online platforms. Even if issuers are given advance notice, they may not be able to respond because existing insider trading rules would generally preclude the target from engaging with the activist short seller on an open access basis. Specifically, the targeted issuer would likely find itself constrained in its reply if the reply to the activist short-seller allegations would involve disclosing material facts. The same issue would arise if, for example, an unfavourable report is published in the media, or allegations arise from other parties not connected to short sellers. Further, imposing requirements on activist short sellers who are not market participants or otherwise registered also poses jurisdictional challenges for regulators. There are also challenges with determining an appropriate length for the advance notice to the issuer. The longer the duration, the higher the risk of information leaking into the market and impacting the issuer's stock price before the issuer has an opportunity to respond.

We also recognize the importance of timely dissemination of material undisclosed information to the market by bona fide short selling reports that improves price discovery.

e. Impose Disclosure of Interest Requirement or Standards

This proposal was to require that any person publishing a statement concerning an issuer's public disclosures and either (i) has either a long or short position in the securities of the issuer to which the statement relates, or (ii) is in any arrangement that may result in financial gain to the person as a result of, or in connection with the publication of the statement, adhere to standards of professionalism and objectivity such as those required by the CFA Institute of its members.

We note that activist short selling reports generally include disclosure that the short seller has a position in the securities of the issuer they cover and that they may stand to realize gains due to price changes.{18}

f. Expanded Offence for Misleading Information

Recent B.C. Securities Act amendments that came into force introduced an additional prohibition for making misleading statements for those engaged in "promotional activities". Under this prohibition, a person engaged in a promotional activity must not make a statement or provide information that is false or misleading in circumstances where a reasonable investor/person would consider that statement or information important when making an investment decision.{19} Unlike other securities law prohibitions against making a misrepresentation, this prohibition does not require that the statement or the information:

• be "materially" misleading or untrue; or

• be reasonably expected to have a significant effect on the market price or value of a security.

Similarly, in Ontario, section 94(1) False or misleading statements, information about reporting issuers, etc. of the proposed Capital Market Act{20} which, if adopted, would replace the Securities Act (Ontario) and the Commodity Futures Act (Ontario), would prohibit a person engaged in a promotional activity from making a statement or providing information about a reporting issuer or an issuer whose securities are publicly traded that the person knows or reasonably ought to know is false or misleading and would be considered to be important by a reasonable investor in determining whether to purchase or trade a security of the issuer or related financial instrument. Proposed section 94(2) prohibits attempts to make these statements and proposed section 94(3) allows the OSC to prescribe exceptions from this prohibition. These proposals are intended to implement Recommendation 57 of the Taskforce report{21} to create a prohibition to effectively deter and prosecute misleading or untrue statements about public companies and attempts to make such statements. The comment period for the proposed Capital Markets Act ended on February 18, 2022.

An activist short seller's attempt to depress an issuer's stock price by knowingly spreading material misinformation is already prohibited conduct under securities legislation. However, there are views that the thresholds for proving this contravention are too high and a reasonable investor standard may be a good balanced approach to improving public disclosure without adding excessive burden to market participants. A few commenters, however, indicated that the elimination of a market impact assessment and materiality threshold can be expected to have a significant chilling effect on short selling and that any benefit to these changes will outweigh the cost. Concerns were also raised that activist short sellers (and other market participants without access to non-public information on an issuer) should not be held to any standard resembling that of company insiders.

The changes to the BC Securities Act with respect to making misleading statements in the course of promotional activities in BC and the proposed section 94 in the Capital Markets Act in Ontario may introduce an additional deterrent to problematic conduct through potential enforcement action. It is too early to conclude whether they will be an effective tool as it relates to activists, or whether they will lead to a potential increase in prosecutable cases against potentially problematic activist short sellers or reduce the number of problematic campaigns against reporting issuers. The CSA will monitor their impact.

g. Civil Liability for Misleading Information

Currently, there is no mechanism under securities law to seek damages against activist short sellers conducting short and distort campaigns. Commenters noted that an issuer targeted by an abusive short selling campaign, as well as the issuer's security holders that are induced to sell their securities on the basis of misinformation, are often forced to wait and see whether the regulator will commence regulatory proceedings. Some foreign jurisdictions provide a private right of action for the making or dissemination of false or misleading information.{22} A private right of action could provide recourse for targets of "short and distort" campaigns while also providing a complementary deterrent to problematic activities associated with activist short selling. One commenter was of the view that a private right of action must be based on a short seller's deliberate and calculated conduct and not mere negligence or a good faith mistake, nor should such a provision become a form of insurance against losses that are actually caused by other forces such as investment risk.

At this point, we have not found evidence of systemic abuse related to activist short selling campaigns that would support regulatory changes such as the introduction of a private right of action against activist short sellers. However, as noted in our Consultation Paper, there are existing common and civil law remedies that could apply to problematic activist short selling campaigns, but those have not typically been used by issuers or favoured by the Courts given the freedom of expression issues they introduce.

Part 5. Questions

Please refer your questions to any of the following CSA staff:

Ruxandra Smith

Senior Accountant, Market Regulation

Ontario Securities Commission

[email protected]Timothy Baikie

Senior Legal Counsel, Market Regulation

Ontario Securities Commission

[email protected]

Kevin Yang

Manager, Regulatory Strategy and Research

Ontario Securities Commission

[email protected]

Serge Boisvert

Senior Policy Advisor

Autorité des marchés financiers

[email protected]Roland Geiling

Derivatives Analyst

Autorité des marchés financiers

[email protected]

Jesse Ahlan

Regulatory Analyst, Market Structure

Alberta Securities Commission

[email protected]Jan Bagh

Senior Legal Counsel

Alberta Securities Commission

[email protected]

Kathryn Anthistle

Senior Legal Counsel, Legal Services

Capital Markets Regulation Division

British Columbia Securities Commission

[email protected]Michael Grecoff

Securities Market Specialist

British Columbia Securities Commission

[email protected]

Eric Pau

Senior Legal Counsel, Legal Services

Corporate Finance

British Columbia Securities Commission

[email protected]Jennifer Whately

Manager, Litigation, Enforcement

British Columbia Securities Commission

[email protected]

Tyler Ritchie

Investigator

Manitoba Securities Commission

[email protected]

{1} https://www.iiroc.ca/news-and-publications/notices-and-guidance/iiroc-priorities-2021

{2} Data sourced from Activist Insight and issuers identified based on their headquarter location.

{3} CSA analysis of activist short seller targets from Activist Insight and annual listed issuer counts from the World Federation of Exchanges for the period 2010 to 2021.

{4} The British Columbia Securities Commission is the principal regulator for four of the issuers, with the Alberta Securities Commission, the Ontario Securities Commission and the Manitoba Securities Commission each being principal regulator for the others.

{5} We note that, while it was published for comment, the Consultation Paper was also distributed to the OSC's Investor Advisory Panel at their meeting in January 2021, shortly after the publication of the Consultation Paper, but no comments were made.

{6} See CSA Staff Notice 51-348 Staff's Review of Social Media Used by Reporting Issuers and CSA Staff Notice 51-356 Problematic promotional activities by issuers.

{7} See Joint CSA -- IIROC statement on recent market volatility dated February 1, 2021: "We caution investors to consider the source of information and advice they are relying on to make investment decisions. Online chat rooms are unregulated and may contain information that is inaccurate or inappropriate for some investors. Investors should always check the registration of any person or business trying to sell them an investment or give them investment advice. To do this, investors can visit https://aretheyregistered.ca or IIROC's database of advisors working for IIROC regulated firms."

{8} One commenter went as far as recommending that activist short sellers should be strictly restricted in terms of their ability to promote their cause to the public via media/communications outlets (for example, short sellers should not be allowed to go on TV with their story).

{9} For example, see How to deal with rumors on social media at https://content.irmagazine.com/story/ir-magazine-summer-2021/page/19.

{10} IIROC reviews social media indicators such as buzz and sentiment analysis provided by third-party data vendors (Eikon and Bloomberg) but does not have full confidence in the effectiveness of these tools to date. The surveillance team also relies on manual search methods on well known websites such as stockhouse.com, AKN (for mining), StockTwits and Seeking Alpha.

{11} Several commenters also provided their views on recommendations from Ontario's Capital Markets Modernization Taskforce (Taskforce) report related to short selling, available at https://www.ontario.ca/document/capital-markets-modernization-taskforce-final-report-january-2021, regarding pre-borrow requirements (the recommendation was for IIROC to revise the Universal Market Integrity Rules (UMIR) to require an investment dealer to confirm the ability to borrow securities prior to accepting a short sale order); mandatory buy-in (the recommendation that short sellers be subject to a mandatory buy-in for short sales that failed to settle, triggered at settlement date + two days); limits on short selling in connection with prospectus offerings and private placements (the recommendation is for OSC to adopt a rule prohibiting market participants and investors who previously sold short securities from acquiring them under prospectus or private placements).

{12} The tick test referred to a previous requirement in UMIR that a short sale not be made at a price which is less than the last sale price of the security.

{13} SEC Rule 201 generally requires marketplaces to establish, maintain, and enforce written policies and procedures that are reasonably designed to prevent the execution or display of a short sale at an impermissible price when a stock has triggered a circuit breaker by experiencing a price decline of at least 10 percent in one day (based on the prior day's closing price). Once the circuit breaker in Rule 201 has been triggered, the price test restriction will apply to short sale orders in that security for the remainder of the day and the following day, unless an exception applies.

{14} Available at https://asic.gov.au/regulatory-resources/markets/short-selling/activist-short-selling-campaigns-in-australia/.

{15} This is related to the reference in the Consultation of a group of U.S. academics who petitioned the SEC to impose a "duty to update" a short position when there has been a voluntary disclosure of that short position.

{16} For example, on May 17, 2019, Muddy Waters disclosed a 0.5% short position on Solutions 30 SE as required under European securities regulations. Following this disclosure and prior to the release of any short report, Solutions 30 SE's stock price dropped by 20% on May 21st, 2019. See "Muddy and 5 other HFs shorting Solutions 30," Breakout Point blog, August 2, 2019 and Michelle Celarier, "Shares of Solutions 30, a Muddy Waters Short, Tank After Auditor Raises Concerns," Institutional Investor, May 24, 2021.

{17} The Consultation Paper referenced a proposal for a 10-day minimum holding period that was mentioned in a news article. See Mark Cohodes, "Pump-and-dump stock trading needs new rules for the digital age", FT Online, April 26, 2020 at https://www.ft.com/content/01b765c2-854e-11ea-b6e9-a94cffd1d9bf.

{18} For example, see the terms of use for Muddy Waters' research reports and the legal disclaimer for Hindenburg's research reports.

{19} Securities Act (British Columbia), RSBC 1996, c 418, 50 (1). A similar amendment was also proposed by the Taskforce.

{20} Available at https://www.ontariocanada.com/registry/view.do?postingId=38527&language=en

{21} Ibid. footnote 11.

{22} See, for example, Australia Corporations Act 2001 (Cth), sections 1041E and 1041I.

APPENDIX A

Summary of Comments on CSA Consultation Paper 25-403 Activist Short Selling

List of Commenters

|

|

Commenter |

Abbreviation |

|

1. |

Anson Advisors Inc. |

Anson |

|

2. |

McMillan LLP |

McMillan |

|

3. |

Global Principles for Sustainable Securities Lending |

GPSSL |

|

4. |

Alternative Investment Management Association |

AIMA |

|

5. |

Save Canadian Mining |

SCM |

|

6. |

Northern Dynasty Minerals Ltd. |

NDM |

|

7. |

NEO Exchange Inc. |

NEO |

|

8. |

Davies Ward Phillips & Vineberg |

DWPV |

|

9. |

Norton Rose Fulbright Canada LLP |

NRF |

|

10. |

Corus Entertainment Inc. |

CEI |

|

11. |

Finning International Inc. |

FII |

|

12. |

NOVAGOLD Resources Inc. |

NRI |

|

13. |

Badger Daylighting Ltd. |

BDI |

|

14. |

Exchange Income Corporation |

EIC |

|

15. |

Standard Uranium |

SU |

|

16. |

Canadian Investor Relations Institute |

CIRI |

|

17. |

Peter Brown |

PB |

|

18. |

Fiore Management & Advisory Corp |

FMAC |

|

19. |

Prospectors & Developers Association of Canada |

PDAC |

|

20. |

Portfolio Management Association of Canada |

PMAC |

|

21. |

Canadian Advocacy Council of CFA Societies Canada |

CAC |

|

22. |

Stikeman Elliott LLP |

SE |

|

23. |

RBC DS |

RBC DS |

Summary of Comments

{23} https://www.osc.ca/sites/default/files/2021-02/joint-osc-iiroc-whistleblower-guidance.pdf

{24} Please also see CSA/IIROC Joint Notice 23-312 -- Transparency of Short Selling and Failed Trades at https://www.osc.ca/sites/default/files/pdfs/irps/csa_20120302_23-312_rfc-trans-short-selling.pdf

{25} https://www.osc.ca/en/securities-law/instruments-rules-policies/5/51-348

{26} At https://www.osc.ca/en/news-events/news/joint-statement-canadian-securities-administrators-and-investment-industry-regulatory-organization