OSC Staff Notice - OSC Bulletin Version: 51-706 - Corporate Finance Report

OSC Staff Notice - OSC Bulletin Version: 51-706 - Corporate Finance Report

OSC STAFF NOTICE 51-706

CORPORATE FINANCE BRANCH REPORT 2007

1. Introduction

A. Purpose of this report

The 2007 Corporate Finance Branch report summarizes the operational activities of the Corporate Finance Branch (Corporate Finance, the Branch or we). This report includes the results of our reviews from April 1, 2006 to March 31, 2007 and discusses key issues that we consider to be of interest to issuers and their advisors. While the discussion about our reviews relates to our 2007 fiscal year, the remainder of the report covers issues arising after March 31, 2007.

We encourage issuers to use this report as a self-assessment tool to strengthen their compliance with Ontario securities law and as guidance in preparing their filings.

B. Highlights

The following are highlights from our operational activities:

- Industry specialization. We rolled out our new structure for continuous disclosure (CD) reviews based on industry specialization.

- Shift in type of CD reviews. We conducted more targeted and issue-oriented reviews of issuers' filings to assess and facilitate compliance with specific CD requirements and accounting standards. This resulted in more refilings of CD documents than in the 2006 fiscal year.

- Offering documents. We saw an increase in the total number of offering documents filed this year. This was primarily driven by an increase in use of the short form prospectus system. As a result, we completed more full and issue-oriented reviews of offering documents than in the 2006 fiscal year.

- Mergers and acquisitions. We participated in three significant regulatory hearings on mergers and acquisitions matters in 2006 and 2007: Falconbridge Limited, Sears Canada Inc. and Sterling Centrecorp. Inc.

- Service standards. We improved our performance against our service standards.

C. About the Branch

(i) Our mandate

The Branch is responsible for regulating reporting issuers other than investment funds and for leading issuer-related policy initiatives. The Ontario Securities Commission (OSC) establishes the regulatory framework for securities offerings in the public and exempt markets, and we monitor compliance through prospectus and rights offering reviews.

The Branch is also responsible for developing requirements for ongoing dissemination of information by issuers and promotes compliance with these requirements through our comprehensive CD review program. A specialized team monitors compliance with Ontario securities law in take-over bids and other mergers and acquisitions activity.

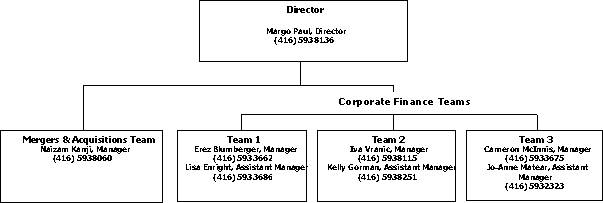

(ii) Structure

The Branch is led by the Director and includes four teams consisting of lawyers, accountants, geologists, administrative and clerical staff.

- Corporate Finance teams. There are three Corporate Finance teams. The lawyers, accountants and geologists in each team conduct prospectus and CD reviews, review and process exemptive relief applications, and carry out policy and project work.

The review officers on Team 1 are involved in preliminary prospectus receipting, basic prospectus reviews, applications administration and exempt market reporting. The review officers on Team 2 are responsible for insider reporting review and the SEDI business function. The financial examiners on Team 3 are responsible for tracking CD filings.

- Mergers & Acquisitions team. This team is responsible for matters relating to take-over bids, issuer bids, business combinations, related party transactions and significant acquisitions of securities of reporting issuers.

2. Continuous disclosure

Our CD review program continues to evolve. This year, we began focusing our reviews along industry lines. The industry groups are as follows:

- banking and insurance

- mining

- technology

- entertainment/communications

- financial services

- retail and services

- real estate

- manufacturing

- biotechnology and healthcare, and

- other.

Industry specialization allows us to gain a greater understanding of the specific issues and concerns of each industry. It also helps us to conduct CD reviews more efficiently and to address key risk areas, accounting issues and general disclosure issues affecting these industries.

A. Issuer profile

There are approximately 4,100 reporting issuers (other than investment funds) in Ontario. We are the principal regulator and generally have responsibility for all reporting issuers with head offices in Ontario. Over 1,100 reporting issuers have head offices in Ontario, representing 35% of Canada's market capitalization.

|

Total Ontario market capitalization

|

$784 billion

|

|

|

|

|

Total Canadian market capitalization

|

$2.25 trillion

|

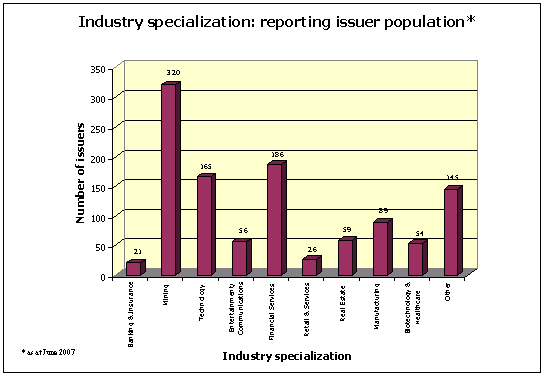

The chart below shows the number of Ontario reporting issuers by industry.

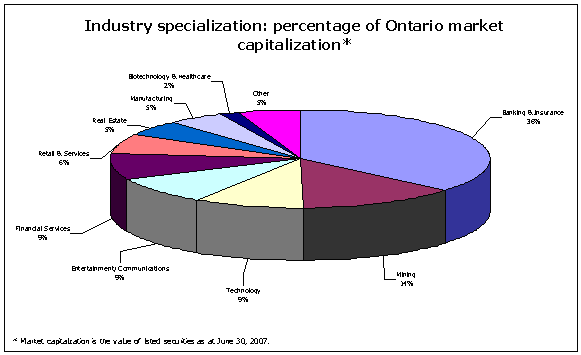

The chart below shows the percentage market capitalization of reporting issuers by industry. The banking and insurance industry represents 36% of the Ontario market capitalization, although there are a relatively small number of reporting issuers in this industry. The mining industry has the largest number of reporting issuers (320) and represents 14% of the Ontario market capitalization.

B. Risk-based approach

We use a risk-based approach to select issuers for CD or prospectus review and to determine the type of review to conduct. Our risk-based procedures incorporate both qualitative and quantitative criteria. The criteria are designed to identify issuers whose disclosure is most likely to be materially improved or brought into compliance with Ontario securities law or accounting standards as a result of our review.

Based on the results of our assessment of the qualitative and quantitative criteria, we may conduct a full, issue-oriented, basic or targeted review. For more information about our selection criteria, see OSC Staff Notice 11-719 A Risk-based Approach for More Effective Regulation.

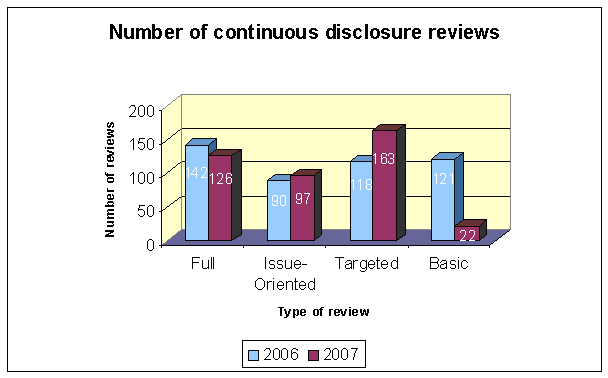

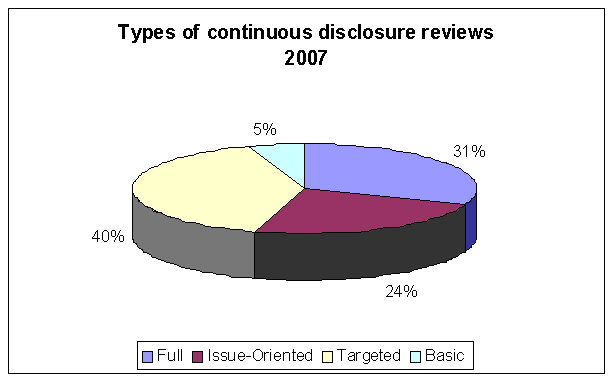

C. Summary of CD reviews

Last year, we completed 408 CD reviews consisting of 163 targeted reviews, 97 issue-oriented reviews, 126 full reviews and 22 basic reviews.

The charts below show the types of reviews for each of the past two fiscal years and the percentage breakdown for the 2007 fiscal year.

Fifty-five per cent of our CD reviews related to issuers listed on the Toronto Stock Exchange (TSX) and 26% related to issuers listed on the TSX Venture Exchange (TSXV). The remaining 19% related to issuers with securities listed over-the-counter, on CNQ or on other trading forums.

D. Targeted reviews

A large percentage of our reviews this year were targeted reviews. Targeted reviews are an effective way to assess issuers' understanding of new accounting standards and regulatory requirements.

This year, we focused our targeted reviews on the following areas:

- Multilateral Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (MI 52-109). We reviewed annual certificates and annual management discussion and analysis (MD&A) to assess compliance with the requirements of MI 52-109. For more information, see Canadian Securities Administrators (CSA) Staff Notice 52-315 Certification Compliance Review.

- Multilateral Instrument 52-110 Audit Committees. We continued to assess compliance with audit committee composition and responsibilities requirements. For more information, see CSA Staff Notice 52-318 Audit Committee Follow-up Compliance Review.

- National Instrument 58-101 Disclosure of Corporate Governance Practices (NI 58-101). We reviewed compliance with the disclosure requirements in NI 58-101. For more information, see CSA Staff Notice 58-303 Corporate Governance Disclosure Compliance Review.

- National Instrument 43-101 Standards of Disclosure for Mineral Projects (NI 43-101). We continued to review the filings of mining issuers to assess compliance with the technical report requirements under NI 43-101. Please refer to the mining issuer discussion below for the most frequently occurring deficiencies.

E. Industry groups

Staff in each industry group has developed a strategic plan and has begun reviews to address the unique issues and concerns of their industry. We have highlighted some of the key initiatives undertaken by four industry specialization groups this year.

(i) Banking and insurance issuers

Banking

Ontario's banking industry, although small in number of issuers, represents approximately 22% of the Ontario market capitalization. The banks are subject to the Office of the Superintendent of Financial Institution's supervisory and disclosure requirements and the guidelines and supervisory standards set by the Basel Committee on Banking Supervision, which promote the quality of banking supervision and disclosure worldwide.

The accounting policies relevant to the banking industry rely heavily on management making significant estimates and assumptions that affect the reported amounts of assets, liabilities and net income, along with related disclosures. Some of the key areas where estimates and assumptions are made include the allowance for credit losses, accounting for financial instruments, securitizations, impairment and contingent liabilities. Our reviews focused on the adequacy of the disclosure in these areas, as any changes in the estimates and assumptions used by management can have a significant impact on a bank's results and related disclosures.

Also imperative in assessing a bank's operations and business is the understanding of risks, exposures to potential losses and the processes a bank has in place to manage and monitor those risks. As a result, our reviews also centred on the adequacy and transparency of a bank's disclosure of the management of its key risks, such as credit risk and market risk. This disclosure assists investors in understanding the trends and risks that affect the financial results and the trends and risks that are reasonably likely to affect future results.

Insurance

The Ontario insurance market includes life insurance companies and property and casualty insurance companies. The life insurance industry is dominated by relatively few very large issuers. Most of them are publicly listed companies and are among the largest insurance companies the world.

The Canadian property and casualty insurance industry consists of more than 200 smaller companies, most of which are not public. Relatively few property and casualty insurance companies are reporting issuers in Ontario.

The business models and accounting standards for both types of insurance issuers are very complex and have inherent uncertainties. For example, compared to most other industries, insurance companies rely heavily on estimates, particularly actuarial estimates. Therefore, our reviews focus on the adequacy of the disclosures of risks and uncertainties and the disclosure related to the actuarial estimates. The discussion of risks and uncertainties in the MD&A and annual information form (AIF) should allow investors to assess the impact of risks and trends on the issuer's financial statements in terms of liquidity, capital and operations, as well as on future performance.

Specifically, this disclosure should address:

- the sensitivity of earnings to potential changes in circumstances, both quantitative and qualitative

- current and prospective risks exposures

- risk management strategies and practices

- whether the issuer's returns are commensurate with the risks it has assumed, and

- its risks in comparison to those of its peer group.

Loss reserves are generally the largest liability recorded on an insurance issuer's balance sheet. Since these reserves are largely based on actuarial methods and assumptions, it is critical for issuers to provide adequate transparency of how the reserves are calculated.

Issuers should provide detail and discussion of the underlying assumptions and estimates that contribute to the financial results.

Disclosure of the underlying assumptions in narrative form and in numerical form is necessary for an understanding of the financial results. Loss reserves are considered a critical accounting estimate and issuers should ensure that they make the disclosures required by item 1.12 of Form 51-102F1 Management Discussion & Analysis (Form 51-102F1).

(ii) Mining issuers

Ontario is the principal regulator of approximately 320 reporting issuers operating in the mining industry. These issuers have a combined market capitalization of more than $107 billion representing 14% of Ontario's market capitalization. Issuers listed on the TSX account for 94% of the industry's market capitalization. The remaining 6% is made up of issuers that are listed on the TSXV, CNQ or are unlisted.

The stage of development of a mining company largely determines its risk profile. Mining issuers can range from start-up companies that conduct a single grass-roots exploration program to multinational companies that develop and operate producing mines throughout the world.

We factor the stage of development of an issuer into how we design and conduct our reviews. Teams of accountants and geologists examine the issuer's CD record, including both its financial and technical disclosure. It is essential that technical and financial disclosure for all mining issuers is factual and balanced. Given the importance of technical disclosure, the focus this year has been on compliance with technical report requirements.

Common NI 43-101 deficiencies

We noted the following frequently occurring deficiencies in technical disclosure that was filed in the 2007 fiscal year:

- No budget. The technical report must include a budget that breaks down costs for each phase of work.

- Incomplete technical reports. The technical report must include all material scientific and technical information as of the date the report is filed.

- Technical disclosure does not set out key assumptions, parameters and methods used to estimate mineral resources. All of these must be included in the technical report.

- Disclaimers of portions of technical report. Disclaimers of responsibility are not permitted for scientific or technical information.

- Consent of qualified person not filed with technical report. A consent must be filed for each qualified person responsible for preparing or supervising each portion of the report.

- Incomplete certificates. The certificate of a qualified person must include all information required by NI 43-101.

- Technical report not filed within prescribed period. The technical report must be filed within 45 days of a news release that discloses material information on a material property.

- News releases do not contain prescribed cautionary language or identify the qualified person. News releases must contain prescribed cautionary language or identify the qualified person who is responsible for the technical disclosure in the release.

Allocation of purchase price of mining assets

Allocation of the purchase price for mining properties can be very complex because issuers are required to allocate the excess of the purchase price over the fair value of net assets between mineral rights and goodwill. EIC 152 Mining Assets - Impairments and Business Combinations (EIC 152) requires issuers to incorporate value beyond proven and probable reserves (VBPP) in allocating the purchase price of a business combination and for testing a mining asset for impairment. Issuers are cautioned that the application of EIC 152 requires VBPP to be factored into a supporting valuation.

If an issuer applies EIC 152 incorrectly, we may require the issuer to restate and refile its financial statements with a revised purchase price allocation.

(iii) Technology issuers

Ontario has approximately 165 reporting issuers in the technology industry. These issuers have a market capitalization of more than $71 billion. The largest 10 make up 86% of this total market capitalization.

The technology business generally falls into one or more of the following four general categories: hardware, software, Internet-related services and other electronic services (i.e. electronic storage providers). Issuers range from small start-up companies developing a new product or service with no revenue to large established international companies selling multiple products and services with significant, sustainable revenues.

Some of the more significant recurring issues that we have identified in our reviews relate to revenue recognition and measurement of stock-based compensation. Errors have resulted in issuers having to restate their financial statements and MD&A. The accounting standards in these areas are often complex and can be a challenge for issuers and their advisors.

Multiple-deliverable arrangements

A technology company may sell a variety of products or services to a customer over a period of time or at different points in time. In our reviews, we noted that some issuers did not correctly apply EIC 142 Revenue Arrangements with Multiple Deliverables (EIC 142) to determine whether there should be separate units of accounting. This can result in improper revenue recognition.

When applying the guidance in EIC 142, issuers should be mindful of separate contracts or agreements that are, in substance, parts of a single arrangement. When determining whether a single arrangement with multiple deliverables exists, issuers should conduct proper analysis to combine contracts or agreements that, for instance, were negotiated within a short time frame of each other or were interdependent on each other.

In instances when separate contracts or agreements are combined for determining whether a single arrangement with multiple deliverables exists, issuers are reminded that contractually stated prices in these contracts or agreements should not be presumed to represent fair value.

Stock-based compensation

Incorrectly measuring the fair value of stock-based compensation is not limited to issuers in the technology industry. However, the prevalent use of stock options in the technology industry tends to magnify the importance of the error for these issuers.

Option pricing models generally require the use of expected volatility to calculate the fair value of stock options. Volatility is a measure of how a stock's price has fluctuated over time. It is measured using the standard deviation of returns for the stock. Most issuers use historical volatility as a proxy for expected volatility, as permitted by accounting standards.

We encountered many instances where issuers incorrectly calculated their historical volatility. One common error is calculating volatility using the standard deviation of the stock price. Another common error is not annualizing the calculated volatility, which results in an underestimation of the stock's anticipated fluctuation. The result is understated compensation expense, which may lead to restatements.

(iv) Biotechnology and healthcare issuers

The biotechnology and healthcare industry has a total of 54 reporting issuers. Thirty-one issuers are listed on the TSX, 23 are listed on the TSXV and the remainder are listed on NASDAQ or other exchanges. The market capitalization of these issuers is approximately $12 billion. This represents 50% of the Canadian market capitalization for the biotechnology and healthcare industry.

In our review of issuers in this industry, we have raised concerns relating to revenue recognition and the filing of material contracts.

Revenue recognition

We have noted two significant revenue recognition issues in the biotechnology and healthcare industry:

- revenue recognition policies do not contain detailed disclosure of material terms of contracts, and

- inappropriate timing and measurement of revenue recognition.

Detailed disclosure of material terms of contracts

Biotechnology and healthcare issuers may have arrangements with a number of pharmaceutical companies. We have noted that the terms, conditions and circumstances of each arrangement may differ significantly and are often not adequately discussed in the revenue recognition policy as required by CICA Handbook section 3400 Revenue. As a result, it is important that issuers provide detailed disclosure of revenue recognition accounting policies for all material arrangements.

Timing and measurement of revenue recognition

Particular revenue recognition issues related to timing and measurement are as follows:

- Timing of recognition of "up-front" fees. We have noted that some issuers are recognizing up-front fees (fees that are typically received at the beginning of a contract) when they are received, not when they are earned. In accordance with EIC 141 Revenue Recognition (EIC 141), up-front fees should generally be deferred and amortized based on the terms of the contractual arrangement.

- Revenue arrangements with multiple deliverables. We have noted that management often has difficulty assessing the fair value of arrangements and we are continuing to monitor this issue. These revenue arrangements are often complex and require management to make judgments about the fair value of the individual elements of the arrangement. Both EIC 141 and EIC 142 provide guidance in this area.

Filing of material contracts

We have noted instances where biotechnology and healthcare issuers have not filed material contracts in accordance with the requirements under Ontario securities law. For example, some issuers are not filing contracts at all or are inappropriately redacting information in the contracts. We are particularly concerned when these contracts relate to material revenue arrangements. When non-compliance is noted, we have asked the issuer to make the appropriate filings.

F. Other segments

We have also identified income trusts and smaller business issuers as areas of focus due to the distinctive concerns regarding these groups. These issuers can be from any industry.

(i) Smaller issuers

Smaller issuers with head offices in Ontario represent over 40% of the Ontario issuer population but less than half of 1% of the Ontario market capitalization.

These issuers tend to have a market capitalization of less than $25 million and are listed on the TSXV, NEX or CNQ, or are unlisted. In addition, they have one or more of the following characteristics:

- fewer lines of business than larger issuers

- leadership by management with significant ownership interest

- fewer management and other staff, who have a wide range of duties

- limited ability to attract and retain resources in line and support positions, including accounting and internal audit, and

- more restricted access to external advisors.

Our primary strategy to assist smaller issuers in complying with their obligations is education. By increasing their awareness of their CD obligations and the common deficiencies we see when we review the CD record of smaller issuers, we hope to increase compliance.

Two key education initiatives that we undertook in the 2007 fiscal year were:

- Webpage. In April 2007, we launched a webpage on the OSC website that consolidates information of interest to smaller issuers. The webpage is at http://www.osc.gov.on.ca/PublicCompanies/SmallBusiness/sb_index.jsp. It highlights some of the more frequently referred to rules and regulations, and includes reports from staff on disclosure deficiencies noted during various CD reviews.

- Outreach. We look for opportunities to speak directly to smaller issuers such as participating in a workshop on smaller issuers' MD&A at the CICA's Financial Reporting and Accounting Conference. In the past, we have also communicated with smaller issuers by emailing them a copy of CSA Staff Notice 51-316 Continuous Disclosure Review of Smaller Issuers, which addresses deficiencies we found in financial statements, MD&A, mining and oil and gas disclosure, and other disclosure.

In addition, we continue to engage with our community of smaller issuers through the Small Business Advisory Committee (SBAC). SBAC was established in 2002 and serves as a forum for communication between the OSC and smaller issuers. It plays a critical role in helping us understand and address ongoing issues that face this sector.

(ii) Income trust issuers

There are approximately 235 income trusts in Canada representing a market capitalization of just over $200 billion.{1} In October 2006, the Federal Government's Department of Finance announced proposed new legislation that would impose additional income taxes upon publicly traded income trusts beginning in fiscal 2011.

In July 2007, in response to this legislation being "substantively enacted" for accounting purposes, the CICA Emerging Issues Committee issued a Draft Abstract, D67, dealing with the impact of the enactment on the recognition of future income tax assets or liabilities by an income trust.

Prior to June 2007, in accordance with CICA Handbook section 3465 Income Taxes, income trusts estimated the future income tax on certain temporary differences between amounts recorded on its balance sheet for book and tax purposes at a nil effective tax rate. Under the legislation, and as outlined in the Draft Abstract, income trusts must now estimate the effective tax rate on the post 2010 reversal of these temporary differences. We intend to monitor disclosures provided by income trust issuers for interim periods ending on or after June 30, 2007 to review the impact of this accounting requirement.

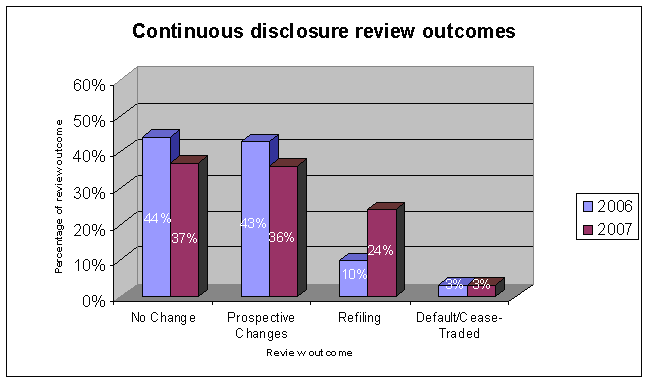

G. General review outcomes

Possible outcomes from a CD review are:

- No changes. No changes or additional filings were determined necessary.

- Prospective changes. The issuer makes the changes in its next filings.

- Refilings. The issuer amends or refiles certain CD documents.

- Default list and cease trade orders. If the issuer has key CD deficiencies, we may place the issuer on the OSC's list of reporting issuers that are in default or we may issue a cease trade order.

The following chart shows the range of review outcomes in the 2007 fiscal year.

Thirty-six per cent of the outcomes involved prospective accounting and disclosure improvements. This is a decrease from 43% in 2006. Twenty-four per cent of the outcomes led to refilings. This is an increase from 10% in the 2006 fiscal year. This increase is largely a result of non-compliance with MI 52-109.

Common areas of concern resulting in prospective changes, refilings or defaults

While some of the outcomes are specific to an industry sector, we also identified some common areas of concern.

Certification

As noted, the majority of refilings related to non-compliance with MI 52-109. This was largely due to a failure by issuers to include in the annual MD&A their certifying officers' conclusions about the effectiveness of disclosure controls and procedures.

MD&A

MD&A continues to be an area that requires more attention. The objectives of the MD&A requirements are to provide a narrative explanation, through the eyes of management, of the issuer's performance, position and future prospects.

Issuers are required to provide a full, in-depth analysis of their results of operations and financial condition in the most recently completed financial year, including a comparison against the previously completed financial year. This involves a comprehensive analysis of why material changes have occurred, including a quantitative and qualitative explanation.

We continue to see situations where issuers repeat information from financial statements and do not provide any management insight on why items are changing or not changing. The MD&A should include a discussion of key value drivers, analysis of known trends and a general description of where the business is heading.

Analysis of risks and uncertainties continues to be a weak area. Some issuers are simply cross-referencing or duplicating the risk factor disclosure. Form 51-102F1 requires an analysis of how material risks and uncertainties may affect the business, not just a description of the risks.

Other areas of concern are inadequate disclosure about related party transactions and failure to provide a clear description, including sensitivity analysis, of critical accounting estimates.

Financial statements

Revenue recognition

Revenue recognition continues to raise issues. In particular, we have seen boilerplate disclosure, particularly relating to the identification and description of revenue recognition triggers for each revenue stream.

Segment reporting

Problems have arisen with the disclosure of reportable operating segments. In particular, we have noted the following:

- failure to disclose information about reportable segments for the current interim period and cumulatively for the current year to date

- no disclosure of information about assumptions in determining segments

- failure to ensure that assumptions are consistent with the way business is conducted

- no disclosure of information required for geographic segments, and

- incorrect application of the aggregation criteria for segments.

Indefinite life intangible assets

Some issuers have misclassified definite life intangible assets as indefinite life intangible assets and are unable to establish the economic useful life for these assets.

CICA Handbook section 3062 Goodwill and Other Intangible Assets requires the best estimate of the useful life of these assets to be used and sets out factors that should be considered. When no legal, regulatory, contractual, competitive, economic or other factors limit the useful life of an intangible asset to the enterprise, the useful life of the asset is considered to be indefinite.

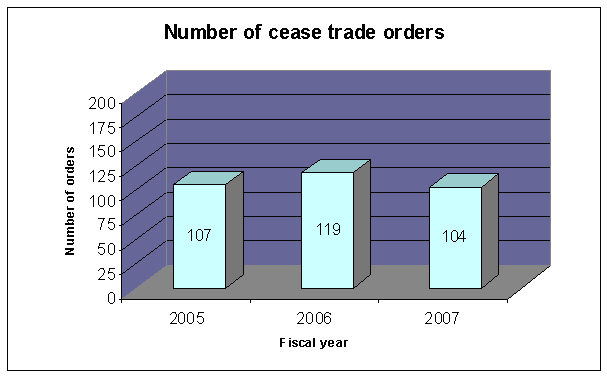

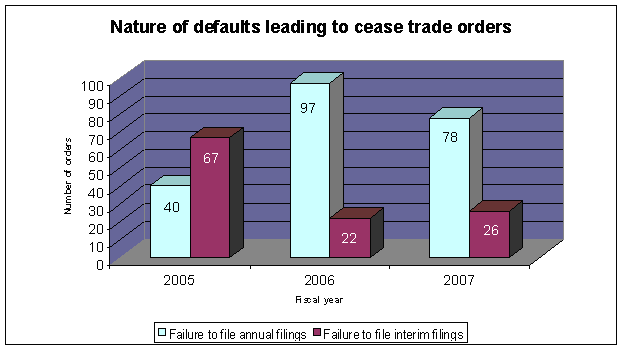

H. Cease trade orders

The OSC may issue a cease trade order when a reporting issuer fails to file the required CD documents.

The number of cease trade orders in the 2007 fiscal year was relatively consistent with the previous two fiscal years. In the 2007 fiscal year, the OSC issued 104 cease trade orders for failure to comply with CD filing requirements, compared to 119 in the 2006 fiscal year and 107 in the 2005 fiscal year.

The majority of the cease trade orders issued in the 2007 fiscal year related to failure to file financial statements and MD&A in accordance with Ontario securities law.

I. Restatements and refilings

(i) Identification of errors as a result of a CD review

Material errors in CD filings may be identified through our review process or by the reporting issuer and its advisors. This year, we continued to see a number of errors that led to restatements and refilings.

We will place an issuer on the OSC's refilings and errors list if, as a result of our review, the issuer:

- is required to restate and refile financial statements

- implements accounting or disclosure changes on a retroactive basis, where the changes represent the correction of an error in the information as originally filed

- amends and refiles other CD documents, or

- files CD documents which were required to be filed at an earlier date.

(ii) Notice of error

We remind issuers that they must immediately issue and file a news release under section 11.5 of National Instrument 51-102 Continuous Disclosure Obligations (NI 51-102) if a material error or deficiency is identified that will result in a refiling of a document or restatement of financial information previously filed under NI 51-102. The news release must disclose the nature and substance of the error or deficiency.

It is not appropriate to wait until the next required filing or earnings release to disclose the error, even if the issuer requires more time to quantify all aspects of the error.

J. 2007/08 CD review program

In addition to continuing our focus on industry specialization, we plan to conduct the following targeted reviews in the 2008 fiscal year:

(i) Financial instruments

Most reporting issuers will be affected by the new financial instruments standards that became effective for fiscal years commencing on or after October 1, 2006. These standards include new CICA Handbook section 3855 Financial Instruments - Recognition and Measurement, section 3865 Hedges, section 3861 Financial Instruments - Disclosure and Presentation and section 1530 Comprehensive Income. The new standards affect any issuer that uses financial instruments, not just issuers in the financial services sector.

The new standards require issuers to examine and classify their financial instruments into five main categories:

- held for trading

- held to maturity

- loans and receivables

- available for sale, and

- other financial liabilities.

The measurement basis used and the presentation of gains and losses will depend on how the issuer has classified its financial instruments. The new standards are premised on fair value being the most relevant measure for financial instruments and the only relevant measure for derivatives. Based on our observations to date, the classification of financial instruments, even among issuers in similar industries, varies based on the issuer's intent to hold or sell the instrument and its risk strategies. This makes comparing financial results of like issuers more challenging and highlights the need for meaningful disclosure.

Given the new measurement and disclosure standards, our reviews across all industry groups will consider the issuer's application and disclosure of the financial instruments standards. If this is unclear from the public disclosure, we may ask the issuer to explain its classification of financial instruments upon adoption of the standards and the resulting transition adjustments. We may ask the issuer how it has identified derivatives, including embedded derivatives, depending on the nature of the issuer's business and its disclosure in this area.

Our reviews will also focus on how an issuer has considered the new measurement considerations for items such as transaction costs and the extensive fair value guidance, including the appendix to section 3855 of the CICA Handbook, in its recording of financial instruments. In these areas, disclosure is essential to understanding key assumptions in determining fair value, especially when valuation techniques and internal models are used. Issuers are reminded of the new disclosure requirements set out in section 3861 of the CICA Handbook and the disclosures for critical accounting estimates and financial instruments required by Form 51-102F1.

(ii) Environmental reporting

Reporting issuers are required to disclose certain environmental matters in their CD documents. For example, they must disclose:

- material changes immediately, including those relating to environmental matters, and

- material facts, risks and uncertainties, including those of an environmental nature, relating to their operations in their MD&A and their AIF.

In addition, Form 51-102F2 Annual Information Form (Form 51-102F2) requires:

- disclosure of the financial and operational effects of environmental protection requirements on the issuer's capital expenditures, earnings and competitive position in the current financial year and the expected effect in future years

- a description of environmental policies that are fundamental to operations, such as policies regarding the issuer's relationship with the environment, and the steps taken to implement them, and

- risk factors relating to the issuer and its business, including environmental and health risks.

Investors are increasingly interested in environmental matters and any impact they may have on the issuer's future operations and financial results. As a result, we will be completing a targeted review, primarily focusing on issuers in the extractive industry, to determine whether they are complying with environmental reporting requirements.

(iii) Options timing

In September 2006, the CSA issued Staff Notice 51-320 Options Backdating (Staff Notice 51-320). When a company grants options to executives, claiming that they were granted at an earlier date (when the exercise price would be more favourable), this is commonly referred to as "options backdating". Staff Notice 51-320 also identified another options timing issue, specifically circumstances where issuers may have timed the granting of stock options based on their expectations of stock price movements.

As indicated in Staff Notice 51-320, we look at the timing of option grants as part of our CD program. This year, we developed a risk-based analytical model for identifying issuers that appear to display indications of options timing issues to assist us in better selecting issuers for review. Our options timing reviews are ongoing and are a significant element of our targeted review program for 2007/08.

3. Offerings

A. Review program

(i) Type of offering document

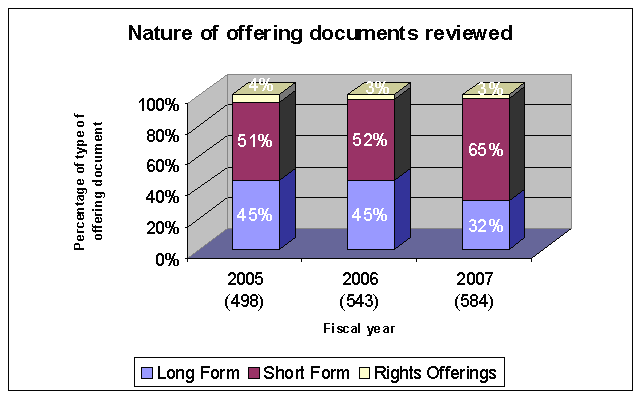

In the 2007 fiscal year, we processed 584 prospectuses and rights offering circulars, compared to 543 in 2006 and 498 in 2005.

We also saw a change in the composition of offering documents reviewed. Sixty-five per cent of the offering documents reviewed were short form prospectuses and 32% were long form prospectuses. Short form prospectuses represented 52% of the total offering documents reviewed in the 2006 fiscal year and 51% in the 2005 fiscal year.

The chart below shows the percentage and type of offering documents reviewed in each of the past three fiscal years.

The increase in use of the short form prospectus system over the last year is primarily due to the implementation of amended and restated National Instrument 44-101 Short Form Prospectus Distributions (NI 44-101) on December 30, 2005. As a result of these amendments, essentially all issuers that have a current AIF can take advantage of the short form prospectus regime.

(ii) Reviews completed

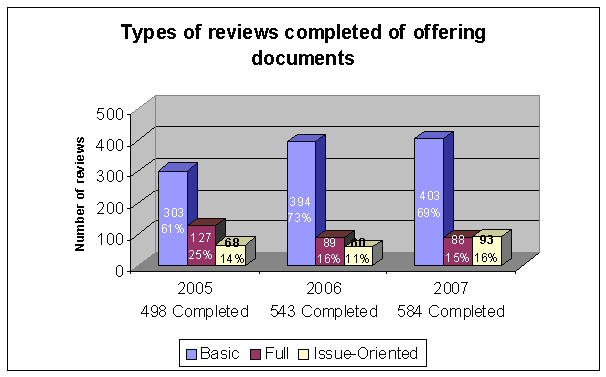

Consistent with our approach to CD reviews, we use a selective review system as a tool for determining the level of scrutiny to apply to each prospectus. There are three possible outcomes under our selective review system: basic review, full review and issue-oriented review. For more information about these reviews, see OSC Staff Notice 11-719 A Risk-based Approach for More Effective Regulation.

During the 2007 fiscal year, we completed 88 full reviews. Twenty-eight reviews related to short form offerings, 45 related to long form offerings and the remaining related to rights offerings. We also completed 93 issue-oriented reviews (89 short form offerings and four long form offerings).

While the number of full reviews is consistent with the 2006 fiscal year, we conducted 5% more issue-oriented reviews in the 2007 fiscal year than we did in 2006.

The chart below shows the number of offering documents reviewed in each of the past three fiscal years.

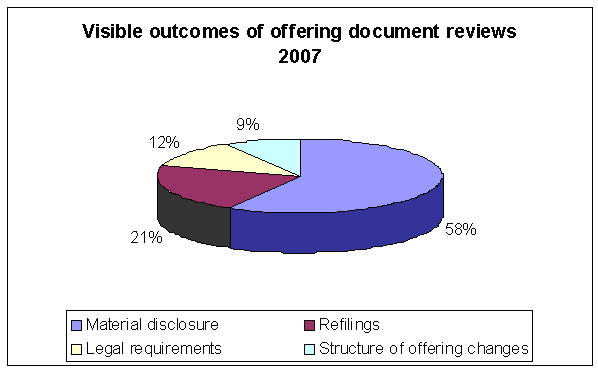

Overall, there were outcomes on 72% of the offering documents we reviewed. This year, we changed the way we report outcomes on offering document reviews. We now have two categories of outcomes: visible outcomes and non-visible outcomes.

Visible outcomes accounted for 70% of the outcomes. This category includes items that are visible in some way from the public record, such as refilings, material accounting changes, other material disclosure enhancements, additional legal requirements being imposed and changes to the offering structure. It also includes cases where we place an issuer on the default list. Approximately half of our visible outcomes were disclosure enhancements in the offering document.

The chart below shows the visible outcomes of our reviews during the 2007 fiscal year.

Non-visible outcomes accounted for 30% of the outcomes. This category includes items that are not found on the public record, but are significant to our mandate in other ways, such as policy or procedural enhancements implemented by an issuer as a result of our review and referrals to the OSC's Enforcement Branch. These outcomes can be of ongoing value because they inform the issuer about our expectations, raise new policy issues for our consideration or enhance our knowledge of the market as a whole.

B. Current issues

(i) Convertible debenture offerings with an interest payment election feature

We recently reviewed a number of prospectuses involving distributions of convertible debentures or similar convertible debt securities.

Some of these prospectuses contained disclosure about an interest payment election feature. This feature allows the issuer to raise funds to satisfy part or all of its obligations to pay interest on the debentures by issuing additional freely tradeable securities to a debenture trustee.

The disclosure typically provides that if the issuer makes the interest payment election, the debenture trustee will:

- accept delivery of securities from the issuer

- accept bids with respect to, and consummate sales of, those securities, as the issuer directs in its absolute discretion, and\

- deliver proceeds of those sales to debenture holders sufficient to satisfy the issuer's interest payment obligations.

The disclosure makes it clear that, whether or not the issuer elects to fund its interest obligation by issuing additional securities, the debenture holders will be entitled to receive cash in an aggregate amount equal to the interest payable.

We question the basis on which the issuer is able to deliver freely tradable securities to a debenture trustee for sale to the public to finance the interest obligations. We take the view that a prospectus relating to the offering of debentures does not extend to future distributions of securities to members of the public in order to finance the issuer's interest obligations to the purchasers of the debentures.

Accordingly, we believe that the exemptions in section 2.42 of National Instrument 45-106 Prospectus and Registration Exemptions (NI 45-106) and section 2.10 of National Instrument 45-102 Resale of Securities (NI 45-102) are not available to the issuer for the distribution of these securities.

If an issuer proposes to satisfy an interest obligation to debenture holders by delivery of additional freely tradable securities to the debenture holders, we will generally remind the issuer to consider the OSC's decision and reasons In the Matter of Crystallex International Corporation dated April 27, 1999.

(ii) Asset-backed securities - incorporation by reference

Over the past several years, we have received a number of applications from issuers of asset-backed securities (ABS issuers) for relief from certain requirements in NI 51-102 and from the certification requirements in MI 52-109.

As explained in OSC Staff Notice 51-706 Corporate Finance Report (2005), we have generally been prepared to recommend CD relief and related certification relief for certain ABS issuers if those issuers make alternative filings. These include filings of:

- monthly distribution date statements

- interim MD&A with respect to the custodial pools, filed on a quarterly basis

- an annual compliance certificate, and

- an annual accountants' report.

We remind ABS issuers and other market participants to consider the mandatory incorporation by reference provisions in items 11.1(1)(8) and (9) of Form 44-101F1 Short Form Prospectus (Form 44-101F1). Our practice is that unless an ABS issuer requests and obtains pre-file relief, as described below, the ABS issuer is required, as a consequence of these provisions, to incorporate by reference the alternative filings described above into any short form prospectus.

We acknowledge that certain ABS issuers may not have contemplated that the alternative filings described above may be subject to an incorporation by reference requirement when the issuer was first established. In many cases, applications for relief from the requirements of NI 51-102 and MI 52-109 were filed before December 2005, when the mandatory incorporation by reference provisions were first introduced. Accordingly, at the time those applications were filed, the issuers may not have had an opportunity to consider whether additional relief would be required.

In light of this concern and in consultation with staff in the other jurisdictions, we have agreed as a transitional measure to recommend limited relief to ABS issuers while we consider these questions further.

Accordingly, we will recommend an exemption from the requirements in items 11.1(1)(8) and (9) of Form 44-101F1 to incorporate by reference the alternative filings described above in the prospectus (with the final receipt evidencing the requested relief) if the final prospectus includes a prominent statement (e.g., in the section identifying the documents incorporated by reference) substantially as follows:

All material information in the distribution date statements will be contained in the issuer's interim and annual management's discussion and analysis.

Recent amendments to securities laws may require the distribution date statements, an annual statement of compliance by the servicers of the receivables and certain related assets acquired by the issuer and an annual accountants' report prepared by a firm of independent public or chartered accountants respecting compliance by such servicers with the Uniform Single Attestation Program for Mortgage Bankers, or such other servicing standard acceptable to the regulators (the Accountants' Report), to be incorporated by reference in this short form prospectus. The issuer has requested an exemption from this requirement from the regulators. This exemption would be evidenced by the issuance of a receipt for this short form prospectus by the regulators.

If an ABS issuer wants to request this relief, it should:

- file a pre-file request in accordance with the pre-file procedures described in Part 9 of National Policy 43-201 Mutual Reliance Review System for Prospectuses (NP 43-201) and in Part A7 of Appendix A of proposed National Instrument 11-102 Passport System (NI 11-102), and

- confirm that the final version of the prospectus will contain disclosure substantially in the form of the above.

(iii) Use of proceeds

General issues

We have recently raised comments relating to the adequacy of the disclosure in the use of proceeds section of the prospectus. For example, we have noted that:

- in some offerings, the principal purpose of the offering is simply described as for general corporate purposes, for potential acquisitions or for working capital

- when a purpose is identified, a significant portion of the remaining proceeds is not allocated to any purpose, and

- when the proceeds are allocated among specific purposes, the prospectus also includes disclosure indicating that management has broad discretion concerning the use of proceeds and that there is no assurance that the proceeds will be used in this manner.

We remind issuers that item 7 of Form 41-501F1 Information Required in a Prospectus (Form 41-501F1) and item 4 of Form 44-101F1 requires issuers to describe in reasonable detail each of the principal purposes, with approximate amounts, for which the issuer will use the net proceeds. If appropriate, this information should be presented in a table.

As indicated in the instructions in item 7 of Form 41-501F1 and the proposed amendments to item 4 of Form 44-101F1 (as published for comment on December 22, 2006), the use of the phrase "for general corporate purposes" will generally not be sufficient. Similarly, we take the view that using the phrases "for potential acquisitions" or "for working capital", without other disclosure, will generally not be sufficient.

Potential acquisitions

We have also reviewed a number of prospectuses that indicate that a principal purpose of the offering is for potential acquisitions, but contain little or no disclosure about these potential acquisitions. Instead, the prospectuses have contained disclosure to the effect that:

- the issuer is currently evaluating various potential acquisition opportunities, some of which would, if consummated, have a material impact on the issuer

- although no commitments have been made with respect to any transaction, there have been significant discussions in certain cases, and

- an agreement on one or more acquisition transactions may be reached shortly following the closing of the offering, in which case all or a portion of the net proceeds of the offering may be allocated to effect those acquisitions.

For disclosure relating to potential acquisitions that are otherwise not described in the prospectus, we may request details such as:

- a description of the potential acquisitions, including, for example, a description of the businesses or entities involved, a description of the discussions with shareholders or management and clarification on whether the issuer has entered into any agreements in principle, letters of intent or other similar arrangements and whether they are binding or non-binding

- the anticipated material impact of these potential acquisitions on the issuer, including a description of how the issuer has concluded that the potential acquisitions are not probable acquisitions or that information relating to the potential acquisitions should not otherwise be considered material to an investor

- the criteria management uses to identify potential acquisitions, and/or

- how the proceeds of the offering will be invested or used pending the completion of an acquisition.

Mining issuers

We remind issuers in the mining sector that disclosure about mineral projects must support the disclosure in their NI 43-101 technical reports.

Issuers are asked to enhance the disclosure in the prospectus when:

- there are inconsistencies between the disclosure in the prospectus and the recommended work plan in the technical report, or

- there is insufficient disclosure in the prospectus to support the disclosure in the technical report.

We will ask issuers to describe in the prospectus the principal purposes for which they are intending to use the net proceeds from the offering and the approximate amount they intend to use for each purpose in order to support the disclosure in the technical report.

(iv) Eligibility for short form prospectus distributions

As noted above, NI 44-101 was amended, effective December 30, 2005, to significantly expand the class of issuers that are eligible to file a short form prospectus.

Issuers and their advisors are reminded that short form eligibility is based on the issuer having filed all periodic and timely disclosure documents. We have seen a number of situations where this has not been the case. This may result in delays in the offering process.

Examples include:

- a failure to file, or a substantively deficient filing of, a technical report required under NI 43-101

- a failure to file, a failure to incorporate by reference, or a substantively deficient filing of, a business acquisition report required under NI 51-102, and

- a substantively deficient MD&A filing that does not meet the requirements of Form 51-102F1.

4. Applications for exemptive relief

A. Review of applications

(i) Number of applications

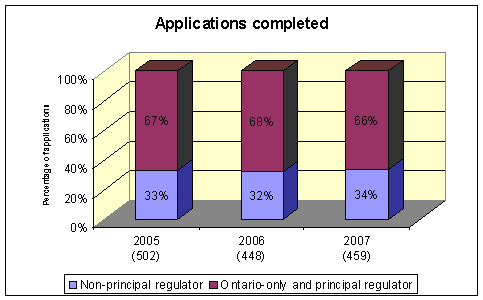

In the 2007 fiscal year, we completed 459 applications for exemptive relief. This compares to 448 in the 2006 fiscal year and 502 in the 2005 fiscal year.

In each of the 2007 and 2006 fiscal years, 305 of the applications completed were only filed in Ontario or were filed in one or more Canadian jurisdictions and the OSC was the principal regulator. This compares to 335 applications in the 2005 fiscal year.

The chart below shows the number of applications completed in each of the past three fiscal years.

(ii) Nature of applications

The applications requested a variety of exemptive relief. Approximately 20% of the applications were for orders not to be a reporting issuer. Applications for exemptions from the CD requirements, the prospectus and registration requirements, and the take-over bid and issuer bid requirements were also common. Each of these represented approximately 10% of the applications completed.

We monitor the nature of relief sought to determine whether there are any routine or frequently occurring issues. Where appropriate, we have proposed amendments to our requirements to eliminate the need for exemptive relief or have addressed issues in frequently asked questions or other notices.

For example, relief from the business acquisition report (BAR) requirements represented approximately 25% of the applications for relief from the CD requirements. When an issuer completes a significant acquisition of a business, it is required to file a BAR under NI 51-102. Since this requirement was implemented in 2004, we have been monitoring the nature of relief granted in respect of BAR requirements. This year, we made changes to NI 51-102, including significant changes to the BAR requirements, which came into effect on December 29, 2006.

The amendments include:

- eliminating the requirement for non-venture issuers to test significance at the 40% level

- requiring only one year of audited financial statements of the acquired business, with unaudited comparative information

- permitting incorporation by reference of previously filed financial statements of the acquired business

- introducing new exemptions from the interim financial statement requirements for the acquired business if certain criteria are met, and

- revising the significance tests in certain circumstances.

The amendments simplify the BAR requirements and codify certain exemptive relief applications. The amendments also streamline business acquisition reporting for issuers.

B. Current issues

(i) At-the-market prospectus distributions

We recently reviewed applications for exemptive relief to permit issuers and underwriters to make at-the-market (ATM) prospectus distributions in Canada.

An ATM distribution is essentially an offering of securities under a base shelf prospectus into an existing market, such as the TSX. It allows the issuer to sell securities through the TSX as if the issuer were an ordinary secondary market seller. As a practical matter, the ATM model collapses the distinction between the primary market and the secondary market.

Features of an ATM distribution

The following are the fundamental features of the proposed ATM distribution model:

- The issuer enters into an equity distribution agreement with an underwriter, under which the issuer may issue and sell equity securities of the issuer in accordance with Part 9 of National Instrument 44-102 Shelf Distributions.

- The issuer files a base shelf prospectus to qualify the distributions of securities through the TSX to purchasers under the ATM distributions.

- The underwriter, acting as agent, signs the prospectus.

- The prospectus is filed with the securities regulatory authorities, but is not physically delivered to the purchasers. The ATM distribution model is based on the concept of constructive delivery as delivery of the prospectus is not practicable in the circumstance as the issuer and the underwriter will generally be unaware of the identity of the purchasers.

- Whenever the issuer wants to raise money through an ATM distribution, the issuer places a sell order with the underwriter. The underwriter processes this sell order in the same manner as any other sell order and puts the order into the ordinary order flow. In the case of the sale of a large block, this may include a special terms or over-the-counter trade.

- From the perspective of the issuer, the sale of newly issued securities from treasury into the secondary market is a primary offering and is a distribution qualified by prospectus.

Granting relief

To effect an ATM distribution, issuers and underwriters have sought relief from the following:

- the prospectus delivery requirement in section 71(1) of the Securities Act (Ontario) (the Act) with the result that the two-day right of withdrawal in section 71(2) of the Act does not apply, and

- certain prospectus requirements, such as the form requirements which prescribe language describing purchasers' statutory rights.

The requested relief was granted subject to the following conditions:

- Registration. All underwriters involved in the ATM distribution must be appropriately registered.

- Modified prospectus certificate. The issuer and the underwriter must sign a modified form of the prospectus certificate that brings the currency of the prospectus forward to the date of distribution.

- Impact on statutory rights. The prospectus must state that the purchasers' statutory rights for rescission or damages if the prospectus contains a misrepresentation remain unaffected by the non-delivery of the prospectus and the relief granted.

- Monthly reporting. The issuer must file monthly reports regarding the securities distributed under the ATM prospectus.

- Quarterly reporting. The issuer must also disclose details regarding the securities distributed under the ATM prospectus in its annual and interim financial statements and MD&A.

- Limit on distributions. The market value of equity securities distributed under the ATM prospectus cannot exceed 10% of the aggregate market value of the issuer's outstanding equity securities of the same class as the class of securities distributed.

- Daily limits on securities distributed. The number of equity securities that may be distributed under an ATM distribution agreement on any trading day cannot exceed 25% of the trading volume of the securities on the TSX on that day.

- No over-allotment. No underwriter or dealer distributing equity securities under the ATM prospectus can over-allot the securities or effect a transaction that is intended to stabilize or maintain the market price of the securities.

For an example of this relief, see In the matter of Canetic Resources Trust, SG Americas Securities, LLC, FirstEnergy Capital Corp. and FIMAT Canada Inc. dated July 24, 2007.

(ii) Application to treat non-controlled entity as a subsidiary for purposes of section 2.24 of NI 45-106

We have recently reviewed a number of applications for relief to permit an issuer to distribute securities to employees of a non-controlled entity in which the issuer has a significant equity investment.

In these applications, the filers have argued that the relief sought is similar to the exemption contained in section 2.24 of NI 45-106 (the employee exemption) for trades by an issuer in a security of the issuer to employees, executive officers, directors and consultants of the issuer or to persons with such a relationship (a specified relationship) with a related entity (as defined in section 2.22 of NI 45-106) of the issuer.

We believe that the concept of control is a fundamental aspect of the related entity definition and the employee exemption in general. Accordingly, the situations are not analogous.

The employee exemption reflects the value in promoting employee participation in, and ownership of, the employee's direct employer. We do not believe that it is in the public interest to permit exempt distributions of securities to employees of a non-controlled entity simply because the issuer has a significant equity investment.

Issuers making this type of application must demonstrate that the proposed recipients of the securities do not require the protection afforded by registrant involvement or the benefits of a prospectus and should not rely on the fact that they are employees.

(iii) Becoming a reporting issuer in Ontario through a securities exchange take-over bid

We have received applications where the filer is undertaking a securities exchange take-over bid of an offeree issuer. The filer is not a reporting issuer in a Canadian jurisdiction, but the structure of the take-over bid will result in the filer becoming a reporting issuer at different dates in different Canadian jurisdictions.

The relief requested is for the filer to be ordered to be a reporting issuer in all applicable Canadian jurisdictions on the same date. This will ensure that the securities of the filer issued under the securities exchange take-over bid are subject to the same resale treatment in all Canadian jurisdictions.

Securities issued under the securities exchange take-over bid are subject to a seasoning period under section 2.6 of NI 45-102, which deems the first trade in securities to be a distribution unless certain conditions are met. Section 2.11 of NI 45-102 provides an exemption from a seasoning period, provided that, among other things, the offeror was a reporting issuer on the date the securities of the offeree issuer were first taken up under the take-over bid.

The relief is needed so the issuer does not find itself with a four-month seasoning period in Ontario while the securities are freely tradeable elsewhere.

For examples of this relief, see In the matter of James Richardson International Limited dated March 28, 2007 and In the matter of US Gold Canadian Acquisition Corporation dated June 1, 2006.

5. Mergers and acquisitions activities

A. Significant regulatory hearings

The OSC held three significant mergers and acquisitions hearings in 2006 and 2007. These hearings addressed important aspects of the regulatory framework applicable to mergers and acquisitions in Ontario, including the treatment of minority shareholders in going private transactions, the determination of joint actor status and the circumstances under which the OSC may exercise its public interest jurisdiction.

(i) Shareholder rights plans -- Falconbridge Limited

On June 27, 2006, the OSC held a hearing to determine whether to cease trade a shareholder rights plan or poison pill implemented by Falconbridge Limited (Falconbridge) so as to permit Xstrata plc (Xstrata), which had made an unsolicited insider bid for Falconbridge, to acquire shares tendered under its bid.

The purpose of the rights plan was to protect a friendly transaction negotiated by Falconbridge with Inco Limited (Inco) prior to the launch by Xstrata, on May 18, 2006, of its hostile bid for Falconbridge. At the time Xstrata launched its bid, it owned almost 20% of the Falconbridge shares.

The main issue at the hearing was whether cease trading the Falconbridge rights plan would prematurely end the auction for Falconbridge by allowing Xstrata to block the Inco offer by acquiring as little as 5% of Falconbridge's shares, whether through exempt market purchases or taking up Falconbridge shares tendered under its bid.

In an order dated June 30, 2006, the OSC held that the rights plan would remain effective until the earlier of July 28, 2006 or Xstrata obtaining a majority of the shares tendered by independent Falconbridge shareholders. This decision effectively sustained the auction for another month.

The OSC issued its reasons on August 17, 2006. The OSC stressed that the decision to allow the rights plan to stay in place for an additional month was based on the credible risk that allowing Xstrata to acquire Falconbridge shares would end the auction prematurely. The OSC's reasons set out a general framework for analyzing shareholder rights plans and discuss the application of this analysis to these unique circumstances.

The OSC's reasons also provide guidance on the circumstances under which it may be prepared to exercise its public interest jurisdiction to deny a bidder the use of a statutory exemption that permits it to make acquisitions outside of a formal bid.

(ii) Taking out the minority -- Sears Canada Inc.

The OSC held hearings relating to two applications that were received in connection with an unsolicited insider bid by Sears Holdings Corporation (Sears Holdings) for all the shares of Sears Canada Inc. (Sears Canada).

The first application was filed by dissident shareholders of Sears Canada. It alleged a number of irregularities in the conduct of the bid by Sears Holdings. The application raised the following significant issues:

- whether Sears Holdings had provided two bank shareholders with collateral benefits by modifying its bid to accommodate their tax planning objectives in exchange for their support of the second step business combination

- whether Sears Holdings had provided another shareholder with a collateral benefit by agreeing to release the shareholder from any litigation claims

- whether Sears Holdings was acting jointly or in concert with its financial adviser and an affiliate of the financial adviser such that Sears Canada shares held by the financial adviser and its affiliate should be excluded from approval of the second step business combination, and

- whether the Sears Holdings bid was otherwise conducted in an abusive fashion.

The second application that the OSC considered dealt with the conduct of the dissident shareholders. Sears Holdings alleged that the dissident shareholders had violated securities law requirements or otherwise acted contrary to the public interest by failing to report their collective ownership of Sears Canada shares at a time when they were joint actors and by acting in concert to manipulate the share price of Sears Canada.

The OSC issued its decision and reasons in respect of the two applications on August 8, 2006. With respect to the first application, the panel found that Sears Holdings had conferred prohibited collateral benefits upon the banks and the shareholder that had received the litigation release. However, the OSC concluded that there was no evidence that the financial adviser to Sears Holdings and its affiliate had acted jointly or in concert with Sears Holdings in connection with the bid.

The OSC was troubled by Sears Holdings' approach to disclosure about its bid and emphasized that disclosure obligations should focus on whether information was material to a tendering decision and not just technical compliance with the law. Finally, the OSC panel held that certain elements of Sears Holdings' conduct were coercive and abusive to the minority shareholders of Sears Canada and the capital markets generally.

The OSC issued an order cease-trading the bid, subject to conditions. The order effectively excluded the shares held by the three supporting shareholders from the minority approval required for the second step business combination under OSC Rule 61-501 Insider Bids, Issuer Bids, Business Combination and Related Party Transactions (OSC Rule 61-501).

The OSC dismissed the second application by Sears Holdings regarding the conduct of the dissident minority shareholders. However, the OSC noted that in appropriate circumstances, the use of swaps to avoid disclosure obligations by parking securities would constitute abusive conduct justifying the use of its public interest jurisdiction.

The Ontario Divisional Court dismissed an appeal from the OSC decision on October 11, 2006.

(iii) Joint actors in business combinations -- Sterling Centrecorp Inc.

This hearing involved a management-led acquisition of Sterling Centrecorp Inc. (Sterling). The application to the OSC was made under sections 104 and 127 of the Act. The application dealt with the issue of whether, under the circumstances, the shares held by certain shareholders of Sterling had to be excluded from the minority approval required under OSC Rule 61-501 on the basis that they were joint actors with the insider group of officers and directors of Sterling (that intended to take the issuer private).

The insiders collectively owned approximately 35.3% of the issued and outstanding Sterling shares. They entered into support agreements with 15 security holders of Sterling (Supporting Shareholders) who controlled, in the aggregate, approximately 37.8% of the securities of Sterling. As a result, the transaction was effectively guaranteed to receive the necessary minority approval required under OSC Rule 61-501. However, the filers, who were shareholders of Sterling that had made an unsolicited take-over bid for all of the securities of Sterling, alleged that the Supporting Shareholders were joint actors with the insiders and that their votes should be excluded from the minority for the purposes of approval of the transaction by a majority of the minority.

The going private transaction was approved at Sterling's annual and special meeting of shareholders on April 30, 2007. The hearing proceeded on May 17, 2007.

Following the hearing, the OSC issued an order stating its finding that none of the Supporting Shareholders, other than David Kosoy (who had initially been a part of the insider group seeking to acquire Sterling) and a company controlled by Mr. Kosoy, were joint actors under OSC Rule 61-501. Accordingly, the OSC ordered pursuant to sections 104 and 127 of the Act, that Sterling had to correct the record of the votes cast at the shareholders meeting to exclude from the calculation all of the votes attached to the common shares and other securities of Sterling held by Mr. Kosoy and his company. The application was otherwise dismissed.

The OSC issued its reasons on May 17, 2007. The OSC's reasons discuss the interpretation of joint actors under OSC Rule 61-501 and the circumstances under which parties to a support agreement could be considered to be joint actors with an acquirer.

6. Insider reporting

The Branch's insider reporting group is responsible for administering insider reporting requirements under the Act. Our objective is to facilitate transparent, timely and complete insider reporting.

A. Common issues on SEDI

(i) General

Many insiders and their agents file insider reports on SEDI that do not correctly report their transactions in the manner required by Form 55-102F2 Insider Report and other applicable securities law. For example, an insider may report the exercise of an option without also reporting the acquisition of the underlying common shares received on exercise of the option and the subsequent sale of those shares.

Other frequently occurring errors include:

• insiders placing a successful order to buy or sell securities with a broker, but not reporting the trade until they receive a confirmation slip or account statement from the broker after the 10-day reporting period

• insiders buying securities in a private placement, but not reporting the purchase until they receive certificates representing the securities from the issuer or its transfer agent after the 10-day reporting period, or

• insiders failing to report securities over which they have or share control or direction (e.g. securities owned by a corporation controlled by the insider or securities held by a trust of which the insider is a trustee).

For additional guidance, see CSA Staff Notice 55-308 Questions on Insider Reporting and previous Branch reports.

(ii) Insider profiles

We have noted a number of frequently occurring errors related to insider and issuer profiles on SEDI and remind them of the following:

• Individuals must use their residential address. Insiders who are individuals may not use the issuer's address in their insider profile. They must use their residential address because the insider reporting obligation is imposed on the insider, not the issuer. Using the issuer's address also makes it difficult for us to contact insiders who have left the issuer. See item 4.2.4 of CSA Staff Notice 55-310 Questions and Answers on the System for Electronic Disclosure by Insiders (SEDI) (CSA Staff Notice 55-310) and the requirements of Form 55-102F1 Insider Profile (Form 55-102F1).

• Use correct category of holdings. Whenever an insider creates an insider profile, SEDI will prompt the insider to indicate how it holds the securities. For example, the insider can hold the securities directly or indirectly, or it can have control or direction over the securities. For guidance, see section 4.2.9 of CSA Staff Notice 55-310.

• When to file an amended issuer profile supplement. Issuers must file an amended issuer profile supplement on SEDI immediately after:

• a new class of security is issued

• there is a change in the designation of any security

• any security has ceased to be outstanding and is not subject to issuance at a future date, or

• there is any other change in the information disclosed in the issuer profile supplement.

B. Late fees and late fee waivers

Insiders have a legal obligation to file an insider report within 10 days of any change in their holdings (unless an exemption is available). We remind insiders that OSC Rule 13-502 Fees (OSC Rule 13-502) imposes a fee for the late filing of an insider report. The fee is $50 per day, per insider, per issuer, to a maximum of $1,000.

The purpose of the fee is to encourage timely reporting by insiders. We do not view the late filing fee as a penalty or sanction imposed by a regulatory authority. Consequently, these fees do not trigger disclosure requirements under item 10.2 of Form 51-102F2, item 7.2.1 of Form 51-102F5 Information Circular, or under the prospectus rules.

(i) When the late fee does not apply

The OSC does not charge late fees if the issuer's head office is located in British Columbia, Manitoba or Quebec because each of these jurisdictions charges late fees to insiders of those issuers.

(ii) Requesting a fee waiver

Insiders who file an application under OSC Rule 13-502 for a waiver of the late filing fee should note the following:

- The application must include the insider's name, the issuer's name, the SEDI invoice number and detailed reasons why the late fee should be waived.

- Late fee waivers may be granted for filing errors such as a typographical error in the transaction date

- In general, we will not waive late fees for insider reports if:

- the insider or its agent misunderstand the 10-day reporting requirement (e.g., reporting within 10 business days rather than 10 calendar days as required)

- delays are caused by vacations or business trips

- the insider and its agent or broker miscommunicate (e.g., broker fails to provide the insider with the details of a trade)

- the late filing results from an administrative error by the insider or its filing agent, or

- the insider is unfamiliar with its legal obligations.

Please refer any questions you may have about insider reporting to:

7. Service standards and procedural matters

We are committed to delivering dependable, prompt and high quality services.

A. How we performed this year

When an issuer files an offering document with us and we are the principal regulator, we aim to complete our review within 30 working days. During the 2007 fiscal year, we met this standard 92% of the time. This is unchanged from the previous year.

When an issuer files an application for exemptive relief with us and we are the principal regulator, we aim to complete our review within 40 working days. During the 2007 fiscal year, we met this standard for 85% of the applications completed. This is a 5% increase from the previous year when we met this standard for 80% of the applications completed.

In the majority of cases where we did not meet our service standard, we failed to do so because:

- we did not receive a timely response from the filer

- the application was for a novel or complex issue, or

- the filer gave us incomplete or inaccurate information.

B. How you can help us improve our service

You can help us improve our service by:

- giving us complete and accurate information

- responding to our requests in a timely manner

- understanding and complying with our deadlines

- appreciating that complex or unusual matters require more time

- recognizing that we cannot provide legal advice, and

- understanding you may not always get the result you want.

(i) Prospectus filings

We continue to see certain deficiencies that can cause unnecessary delays in issuing a receipt on a preliminary prospectus or prospectus and often result in additional communication among us, issuers and/or their advisors.

Accordingly, we remind issuers and their advisors to ensure the following:

- red herrings on a preliminary prospectus comply with legal requirements

- details of prior discussions with us are set out in the cover letter

- all documents incorporated by reference are filed with each jurisdiction on the date the short form preliminary prospectus is filed

- activity fees and participation fees are paid as required

- prospectus certificates on preliminary and final prospectuses comply with applicable requirements

- the qualification certificates and the auditor's comfort and consent letters refer to the correct name and date of the preliminary or final prospectuses

- fees are attached to the correct filing and fee category, and

- blacklined documents are filed as correspondence and not as amendments on SEDAR.

(ii) What to include in applications for exemptive relief

Each year, we receive and review applications for exemptive relief that contain deficiencies. These deficiencies often delay the processing of the application and may consequently delay the granting of the requested relief.

In particular, filers and their advisors are reminded of the following:

- Clearly set out the relief sought in the application. The application should clearly set out the relief sought, why the relief is needed (e.g., if there is a provision the filer would like to rely on but cannot, explain why the filer cannot rely on the it), the filer's submissions regarding the policy reasons for granting the relief and how the key facts support granting the relief.

- Include the reasons for confidentiality during review period. Requests for confidentiality during the review process should set out reasons for the request.