CSA Staff Notice 51-344 - Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2015

CSA Staff Notice 51-344 - Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2015

CSA Staff Notice 51-344 Continuous Disclosure Review Program Activities

for the fiscal year ended March 31, 2015

July 16, 2015

Introduction

This notice contains the results of the reviews conducted by the Canadian Securities Administrators (CSA) within the scope of their Continuous Disclosure Review Program (CD Review Program). The goal of the program is to improve the completeness, quality and timeliness of continuous disclosure provided by reporting issuers{1} (issuers) in Canada. This program was established to assess the compliance of continuous disclosure (CD) documents and to help issuers understand and comply with their obligations under the CD rules so that investors receive high quality disclosure.

In this notice, we summarize the results of the CD Review Program for the fiscal year ended March 31, 2015 (fiscal 2015). To raise awareness about the importance of filing compliant CD documents, Appendix A includes information about areas where common deficiencies were noted, with examples in certain instances, to help issuers address these deficiencies as well as best practices.

For further details on the CD Review Program, see CSA Staff Notice 51-312 (revised) Harmonized Continuous Disclosure Review Program.

Results for Fiscal 2015

CD Activity Levels

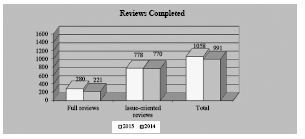

During fiscal 2015, a total of 1,058 CD reviews (280 full reviews and 778 issue oriented reviews (IOR)) were conducted. This represents a 7% increase from the 991 CD reviews (221 full reviews and 770 IORs) completed during fiscal 2014.

Issuers annually selected for a full CD review are identified using a risk based approach. Issuers selected for an IOR are identified based on the targeted objective or subject matter of the review.

We apply both qualitative and quantitative criteria in determining the level of review and type of review required. Some CSA jurisdictions also devote additional resources to communicating results and findings to market participants by issuing local staff notices and reports, where applicable, and holding education and outreach seminars to help issuers better understand their CD obligations.

Issue-Oriented Reviews

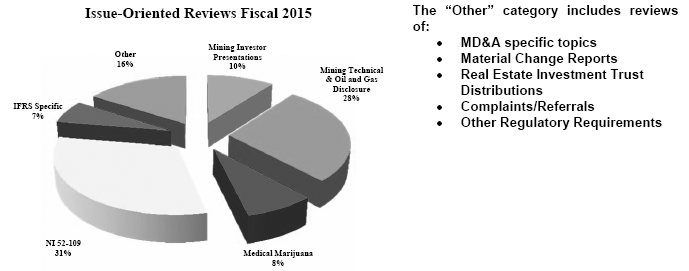

An IOR focuses on a specific accounting, legal or regulatory issue. IORs may focus on emerging issues, implementation of recent rules or on matters where we believe there may be a heightened risk of investor harm. In fiscal 2015, a total of 74% of all CD reviews completed were IORs (fiscal 2014 -- 78%). The following are some of the IORs conducted by one or more jurisdictions:

The "Other" category of IORs noted above is not an exhaustive list. We may undertake an IOR for various other subject matters during the year. Refer to Appendix A -- Financial Statements, MD&A and Other Regulatory Deficiencies (Appendix A) for some common deficiencies identified as a result of our IORs.

Full Reviews

A full review is broad in scope and covers many types of disclosure. A full review covers the selected issuer's most recent annual and interim financial reports and MD&A filed before the start of the review. For all other CD disclosure documents, the review covers a period of approximately 12 to 15 months. In certain cases, the scope of the review may be extended in order to cover prior periods. The issuer's CD documents are monitored until the review is completed. A full review also includes an issuer's technical disclosure (e.g. technical reports for oil and gas and mining issuers), annual information form (AIF), annual report, information circulars, news releases, material change reports, business acquisition reports, corporate websites, certifying officers' certifications and material contracts. In fiscal 2015, a total of 26% of the CD reviews were full reviews (fiscal 2014 -- 22%).

CD Outcomes for Fiscal 2015

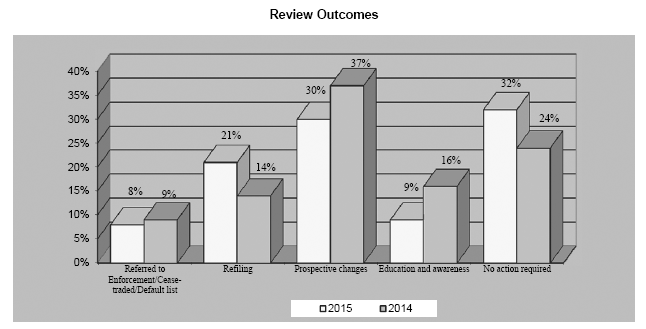

In fiscal 2015, 59% of our review outcomes required issuers to take action to improve and/or amend their disclosure or resulted in the issuer being referred to enforcement, ceased traded or placed on the default list. In fiscal 2014, 60% of the reviews resulted in a similar outcome.

We classify the outcomes of the full reviews and IORs into five categories as described in Appendix B. Some CD reviews may generate more than one category of outcome. For example, an issuer may have been required to refile certain documents and also make certain changes on a prospective basis.

Where possible, we have attempted to identify trends we observed when reviewing comparative results. However, given our risk based approach noted above, the outcomes on a year to year basis may vary and cannot be interpreted as an emerging trend. Issues and issuers reviewed each year might be different. The result in fiscal 2015 is that we continued to see substantive outcomes being obtained as a result of our reviews as noted in the refilings and referred to enforcement/default list/cease traded categories.

The refilings of issuers' CD record included some of the following areas:

• Financial Statements: compliance with recognition, measurement and disclosure requirements in IFRS, which included, but was not limited to, impairment, revenue, accounting policies, significant judgements and auditors' reports;

• Management's Discussion and Analysis (MD&A): compliance with Form 51-102F1 of NI 51-102 (Form 51-102F1), which included, but was not limited to, non-GAAP measures, discussion of operations, liquidity, related party transactions, disclosure controls and procedures (DC&P) and internal controls over financial reporting (ICFR);

• Other Regulatory Requirements: compliance with other regulatory matters, which included, but was not limited to, mining technical reports and investor presentations for content deficiencies, business acquisition reports, certificates, and filing of previously unfiled documents, such as material contracts, or clarifying news releases to address concerns around unbalanced disclosure.

Refilings are significant events that should be clearly and broadly disclosed to the market in a timely manner. Please refer to "News Release upon Refiling of CD Documents" in Appendix A to this Notice for further discussion.

Common Deficiencies Identified

Our full reviews and IORs focus on identifying material deficiencies and potential areas for disclosure enhancements. We have provided guidance and examples of common deficiencies in Appendix A.

This is not an exhaustive list of disclosure deficiencies noted in our reviews. Issuers must ensure that their CD record complies with all relevant securities legislation. The volume of disclosure filed does not necessarily equate to full compliance. The examples in Appendix A do not include all requirements that could apply to a particular issuer's situation and are provided for illustrative purposes only.

Results by Jurisdiction

All CSA jurisdictions participate in the CD Review Program and some local jurisdictions may publish staff notices and reports summarizing the results of the CD reviews conducted in their jurisdictions. Refer to the individual regulator's website for copies of these notices and reports:

• www.bcsc.bc.ca

• www.albertasecurities.com

• www.osc.gov.on.ca

• www.lautorite.qc.ca

{1} In this notice "issuers" means those reporting issuers contemplated in National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102).

APPENDIX A

FINANCIAL STATEMENT, MD&A AND OTHER REGULATORY DEFICIENCIES

Our CD reviews identified several financial statement, MD&A and other regulatory deficiencies that resulted in issuers enhancing their disclosure and/or refiling their CD documents. To help issuers better understand and comply with their CD obligations, we present the key observations from our reviews in both a hot buttons chart as well as detailed discussions. The hot buttons section includes observations along with considerations for issuers including the relevant authoritative guidance. The discussion that follows each chart includes examples of deficient disclosure contrasted against more robust entity-specific disclosure or a more in-depth explanation of the matters we observed.

Please note that the following observations do not constitute an exhaustive list.

FINANCIAL STATEMENT DEFICIENCIES

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

||

|

|

||||

|

FINANCIAL STATEMENTS |

||||

|

|

||||

|

Operating Segments |

• |

We continue to see issuers that fail to disclose certain information about geographic areas, in particular revenues from external customers. |

• |

Issuers must disclose information about operating segments so that investors are able to evaluate the nature and financial effects of the business activities in which they engage and the economic environments in which they operate. |

|

|

||||

|

|

• |

We also see issuers that fail to disclose information about major customers, in particular when revenues from transactions with a single external customer amount to 10% or more of the issuer's revenues. |

• |

Disclosure about major customers may assist users in determining if there is economic dependence. |

|

|

||||

|

|

|

|

Reference: Paragraph 33 and 34 of IFRS 8 Operating Segments |

|

|

|

||||

|

Business Combinations |

• |

Upon acquisition of a business, issuers are reporting a significant portion of the purchase price in goodwill without separately identifying and assigning a value to other intangible assets, such as customer lists, intellectual property, etc. |

• |

The allocation to the appropriate identifiable assets is important as it may impact an issuer's accounting for intangibles in its financial statements. For example, definite life intangibles require amortization into the statement of profit or loss and will therefore impact income in subsequent periods. |

|

|

||||

|

|

|

|

• |

The measurement period shall not exceed one year from the acquisition date. |

|

|

||||

|

|

|

|

Reference: Paragraph 10 to 13 and 45 and Appendix B of IFRS 3 Business Combinations |

|

|

|

||||

|

Fair Value Measurement |

• |

We continue to see issuers that fail to disclose a description of the valuation technique and inputs used for fair value measurements categorized within Level 3 of the fair value hierarchy. |

• |

For Level 3 fair value measurements, issuers must describe the valuation technique used in the fair value measurement. |

|

|

||||

|

|

|

|

• |

Issuers must also describe and provide quantitative information about all significant unobservable inputs used. |

|

|

||||

|

|

|

|

• |

These disclosures will assist users to understand the measurement uncertainty inherent in fair value measurements. |

|

|

||||

|

|

|

|

Reference: Paragraph 93(d) to (h) of IFRS 13 Fair Value Measurement |

|

DISCLOSURE EXAMPLE

1. Impairment of Assets

In the prior year, we noted that some issuers did not disclose how they determined the amount of impairment loss in accordance with paragraph 130 of IAS 36 Impairment of Assets (IAS 36). Given the current economic conditions, we continue to note this issue.

In accordance with paragraph 130 of IAS 36, if an impairment loss has been recognized or reversed for an individual asset, or a cash-generating unit (CGU), an issuer must disclose whether the recoverable amount of the asset or CGU is its fair value less costs of disposal or its value in use. If the recoverable amount is fair value less costs of disposal, an issuer must disclose the level of the fair value hierarchy within which the fair value measurement of the asset or CGU is categorized. In the case of Level 2 and Level 3 of the fair value hierarchy, an issuer must also describe the valuation technique and key assumptions used. If the recoverable amount is value in use, an issuer must disclose the discount rate(s) used in the current estimate and previous estimate (if any) of value in use.

Some issuers who measured the recoverable amount of an asset or a CGU as value in use did not base cash flow projections on reasonable and supportable assumptions that represent management's best estimate of the range of economic conditions that will exist over the remaining useful life of the asset or CGU, as required by paragraph 33(a) of IAS 36. Some issuers inappropriately based cash flow projections on forecasts for periods longer than five years where management could not demonstrate its experience to forecast over such periods, as discussed in paragraph 35 of IAS 36.

Additionally, some issuers did not disclose the significant judgements and the uncertainties involved in estimating the recoverable amount of the asset or the CGU, where such judgements and sources of estimation uncertainty met the criteria for disclosure under IAS 1 Presentation of Financial Statements (IAS 1).

Issuers should assess at the end of each reporting period whether there is any indication that an asset or CGU may be impaired in accordance with paragraphs 8 -- 17 of IAS 36, or paragraph 18-20 of IFRS 6 as applicable to exploration for and evaluation of mineral resources. If any such indication exists, the entity must estimate the recoverable amount of the asset in accordance with paragraphs 18 -- 57 of IAS 36. At the end of each reporting period, issuers must assess the need to reverse an impairment loss recognized for an asset or a CGU in prior periods as required by paragraphs 109 -- 123 of IAS 36. We caution issuers that an improper impairment test and impairment charge may result in misstatements in profit or loss in the current and future periods.

- - - - - - - - - - - - - - - - - - - -

Example of Deficient Disclosure -- Impairment of Assets (exploration stage mining company)

Due to poor market conditions, the Company considered the likelihood of obtaining suitable financing in the foreseeable future in order to conduct further exploration on Property Y was unlikely. Therefore, it determined that Property Y is impaired and recognized an impairment loss of $5 million to write down the carrying value of Property Y from $7.5 million to $2.5 million in the year ended December 31, 2014.

- - - - - - - - - - - - - - - - - - - -

In the above example, the issuer did not disclose how it measured the recoverable amount of Property Y and the associated judgements and estimation uncertainty including:

• Whether the recoverable amount of $2.5 million is value in use or fair value less costs of disposal;

• If the recoverable amount is value in use, the discount rate(s) used in the current and previous estimate (if any) of value in use (IAS 36, paragraph 130(g));

• If the recoverable amount is fair value less costs of disposal, the applicable level of the fair value hierarchy, and in the case of Level 2 and Level 3 of the hierarchy, the valuation technique and key assumptions used (IAS 36, paragraph 130(f)); and

• Judgements made and the uncertainties involved in estimating the recoverable amount of the property (IAS 1, paragraph 125).

- - - - - - - - - - - - - - - - - - - -

Entity-Specific Disclosure Example -- Impairment of Assets (exploration stage mining company)

Due to the lack of suitable financing, the Company has determined that it does not have adequate resources to conduct further exploration on Property Y for the foreseeable future. Therefore, the Company suspended the exploration program at Property Y in the year ended December 31, 2014, wrote down the carrying value of Property Y from $7.5 million to $2.5 million, and recognized an impairment loss of $5 million. The recoverable amount of $2.5 million is based on Property Y's fair value less costs of disposal. In estimating the fair value less costs of disposal, the Company used a market approach. The Company used sale prices of adjacent properties obtained from the local Ministry of Mines, and adjusted this to consider market capitalization declines of comparable companies with comparable properties over the past year. The Company also discussed with its external technical consultants the drilling activities and exploration program conducted on Property Y and the uncertainty regarding future prospects in the mining industry. As this valuation technique requires the use of unobservable inputs including the Company's data about the property and management's interpretation of that data, it is classified within Level 3 of the fair value hierarchy. A value in use calculation is not applicable as the Company does not have any expected cash flows from using the property at this stage of operations.

In estimating fair value less costs of disposal, management's judgement was involved in identifying comparable properties with characteristics similar to Property Y (e.g. nature and amount of resources, size and accessibility). The comparable properties are in the same mineral district, with exploration directed for the same commodity using the same mineral deposit model. The comparable properties are also at a similar stage of development in terms of the existence, quantity and quality of mineral resources and availability of critical infrastructure.

- - - - - - - - - - - - - - - - - - - -

The above example is specific to the facts of this issuer. The nature and extent of the information provided by issuers may vary depending on facts and circumstances; however, the information provided must help users of financial statements understand the judgements that management made about the future and other sources of estimation uncertainty. This may include more qualitative and quantitative information about the assumptions used.

MD&A DEFICIENCIES

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

||

|

|

||||

|

MD&A |

||||

|

|

||||

|

Liquidity and Capital Resources |

• |

We continue to see issuers that fail to provide sufficient analysis of their liquidity and capital resources. |

• |

This section of the MD&A should focus on an issuer's ability to generate sufficient liquidity in the short term and long term in order to fund planned growth, development activities or expenditures necessary to maintain capacity. |

|

|

||||

|

|

• |

Issuers often reproduce information in the MD&A that is readily available from the financial statements. For example, repeating the balances of cash flows from operating, investing and financing activities. |

• |

In addition, the MD&A should provide an analysis of an issuer's capital resources, including the amount, nature and purpose of commitments and the expected source of funds to meet these commitments. |

|

|

||||

|

|

|

|

• |

While these disclosures are required for all issuers, they are especially important when issuers have negative cash flows from operations, a negative working capital position or a deteriorating financial condition. |

|

|

||||

|

|

|

|

• |

This disclosure enables users to assess how the issuer will meet its obligations and its short and long term objectives. |

|

|

||||

|

|

|

|

Reference: Item 1.6 and 1.7 of Form 51-102F1 |

|

|

|

||||

|

Results of Operations |

• |

We continue to see issuers that provide boilerplate disclosure when discussing their results of operations. Issuers simply repeat information that is readily available in the financial statements. |

• |

This section of the MD&A should provide a narrative explanation of how the issuer performed during the period, along with trends, commitments, risk and uncertainties that will impact the company. |

|

|

||||

|

|

• |

Issuers provide the year over year change in the balance without explaining, in sufficient detail, the key drivers and reasons contributing to the change. |

• |

Trend analysis should include a discussion of the significant factors that caused the change in the financial statement balance. For example, revenues, expenses, gross profit, etc. |

|

|

||||

|

|

|

|

• |

In certain instances, for example general and administrative expenses, it may be helpful to quantify each material component of the balance to better explain the movement in the total balance. |

|

|

||||

|

|

|

|

• |

This disclosure provides users the ability to assess the business of the issuer and to identify and understand trends. |

|

|

||||

|

|

|

|

Reference: Item 1.4 of Form 51-102F1 |

|

|

|

||||

|

Forward Looking Information (FLI) / Non-GAAP Measures (NGM) |

• |

We continue to see issuers that use FLI and NGM in the MD&A, news releases, websites, marketing materials and other documents without clearly identifying them as such or including the appropriate disclosures. |

• |

The disclosure requirements for FLI and the disclosure guidance provided for NGM apply regardless of whether FLI and NGM are used in the MD&A or on a website, news release or other public document. |

|

|

||||

|

|

|

|

• |

If the above-noted disclosure of FLI and/or NGM are made in another document, such as the MD&A, the information should be cross referenced or re-produced. |

|

|

||||

|

|

|

|

• |

Users may be misled if these disclosures are not provided. |

|

|

||||

|

|

|

|

Reference: FLI -- Part 4A and 4B of NI 51-102 NGM -- CSA Staff Notice 52-306 |

|

|

|

||||

|

Real Estate Investment Trust (REIT) Distributions |

• |

We note that some REITs declare distributions which exceed the cash they generate from operating their own underlying properties (cash flow from operations) but do not provide the relevant disclosure in their MD&A and AIF. |

• |

The disclosure should signal to investors that excess distributions occurred, how they were financed, and that they represented a return of capital, amongst other things. |

|

|

||||

|

|

|

|

• |

Investors may be misled if such excess distributions, in addition to risks about their sustainability, are not appropriately disclosed. |

|

|

||||

|

|

|

|

Reference: Section 6.5.2 of National Policy 41-201 Income Trusts and Other Indirect Offerings |

|

DISCLOSURE EXAMPLES

1. Related Party Transactions

While many of the MD&A requirements for related party transactions in Form 51-102F1 are similar to the requirements under IAS 24 Related Party Disclosures, Form 51-102F1 specifically requires an issuer to identify the related person or entity, as well as to discuss the business purpose of the transaction.

MD&A disclosure of related party transactions is intended to provide both qualitative and quantitative information that is necessary for an understanding of the business purpose and economic substance of a transaction. To meet this requirement, the disclosure should be specific and detailed, rather than simply repeat disclosure from the financial statements.

The disclosure below is an example of boilerplate disclosure for a related party transaction:

- - - - - - - - - - - - - - - - - - - -

Example of Deficient Disclosure -- Related Party Transactions

For the years ended December 31, 2014 and 2013 the Company paid a related party $43 million and $40 million, respectively, for management and administrative fees. As of December 31, 2014 and 2013 outstanding balance amounted to $4 million and $5 million, respectively.

- - - - - - - - - - - - - - - - - - - -

In the above example, the issuer does not disclose the identity of the related party and the business purpose of the transaction. A better example of disclosure for related party transactions would be as follows:

- - - - - - - - - - - - - - - - - - - -

Example of Entity-Specific Disclosure -- Related Party Transactions

The Company does not directly employ any of the individuals responsible for managing and operating the business. XYZ Corp., a major stockholder, provides management and administrative workforce to the Company under the terms of the Agreement. The costs of all compensation, benefits and employer expenses are invoiced by XYZ Corp. based on actual costs incurred and are settled on a monthly basis. The Company presents these charges as general and administrative costs and costs incurred under administrative services agreements. For the years ended December 31, 2014 and 2013, the Company incurred $43 million and $40 million, respectively, under this Agreement. As of December 31, 2014 and 2013, outstanding balance payable to XYZ Corp. amounted to $4 million and $5 million, respectively.

- - - - - - - - - - - - - - - - - - - -

2. NI 52-109 Certification of Disclosure in Non-Venture Issuers' Annual and Interim Filings

NI 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109) requires both non-venture and venture issuers to file certificates of annual and interim filings signed by an issuer's Chief Executive Officer and Chief Financial Officer (Certifying Officers). In addition, non-venture issuers must establish and maintain DC&P and ICFR.

Forms 52-109F1 Certificate of Annual Filings-Full Certificate (Annual Certificate) and 52-109F2 Certification of Interim Filings-Full Certificate (Interim Certificate), which NI 52-109 requires non-venture issuers to file, state that the Certifying Officers have designed, or caused to be designed, DC&P and ICFR. Furthermore, Annual Certificates indicate that the Certifying Officers have evaluated or caused to be evaluated, under their supervision, the effectiveness of DC&P and ICFR, and that the issuer has disclosed in its annual MD&A the Certifying Officers' conclusions about the effectiveness of DC&P and ICFR. When the Certifying Officers determine there is a material weakness relating to the design or operations of ICFR, or when there has been a limitation on the scope of design, issuers must include paragraphs 5.2, 5.3 and/or 6(b)(ii) in an Annual Certificate or paragraph 5.2 or 5.3 in an Interim Certificate, and include disclosure in the MD&A describing the material weakness or summary financial information relating to the entities subject to the scope limitation.

Our reviews identified three common areas of deficiencies: (i) inconsistency between a certificate and MD&A disclosure; (ii) material weakness disclosure; and (iii) limitations on scope of design relating to an acquired business.

(i) Inconsistency between a certificate and MD&A disclosure

We observed inconsistency between conclusions in a certificate about the effectiveness of ICFR and the related disclosure in an issuer's MD&A. This inconsistency caused uncertainty as to whether the Certifying Officers were concluding ICFR were effective. The two most common deficiencies were:

• Certifying Officers specified the existence of a material weakness in paragraph 5.2 and/or 6(b)(ii) of their Annual Certificate. However, the MD&A did not include any discussion of a material weakness.

• paragraph 6(b)(i) of an issuer's Annual Certificate stated that the Certifying Officers' conclusion about effectiveness of the issuer's ICFR was disclosed in the MD&A. However, the MD&A conclusions were incomplete or qualified.

(ii) Material Weakness

When Certifying Officers identify a material weakness in the design or operations of ICFR at the period-end date, the Certifying Officers cannot conclude ICFR is effective. If a non-venture issuer determines that it has a material weakness, section 3.2 of NI 52-109 requires the issuer to disclose in its annual or interim MD&A a description of the weakness, the impact of the material weakness on the issuer's financial reporting and its ICFR, and the issuer's current plans, if any, or any actions already undertaken, for remediating the material weakness. A material weakness may relate to the design or operation of an issuer's ICFR. The MD&A disclosure should clearly describe the nature of the material weakness.

We observed issuers that identified a material weakness, provided a vague description of the material weakness and gave little insight about the impact on the issuer's financial reporting. We also noted a few issuers identified the same material weakness for a number of consecutive years, and during that same time period had experienced significant growth in their operations. While NI 52-109 does not require an issuer to remediate an identified weakness, section 9.7 of Companion Policy 52-109CP (52-109CP) notes that MD&A disclosure will be useful to investors if it discusses whether the issuer has committed, or will commit, to a plan to remediate an identified material weakness, and whether there are any mitigating procedures that reduce the risks that have not been addressed as a result of the identified material weakness. A meaningful discussion of an un-remediated material weakness should be updated in each MD&A to ensure the impact of the material weakness continues to be properly reflected as the company grows or experiences other changes in operations.

- - - - - - - - - - - - - - - - - - - -

Example of Deficient Disclosure -- NI 52-109 Certification

The Company's Chief Executive Officer (CEO) and Chief Financial Officer (CFO) have designed an internal control framework to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with IFRS. The control framework used to design the Company's Internal Control over Financial Reporting (ICFR) is Risk Management and Governance -- Guidance on Control, published by the Canadian Institute of Chartered Accountants. The CEO and CFO have concluded that the design and operation of the Company's disclosure controls and procedures were not effective as of December 31, 2014 due to the deficiencies noted in the following paragraph.

The Company identified internal control deficiencies that are common for a company of this size including lack of segregation of duties due to a limited number of employees dealing with accounting and financial matters. However, management believes that at this time, the potential benefits of adding employees to clearly segregate duties do not justify the costs associated with such an increase. The risk of material misstatement is mitigated by the direct involvement of senior management in the day-to-day operations of the Company and review of the financial statements and disclosures by senior management, the members of Audit Committee and the Board of Directors. These mitigating procedures are not considered sufficient to reduce the likelihood that a material misstatement would not be prevented or detected.

There were no material changes in ICFR during 2014.

- - - - - - - - - - - - - - - - - - - -

The above example includes the following deficiencies:

i. Inconsistency between the certificate and MD&A disclosure. The issuer filed its annual certificate and included the paragraphs 5.2 and 6(b)(ii); however, the issuer only concluded that the DC&P was ineffective in its MD&A disclosure.

ii. Material weakness. The MD&A disclosure did not sufficiently describe the material weakness, the impact of the material weakness on the issuer's financial reporting and its ICFR, or the issuer's plans, if any, to remediate as follows:

• the second paragraph refers to more than one internal control deficiency but only describes one deficiency (a lack of segregation of duties);

• the disclosure does not clearly identify the deficiency as a material weakness;

• the meaning of the term "financial matters" used in the description of the deficiency relating to segregation of duties is unclear and insufficient; and

• the issuer has a market capitalization of over $300 million, assets greater than one billion and net income greater than $60 million; however, the disclosure states that lack of segregation of duties is common for an issuer of this size. Staff have not observed this to be the case and have requested issuers provide clarification.

(iii) Limitations on Scope in Design

Section 3.3 of NI 52-109 permits limitations on the scope of design of DC&P and ICFR to exclude controls, policies, and procedures of a business the issuer acquired not more than 365 day before issuer's financial year end, for an allowed period of time as set out in 3.3(4) of NI 52-109. When issuers limit the scope of their design, subsection 3.3(2)(b) requires that they disclose the scope limitation and provide meaningful summary financial information about each underlying entity in the MD&A. Certain issuers had a scope limitation relating to two or more unrelated entities but presented combined financial summary information instead of disclosing information for each entity separately. Section 14.2 of 52-109CP allows for the presentation of combined financial information only in instances where the businesses are related.

OTHER REGULATORY DISCLOSURE DEFICIENCIES

HOT BUTTONS

|

|

OBSERVATIONS |

CONSIDERATIONS |

||

|

|

||||

|

REGULATORY |

||||

|

|

||||

|

Material Contracts |

• |

We continue to see issuers that fail to file material contracts. |

• |

Subsection 12.2(2) of NI 51-102 provides a list of contracts required to be filed even if entered into in the ordinary course of business. These may include a financing or credit agreement with terms that have a direct correlation with anticipated cash distributions or a contract on which the issuer's business is substantially dependent. |

|

|

||||

|

|

|

|

• |

Material contracts must be filed no later than the time the issuer files a material change report if the making of the document constitutes a material change for the issuer, or when the AIF is filed within 120 days after the end of the issuer's most recently completed financial year. |

|

|

||||

|

|

|

|

Reference: Sections 12.2 and 12.3 of NI 51-102 |

|

|

|

||||

|

Material Change Reports (MCRs) |

• |

We continue to see situations where it appears that a material change has occurred and issuers do not file a MCR as soon as practicable, or within 10 days of the date of which the change occurs. For example, in situations where the issuer has eliminated or significantly reduced its dividend payments or the issuer has experienced a significant increase or decrease in near-term earnings prospects. |

• |

Announcements of material changes should be factual and balanced. Unfavourable news must be disclosed just as promptly and completely as favourable news. |

|

|

||||

|

|

|

|

• |

National Policy 51-201, Disclosure Standards (NP 51-201) lays out examples of potentially material information, including changes in a company's dividend payments or policies. |

|

|

||||

|

|

|

|

• |

Part 7 of NI 51-102 requires an issuer to file a MCR within 10 days of the occurrence of a material change. |

|

|

||||

|

|

|

|

Reference: Section 4.3 of NP 51-201 and Part 7 of NI 51-102 |

|

|

|

||||

|

Selective Disclosure |

• |

Selective disclosure occurs when a company discloses material non-public information to one or more individuals or companies and not broadly to the investing public. |

• |

Issuers holding private meetings with analysts, industry conferences etc., must ensure that selective disclosure is not provided in these meetings. |

|

|

||||

|

|

|

|

• |

If unintentional selective disclosure has occurred, issuers must make a full public announcement including contacting the relevant stock exchange and asking that trading be halted. |

|

|

||||

|

|

|

|

• |

Keeping detailed meeting notes and/or transcripts may be useful to determine if unintentional selective disclosure has occurred. |

|

|

||||

|

|

|

|

Reference: Section 5.1 of NP 51-201 |

|

DISCUSSION OF OTHER REGULATORY DEFICIENCIES

1. Mineral Projects

Mining issuers' disclosure must comply with National Instrument 43-101 Standard of Disclosure for Mineral Projects (NI 43-101) including written disclosure contained on an issuer's website such as investor presentations, fact sheets, media articles, and links to third party content. A review of mining issuers' investor presentations identified several areas where issuers need to improve their disclosure in order to better comply with NI 43-101 including:

• Naming the qualified person: naming the individual who approved technical information and noting their relationship to the issuer;

• Preliminary economic assessments: providing required cautionary statements so investors can understand the limitations of study's results;

• Mineral resources and mineral reserves: including a clear statement on whether mineral resources include or exclude mineral reserves;

• Exploration targets: expressing potential quantity and grade as a range and including the required statements outlining the target limitations;

• Historical estimates: including source, date, reliability, and key assumptions along with the required cautionary statements rather than simply stating "not NI 43-101 compliant"; and

• Avoiding overly promotional terms and potentially misleading information especially exploration stage and mineral resource stage issuers: securities legislation prohibits misleading disclosure and misrepresentation. Terms which may be used inappropriately in certain circumstances include: "world-class", "spectacular and exceptional results", "production ready".

Refer to CSA Staff Notice 43-309 Review of Website Investor Presentations by Mining Issuers for further information.

Given the significance of the mining sector in Canadian capital markets, compliance with NI 43-101 and Form 43-101F1 for issuers with mineral projects is critical. We will continue to review mining issuers' website disclosure as part of our overall CD Review Program.

2. Filing of News Releases

Unbalanced and Promotional Disclosure

We continue to see news releases filed by issuers that contain unbalanced and promotional disclosure. In fiscal 2015, staff from certain CSA jurisdictions reviewed the disclosure provided by issuers that publicly announced their intention to enter into Canada's medical marijuana industry. As a result of our review, we published CSA Staff Notice 51-342 Staff Review of Issuers Entering Into Medical Marijuana Business Opportunities (SN 51-342).

The guidance in SN 51-342 is applicable to all industries, particularly companies thinking about material changes to their primary business or where an event has or will have an impact on future prospects.

In general, staff found that issuers' news releases were unbalanced and promotional in nature. While the benefits associated with involvement in the medical marijuana industry were often discussed, these discussions were not consistently accompanied by disclosures about the necessary approvals required to enter the industry, risks, uncertainties, cost implications and time required before the issuer can begin licensed operations. Additionally, a discussion of barriers and obligations to enter the industry was often not provided. Issuers that did not provide sufficient disclosure in their news releases were required to file a clarifying disclosure document as a result of our review. All issuers should provide investors comprehensive, factual and balanced disclosure and avoid promotional commentary.

Issuers should refer to the guidance on best disclosure practices in National Policy 51-201 as well as the disclosure requirements in Part 1(a) of Form 51-102F1.

News Release upon Refiling of CD Documents

We note that certain issuers failed to issue and file a news release on a timely basis after deciding to refile a CD document or restate financial information for comparative periods in financial statements. In certain instances, issuers indicated that the delay to issue a news release was due to the fact that there were no scheduled Audit Committee and/or Board meetings where the news release would be approved. As a result, issuers waited to issue a news release until the next scheduled meeting and in many cases until the actual refiling of the CD documents. In our view, it is not appropriate for issuers to delay the filing of a new release for these reasons.

Section 11.5 of NI 51-102 indicates that if the issuer decides it will re-file a document under NI 51-102 and the information in the refiled document or restated financial information will differ materially from the information originally filed, the issuer must immediately issue and file a news release authorized by an executive officer disclosing the nature and substance of the change or proposed changes. This may involve engaging Audit Committee and/or Board members prior to their next scheduled meeting. This will ensure timely issuance of a news release.

Certain CSA jurisdictions have published a staff notice that provides guidance on their expectations related to refiling of documents by issuers and the associated news releases. We note that certain jurisdictions also maintain a list on their website that includes issuers that amend and refile continuous disclosure documents pursuant to staff's review.

We will continue to monitor issuers' compliance with these requirements.

APPENDIX B

CATEGORIES OF OUTCOMES

Referred to Enforcement/Cease-Traded/Default List

If the issuer has substantive CD deficiencies, we may add the issuer to our default list, issue a cease trade order and/or refer the issuer to enforcement.

Refiling

The issuer must amend and refile certain CD documents or must file a previously unfiled document.

Prospective Changes

The issuer is informed that certain changes or enhancements are required in its next filing as a result of deficiencies identified.

Education and Awareness

The issuer receives a proactive letter alerting it to certain disclosure enhancements that should be considered in its next filing or when staff of local jurisdictions publish staff notices and reports on a variety of continuous disclosure subject matters reflecting best practices and expectations.

No Action Required

The issuer does not need to make any changes or additional filings. The issuer could have been selected in order to monitor overall quality disclosure of a specific topic, observe trends and conduct research.

Questions -- Please refer your questions to any of the following: