OSC Staff Notice: 51-719 - Emerging Markets Issuer Review

OSC Staff Notice: 51-719 - Emerging Markets Issuer Review

OSC Staff Notice 51-719

Emerging Markets Issuer Review

March 20, 2012

PURPOSE OF THE EMERGING MARKET REVIEW

Introduction

On July 5, 2011, the OSC announced the commencement of a regulatory review (EMIR Review or the Review) of emerging market issuers (EM issuers) that would examine a targeted selection of Ontario reporting issuers that were listed on Canadian exchanges and had significant business operations in emerging market jurisdictions.

We conducted the Review in the face of notable concerns that began to surface involving some EM issuers that were listed for trading and raising capital in our markets. We also did this work in recognition of our increasingly globalized marketplace and the corresponding importance of remaining focused on investor protection and the integrity of our markets.

Given the importance of EM issuers in both the global and Canadian marketplace, we wanted to ensure that any systemic or specific issues that affect these issuers were identified and addressed. This is important to investors and for the integrity of the Canadian capital markets.

Several securities regulators in other jurisdictions had also been taking action in similar areas due to some concerns relating to information about title to assets and operations of issuers headquartered in foreign jurisdictions, as well as access to that information. In addition, the body responsible for the oversight of auditors in the U.S., the Public Company Accounting Oversight Board (PCAOB), focused on the fraud risks that auditors might encounter in audits of companies with operations in emerging market jurisdictions and published in October, 2011, a Staff Audit Practice Alert on auditors' responsibilities for addressing those risks, and certain other auditor responsibilities under PCAOB auditing standards. In Canada, the Canadian Public Accountability Board (CPAB) issued a special report in February, 2012, outlining its significant findings and recommendations following its review of audit files for Canadian public companies with their primary operations in China.

The purpose of the Review was to assess the quality and adequacy of selected EM issuers' disclosure and corporate governance practices, as well as the adequacy of the gatekeeper roles played by auditors, underwriters and the exchanges, to identify any broad policy issues and entity-specific concerns. In addition, the Review also examined the legal vehicles through which EM issuers have accessed the Ontario market. In undertaking the Review, staff contacted issuers and their advisors, and organizations such as Canadian exchanges, CPAB and other provincial securities regulators.

We understand the importance of Ontario's markets being attractive globally to quality issuers seeking capital investment. We want Ontario investors to have access to a wide variety of investment opportunities but also want to ensure that this access is balanced with the right level of investor protection. The Review was undertaken to determine if there are areas in the regulation of EM issuers that we can improve or strengthen, including the oversight of the performance of different entities that play a role in bringing these issuers to our market.

A snapshot of EM issuers in Canada

While the term 'emerging market' has different meanings in different contexts, for the purposes of conducting the Review, staff considered a number of criteria in determining whether a reporting issuer was an EM issuer. Staff focused on issuers with the following characteristics:

• whose mind and management are largely outside of Canada and

• whose principal active operations are outside of Canada, in regions such as Asia, Africa, South America and Eastern Europe

TMX Group issuers listed on the TSX and TSXV and CNSX issuers listed on the CNSX as at April 30, 2011, and having headquarters in jurisdictions other than Canada, the US, the UK, Western Europe, Australia and New Zealand, totalled 108.

At April 30, 2011, these 108 issuers had a total market capitalization of approximately $40 billion. This was in contrast to a total of nearly 4,000 exchange-listed reporting issuers in Canada, having a total market capitalization of $2.39 trillion.

- - - - - - - - - - - - - - - - - - - -

EM Issuers -- Canada

All data as at April 2011, as supplied by TMX Group and CNSX

# Issuers

Market Cap. (CAD $ mill)

TSX

50

$37,108

TSXV

55

$3,228

CNSX

3

$33

Total

108

$40,369

- - - - - - - - - - - - - - - - - - - -

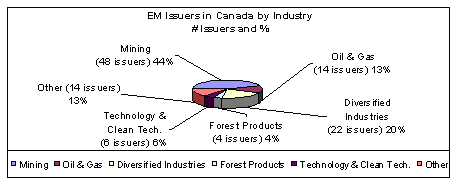

EM issuers were present and operated in a variety of industries, primarily mining, as indicated in the chart below.

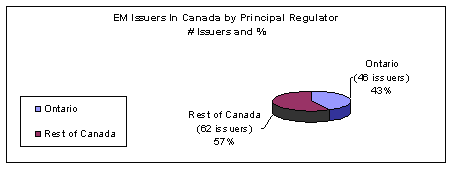

Of the 108 EM issuers in Canada, approximately 43% had the OSC as their principal regulator.

The number of EM issuers in Ontario is relatively small compared to the total number of reporting issuers in Ontario. However, staff wished to assess if investors in EM issuers could be exposed to any inappropriate risks or associated risks that were not fully understood. While we appreciate the importance of EM issuers to our markets, we thought it was important to determine if any issues existed that could impact the reputation and integrity of Ontario's market, either at home or abroad.

Who we looked at

Staff selected and reviewed 24 issuers, which represented more than 50% of the EM issuers for which Ontario is the principal regulator. All had operations in emerging market jurisdictions and were listed on Canadian exchanges. The issuers ranged across a number of industries, including mining, forestry, financial services, technology and clean energy, and diversified industries and operated in a variety of countries.

Integrity of public disclosure is the bedrock of investor protection

The integrity of public disclosure by reporting issuers, including financial reporting, is core to investor information and protection. This disclosure depends critically on each of the following performing their duties responsibly:

• the Chief Executive Officer (CEO)

• the Chief Financial Officer (CFO)

• the board of directors (board)

• the audit committee of the board

• the external auditor

• the underwriter

• the exchange

Integrity of public disclosure starts with management. The CEO and CFO are the key individuals that investors rely on to provide accurate and comprehensive information on an issuer's performance and prospects through the issuer's disclosure. The CEO and CFO must ensure the issuer's disclosure is accurate and complete and certify the disclosure and the internal controls over financial reporting.

Effective oversight of management by the board is a critical component of the investor protection framework. The board has a duty to act honestly and in good faith in the best interests of the issuer and must supervise the issuer's management. It plays a pivotal role in effective governance and is responsible for overseeing the general business direction of the issuer.

The board appoints the audit committee whose primary responsibility is to oversee the financial reporting process and manage the issuer's relationship with its external auditors. The external auditor has a unique role in the reporting process for annual financial statements which are relied upon by the board, audit committee and, most importantly, investors to provide an independent assessment of whether the information presented in the issuer's annual financial statements has been fairly presented.

Underwriters are uniquely situated to verify information about an issuer, its operations and management and act as gatekeepers to our markets. In prospectus offerings, underwriters certify that they have undertaken due diligence and that to the best of their knowledge, information and belief the issuer's prospectus constitutes full, true and plain disclosure of all material facts relating to the offered securities. As part of the EMIR Review, staff reviewed the underwriters' activities as they are essential contributors to the oversight of the integrity of public disclosure.

Staff also acknowledge the important role played by other professionals such as lawyers, experts and consultants in bringing issuers to market and confirming the completeness and accuracy of issuers' ongoing public disclosure. Although they were not the focus of the Review, staff also encourage these professionals to be cognizant of the role they play in the disclosure process, and of the importance of due diligence, professional scrutiny and full disclosure of the risks in their work on emerging market related matters.

What we did

The Review involved a broad examination of the public disclosure record of each selected EM issuer and an examination of the issuer's board and audit committee activities. In addition, staff examined the detailed files of auditors of the EM issuers because of the integral role they play in enhancing the degree of confidence that the investing public place on the information presented in an EM issuer's annual financial statements. The auditor's report is a critical third party communication that investors rely on to ensure that the issuer's annual financial information has been sufficiently examined and verified. Staff also reviewed the due diligence activities undertaken by issuers' underwriters, focusing on the depth of the due diligence they performed when underwriting a public offering of securities.

The exchanges undertake a fundamentally important role in promoting market integrity and fostering investor confidence in our markets. The exchanges have detailed and prescriptive listing requirements that require the filing of audited financial statements and, in many cases, sponsorship by an exchange participating organization. We examined whether the core processes of the exchanges are sufficiently robust to address the unique concerns raised by EM issuers and if the review processes would benefit from additional due diligence in the emerging market context.

Purpose of this Report

The purpose of this Report is to identify areas of concern arising from the Review. At this time our observations are preliminary and identify the key policy areas that we believe merit further examination.

The ultimate goals of the EMIR Review and Report are to identify areas of concern and recommend changes that will contribute to the protection of investors and strengthen the integrity of our markets.

Much of the information staff reviewed is protected by confidentiality provisions in the Securities Act (Ontario) and therefore cannot be publicly disclosed. As a result, this Report is general in its discussion, rather than citing specific instances or examples.

Where the Review resulted in significant staff concerns about an issuer's, auditor's or underwriter's apparent regulatory non-compliance, files were referred to the Enforcement Branch of the OSC for further assessment and, if warranted, the initiation of enforcement proceedings.

GENERAL CONCERNS

In this section of the Report, we identify four principal concerns arising from our EMIR Review including:

• the level of EM issuer governance and disclosure

• the adequacy of the audit function for an EM issuer's annual financial statements

• the adequacy of the due diligence process conducted by underwriters in offerings of securities by EM issuers

• the nature of the exchange listing approval process

For each of these four areas of concern, we have identified the main focus for additional examination and analysis. We anticipate that these concerns can be addressed by a combination of action by issuers, auditors, underwriters, exchanges, securities regulators, other oversight bodies and gatekeepers working together to strengthen our markets and protect investors.

Overall concerns

As noted, the regulatory framework for issuers involves a system of reliance and connection between different groups -- the issuers themselves, their boards and audit committees, auditors, underwriters and exchanges. We found examples of practices in all of these areas that concerned us and we believe further work is warranted to improve compliance by all of these important groups of market participants with their regulatory obligations.

One of our central concerns was the apparent 'form over substance' approach to compliance with applicable standards for disclosure, issuer governance, board oversight, audit practices and due diligence practices. In our view, the level of rigor and independent-mindedness applied by boards, auditors and underwriters in doing their important jobs -- management oversight, audit, due diligence on offerings -- should have been more thorough.

The fact that the core operations and assets of many of the issuers were located in an emerging market jurisdiction, with very little presence in Canada in most cases, contributed to a separation between the issuer's Canadian governance and local management functions. It also contributed to challenges for both the audit process and the performance of due diligence by underwriters.

The need for a good understanding of local business practices, how the business operates in the emerging market jurisdiction, and the degree of reliance that can be placed on local members of management, should generally have been given more prominence in management oversight, audits and due diligence functions. Language barriers and translation issues also appeared to be important factors in how well those functions were performed.

EM issuers

Staff conducted in-depth reviews of the public disclosure record of the selected EM issuers and examined information concerning the function of each selected EM issuer's board and audit committee. Our principal concerns are set out below.

EM issuers, their management and boards are expected to discharge all of their responsibilities in a way that promotes the protection of Ontario investors and confidence in our markets. They are expected to do this on a basis that is fully informed by both the business and cultural practices of all of the jurisdictions in which the EM issuer operates.

Corporate governance practices

An issuer's board and audit committee must have a thorough understanding of the business and the operating environment of the issuer as this understanding is the foundation upon which the executives will execute all of their responsibilities. For Canadian reporting issuers whose businesses are based in Canada, the Canadian directors serving on their boards are expected to have a thorough understanding of the Canadian marketplace and its legal, business and political environment.

We recognize that board members of EM issuers may face a steeper learning curve to understand these same aspects of the EM issuer's business and operating environment. The time zone, language, location of key books and records and cultural differences may make communication especially complicated in these situations. Nevertheless, all board members of Canadian reporting issuers, regardless of where they are located and where the business operations are located, are required to adhere to Canadian regulatory requirements.

It appeared to us that the level of engagement by boards and audit committees in their oversight of management and sense of responsibility for the stewardship of an EM issuer with public investors was in certain cases deficient. For example, in some cases it appeared that the board had very little contact with senior management in the emerging market jurisdiction running the business.

We were concerned with the extent of knowledge of boards and audit committees of the cultural and business practices of the jurisdictions in which the issuer operated. In some situations, it appeared that the board was not aware of environmental factors that could have a significant impact on the issuer, such as banking practices, currency restrictions and the regulatory and legal environment specific to the industry in which the issuer operated. To the extent there was knowledge of relevant cultural and business practices, the manner of board oversight was not, in some situations, appropriately adjusted to reflect those practices. For instance, we observed situations in which it appeared that board members relied solely on a member of management to provide an overview of key business documents in a foreign language and did not obtain appropriate translations in order to read and assess the documents themselves.

Corporate structures

An issuer's structure should be designed to facilitate the conduct of its business. Emerging market jurisdictions may present additional challenges to issuers as they must navigate the political, legal and cultural realities of those markets and design an appropriate corporate structure. In some cases, the legal or regulatory system may present impediments to foreign ownership or control and may result in the need for specific structures to enable the issuer to do business in that market.

Complex structures may increase the risk profile of an issuer. These structures may be difficult to adequately describe to investors in disclosure, and they may impact the ability of the board to properly oversee management or understand the full extent of the issuer's operations. In particular, boards should consider the potential for complex structures to facilitate inappropriate activity, such as fraud or misappropriation of assets, or misrepresentations about an issuer's financial performance or condition.

In the Review, we observed structures that caused us to question their appropriateness and transparency, such as the presence of multiple legal entities supporting a single operating business. We were concerned that the complexity of certain corporate structures did not appear to be clear or necessary to support the EM issuer's underlying business model. The quality of controls in place to manage the risks arising from the complexity of the structure was also a concern in these cases.

Related party transactions

Related party transactions (RPTs) warrant careful scrutiny by investors so that they may evaluate the fairness of the transactions and the impact they may have on an issuer's operations and financial results. Although not unique to EM issuers, transactions with other issuers in the same group of issuers, or with parties linked to an issuer's shareholders, directors or management may represent a heightened risk for issuers conducting business in these markets. Some of this may be due to differences between local business practices and cultural norms and the legal requirements in North America. Nevertheless, they need to be understood and disclosed accurately.

While RPTs may provide the issuer with benefits that are not available from other arms-length parties or to other issuers on the same terms, they can also be abusive if they only benefit the related party and not the issuer. We are concerned about transactions of this nature as they can be detrimental to investors in the issuer and can undermine the integrity of our capital markets.

Boards and audit committees are expected to approach their oversight role with an appropriate degree of independent-mindedness. In the case of the RPTs involving some EM issuers we reviewed, we observed that this could have been done better. In these cases, we were particularly concerned with the extent and frequency of RPTs and the quality of the management and board processes in place to identify and approve RPTs. Our disclosure reviews also revealed deficiencies in the completeness and appropriate clarity of related party disclosures.

Risk management and internal controls

The board's responsibility for the stewardship of an issuer includes the identification of principal risks to the issuer's business and oversight of the implementation of appropriate systems to manage those risks. The board oversees management, which is responsible for identifying and quantifying an issuer's exposure to risks and for adopting suitable risk management systems to address those risks.

Boards of EM issuers should be particularly sensitive to the unique risks associated with operations in emerging market jurisdictions, especially those that could result in a serious disruption to business operations. Board members should ensure that they have a sufficient understanding of the political and cultural risks impacting the EM issuer and assess those risks in the context of the emerging market jurisdiction, and not only from a North American viewpoint. Risk analysis and mitigation techniques that may seem appropriate in a Canadian or North American business context may not be effective in emerging market jurisdictions. It is important that boards obtain a clear understanding of how the risks of operating in emerging market jurisdictions could impact the corporate structure, operations and material assets of the issuer.

Internal controls are an important way to manage risk. Boards should review and be satisfied that management has put in place appropriate internal controls to manage the risks facing the issuer. For example, effective internal controls help reduce the risks of inaccurate financial reporting. A breakdown of the integrity of financial reporting often stems from a lack of, or a circumvention of, internal controls. It is therefore important for board members to oversee the design and implementation of internal controls and to assess the appropriateness of the remediation of significant deficiencies and material weaknesses. Board members should also be aware of the risks if there is a material weakness in the issuer's internal controls.

Staff concerns with some EM issuers' internal controls related to the risks of doing business in emerging market jurisdictions, and linked to this, the quality and extent of work performed by the CEO and CFO to support their certification of annual and interim filings. We would have expected to see the internal controls adjusted to reflect the particular risks of having significant business operations located in an emerging market, including those associated with political, legal and cultural factors, as well as the location of books and records and language barriers. However, in certain cases, this was not what we observed.

For EM issuers, internal controls may be particularly important to assist in mitigating such risks. For example, it is particularly challenging for a board whose members principally reside in Canada to govern an issuer whose operations are located in a foreign jurisdiction. This challenge may further be magnified in circumstances where the CEO, being the principal decision-maker, resides in the emerging market, and the CFO resides in Canada.

In the Review, we noted risks that may not have been appropriately identified, understood or managed by the board including risks related to:

• political factors, such as government instability and changing governmental policy that may affect legal rights, such as property ownership

• the legal and regulatory framework, given that emerging market jurisdictions may have less developed legal or regulatory systems

• the movement and conversion of currency out of the foreign jurisdiction, which could hinder the repatriation of profits to Canadian investors

• legal title to assets

We also found that risk disclosures by the issuers were not as specific or relevant as they should have been to be helpful and informative to investors.

Auditors

In the course of the Review, we identified several areas of potential concern with respect to the way in which the external audit function was performed for EM issuers. We were concerned that auditors may not have performed sufficient procedures in some instances to understand and appropriately scrutinize the information provided to them by an issuer and/or foreign 'component' auditor. On February 21, 2012, CPAB issued a special report "Auditing in Foreign Jurisdictions" outlining its significant findings and recommendations following its review of audit files for Canadian public companies with their primary operations in China. The observations noted in CPAB's report are largely consistent with our principal concerns, as set out below.

Level of professional scepticism

The level of professional scepticism exhibited by auditors when examining the information gathered in the course of their audit was generally lacking. We were concerned that in some instances the auditor accepted management's representations at face value and did not perform sufficient alternative procedures to independently verify the information they received. There were also instances where, in our view, auditors should have been uncomfortable based on the work performed and information received -- for example if responses received were unusual or unexpected, we would have expected an auditor to further challenge or examine the response to ensure they understood the situation.

In addition, we saw conclusions for areas of judgement that were not supported by an underlying analysis, for example, broad-based conclusions (i.e., a conclusion that no issues were noted) with no underlying analysis regarding the procedures or evidence obtained to support the general statement. This disconnect raised issues on what work, if any, was done to substantiate the auditor's conclusion or ensure that risks were sufficiently mitigated.

Degree of knowledge auditors had of the local cultural and business practices

It was unclear in some instances what was done to understand an issuer's business environment. For example, if checklists were prepared it was questionable that responses resulted in sufficient understanding of the cultural and business practices of the jurisdictions in which the issuer operated. Some auditors appeared to have an insufficient understanding of the legal environment (i.e. use of corporate seals) and/or procedures to obtain licenses and/or permits in the emerging market. In some cases auditors appeared to accept certain information provided by management at face value without performing any procedures to support those representations with independent external information.

Extent of delegation to a foreign 'component' auditor

Applicable auditing standards have no defined parameters for the extent of work that can be delegated to a component auditor, and we were concerned that this resulted in group auditors' insufficient involvement with the audit of underlying operations in some circumstances. This was particularly true in situations where an issuer's underlying operations were entirely in the emerging market and the foreign component auditor performed all audit procedures in the emerging market.

A key concern noted was that some component working paper files could not be removed from a foreign jurisdiction. This could prevent regulators (i.e., the Commission or CPAB) from reviewing files or group auditors from including key working papers from a component auditor in their files. It was also unclear to us the extent of review that group auditors were choosing to, or were able to, perform on audit files of component auditors or whether group auditors were visiting the foreign jurisdiction.

It appeared in some instances that group auditors asked component auditors to do the work to understand the business and environment but did not receive sufficient communication back to understand what the component auditor learned or understood. In fact, we do not believe there was enough communication in general between group and component auditors, particularly communication from the component auditor to the group auditor. We would expect to see more group auditor executives visiting foreign operations or interacting with members of issuers' management.

Inability to access audit working papers

We experienced difficulty in obtaining domestic auditor working papers voluntarily, so other means were generally needed to obtain audit working papers. When an auditor resided in a foreign jurisdiction, or a portion of the audit work was done by a component auditor, we were unable to obtain those working papers.

Language barriers

We observed that language barriers impacted an auditor's ability to communicate with management or examine documentation. We could not discern how audit executives addressed these language concerns in some audits or why this was not an issue for consideration in connection with the audit. For example, in some instances the communication between audit executives and key client executives appeared to be insufficient due to language differences. Perhaps more importantly, there also appeared to be insufficient translation of key documents despite audit engagement executives not being fluent in the local language. It was not clear from the Review how auditors addressed language barriers in client documents for audit executives who did not speak the local language.

Underwriters

Underwriters, as gatekeepers to our securities markets, are uniquely situated to verify information about an issuer, its operations and management. In prospectus offerings, underwriters must certify that to the best of their knowledge, information and belief, the prospectus constitutes full, true and plain disclosure of all material facts relating to the offered securities. In the listing process, the underwriters may act as sponsors. In this role, they conduct due diligence and may prepare reports on, among other things, the issuer's business and financial position, the issuer's directors and officers, and the issuer's qualifications for meeting all relevant listing criteria. The role of the sponsor in the listing process is a critical part of the listing review and approval.

Underwriters should participate in the offering process with a healthy amount of scepticism regarding management claims. Their due diligence must be designed to detect if there are material misstatements or omissions in prospectus disclosure. An underwriter must also develop a full understanding of an issuer's finances, management, operations, industry and country of origin, in order to be able to certify the prospectus. They should also document their findings in a clear and concise manner.

Staff reviewed the work of underwriters in the public offerings of securities by selected EM issuers. Our principal concerns are set out below.

Variations in due diligence practices

While there is some general guidance on due diligence practices for Canadian underwriters, there are no explicit, standard requirements for the conduct of due diligence by underwriters. As a result, it was evident during the Review that underwriters adopted a varied array of policies, procedures and practices. Some underwriters provided internal policies and due diligence checklists, while others had limited processes. Some of the reviews appeared to be thorough and some were not. We also noted that internal committee memoranda, due diligence committee meeting minutes and due diligence checklists were largely not provided to us. We observed in some cases that risks were not always documented, and if they were raised, there was little or no follow-up recorded or evident in the due diligence materials.

We reviewed transcripts of due diligence calls with issuers and observed a number of instances where several customers of a single issuer provided identical answers to questions posed by the underwriters. We think the similarity of these responses should have raised some degree of scepticism and further questioning by the underwriter, yet this did not occur. In addition, in some cases, questions posed during the course of due diligence calls were deflected, not answered or inadequately explained by the issuer's management and the questions were not pursued nor were satisfactory explanations provided. We also noted situations where site visits were attempted unsuccessfully and these were not rescheduled, nor were additional questions asked about the site's availability during the remainder of the due diligence process.

Level of professional scepticism and rigor

In the underwriter material we examined, we observed that the level of professional scepticism and rigor that appeared to be applied in the due diligence process was lacking. We noted several instances where 'red flags' (such as significant growth or a change in the issuer's business in the recent past, financial metrics that were superior to an industry average, unusual year-over-year growth results and a high degree of reliance on government relationships or the founder/CEO) should have prompted further probing or questions. Our review indicated little or no follow-up in these instances to either understand or analyze the concerns, or disclose them.

Approval process for offerings

We observed some cases where, due to a lack of documentation of due diligence meetings, site visits and bring-down calls (calls among the underwriter, issuer, auditors and legal counsel to reconfirm statements previously made during the due diligence investigation), it was not always evident that the approvals process called for by the underwriter's own internal process was followed.

Understanding of emerging market jurisdictions

The due diligence information and process we examined in connection with a number of EM issuer offerings contained little documentation or discussion of the risks associated with the issuer's operations. Even where the due diligence policies and procedures of a firm contemplated additional factors or steps that should be considered or taken in light of additional risks, it was evident from the documentation that these were not taken into account in performing the due diligence.

Due diligence documentation

In the Review, we noted that the amount and degree of due diligence documentation varied widely. In some circumstances, the documentation did not reflect the process by which due diligence was undertaken and completed nor the risks identified in connection with the offering (including those related to the issuer's industry group or market, if appropriate).

In terms of due diligence calls, while we found the lists of questions to be asked of the issuer were documented, in some cases the names of the participants on the calls were not provided and written transcripts were not provided.

Exchanges

The exchanges are important gatekeepers to our securities markets as they set standards for issuers seeking to list their securities on Canadian markets. The exchanges undertake a vigorous review process, including review and reliance on third party reports to determine if the issuer meets the listing requirements, which is a critical part of the access to public capital. As part of this process, when sponsorship is required, the sponsors conduct due diligence and prepare reports on the issuer's business and financial position, the issuer's directors and officers, and the issuer's qualifications for meeting all relevant listing criteria.

We examined the listing processes in place and the listing review that was undertaken for the EM issuers selected for this study. We considered whether the core processes of the exchanges are sufficiently robust to address the unique concerns raised by EM issuers that have come to light as a result of the EMIR Review and other recent events. We also considered whether the exchange review processes would benefit from additional due diligence in the emerging market context, particularly with respect to reliance on work performed by third parties and the quality of third parties' work.

We also examined the methods by which EM issuers selected for review accessed the Ontario market and raised capital from Ontario investors. An issuer can become a reporting issuer through different methods, including:

• an initial public offering (IPO), which involves the preparation of a prospectus to be filed with securities regulators and is often accompanied by an application for a public listing on an exchange

• a direct listing on a recognized Canadian exchange, which may be facilitated if the issuer is already listed on another exchange in a foreign jurisdiction

• a reverse take-over (RTO) (also known as a back door listing or reverse merger), which usually involves a transaction with an existing issuer that is already a reporting issuer. The form of transaction varies but typically involves an amalgamation or issuance of shares in exchange for other shares or assets.

The EM issuers in our review sample accessed our market through different methods, including IPOs, direct listings and RTOs. We did not identify any particular method of accessing the market and becoming a reporting issuer as being specifically problematic.

In conducting this work, we worked co-operatively with staff at the TSX and considered:

• how the issuers 'went public'

• the various parties involved in the listing of an EM issuer

• the inter-reliance of those parties and their interconnectivity with the exchange listing framework applicable to EM issuers

• the listing requirements and review processes of Canadian exchanges that generally apply to the types of reporting issuers selected for review

Our principal concerns are set out below.

Specific listing requirements for EM issuers

The exchanges have supplemental procedures and policies geared to EM issuers. However, a re-examination of the sufficiency of those procedures and policies may be warranted in light of our increased understanding of risks associated with emerging markets. There also does not appear to be a requirement for an EM issuer whose primary listing is in Canada to maintain a meaningful 'Canadian presence' (which could include having a combination of directors, key officers, employees, books and records and assets (such as cash) located in Canada).

Transparency when exchanges waive any listing requirements

In accordance with the exchanges' listing requirements, the exchanges have broad discretion in how they apply the listing requirements. The exchanges may, in their discretion, take into account any factors they consider relevant in assessing the merits of a listing application, resulting in the granting or denial of a listing application notwithstanding the published criteria. There does not generally appear to be any public disclosure that is made about waivers of listing requirements granted to specific issuers.

Strong reliance on third parties in conducting due diligence

The listing process involves the exchanges' review of various documents prepared for the issuer by outside experts, such as auditors, geologists or sponsors. In particular, the exchanges place significant reliance on the role of sponsors to conduct due diligence of prospective listings. Sponsors are expected to undertake a comprehensive review of the issuer being sponsored, including, potentially, site visits, reviewing all relevant documentation and evaluating past conduct of directors and officers, among other things. Notwithstanding the prescribed exchange requirements for a sponsorship report, the actual terms of a sponsorship report are generally negotiated between the sponsor and the issuer seeking a listing, and the sponsor is paid a fee for providing this service. In addition, there does not generally appear to be publicly available information regarding a particular sponsor's role in a new listing or the sponsor's due diligence report.

RECOMMENDATIONS AND NEXT STEPS

All issuers, including emerging market issuers, their management and boards are expected to discharge all of their responsibilities in a way that promotes the protection of Ontario investors and confidence in our markets. They are expected to do so on a basis that is fully informed by the business and cultural practices of all of the jurisdictions in which the EM issuer operates. Auditors, underwriters and all other advisors to issuers are also expected to discharge their responsibilities in a similar manner with a full appreciation of the reliance that Ontario investors place on them.

This Report raises particular issues associated with EM issuers coming to market. Emerging market issuers are an important growth market for Canadian investors and this Report identifies areas for improvement related to governance and the critical work of auditors, underwriters and other experts. We will continue to follow up with individual issuers and their advisors as appropriate, and will continue to refer matters to our Enforcement Branch as warranted. We will also continue to work with CPAB to address audit related concerns, with staff at the Canadian exchanges to address concerns related to the listing process and with the Investment Industry Regulatory Organization of Canada (IIROC) on the underwriter practices we observed in the Review.

The concerns we have identified in this Report are, to varying degrees, unfolding on a global basis. With that in mind, we will continue to engage in dialogue with other securities regulators within and outside of Canada to share perspectives and best practices to address areas of common concern.

Staff expect that EM issuers, their auditors, underwriters and their other advisors, as well as the exchanges, will address the concerns identified in this Report and will, where necessary, take immediate steps to improve their practices to effectively discharge their responsibilities to protect investors in Ontario.

What follows is a list of recommendations for further work needed to address the principal concerns in this Report. In most cases, these recommendations do not involve the creation of new policies or rules but instead involve the development of guidance, best practices or enhanced vigilance to support compliance with current requirements.

EM issuers

• establish guidance to improve corporate governance practices, particularly in the areas related to the responsibilities of the board and its committees to understand the business, operating environment and risks for issuers whose principal operations are in foreign jurisdictions

• clarify the regulatory expectations of CEOs and CFOs in conducting reasonable due diligence to support their certifications for companies whose principal operations are in foreign jurisdictions

• require better disclosure to investors of complex corporate structures and their purpose

• require better explanations of risk factors relevant to EM issuers

• raise investor awareness of risks associated with investments in issuers whose principal operations are in foreign jurisdictions

• ensure the maintenance of appropriate books and records in Canada

• consider a minimum language competency component for Canadian-resident board members in the applicable local language where the issuer's principal business operations are located

• consider minimum Canadian director residency requirements

Auditors

• facilitate access by the OSC to the audit working papers of Ontario reporting issuers

• determine what should be done to address situations where regulators are unable to access foreign audit files relating to reporting issuers

• work with CPAB to analyse whether securities rules can be enhanced to allow more information sharing in connection with the oversight of audit firms

• examine whether suitability standards for auditors of reporting issuers should be developed

• analyse whether auditors should be required to publicly disclose their resignation from a file, and to explain the reasons for that resignation

• develop greater cooperation among securities regulators and audit oversight bodies to monitor the quality of audits of public companies with operations in emerging markets

• continue to discuss the audit-related concerns in this Report with CPAB and audit firms

• bring these concerns to the attention of both the Canadian Audit and Assurance Standards Board and the International Auditing and Assurance Standards Board

Underwriters

• establish a consistent and transparent set of requirements for the conduct of due diligence by underwriters

• ensure these requirements include a process that addresses:

• the issuer's operational structure

• internal controls and risk management

• translation and foreign language issues

• business practices and business environment in which the issuer operates

• government relationships

• asset ownership

• CEO/founder shareholdings and RPTs

• cultural norms that affect the issuer's structure, operations, governance and the ability to do business

• review of key documents

• review of key members of management

• review of customers, suppliers and others parties relevant to the issuer's business

• reporting on results of site visits

• develop best practices around documentation of all aspects of an underwriter's due diligence

• develop best practices for due diligence calls and site visits

Exchanges

• assess whether additional listing requirements are needed for EM issuers to address specific risks associated with them, or if additional exchange review procedures are required to assess if significant risks are present and how those risks could be addressed

• provide greater transparency regarding waivers of any listing requirements

• assess whether the extent of reliance on third parties in conducting due diligence is appropriate in the listings process or whether additional due diligence steps are warranted

• review the role of sponsors (if applicable) in bringing EM issuers to market to ensure that there is adequate accountability placed on the sponsor and if there is an appropriate level of transparency regarding the sponsor's due diligence work

OSC staff will continue to work on the issues identified in this Report with other provincial securities regulators, CPAB, IIROC, the exchanges and other interested parties so that we can advance the work we have begun through the EMIR Review. We think it is also important to recognize that some of the policy issues we may pursue from the EMIR Review could have broader applications and a more general benefit to our markets.

We are focused on our markets remaining open and attractive to issuers from all jurisdictions. Fostering markets that are fair and efficient and that protect investors interests will continue to attract both domestic and foreign issuers.