CSA Staff Notice 51-348 - Staff’s Review of Social Media Used by Reporting Issuers

CSA Staff Notice 51-348 - Staff’s Review of Social Media Used by Reporting Issuers

CSA Staff Notice 51-348

Staff’s Review of Social Media Used by Reporting Issuers

March 9, 2017

1. EXECUTIVE SUMMARY

Social media has emerged in recent years as a common and important venue for reporting issuers to connect with potential customers, shareholders and other stakeholders. As social media and the use of the internet have become increasingly part of how we communicate information, we have observed a higher proportion of corporate disclosure being provided through chat rooms, investor presentations, blogs and social media websites.

Reporting issuers must constantly be aware of the securities reporting obligations that their social media activities may trigger, even if these activities are not directly intended to communicate with investors. Given that investment decisions are made on material information, it is critical for issuers to adhere to high quality disclosure practices regardless of the venue used for dissemination.

Staff of the Canadian Securities Administrators (Staff or we) are publishing this notice based on a review conducted by the securities regulatory authorities in Alberta, Ontario and Québec. Staff reviewed the disclosure provided on social media by 111 reporting issuers.{1} This included a review of information provided on websites such as Facebook, Twitter, YouTube, LinkedIn, Instagram and GooglePlus, amongst others. We also reviewed the disclosure issuers posted on their own websites, including on any message boards or blogs hosted on those websites.

We reviewed this material to assess whether the disclosure provided in this relatively new and growing disclosure venue adheres to the principles outlined in National Policy 51-201 Disclosure Standards (NP 51-201) and the requirements of National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102).

Our results identified the following three key areas where issuers are expected to improve their disclosure practices:

• Selective or early disclosure when some investors receive material information through social media that other investors do not receive because it is not generally disclosed.

• Misleading and unbalanced social media disclosure where information is not sufficient to provide a complete picture or is inconsistent with information already disclosed by issuers on the System for Electronic Document Analysis and Retrieval (SEDAR).

• Insufficient social media governance policies in place to support social media activity.

In some cases we observed deficient disclosure resulting in material stock price movements, which may have led to investor harm. This illustrates how unintended consequences, including potential securities regulatory action, may arise when social media is misused.

Where deficient disclosure was identified, one or more of the following outcomes occurred:

• Issuers provided clarifying disclosure on SEDAR and/or removed social media disclosure.

• Issuers committed to improving prospective social media disclosure and/or their internal controls and policies.

Given the significant growth in the popularity and use of social media in recent years, we will continue to monitor these areas in our review program activities. Issuers that have not complied will be expected to take corrective action.

2. DISCLOSURE EXPECTATIONS

The following guiding principles, which issuers should consider in order to prevent unbalanced, misleading or selective disclosure, are discussed in securities legislation{2} and in NP 51-201. A summary of disclosure requirements applicable to the presentation of forward-looking information is also included below.

We note that, in some cases, these disclosure expectations refer to our expectations about balanced disclosure for material changes, or for information contained in a press release. High quality disclosure practices are important regardless of the venue of disclosure and, as a result, these disclosure expectations are equally important in the context of social media.{3}

|

Topic |

Disclosure Expectation |

|

|

|

|

Unbalanced and misleading disclosure{4} |

Do not make a statement that is misleading or untrue, or which does not state a fact that is necessary to make the statement not misleading and would be expected to have a significant effect on the market price of a security |

|

|

|

|

|

Announcements of material changes should be factual and balanced |

|

|

|

|

|

Unfavourable news must be disclosed just as promptly and completely as favourable news |

|

|

|

|

|

An issuer's press release should contain enough detail to enable the media and investors to understand the substance and importance of the change it is disclosing |

|

|

|

|

|

Issuers should avoid including unnecessary details, exaggerated reports or promotional commentary |

|

|

|

|

Selective disclosure{5} |

Issuers (and any person or company in a special relationship with a reporting issuer) are prohibited from informing, other than in the necessary course of business, anyone of material non-public information before that material information has been generally disclosed |

|

|

|

|

|

Information has been generally disclosed if it has been disseminated in a manner calculated to effectively reach the marketplace, and if investors have been given a reasonable amount of time to analyze the information |

|

|

|

|

|

Posting material information on an issuer's website is not acceptable as the sole means of satisfying the requirement to "generally disclose" information |

|

|

|

|

Forward-looking information{6} |

An issuer that discloses material forward-looking information must identify it as such and state the material factors or assumptions used to develop the forward-looking information |

|

|

|

|

|

Issuers should discuss in their MD&A events and circumstances that occurred in the period that are reasonably likely to cause actual results to differ materially from material forward-looking information which has been previously disclosed, for a period that is not yet complete |

|

|

|

|

|

Issuers should disclose in their MD&A any differences between actual results and previously disclosed forward-looking information for the period |

{4} The disclosure expectations outlined in securities legislation (as such term is defined in NI 14-101) and in subsection 2.1(2) of NP 51-201 are referred to in this section.

{5} The disclosure expectations outlined in section 3.1 and subsections 3.5(2) and 6.11(1) of NP 51-201 are referred to in this section.

{6} The disclosure requirements outlined in part 4A, part 4B and section 5.8 of NI 51-102 are referred to in this section.

3. REVIEW SCOPE

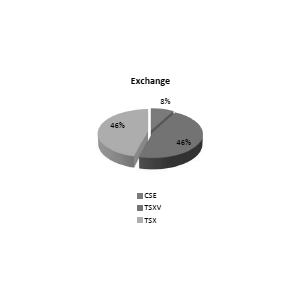

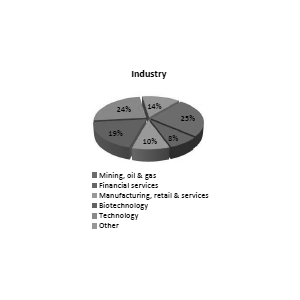

A breakdown of the issuers that we selected for review by stock exchange, industry classification and market capitalization is presented in the charts below.

For many of these issuers, our review noted at least one specific instance of potential non-compliance with securities law in connection with information posted on social media websites. As a result, we sent comment letters with specific compliance-based comments to 44% of the issuers that we reviewed.

4. REVIEW OUTCOMES AND ISSUES IDENTIFIED

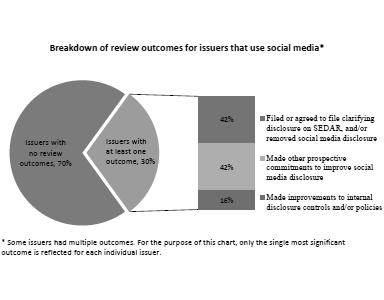

While a majority of the issuers in our sample that used social media did not raise securities related concerns, our review results were significant as 30% of these issuers took action to improve their disclosure in response to issues raised. We also noted that 77% of issuers had not developed specific policies and procedures which would promote internal governance and compliance with securities law in relation to their use of social media.

72% of the issuers that we reviewed were actively using at least one social media website. The following chart provides additional information about the nature and frequency of the different types of outcomes that we obtained for these issuers.

Of the issuers we reviewed that were actively using social media, 25% either filed clarifying disclosure, edited or removed disclosure, or made prospective commitments to improve disclosure. These actions were mainly taken in order to address inconsistencies between specific social media disclosures and certain securities law requirements. In the case of four specific issuers, the original non-compliant disclosure and/or the subsequent correction of that disclosure resulted on average in a 26% movement in the stock prices of the issuers involved. In these cases, the deficient disclosure appeared to be material and Staff may consider further engagement with these issuers.

4.1 Selective Disclosure on Social Media

During our review, we noted that many reporting issuers use social media as a tool for general marketing and customer outreach. Because of the nature and purpose of marketing activities, these issuers may not necessarily intend to provide information on social media websites which could interact with their obligations under securities law. However, an unintended breach of securities law obligations can occur if material non-public information is disclosed improperly.

When issuers disclose material information, they should ensure this information is "generally disclosed" consistent with the disclosure expectations outlined in NP 51-201. Subsection 6.11(1) of NP 51-201 provides that information is not considered to have been generally disclosed solely because it has been disclosed on an issuer's website. Similarly, the disclosure of material information on a social media website alone would not be sufficient in order for information to be considered "generally disclosed" under NP 51-201. As a result, Staff had selective disclosure concerns in instances where material information was posted only on a social media website.

During the course of our review, we identified selective disclosure issues in the following areas.

4.1.1 Forward-Looking Information Disclosed Only on Social Media

We noted a number of instances where issuers provided material forward-looking information on social media websites without ensuring that this information had been generally disclosed to all stakeholders. Forward-looking information provides key information to market participants on future prospects and, as a result, it was not surprising to see significant share price increases in several cases when this information was selectively disclosed on social media. Examples of the type of forward-looking information which we observed being selectively disclosed on social media websites included revenue, earnings per share and cash flow targets. These projections were often material because they were significantly more favourable than historical results or any other information reflected in the issuers' continuous disclosure record.

We also noted instances where the expected timing of significant future milestones, such as the timing for a new product launch or the amount of time before an asset can begin generating revenue, was selectively disclosed on social media websites only.

We had concerns in all of these cases because some investors may have received the information and been aware of it when forming an investment decision, whereas other investors may not have been aware of the selective disclosure. We also noted that issuers who disclosed material forward-looking information on social media websites alone tended not to comply with other disclosure obligations related to forward-looking information. For example, the requirement to provide material factors and assumptions supporting the forward-looking information or the requirement to update the forward-looking information when events occur that make it no longer likely for the target to be met. As a result, this forward-looking information could have been misleading even to those investors who did receive it.

4.1.2 Lack of Coordination about the Timing of Social Media Announcements

We noted instances where the disclosure provided by issuers on social media was eventually generally disclosed on SEDAR or via a news release, but where we still had selective disclosure concerns because the information was released on social media in advance. This included disclosure about events which were not forward-looking but which had recently occurred, such as an issuer having received a licence to begin selling a key product in a new jurisdiction.

In some cases information was posted on social media minutes before it was disclosed elsewhere, and in other cases there was a time delay amounting to days or weeks. Weak social media disclosure controls and governance policies, combined with incorrect assessments that the items being disclosed initially on social media were not material, were often involved in the initial selective disclosure of these items.

4.1.3 Third Party Posts on Social Media Which Suggest Missing Continuous Disclosure

Arm's length third parties often post commentary about issuers through online blogs, message boards or other social media websites. During our review we noted examples of third party posts which suggested that a material event had occurred, such as the insolvency of a major customer, where those events had not been disclosed by an issuer through their continuous disclosure record or otherwise. Although these instances do not relate to social media disclosure provided directly by an issuer, they do point to the importance of social media as a venue for investors to receive potentially material information.

In these cases, investors may have received important information about an issuer which the issuer itself omitted to disclose. We have concerns where investors are receiving material information about an issuer on social media that the issuer itself has not generally disclosed in connection with its ongoing disclosure obligations, because the end result is the selective disclosure of material information.

4.2 Unbalanced or Misleading Disclosure on Social Media

Information posted by issuers on social media websites generally had a strong positive tone. We did not have regulatory concerns solely because an issuer's social media disclosure focused on positive information. However, we noted a number of instances where social media postings were, individually or in the aggregate, sufficiently promotional or unbalanced that they raised concerns under securities law.

NP 51-201 states that an issuer's disclosure should be factual and balanced, giving unfavourable news equal prominence to favourable news. It also indicates that disclosure should include sufficient detail for investors to be able to understand the substance and significance of the events being discussed, and that exaggerated reports and promotional commentary should be excluded.

In connection with our review, all of the issuers identified as having unbalanced or misleading disclosure agreed to improve their use of social media in response to comments raised by Staff.

During the course of our review, we identified misleading or unbalanced disclosure issues in the following areas.

4.2.1 Misleading or Untrue Statements Provided on Social Media

We observed instances where the disclosure provided by issuers on social media was either untrue or promotional to such an extent that it could have misled investors. In several instances, issuers provided commentary or other information about their financial results on social media which did not appear to be consistent with or contained in their continuous disclosure on SEDAR. For example, this occurred when figures being disclosed on social media were non-GAAP financial measures which had not been disclosed in any regulatory filings, or in any other disclosure outside social media. Beyond any selective disclosure issues which may have existed, those investors who had received the non-GAAP financial measure disclosure on social media were not provided with all of the disclosures that issuers should provide when they present non-GAAP financial measures,{7} including a quantitative reconciliation of the non-GAAP financial measure to its most directly comparable GAAP measure. In the absence of these disclosures, investors may be unable to understand the full meaning and significance of the non-GAAP financial measures being disclosed, which can result in their being misled on the basis of incomplete information.

4.2.2 Analyst Reports and Other Articles Provided on Social Media

In some cases, misleading or untrue statements were provided through links to other documents. For example, on Twitter issuers are currently subject to a 140 character limit on information provided in a single post. As a result of this limit we frequently observed issuers providing lengthier commentary through hyperlinks or file attachments. In many cases these links or attachments included reports and research about the issuer from analysts.

When issuers provide copies of reports from independent analysts, they should ensure that they are providing the names and/or recommendations of all independent analysts who cover the issuer.{8} We expect that this disclosure will be provided in order to prevent issuers from selectively disclosing the reports of only those analysts whose views are favourable to the issuer.

We also observed a number of cases where analyst reports, or other third party news articles, included fine print disclosure indicating that they were paid for by the issuer. Some of these documents included stock price targets and valuations for the issuer which were more than double their stock price at the time the report was written. Given that these documents are not independent, issuers should provide more prominent disclosure to that effect in order to avoid misleading investors. Burying a statement at the end of an article or report, or in fine print, that the issuer paid for the publication may raise misleading disclosure concerns around prominence. In these cases, issuers provided clarifying disclosure in connection with our review, in order to highlight that these documents were not independently prepared.

Some issuers posted links to analyst reports or other news articles, where the linked document contained forward-looking information about the issuer. During our review some of these issuers indicated that, while they were no longer on track to achieve these forward-looking targets, they were not responsible for updating the targets because they were solely the opinion of a third party. In these cases Staff asked issuers to provide clarifying disclosure updating the forward-looking targets, because the issuer had effectively endorsed the targets by linking them to a social media post.

4.3 The Importance of a Social Media Governance Policy

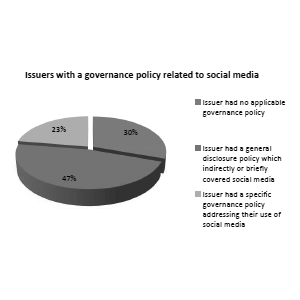

Staff expect reporting issuers to understand the importance of having rigorous governance policies and disclosure practices which ensure the integrity of the disclosure they provide in formal regulatory filings. However, our review found that a significant number of issuers did not have the policies, procedures or controls in place which would be required in order to ensure that similarly high standards are met in the disclosure they provide on social media.

This finding is critically important because a misleading statement causing investor harm has serious implications for the integrity of capital markets. Issuers that provide deficient disclosure on social media may incur significant reputational, regulatory and other costs when addressing deficiencies. In light of the wide popularity of social media and the lack of significant obstacles for issuers and their executive officers to access it, issuers should enhance the strength of their social media governance frameworks.

A strong social media governance policy should include consideration of at least the following items:

• Who can post information about the issuer on social media

• What type of sites (including personal social media accounts vs corporate) can be used

• What type of information about the issuer (financial, legal, operational, marketing, etc.) can be posted on social media

• What, if any, approvals are required before information can be posted

• Who is responsible for monitoring the issuer's social media accounts, including third party postings about the issuer

• What other guidelines and best practices are followed (for example, if an employee posts about the issuer on a personal social media site they should identify themselves as an employee of the issuer)

While not an exhaustive list, we encourage reporting issuers to consider implementing a specific internal policy on social media, meeting the principles disclosed above.

Of the four issuers mentioned above, whose non-compliant social media disclosure resulted in material stock price movements, none had a specific governance policy related to how their directors, officers or employees could or should be using social media websites.

A number of the issuers we reviewed that were using social media agreed to improve their internal policies and practices by either adopting a specific social media governance policy, restricting internal posting access to the issuer's social media websites and/or reminding insiders of their obligations under securities law.

5. QUESTIONS

Please refer your questions to any of the following:

Ontario Securities CommissionSonny RandhawaDeputy Director, Corporate Finance416-204-4959Melanie SokalskySenior Legal Counsel, Corporate Finance416-593-8232Jonathan BlackwellSenior Accountant, Corporate Finance416-593-8138Alberta Securities CommissionRoger PersaudSenior Securities Analyst, Corporate Finance403-297-4324Zara NanjiSecurities Analyst, Corporate Finance403-297-3253Autorité des marchés financiersMartin LatulippeDirector, Continuous Disclosure514-395-0337, ext. 4331Georgia KoutrikasSecurities Analyst, Corporate Finance514-395-0337, ext. 4393British Columbia Securities CommissionAllan LimManager, Corporate Finance604-899-6780Manitoba Securities CommissionWayne BridgemanDeputy Director, Corporate Finance204-945-4905Financial and Consumer Services Commission (New Brunswick)To-Linh HuynhSenior Analyst506-643-7856Nova Scotia Securities CommissionKevin ReddenDirector, Corporate Finance902-424-5343Financial and Consumer Affairs Authority of SaskatchewanTony HerdzikDeputy Director, Corporate Finance306-787-5849

{1} Non-investment fund reporting issuers.

{2} As such term is defined in National Instrument 14-101 Definitions (NI 14-101).

{3} While social media is not explicitly noted in NP 51-201, Staff expect this policy will assist issuers and their officers and directors in meeting disclosure obligations on the use of social media.

{7} CSA Staff Notice 52-306 (Revised) Non-GAAP Financial Measures outlines our disclosure expectations for non-GAAP financial measures.

{8} Refer to the guidance in subsection 5.2(4) of NP 51-201.