CSA Multilateral Staff Notice 51-349 Report on the Review of Investment Entities and Guide for Disclosure Improvements

CSA Multilateral Staff Notice 51-349 Report on the Review of Investment Entities and Guide for Disclosure Improvements

1. Introduction

Staff from the securities regulatory authorities in Ontario, Saskatchewan and Alberta (Staff or we) provide this notice based on a targeted review conducted by the staff from the Ontario Securities Commission (OSC Staff).

OSC Staff recently reviewed the continuous disclosure provided by certain reporting issuers who determined they meet the definition of an investment entity under IFRS 10 Consolidated Financial Statements (IFRS 10), an emerging subsector of the financial services industry that is mainly concentrated in Ontario (the Review).

The Review identified several areas where disclosure could be improved and resulted in many disclosure changes to provide more fulsome information to investors. Overall, OSC Staff observed a wide range in the quality of disclosures provided by investment entities to comply with securities requirements.

This notice summarizes the findings of the Review and also sets out Staff's disclosure expectations and provides guidance to assist investment entities in meeting their ongoing continuous disclosure obligations.

2. Application

Reference to "investment entity" in this notice applies to reporting issuers that have determined they do not meet the definition of an investment fund under National Instrument 81-106 Investment Fund Continuous Disclosure (NI 81-106) and are therefore subject to the requirements of National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102).

In addition to investment entities, some of the observations outlined in this notice may be applicable to non-investment entities that record investments at fair value and we expect these reporting issuers to also consider our findings.

3. Executive Summary

The Review considered compliance with several areas of securities legislation including:

• how reporting issuers met the definition of an investment entity in IFRS 10;

• fair value measurements and disclosures;

• sufficiency of disclosures to understand investment portfolio composition, investment performance, investment strategies and oversight and related risks; and

• disclosure provided by reporting issuers heavily concentrated in only a few investments.

The Review resulted in several outcomes as discussed in Section 5 of this notice. At a high level, we emphasize the following points to investment entities:

• the importance of fair value measurements and entity specific fair value disclosures in both the financial statements and the Management's Discussion & Analysis (MD&A) to help investors understand the performance of the investment entity and judgements made by management;

• with so much dependency on fair value, consider if external expertise is needed to determine fair value of private investments;

• in addition to fair value disclosures, there may be instances where additional investee specific financial information and operational disclosure is necessary to inform an investment decision;

• the unique financial reporting of investment entities does not preclude compliance with other securities requirements such as executive compensation disclosure, business acquisition disclosure and entity specific technical requirements; and

• this is an emerging area where market participants may need to look through the structure and look to other securities requirements for guidance. This notice provides examples of these instances and when investment entities should consider consultation with Staff to determine how specific securities requirements may apply to them.

We will continue to evaluate the disclosure and evolving profile of investment entities and consider the need for policy changes if we believe sufficient disclosure is not being provided to investors.

4. Background

What are the attributes of an investment entity?

To qualify as an investment entity for accounting purposes, a reporting issuer must meet the definition of an investment entity under IFRS 10 which was applicable to reporting issuers for fiscal years beginning on or after January 1, 2014. To meet this definition, a reporting issuer must:

• obtain funds from one or more investors for the purpose of providing those investors with investment management services;

• commit to its investors that its business purpose is to invest funds solely for returns from capital appreciation, investment income, or both; and

• measure and evaluate the performance of substantially all of its investments on a fair value basis.

Except in limited circumstances as described in IFRS 10.32, an investment entity does not consolidate its subsidiaries. Instead, an investment entity measures an investment in a subsidiary at fair value through profit or loss.

Prior to the adoption of IFRS 10, reporting issuers considered Accounting Guideline 18 Investment Companies (AcG 18) in order to determine if they met the definition of an investment company for accounting purposes.

What is the difference between an "investment fund" and an "investment entity"?

One key difference is that an investment entity in the corporate finance regime{1} can hold a significant interest, including a controlling interest in an investee, which is generally precluded under the investment fund regime.

Both continuous disclosure regimes require annual and interim disclosure to investors. However, there are a number of specific differences in the disclosure and regulatory requirements under each regime.

What is the reporting issuer population and what are the emerging trends?

There are approximately 18 reporting issuers that have disclosed they meet the definition of an investment entity under IFRS 10 and for which Ontario is principal regulator (PR). By comparison, there were 6 such reporting issuers when the AcG 18 rules were in effect.

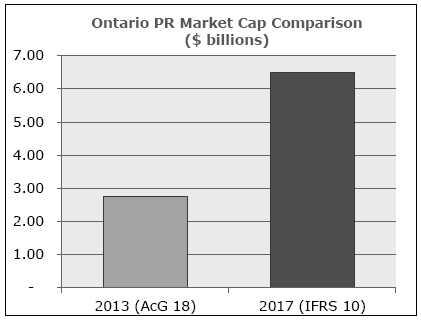

The collective market capitalization of this subsector has increased substantially in recent years from $2.7 billion under AcG 18 in 2013 to approximately $6.5 billion (a 140% increase) presently under IFRS 10. Most investment entities in Ontario are currently listed on the TSX.

Factors contributing to this increase include:

• more reporting issuers have determined that they meet the definition of an investment entity since the adoption of IFRS 10, including reporting issuers who previously consolidated subsidiaries with operations in the resource, insurance and real estate industries;

• some reporting issuers have transitioned from the investment fund regime to the corporate finance regime with the introduction of additional requirements for non-redeemable investment funds that took effect on March 21, 2016; and

• recent initial public offering (IPO) activity in this sector.

OSC Staff have also seen other notable trends with this subsector including:

• a growing number of investment entities have few investments, or one investment that represents a significant portion of their portfolio;

• a larger percentage of portfolio holdings being comprised of investments in private companies;

• investment entities with investments in emerging markets;

• significant related party transactions; and

• larger market cap investment entities holding significant assets have been more common.

Both the growth and evolving profile in this subsector contributed to the initiation of the Review.

What was the purpose and scope of the Review?

OSC Staff examined the continuous disclosure record of 12 investment entities representing over 90% of the market capitalization of investment entities for which the OSC is PR. The sample consisted of investment entities of varying size and investment strategy.

The purpose of the Review was to improve disclosures in material areas, assess accounting areas which require the exercise of significant judgement, and to inform policy related issues given the attributes of this group of reporting issuers.

The following charts illustrate some key attributes of the investment entities reviewed:

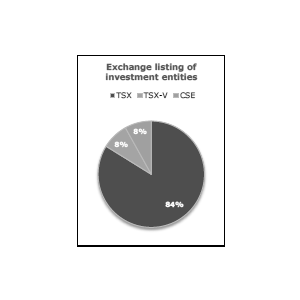

Exchange listing of reporting issuers -- the majority of investment entities are listed on the TSX. Of the 12 investment entities reviewed by OSC Staff, one was listed on each of the TSX-V and CSE.

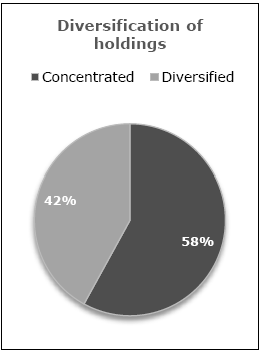

Diversification of holdings -- investment entities with concentrated holdings were considered those with a single investment that represented 20% or more of the fair value of their investment portfolio, excluding cash and cash equivalents, temporary investments and derivative instruments. Additionally, one third of investment entities reviewed by OSC Staff had a single investment that represented 40% or more of their investment portfolio.

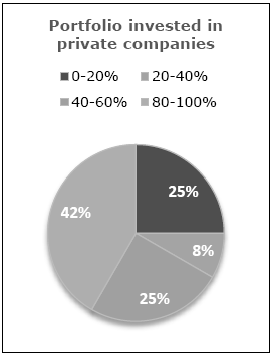

Portfolio invested in private companies -- over 40% of the investment entities reviewed by OSC Staff had invested over 80% of their portfolio in private companies, often resulting in a fair value measurement categorized within level 3 of the fair value hierarchy, and for which information is not publically available.

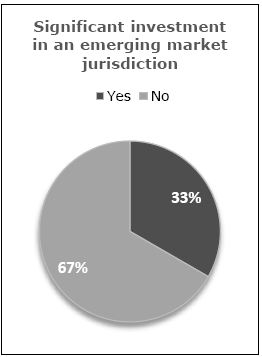

Significant investment in an emerging market jurisdiction -- one third of investment entities reviewed by OSC Staff had a significant investment located in an emerging market jurisdiction.

5. Overall Results

The tables below summarize the outcomes of the 12 reviews. A review may have multiple outcomes.

Overall, the findings were disappointing. Five of the 12 reviews (42%) resulted in the investment entity being placed on the OSC Refilings and Errors List{2} for material disclosure non-compliance issues. Deficiencies included:

Area of disclosure

Reason for placement on the Refilings and Errors List

MD&A

•

insufficient discussion of the investment entity's operations, investments (including portfolio changes) and risks

•

prominence of non-GAAP measures in the MD&A

Annual Information Form (AIF)

•

lack of specific risks and operational information regarding the investment entity's significantly concentrated investments or investments in emerging markets

•

material contracts disclosure was not included

Corporate governance

•

executive compensation, corporate governance or audit committee disclosure was not included in the investment entity's filings

Material contracts

•

material contracts not filed

Technical disclosure

•

a technical report was not filed to support the disclosure of mineral reserves and resources

In addition, the reviews resulted in many prospective disclosure enhancements. Some of the areas OSC Staff requested prospective changes included:

Area of disclosure

Prospective enhancement

Financial statements

•

changes to the valuation approach for investments in private companies

•

fair value disclosures for investments in private companies

•

related party transaction disclosure

•

further disclosure of portfolio composition

MD&A

•

enhanced analysis of fair value changes and valuation methodologies

•

trends and risks for material investments

•

related party transactions and management company fee disclosure

•

summary financial information for significantly concentrated investments

AIF

•

more detailed disclosure for investment selection and criteria, related party transactions, corporate structure, investee specific risk factors and material contracts

Information circular

•

enhanced disclosure for management contracts and executive compensation

Other notable outcomes included:

• the filing of insider and early warning reports not previously filed;

• changes to internal insider reporting policies.

6. Detailed Findings and Guidance

The findings were primarily focused on the following areas:

6.1 Financial Statements

Investment Entity Criteria

Further information was requested when it was not clear from an investment entity's disclosure how it met the definition of an investment entity in IFRS 10. For example:

• When an investment entity appeared to have significant involvement with an investee at an operational level, particularly in instances where its portfolio was significantly concentrated, OSC Staff questioned whether the purpose of the investment was made solely for returns from capital appreciation, investment income, or both. An investment entity may provide management services, strategic advice, and financial support to an investee; however, these activities must not represent a separate substantial business activity or a separate substantial source of income.

• When significant investments were carried at their original cost (i.e. the transaction cost) or when disclosure of the investment entity's determination of the fair value of an investment was limited, it was unclear whether fair value was the primary basis on which the investment entity measures and evaluates the performance of substantially all of its investments.

• When an investment entity's exit strategies were unclear from the review of the reporting issuer's disclosure record.

OSC Staff would also raise questions if an investment entity's portfolio was primarily based on one investment for a period of more than one year and it was unclear whether there was an investment plan in place that could result in the acquisition of several investments in the near term to diversify the investment entity's risk and maximize its returns.

Based on the responses provided, OSC Staff did not object to a reporting issuer's determination that they met the definition of an investment entity in IFRS 10. However, the information received prompted additional requests for enhanced disclosure in certain areas, including MD&A and AIF disclosure to assist investors in understanding the operations and risk profile of the investment entity. The notice addresses these issues further in sections 6.2 and 6.3.

- - - - - - - - - - - - - - - - - - - -

Additional Consideration -- Significant Judgements

Management's determination that a reporting issuer has met the definition of an investment entity often requires significant judgement, in particular when one or more of the typical characteristics of an investment entity (as described in IFRS 10.28) are not present.

Disclosure of such significant judgements, as required generally by IAS 1 Presentation of Financial Statements and specifically by IFRS 12 Disclosure of Interests in Other Entities should include entity specific disclosure of the judgements made, including why the reporting issuer ultimately determined it met the definition of an investment entity.

- - - - - - - - - - - - - - - - - - - -

Disaggregation of Investment Portfolio

Investment funds subject to NI 81-106 are required to provide a statement of investment portfolio as part of its financial statements disclosing the investee name, cost and fair value for each investment held. While not an IFRS requirement, OSC Staff were encouraged that the majority of investment entities in the Review provided this disclosure in their financial statements, or in certain instances, in their MD&A. Where investment entities aggregated their investment portfolio by industry, geography or other categorization, OSC Staff requested further disclosure by investment, similar to the disclosure provided by investment funds.

The investment portfolio should be presented with sufficient disaggregation and transparency to allow an investor to understand the key characteristics of the portfolio composition including the associated risks and the drivers of any change in fair value. Given the nature of an investment entity's business and the importance of understanding the investment portfolio, we believe this objective is best met by disclosing a statement of investment portfolio. This disclosure also helps investment entities meet their MD&A requirements to provide a meaningful analysis of its performance and trends during the period. The following example illustrates useful disclosure of an investment entity's investment portfolio:

EXAMPLE 6.1(a) -- sufficiently disaggregated investment portfolio:

Name

Investment type

%

Location

Average cost

Fair value 2016

Fair value 2015

Investment A

Common shares

52%

Canada

$14m

$9m

$5m

Investment B

Convertible debentures

20%

Chile

$5m

$6m

$6m

Investment C

LP units

15%

Japan

$2m

$2.5m

$1.5m

Disaggregation of Fair Value Gains / Losses

OSC Staff raised comments to understand the components of fair value gains or losses reported on the statement of comprehensive income. When both realized and unrealized fair value gains or losses were presented in the same financial statement line item, OSC Staff requested investment entities to provide supplemental disclosures in the financial statements that clearly reconcile the balance. Staff would expect this disclosure to include the amount that relates to the reversal of previously unrealized fair value gains or losses. For this disclosure, a tabular reconciliation was the most useful. This disclosure assists investors in understanding what portion of the realized gains or losses presented relates to a reversal of unrealized gains or losses previously recorded, and what portion of the unrealized gain or loss relates to the remaining portfolio.

The following example illustrates useful disclosure of the components of an investment entity's fair value gains or losses:

EXAMPLE 6.1(b) -- useful disaggregation of fair value gains or losses:

Net gain on investments

2016

Net realized gain on investments

$100

Reversal of previously recorded unrealized gain on investments (triggered in connection with the sale of investments)

(125)

Change in unrealized gain on investments held at period end

50

Change in unrealized foreign exchange gain on investments

10

Net gain on investments for the period

<<$35>>

Fair Value Measurements{3}

When a specific valuation technique used to determine fair value appeared inconsistent with the objective of fair value measurement{4}, OSC Staff raised comments and questioned the appropriateness of such a valuation technique.

For example, non-independent transaction prices may not be representative of fair value. Additionally, the use of an independent transaction price may not be appropriate after a period of time has elapsed that has rendered the transaction price no longer representative of current fair value. In these instances, we are of the view that use of a separate valuation technique (for example, a discounted cash flow) is necessary to determine the fair value of the investment.

Investment entities and non-investment entities that record investments at fair value should also consider whether management has the necessary expertise to perform a valuation of its investments, particularly when the investment entity holds significant investments which are subject to a fair value measurement categorized within level 3 of the fair value hierarchy. Staff encourage consideration of the use of independent valuation experts where appropriate.

Fair Value Disclosures

As noted above, the majority of the investment entities reviewed have significant investments in private entities, with 40% of the reporting issuers reviewed disclosing investments in private entities that represent greater than 80% of their investment portfolio. The fair value measurements for such investments are inherently subject to a greater degree of management estimation due to the lack of observable inputs, and therefore additional disclosures are required by IFRS 13 Fair Value Measurement (IFRS 13).

IFRS 13.91 recognizes that disclosures of fair value measurements should help users of financial statements assess (a) the valuation techniques and inputs used to develop the fair value measurements; and (b) for recurring fair value measurements using significant level 3 inputs, the effect of the measurements on profit/loss or other comprehensive income.

Significant variance was observed in the level of detail provided for fair value disclosures across investment entities. While some investment entities provided very detailed disclosures, others provided disclosure that was generic or vague making it less useful for investors. For example:

• IFRS 13.93(d) requires, among other things, a description of the valuation technique(s) and the inputs used for fair value measurements categorized within level 2 or level 3 of the fair value hierarchy. Some investment entities did not provide this information.

• IFRS 13.93(g) requires a description of the valuation processes used by the entity for fair value measurements categorized within level 3 of the fair value hierarchy. Some investment entities provided boilerplate disclosure that did not describe their valuation processes in sufficient detail for an investor to understand the processes, including the level of rigour and sophistication that the fair value measurements are subject to.

• IFRS 13.93(h) requires a narrative description of the sensitivity of the fair value measurement categorized within level 3 of the fair value hierarchy to changes in significant unobservable inputs. Some investment entities failed to provide this required disclosure, despite its particular importance when an entity has a significant investment in a private company.

To help contextualize some of the disclosure requirements in IFRS 13, the table in Appendix A provides some disclosure considerations that investment entities and non-investment entities that record investments at fair value may find useful.

Below are illustrative examples of useful entity specific disclosures with specific reference to IFRS 13.93(d) and IFRS 13.93(h).

- - - - - - - - - - - - - - - - - - - -

EXAMPLE 6.1(c) -- useful description of unobservable inputs for IFRS 13.93(d):

The Company determines the fair value of Investment E, a real estate company, using the net present value of estimated future cash flows. The most significant unobservable inputs to this calculation are the estimated rental revenue cash inflows ($7.5 million annually), growth rate (1.5%), and discount rate (12%). The estimated rental revenue cash inflows are based on the type, quality and location of Investment E's properties and are supported by either existing rental agreements or current external market data. Growth rates are based on external market forecasts for Investment E's real estate sectors (office and residential), and discount rates are reflective of current market risks and uncertainties.

- - - - - - - - - - - - - - - - - - - -

EXAMPLE 6.1(d) -- useful sensitivity disclosure for IFRS 13.93(h):

Investment

Unobservable input

Value of input used in valuation

Reasonable potential increase/decrease

Impact on fair value of increase/decrease

Investment A

Gold spot price

$1,300 USD/oz

+/- ×

+/- $×

Discount rate

13.5%

+/- ×

+/- $×

Investment B

Revenue multiple

3×

+/- ×

+/- $×

USD/CAD FX rate

1.35

+/- ×

+/- $×

6.2 Management's Discussion & Analysis

Analysis of Changes to Fair Value and Investment Portfolio Changes

Fair value disclosures are significant in both the understanding of the performance of the investment entity and often the related management and performance fees paid or accrued by an investment entity. To meet the requirements of Item 1.2 -- Overall Performance and Item 1.4 -- Discussion of Operations of Form 51-102F1 Management's Discussion & Analysis (Form 51-102F1), the MD&A must provide sufficient disclosure about the investment entity's material investments and portfolio changes.

OSC Staff raised comments where an investment entity's discussion of the performance of its investment portfolio did not provide enough disclosure to understand:

• material changes to the composition of the investment portfolio (i.e. what specific investments have been purchased/sold or have resulted in unrealized gains and losses during the period); and

• the key drivers of significant fair value changes by investment.

In many cases, the investment entity's disclosure was not granular enough for investors to have a clear understanding of why fair value changed for specific private investments and the risks and trends in its investment portfolio.

Staff expect investment entities and non-investment entities that record investments at fair value to provide a fulsome analysis in the MD&A of the financial and operational trends for material investments which led to the current determination of fair value.

- - - - - - - - - - - - - - - - - - - -

EXAMPLE 6.2(a) -- deficient disclosure of fair value changes

• does not discuss specific investments

• does not explain key drivers for fair value changes

The Company recognized a realized loss on its corporate investments of $4 million and an unrealized gain of $6 million for the fiscal year ended December 31, 2016. The realized loss was attributable primarily to an investment in the technology sector, while the unrealized gain recorded in the current period was due to increases in the fair value of the Company's investments in the manufacturing sector.

- - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - - - - -

EXAMPLE 6.2(b) -- enhanced disclosure of fair value changes

• discusses how investment is valued

• explains key inputs and why fair value changed

The Company recognized a realized loss on its corporate investments of $4 million and an unrealized gain of $6 million for the fiscal year ended December 31, 2016.

The Company's realized loss of $4 million was due primarily to the sale of 1,000,000 common shares of Investment B on October 31, 2016, on which the Company recognized a $3.8 million loss.

The unrealized gain was due primarily to an increase in the fair value of Investment A. The Company determined the fair value of Investment A at December 31, 2016 based on the net present value of estimated future cash flows to be $15 million (an increase of $5.5 million from the prior period). The increase in fair value was due to an increase in the estimated future cash flows as a result of the performance of Investment A in the current period, which accounted for a $4 million increase in fair value, as well as a favorable movement in the USD to CAD foreign exchange rate that increased the fair value of Investment A by $1.5 million.

Specifically, the revenues and gross margin of Investment A increased significantly for the year ended December 31, 2016. Investment A entered a new geographic market in the Southern U.S. in April which resulted in a 20% increase in sales year over year. Investment A also began outsourcing the production of its principal product, which increased margins year over year by 4%.

- - - - - - - - - - - - - - - - - - - -

Disclosure for Significantly Concentrated Investments

One third of the investment entities reviewed had a single investment that represented 40% or more of their portfolio. Where such a significant concentration exists, Staff expect sufficient disclosure about the investment to enable investors to evaluate the performance, operations and risks of the investee. This is of particular importance when the investee is private and disclosure is not otherwise available to investors.

For example, NI 51-102 requires summarized financial information of an investment for reporting issuers with significant equity investees. For investment entities and non-investment entities that record investments at fair value, we are of the view that this information may be reflective of the minimum disclosure necessary for significantly concentrated investments generally and can assist in understanding management's judgements in arriving at fair value.

Most investment entities in the Review sample provided some financial and operational information for their significantly concentrated investments in the MD&A. OSC Staff requested summarized financial information be included in the MD&A when it had not been provided, along with a discussion of those results. OSC Staff also requested further disclosure on the risks and operations of concentrated investments in certain instances when such risks could materially impact the investment entity.

OSC Staff found that the above information was often available to the investment entity as part of its investee monitoring process. We recognize that investment entities may have a concentrated investment for which it does not have direct access to the investee's information. Investment entities that do not have a diversified investment portfolio should consider the need for access to operational and financial investee information upon acquisition.

We may have similar policy concerns and request standalone financial statements as contemplated by National Policy 41-201 Income Trust and Other Indirect Offerings where an investment entity's operations are dependent on a single investment and current disclosures are not sufficient for an investor to make an informed investment decision. Investment entities and non-investment entities that record investments at fair value are encouraged to consult with Staff in this circumstance.

Related Party Transactions

Many investment entities have complex corporate structures, related management companies, and/or other significant related party agreements. Form 51-102F1 requires a discussion of all transactions between related parties as defined by the reporting issuer's generally accepted accounting principles (GAAP).

Many investment entities have a complex management fee structure including ongoing fees and performance based fees. As management fees can be one of the largest expenses of an investment entity, we expect this fee structure and the amounts paid or accrued in the current period to be disclosed in detail in the MD&A. In certain corporate structures where investors receive distributions, the impact of fees on cash flows from operating activities and distributions should also be specifically discussed in the MD&A.

6.3 Annual Information Form

Investment strategies, the investment and management fee structure, and investment specific risk factors are important in understanding the operations and risk profile of an investment entity or a non-investment entity that records investments at fair value. The Review found that:

• the majority of investment entities provided fairly detailed disclosure of its investment policies and oversight, however, some investment entities provided limited disclosure;

• some investment entities with concentrated investments did not provide sufficient investee specific risk factors, including investment entities with investments in emerging markets; and

• in a few instances, more disclosure was required to better understand the investment entity's corporate and management fee structure.

The table in Appendix B provides guidance to illustrate industry specific disclosures consistent with certain requirements of Form 51-102F2 Annual Information Form (Form 51-102F2).

6.4 Information Circular

Executive Compensation Disclosure

In the Review, it was observed that many investment entities have executive management services provided by an external management company (an External Manager). Item 1.3(4) of Form 51-102F6 Statement of Executive Compensation (in respect of financial years ending on or after December 31, 2008) (51-102F6) and Item 2.2 of Form 51-102F6V Statement of Executive Compensation -- Venture Issuers (51-102F6V) requires disclosure of compensation paid to a reporting issuer's named executive officers or NEOs (as defined in 51-102F6) (NEOs), employed or retained by an External Manager.

Where NEOs were paid a salary by the investment entity or the External Manager, OSC Staff found that investment entities were generally disclosing the compensation paid to NEOs. However, it was also observed that compensation to NEOs may be deferred or provided in a manner other than in the form of wages. An illustrative example is where a NEO is also the owner of, or otherwise holds an equity position in, the External Manager. As a result, OSC Staff found certain investment entities disclosing no compensation having been paid to its NEOs, although the investment entity paid a management fee to the External Manager for services that would include the provision of executive management services.

The provisions of 51-102F6 and 51-102F6V are intended to capture the wide variety of ways in which the form, timing and manner of compensation can be made. Investment entities and their boards of directors should make every attempt to allocate what they view to be the portion of the management fee attributable to the services provided by their NEOs, regardless of how compensation is paid.

- - - - - - - - - - - - - - - - - - - -

EXAMPLE 6.4(a) -- deficient executive compensation disclosure

• does not identify NEOs

• no compensation disclosed for NEOs

The Company paid $2,000,000 to the Manager under the Management Agreement for the year ended December 31, 2016. The Company's officers are not employees of the Company. The services of the Company's officers are provided pursuant to the Management Agreement.

- - - - - - - - - - - - - - - - - - - -

EXAMPLE 6.4(b) -- enhanced executive compensation disclosure

• provides an allocation of the management fee for NEO services

Name

Year

Salary ($)

Share-- based awards ($)

Non-equity incentive plan compensation ($)

Pension value ($)

All other compensation ($)

Total ($)

CEO

2016

300K

Nil

Nil

Nil

Nil

300K

CFO

2016

250K

Nil

Nil

Nil

Nil

250K

The Company paid $2,000,000 to the Manager under the Management Agreement for the year ended December 31, 2016. The services of the CEO and CFO are provided pursuant to the Management Agreement. The salary of the CEO and CFO reflect an allocation of the management fee attributable to the services of the CEO and CFO based on the estimated fair value of such services.

Management Contracts

In the Review, it was noted that many investment entities have an external investment manager that provides investment management or advisory services to the investment entity (an Investment Manager).

In light of an investment entity's overall business being generally the investment of funds for capital appreciation, investment income and other returns, OSC Staff may take the view that an Investment Manager is performing a substantial management function of the investment entity, depending on the services and authority that the Investment Manager had with respect to the investment decisions of the investment entity. For example, where an Investment Manager exercised significant discretion in selecting and executing upon investments for an investment entity's portfolio, OSC Staff took the view that it was providing a substantial management function of the investment entity.

In such cases, an investment entity should be aware of the disclosure requirements relating to the agreement entered into with its Investment Manager, particularly with respect to the filing of material contracts under Part 12 of NI 51-102 and disclosure under Item 13 of Form 51-102F5 -- Information Circular.

6.5 Insider Reporting

The operations of an investment entity may result in certain insider reporting considerations. While the majority of the reviews did not identify insider reporting non-compliance, OSC Staff did observe the following:

• Not all investment entities considered their Investment Managers to be reporting insiders under NI 55-104 Insider Reporting Requirements and Exemptions (NI 55-104). Subparagraph (f) to the definition of "reporting insider" (Subparagraph (f)) includes a management company (including its directors, certain executives and significant shareholders) that provides significant management or administrative services to the investment entity or a major subsidiary. In light of an investment entity's overall business (as described above) and the role performed by an Investment Manager in such business, OSC Staff have taken the view that an Investment Manager is a reporting insider pursuant to Subparagraph (f).

• Insider and early warning reports were not filed for certain investment holdings.

- - - - - - - - - - - - - - - - - - - -

Additional Insider Reporting Considerations -- Concentrated Investments

Investment entities with significantly concentrated investments should also consider whether the investee and/or its officers or directors are reporting insiders under the definition of "reporting insider" of NI 55-104. We encourage reporting issuers to adopt internal policies prohibiting trading by insiders of material investees in the securities of the reporting issuer while in the possession of material undisclosed information about such investee entities.

- - - - - - - - - - - - - - - - - - - -

6.6 Other Considerations

Investment Entity Reporting Issuers with Material Mining or Oil and Gas Investments

Investment entities with material mining or oil and gas investments need to consider the applicability of technical disclosure requirements in NI 43-101 Standards of Disclosure for Mineral Projects (NI 43-101) and NI 51-101 Standards of Disclosure for Oil and Gas Activities in their filings.

For example, the disclosure of technical information relating to a material investee may trigger the requirement to file a technical report under NI 43-101. In addition, if the investment entity files an AIF, disclosure requirements of Item 5.4 -- Companies with Mineral Projects or Item 5.5 -- Companies with Oil and Gas Activities of Form 51-102F2 may apply.

Investment entities are encouraged to consult Staff if there is uncertainty relating to the applicability of the above requirements.

Prospectus Pre-Filing Matters

IPOs of investment entities may raise disclosure and regulatory policy concerns when the investment entity has few investments or when the net proceeds of the offering are largely unallocated. We recommend submitting a pre-filing application to address these issues with Staff in advance of the filing of a preliminary prospectus.

Conclusion

In Ontario, we have seen an increase in the number of reporting issuers that have determined they are an investment entity under IFRS 10 and therefore, except in limited circumstances, measure substantially all of their investments at fair value through profit and loss, including investments in subsidiaries. While some investment entities have provided detailed disclosures in continuous disclosure filings, improvements were required in many areas to provide sufficient disclosure to investors. Investment entities must ensure investors are receiving complete and transparent information about their underlying investments to make informed investment decisions.

Companies considering an IPO or a change in business to become an investment entity should carefully consider the disclosure requirements detailed above and the guidance in this notice to assist them with meeting the regulatory requirements following the adoption of the investment entity provisions of IFRS 10.

We will continue to evaluate the disclosure of our reporting issuers that are investment entities and will consider the need for policy changes if we believe these reporting issuers are not providing sufficient disclosure to their investors.

Questions

Please refer your questions to any of the following people:

Ontario Securities Commission

Sonny Randhawa

Deputy Director, Corporate Finance

(416) 204-4959

Mark Pinch

Associate Chief Accountant, Office of the Chief Accountant

(416) 593-8057

Jodie Hancock

Senior Accountant, Corporate Finance

(416) 593-2316

Tamara Driscoll

Accountant, Corporate Finance

(416) 596-4292

Steven Oh

Legal Counsel, Corporate Finance

(416) 595-8778

Financial and Consumer Affairs Authority of Saskatchewan

Tony Herdzik

Deputy Director, Corporate Finance

(306) 787-5849

Alberta Securities Commission

Cheryl McGillivray

Manager, Corporate Finance

(403) 297-3307

{1} Reporting issuers in the corporate finance regime are subject to the requirements of NI 51-102, rather than the requirements of NI 81-106.

{2} This list is available on the OSC website at: http://www.osc.gov.on.ca/en/Investors_refilings-errors-list.htm

{3} For additional observations on fair value measurements and disclosures, please refer to OSC Staff Notice 52-723 Office of the Chief Accountant Financial Reporting Bulletin (November 2016) which can be found on the OSC website at: http://www.osc.gov.on.ca/en/SecuritiesLaw_sn_20161124_52-723_financial-reporting-bulletin.htm

{4} The objective of a fair value measurement is to estimate the price at which an orderly transaction to sell the asset or to transfer the liability would take place between market participants at the measurement date under current market conditions.

APPENDIX A

FAIR VALUE MEASUREMENT DISCLOSURE CONSIDERATIONS

|

IFRS 13 Requirement{5} |

Disclosure Considerations |

|

|

|

||

|

Description of valuation processes |

• |

Who is responsible for determining and reviewing fair value measurements? Does the investment entity have a valuation committee? |

|

|

||

|

IFRS 13.93(g) |

• |

What is the role of the board of directors and the audit committee in fair value measurements? |

|

|

• |

Does the investment entity engage the services of an independent valuation expert? |

|

|

||

|

Description of valuation techniques and inputs |

• |

When comparable companies are considered in the fair value analysis, how does management determine which companies are considered comparable? |

|

|

||

|

IFRS 13.93(d) |

• |

When recent transaction prices are utilized, what did management consider to be "recent"? At what time would management determine that a transaction price was outdated and therefore not reflective of current fair value? |

|

|

• |

How does management consider other relevant factors such as investee performance to plan, general industry conditions, funding availability and liquidity discounts in its valuation? |

|

|

||

|

Quantitative information about significant unobservable inputs |

• |

Is disclosure detailed enough to understand the use of discount rates, valuation multiples, expected volatility, discounts for lack of marketability and how they are derived? |

|

|

||

|

IFRS 13.93(d) |

• |

Does the disclosure of an input that is used in the valuation of multiple investments (such as a discount rate) have a wide range that suggests information is not sufficiently disaggregated by investment? |

|

|

||

|

Disclosures for each class of assets |

• |

Does the investment entity's determination of asset classes give adequate consideration to the nature, characteristics and risks of its investment portfolio? |

|

|

||

|

IFRS 13.93 & 94 |

• |

Do risks differ by industry or stage of development of the investee resulting in additional disaggregation being useful? |

|

|

||

|

Description of sensitivity to changes in unobservable inputs |

• |

Would a change in unobservable inputs result in a materially different fair value measurement? |

|

|

||

|

IFRS 13.93(h) |

• |

What are the interrelationships between unobservable inputs used in the fair value measurement? How would those interrelationships magnify or mitigate the effect of changes in the unobservable inputs on the fair value measurement? |

{5} IFRS 13.93(d) is applicable to fair value measurements categorized within level 2 or level 3 of the fair value hierarchy, while IFRS 13.93(g) and (h) are applicable only to those categorized within level 3.

APPENDIX B

DISCLOSURE GUIDANCE TO MEET THE REQUIREMENTS OF FORM 51-102F2

|

Form 51-102F2 Requirement |

Disclosure Considerations |

|

|

|

||

|

Corporate Structure |

• |

Does disclosure also provide an understanding of the investment entity's investment structure and fees with entities that provide management or advisory services? |

|

Item 3 of Form 51-102F2 |

|

|

|

|

||

|

|

<<Investment Strategies and Oversight:>> |

|

|

Description of Business |

• |

What are the criteria used for investment selection? Are there targets or restrictions by geography, industry, stage of development or type of security? |

|

Item 5.1 of Form 51-102F2 |

• |

What is the time horizon for investments and how are investments anticipated to be realized? |

|

|

• |

What is the investment entity's involvement with investee companies? Is there involvement on the board of directors of investee companies? |

|

|

• |

What processes does the investment entity have to monitor ongoing performance? What information is reviewed by the investment entity? |

|

|

• |

Who is on the investment committee and what are the key responsibilities of the committee? |

|

|

• |

What is the role of an Investment Manager vs the investment entity? |

|

|

• |

What is the role of the board of directors in approving investment purchases, sales and valuations? |

|

|

||

|

|

<<Concentrated Investments>> |

|

|

|

• |

What information is required to understand the operations and industries of significant and material investees? |

|

|

||

|

Risk Factors |

• |

What are the key risks related to the reporting issuer's investment strategy? Is concentration risk, currency risk or valuation risk related to investments in private companies adequately disclosed? |

|

Item 5.2 of Form 51-102F2 |

• |

Does the investment or fee structure result in conflicts of interest? How is this risk mitigated? |

|

|

• |

What are the risks of the industries that the investment entity significantly invests in? |

|

|

• |

For concentrated investments, what are the key risks of the investee? |

|

|

• |

What are the regulatory, legal and economic risks of investing in companies that operate in emerging markets? |

|

|

||

|

Material Contracts |

• |

Are agreements to provide management or investment services included as material contracts? |

|

Item 15 of Form 51-102F2 |

• |

Are agreements with significant investees and credit agreements considered to be material contracts? |