CSA Staff Notice 81-334 - ESG-Related Investment Fund Disclosure

CSA Staff Notice 81-334 - ESG-Related Investment Fund Disclosure

A. Introduction

The purpose of this Canadian Securities Administrators (the CSA) Staff Notice (the Notice) is to provide guidance on the disclosure practices of investment funds as they relate to environmental, social and governance (ESG) considerations, particularly funds whose investment objectives reference ESG factors (ESG Funds) and other funds that use ESG strategies (ESG Strategy Funds, and together with ESG Funds, ESG-Related Funds). This Notice also provides guidance on the types of investment funds that may market themselves as being focused on ESG.

The guidance provided in this Notice is based on existing securities regulatory requirements and does not create any new legal requirements or modify existing ones. This Notice clarifies and explains how the current securities regulatory requirements apply to ESG-related investment fund disclosure. It also includes best practices that, while not required, staff of the CSA (staff or we) are of the view would enhance ESG-related disclosure and sales communications.{1} The Notice aims to bring greater clarity to ESG-related fund disclosure and sales communications to enable investors to make more informed investment decisions.

Interest in ESG investing has grown considerably in Canada for both retail and institutional investors, including in the investment fund industry. According to a 2020 report from the Global Sustainable Investment Alliance, compared to other regions such as the United States, Japan and Australasia, Canada experienced the largest increase in "sustainable investment" assets over the preceding two years, with 48% growth, and at the time of the report, Canada was the market with the highest proportion of sustainable investment assets at 62%.{2} Similarly, according to a report from the Responsible Investment Association, as of November 2020, retail "responsible investing" mutual fund assets had increased from $11.1 billion to $15.1 billion, an increase of 36% over two years.{3} In 2021, the value of "sustainable funds" in Canada was $18 billion at the end of the first quarter, representing a 160% increase from 2020, and there were 156 sustainable funds at the end of March 2021 as compared to 105 at the same time the prior year.{4}

As the investment fund industry has responded to investor demand by creating new ESG-Related Funds and incorporating ESG considerations into existing funds, there has been an increased potential for "greenwashing", whereby a fund's disclosure or marketing intentionally or inadvertently misleads investors about the ESG-related aspects of the fund. In addition to leading investors to invest in funds that do not meet their objectives or needs, greenwashing may also have the effect of causing investor confusion and negatively impacting investor confidence in ESG investing, including ESG-Related Funds.

The growth of interest in ESG investing and the increased potential for greenwashing have led securities regulators and international organizations to address issues related to ESG investing, including ESG-Related Funds. In particular, the International Organization of Securities Commissions (IOSCO) has recently published a final report setting out recommendations for securities regulators and policymakers to improve sustainability-related practices, policies, procedures and disclosure in the asset management industry (the IOSCO Report).{5}

Considering these global developments and the increased potential for greenwashing, staff are providing guidance in this Notice on ESG-related disclosure practices by investment funds, particularly in relation to ESG-Related Funds. We encourage investment funds, investment fund managers (IFMs) and portfolio advisers to review this Notice.

B. Purpose

This Notice

• provides an overview of common ESG-related terms and strategies,

• briefly summarizes key international and domestic developments in this area, including the recommendations from the IOSCO Report relating to investment product-level disclosure, and

• provides relevant and practical guidance for investment funds, particularly ESG-Related Funds, and their IFMs to enhance the ESG-related aspects of the funds' regulatory disclosure documents and ensure that the sales communications of such funds are not untrue or misleading and are consistent with the funds' regulatory offering documents.

Any examples provided in this Notice are for illustrative purposes only and are not meant to be exhaustive of all potential scenarios or approaches.

C. ESG-Related Terms and Strategies

While this Notice uses the term "ESG", there are other related terms that are commonly used by ESG-Related Funds and more broadly throughout the investment fund industry. Those terms include the following:

• sustainable

• responsible investing or RI

• socially responsible investing or SRI

• ethical

• green

ESG-Related Funds, whether they are ESG Funds or ESG Strategy Funds, generally consider ESG factors in their investment decision-making processes, although ESG-Related Funds may focus on only one or two of the three areas of ESG. ESG-Related Funds may even only focus on one or a small group of factors in one of the areas of ESG, such as a fund that is focused only on board diversity. For illustrative purposes, the following is a non-exhaustive list of ESG factors that may be considered by such funds in their investment decision-making processes:

Environmental

Social

Governance

Air and water pollution

Community relations

Audit committee structure

Biodiversity

Data protection and privacy

Board diversity

Climate change and carbon emissions

Diversity

Bribery and corruption

Deforestation

Employee engagement

Executive compensation

Energy efficiency

Human rights

Lobbying

Waste management

Indigenous inclusion and reconciliation{6}

Political contributions

Water scarcity

Labour standards

Whistleblower schemes

{6} Some stakeholders are of the view that, given the importance of Indigenous inclusion and reconciliation in Canada, the concept of "ESG" should be expanded to "ESGI", with Indigenous inclusion and reconciliation being included as a separate area.

ESG-Related Funds incorporate ESG factors into their investment decision-making processes using one or more ESG strategies. While many ESG strategies are widely used across the industry, there is currently a lack of consistency in ESG-related terminology and definitions used to describe these ESG strategies throughout the industry.

The following are some of the most common ESG strategies:

Negative screening (sometimes referred to as exclusionary screening or ESG exclusions)

The fund excludes certain types of securities or companies from its portfolio based on certain ESG-related activities, business practices, or business segments.

ESG integration

The fund explicitly considers ESG-related factors that are material to the risk and return of the investment, alongside traditional financial factors, when making investment decisions.

Best-in-class (sometimes referred to as positive screening or inclusionary screening)

The fund aims to invest in companies that perform better than their peers on one or more performance metrics related to ESG matters.

Thematic investing

The fund aims to invest in sectors, industries, or companies that are expected to benefit from long-term macro or structural ESG-related trends.

Impact investing

The fund seeks to generate a positive, measurable social or environmental impact alongside a financial return.

Stewardship (sometimes referred to as active ownership)

The fund uses rights and position of ownership to influence the activities or behaviour of underlying portfolio companies in relation to ESG matters. This may include the use of ESG strategies such as proxy voting and/or shareholder engagement, which are explained below.

Proxy voting

The fund votes on management and/or shareholder resolutions in accordance with certain ESG-related considerations or aims.

Shareholder engagement

The fund interacts with the management of the company through meetings and/or written dialogue in accordance with certain ESG-related considerations or aims.

The above terms and definitions have been included for illustrative purposes only, and the Notice does not require or endorse the use of the above names and definitions for these ESG strategies, or the ESG strategies themselves. As further discussed under "Investment objectives and fund names", an ESG-Related Fund's description of these ESG strategies must be written using plain language so that investors can understand the fund's investment strategies.{7}

D. Key international and domestic developments

There have been a number of key international and domestic developments regarding ESG-related issues in asset management.

I. International developments

A number of securities regulators around the world have developed and implemented regulatory requirements or published policy recommendations and guidance pertaining to ESG or sustainability-related disclosure for investment funds.{8}

In addition, IOSCO has established the Sustainable Finance Task Force (the STF) with the aims of: (a) improving sustainability-related disclosures made by issuers and asset managers; (b) collaborating with other international organizations to avoid duplicative efforts and enhance coordination of relevant regulatory and supervisory approaches; and (c) conducting case studies and analyses of transparency, investor protection and other relevant issues within sustainable finance. The STF has three workstreams, with Workstream 2 being focused on sustainability-related practices, policies, procedures and disclosure in the asset management industry.{9}

As mentioned above, the IOSCO Report, which was produced by Workstream 2, sets out recommendations for securities regulators and policymakers, as applicable, in order to improve sustainability-related practices, policies, procedures and disclosure in the asset management industry.

One of the recommendations relates to the improvement of product-level disclosure in order to help investors better understand sustainability-related products and material sustainability-related risks for all products (the IOSCO Product Disclosure Recommendation). The IOSCO Product Disclosure Recommendation covers ten areas relating to product disclosure: (a) product authorization; (b) naming; (c) labelling and classification; (d) investment objectives disclosure; (e) investment strategies disclosure; (f) proxy voting and shareholder engagement disclosure; (g) risk disclosure; (h) marketing materials and website disclosure; (i) monitoring of compliance and sustainability-related performance; and (j) periodic sustainability-related reporting.

Another one of the recommendations in the IOSCO Report is that securities regulators and/or policymakers, as applicable, consider encouraging industry participants to develop common sustainable finance-related terms and definitions to ensure consistency throughout the global asset management industry (the IOSCO Terminology Recommendation, and together with the IOSCO Product Disclosure Recommendation, the IOSCO Recommendations).{10}

Lastly, in November 2021, the CFA Institute published the CFA Institute Global ESG Disclosure Standards for Investment Products to provide greater transparency and comparability to investors by enabling asset managers to clearly communicate the ESG-related features of their investment products.{11}

II. Domestic developments

Staff have conducted continuous disclosure reviews of the regulatory disclosure documents and sales communications of ESG-Related Funds and other funds that market themselves as ESG-Related Funds (the ESG CD Reviews). These reviews are discussed further below.

In addition, in October 2020, the Canadian Investment Funds Standards Committee (CIFSC) proposed a framework to identify Canadian investment funds that practice responsible investing (the RI Fund Identification Framework).{12} The goal of the RI Fund Identification Framework is to provide an objective, comprehensive list of Canadian responsible investing funds. In March 2021, following a comment period, the CIFSC published a response to the comments received and announced that it will be releasing a second version of the RI Fund Identification Framework for further comment.{13}

E. ESG CD Reviews

I. Scope and purpose

The purpose of the ESG CD Reviews was to assess, through reviews of each fund's regulatory disclosure documents and sales communications, the quality of the ESG-related aspects of the fund's disclosure, including whether the fund's disclosure of how ESG factors are integrated into its investment objectives and/or strategies in the fund's prospectus met the standard of full, true and plain disclosure of all material facts, and whether the fund's sales communications were misleading.

The ESG CD Reviews were also aimed at evaluating how well the current disclosure requirements address ESG-Related Funds and ESG-related disclosure and determining whether regulatory guidance is needed to explain how the current disclosure requirements apply to ESG-Related Funds and ESG-related disclosure.

The ESG CD Reviews included 32 funds managed by 23 different IFMs. Staff selected funds that referenced ESG in their investment objectives or strategies and/or that marketed themselves in online sales communications as ESG-Related Funds.

For each selected fund, staff reviewed: (a) the fund's prospectus and, where applicable, annual information form (AIF); (b) the fund facts document (Fund Facts) or ETF facts document (ETF Facts), as applicable; (c) the fund's annual and interim management reports of fund performance (MRFPs); and (d) some of the fund's online sales communications, including the fund's website.

II. Findings

The findings of the ESG CD Reviews are summarized below. Staff note, however, that some of these findings are observations rather than findings related to compliance with disclosure requirements. For guidance on how the disclosure requirements relate to each of the topics covered in the findings, see "Guidance" below.

(a) Investment objectives

One of the funds referenced ESG in its name and investment strategies disclosure but did not reference ESG in its investment objectives.

(b) Investment strategies

Most of the funds reviewed use ESG factors as part of their investment strategies. However, more than half of those funds lacked detailed disclosure in their investment strategies about the specific ESG factors considered by the fund, including failing to identify or explain the ESG factors. These funds also failed to disclose how the factors are evaluated.

In addition, around two-thirds of the funds reviewed use negative screening as an investment strategy, but a small portion of those funds did not provide an explanation of the negative screening factors where they were not self-explanatory.

A small number of the funds reviewed use multiple ESG strategies outside of negative screening but did not provide disclosure about how the various strategies work together, including the order in which they are applied during the investment selection process.

Slightly over a third of the funds held investments in industries that, according to their exclusionary investment strategies, should not have been permitted. In addition, a fifth of the funds had portfolio holdings that appeared to be inconsistent with the fund's name, investment objectives or investment strategies.{14}

(c) Risks

Almost half of the funds disclosed ESG-specific risks in their prospectuses.

(d) Proxy voting

More than half of the funds reviewed use proxy voting as a strategy to achieve their ESG-related investment objectives. However, more than half of those funds did not disclose this in their investment strategies disclosure.

In addition, of the funds that use proxy voting as an ESG strategy, more than half of those funds did not disclose their ESG-specific proxy voting policies and procedures in their prospectuses or AIFs, as applicable.

(e) Continuous disclosure

Around three-quarters of the funds reviewed did not report on the changes in the composition of their investment portfolios due to the ESG-related aspects of their investment objectives and investment strategies.

In addition, the vast majority of the funds reviewed did not report on their progress or status with regard to meeting their ESG-related investment objectives.

(f) Sales communications

One fund marketed itself as an ESG-Related Fund and identified itself as being suitable for investors that wish to invest primarily in companies that operate in accordance with ESG-related values, but its name, investment objectives and investment strategies did not reference ESG.

Around one-third of the funds reviewed provided more detailed disclosure of their investment strategies in their sales communications than they did in their prospectuses.

In addition, for a number of funds, there were discrepancies between their prospectuses and sales communications in the way that they described their investment strategies.

(g) Conclusion

In general, staff consider the current disclosure requirements to be broad enough in scope to address ESG-Related Funds and other ESG-related disclosure. However, in staff's view, regulatory guidance is needed to clarify how the current disclosure requirements apply to ESG-Related Funds and other ESG-related disclosure in order to improve the quality of ESG-related disclosure and sales communications. In addition, in staff's view, the ESG CD Reviews indicated that the disclosure of ESG-Related Funds would benefit from greater detail about the ESG-related aspects of the fund, particularly regarding investment strategies disclosure, proxy voting disclosure and continuous disclosure.

F. ESG-related changes to existing funds

In addition to the findings from the ESG CD Reviews, staff note that there have been a number of recent prospectus amendment filings by existing funds that wish to add references to ESG factors to their names and investment strategies without referencing ESG factors in their investment objectives.

G. Guidance

Based on the findings of the ESG CD Reviews, staff's observations of ESG-related changes to existing funds, and the IOSCO Recommendations, staff are providing guidance on how existing securities regulatory requirements apply to investment funds as they relate to ESG considerations, particularly ESG-Related Funds, in the following areas: (i) investment objectives and fund names; (ii) fund types; (iii) investment strategies disclosure; (iv) proxy voting and shareholder engagement policies and procedures; (v) risk disclosure; (vi) suitability; (vii) continuous disclosure; (viii) sales communications; (ix) ESG-related changes to existing funds; and (x) ESG-related terminology.

I. Investment objectives and fund names

An investment fund is required to disclose, in its prospectus, the fundamental investment objectives of the fund, including information that describes the fundamental nature or fundamental features of the fund that distinguish it from other funds.{15} Similarly, an investment fund is required to include, in its Fund Facts or ETF Facts, as applicable, a description of the fundamental nature or fundamental features of the fund that distinguish it from other funds.{16}

A fund's name and investment objectives play a role in identifying the primary focus of the fund and distinguishing it from other funds. A fund's name and investment objectives should therefore accurately reflect the primary focus of the fund. To prevent greenwashing, it is important that the name and investment objectives of a fund accurately reflect the extent to which the fund is focused on ESG, where applicable, including the particular aspect(s) of ESG that the fund is focused on.

Staff note that funds that do not have ESG-related investment objectives may still use ESG strategies. However, a fund that uses one or more ESG strategies as a material or essential aspect of the fund, as evidenced by the name of the fund or the manner in which it is marketed, is required to disclose such ESG strategies as an investment objective in its prospectus{17} and in its Fund Facts or ETF Facts, as applicable.{18} As discussed above, staff remind funds that the description of these ESG strategies must be written using plain language so that investors can understand the fund's investment objectives, in accordance with the requirement that the prospectus provide full, true and plain disclosure of all material facts.

Furthermore, a fund that primarily invests or intends to primarily invest, or whose name implies that it will primarily invest, in a type of issuer or industry segment associated with ESG is required to indicate this in its fundamental investment objectives,{19} as well as in its Fund Facts or ETF Facts, as applicable.{20} For example, this may include a fund that intends to primarily invest in companies that are transitioning to a low-carbon economy or a fund whose name implies that it will primarily invest in the water conservation industry.

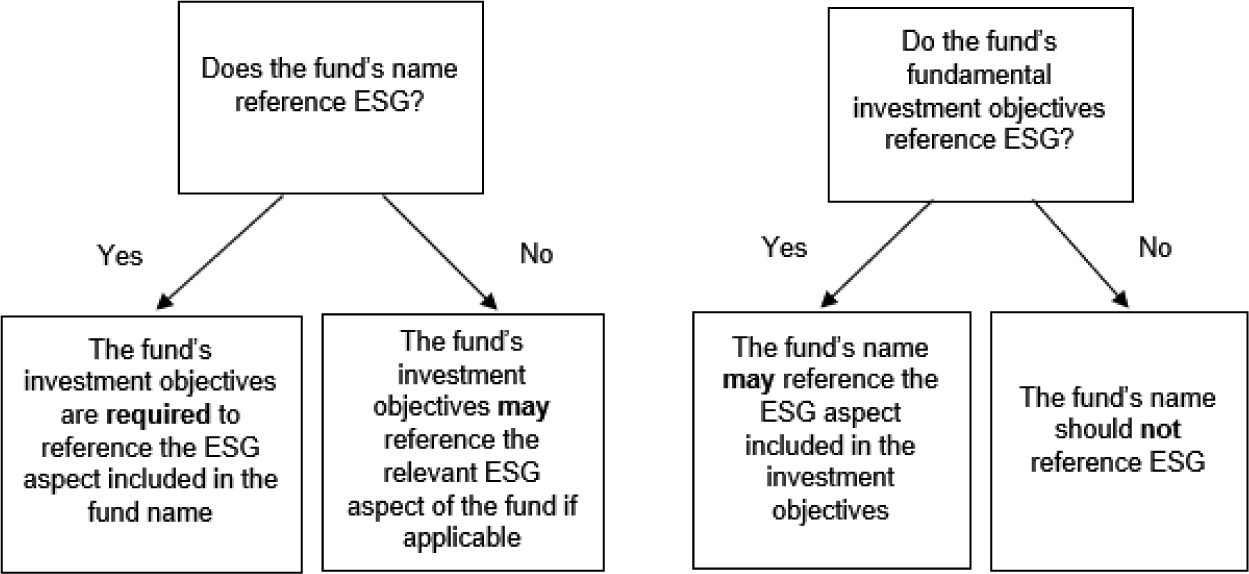

Staff note that the existing requirements draw a link between a fund's name and its investment objectives in order to ensure that there is consistency between them, given the importance of a fund's name in distinguishing it from other funds. Accordingly, in staff's view, where a fund's name references ESG or other related terms such as sustainability, green, social responsibility, etc., the fundamental investment objectives of the fund are required to reference the aspect of ESG included in the name of the fund. This is illustrated in Figure 1 below.

Staff acknowledge that not all ESG-related investment objectives relate to a measurable ESG outcome. However, where an ESG Fund intends to generate a measurable ESG outcome, staff encourage such funds to clearly state the intended outcome as part of their investment objectives in order to allow investors to identify funds that match their own ESG-related goals. For example, staff encourage funds that aim to reduce carbon emissions to disclose a measurable carbon emissions reduction target in their investment objectives. The inclusion of a measurable ESG outcome in a fund's investment objectives would also allow funds to provide meaningful continuous disclosure that reports on whether the fund is achieving its intended ESG outcome.

II. Fund types

A mutual fund that is not an ETF is required to identify, in its prospectus, the type of mutual fund that the fund is best characterized as.{21} Examples of types of mutual funds may include money market, equity, bond or balanced funds related, if appropriate, to a geographical region, or any other description that accurately identifies the type of mutual fund.{22}

Similar to fund names and investment objectives, the fund type identified in a fund's prospectus plays a role in identifying the focus of the fund.

While it is not a requirement, a mutual fund that includes ESG in its fundamental investment objectives may wish to characterize itself as a fund that is focused on ESG in addition to its primary fund type. For example, an ESG Fund may wish to identify itself as an ESG Canadian equity fund.

However, staff's view is that a fund that does not include ESG in its fundamental investment objectives should not characterize itself as a fund that is focused on ESG as it would not be an accurate identification of the fund type.

III. Investment strategies disclosure

An investment fund is required to disclose, in its prospectus, the principal investment strategies that the fund intends to use in achieving its investment objectives and the process by which the fund's portfolio adviser selects securities for the fund's portfolio, including any investment approach, philosophy, practices and techniques used.{23} In addition, as mentioned above, a prospectus must provide full, true and plain disclosure of all material facts.

Investment strategies disclosure provides clarity to investors about how the fund will achieve its investment objectives, including the nature and extent of the strategies employed by the fund, the investment universe from which the fund will select its investments, and which countries, industries, sectors or companies the fund may invest in. Full, true and plain ESG-related investment strategies disclosure enables investors to understand the ways in which the fund will meet its ESG-related investment objectives (if the fund is an ESG Fund) and the types of investments that the fund may make.

A fund that uses one or more ESG strategies, either as principal investment strategies or as part of its investment selection process, is required to provide disclosure about the ESG-related aspects of its investment selection process and strategies.

For both funds that use one or more ESG strategies as part of their principal investment strategies and those that use one or more ESG strategies as part of their investment selection process, the description of these ESG strategies must be written using plain language in order to ensure that investors are able to understand the fund's investment strategies, in accordance with the requirement that the prospectus provide full, true and plain disclosure of all material facts.

In addition, in staff's view, the investment strategies disclosure should include identifying any ESG factors used and explaining the meaning of each ESG factor and how the ESG factors are evaluated and monitored. This may include an explanation of whether the evaluation of the ESG factor is quantitative or qualitative and whether the evaluation is conducted using third-party data. Some ESG factors may be more complicated for investors to understand and may require further explanation, such as "involvement in severe controversial events" and "clean air", which are examples of some of the factors that were identified but not explained in the regulatory disclosure documents reviewed as part of the ESG CD Reviews.

If a fund's use of one or more ESG strategies includes the use of targets for specific ESG-related metrics, such as carbon emissions, staff encourage such funds to disclose those targets as part of their investment strategies and identify if those targets may evolve or change over time in response to changing circumstances.

Staff note that funds that reference ESG in their names or investment objectives may invest in companies that appear to be inconsistent with ESG values. For example, some investors may expect funds that reference ESG in their names or investment objectives to exclude investments in companies involved in thermal coal and weapons. However, a fund's disclosed ESG-related investment objectives and strategies may permit such holdings. For example, some of these funds may be permitted to invest in such companies up to a certain percentage of their portfolios or in order to use shareholder engagement to improve the ESG practices of those companies. Alternatively, a fund's ESG-related investment objectives and strategies may be focused only on a particular aspect of ESG that would not preclude investments in such companies.{24} To provide greater clarity to investors and in line with the principle of full, true and plain disclosure of all material facts, staff's view is that an ESG Fund should disclose whether it may, at any point in time, hold such investments, what those holdings would include (including examples), and how such holdings meet the fund's investment objectives. If an ESG Fund is not permitted to hold such investments at any point in time, this should be disclosed in its investment strategies along with information about the monitoring process used by the fund to screen out such investments, and the fund should ensure that its portfolio does not include any such investments.

Staff have observed that the prospectuses of some funds state that the fund "may" exclude certain types of investments from their portfolios. If a fund has discretion over whether a type of investment is excluded from its portfolio, this should be clearly disclosed.

Staff note that the above guidance relating to investment strategies disclosure applies to all investment funds, including index-tracking funds. The following guidance applies specifically to funds that use any of the following: (a) proxy voting or shareholder engagement as an ESG strategy; (b) multiple ESG strategies; and (c) ESG ratings, scores, indices or benchmarks.

(a) Use of proxy voting or shareholder engagement as an ESG strategy

Some ESG-Related Funds use proxy voting or shareholder engagement as ESG strategies. If a fund uses proxy voting or shareholder engagement as a principal investment strategy, the fund is required to disclose this in its investment strategies. Furthermore, funds that use proxy voting or shareholder engagement as a part of their investment selection process are required to disclose how they are used by the fund.

For both scenarios, in staff's view, the disclosure should include the criteria used by the proxy voting or shareholder engagement strategy, the goal of the proxy voting or shareholder engagement strategy and the extent of the monitoring process used to assess the success of the proxy voting or shareholder engagement strategy.

For example, a portfolio adviser may choose to invest in a company that has poor environmental practices in order to improve those practices by way of shareholder engagement. In this scenario, the use of shareholder engagement should be disclosed in the fund's investment strategies, along with the criteria used to determine whether a company has poor environmental practices, the aim of improving those practices through shareholder engagement and the extent of the monitoring process used to assess the success of the shareholder engagement strategy in improving the environmental practices of the company.

While staff acknowledge that for some IFMs, proxy voting and shareholder engagement are conducted at the IFM level rather than at the fund level, the above guidance is intended to apply specifically to funds that use proxy voting or shareholder engagement as an ESG investment strategy.

(b) Use of multiple ESG strategies

Funds that use multiple ESG strategies are required to provide disclosure explaining how the different ESG strategies are applied during the investment selection process. In staff's view, this disclosure should include the order in which the strategies are applied, if the strategies are not applied simultaneously. For example, a fund that uses negative screening as an initial filter on the fund's investment universe and then uses an ESG integration strategy to evaluate the potential investments should disclose this in its prospectus.

(c) Use of ESG ratings, scores, indices or benchmarks

An ESG rating or score is an assessment of an organization or product's relative ESG characteristics, effectiveness and performance, including its exposure to ESG risks and/or opportunities.

In staff's view, where an ESG-Related Fund uses internal or third-party company-level ESG ratings or scores, or ESG-related indices or benchmarks, as part of its principal investment strategies or investment selection process, the fund should explain how those ratings, scores, indices or benchmarks are used.

Staff's view is that, for funds that use ESG-related indices or benchmarks as part of their principal investment strategies or investment selection process, the fund should identify the index or benchmark used.{25} For funds that use third-party, company-level ESG ratings or scores as part of their principal investment strategies or investment selection process, the fund should identify the provider of the ratings or scores.

In staff's view, the disclosure should also include a description of the methodology used to create the company-level ESG ratings or scores, or ESG-related indices or benchmarks, including, for example, whether the methodology is based on quantitative or qualitative data and the level of subjectivity involved in the methodology.

IV. Proxy voting and shareholder engagement policies and procedures

(a) Proxy voting

An investment fund must include in its prospectus and/or AIF, as applicable, a summary of the policies and procedures that the fund follows when voting proxies relating to portfolio securities.{26}

Further, an investment fund is also required to promptly send the most recent copy of its proxy voting policies and procedures to any securityholder upon request.{27}

Disclosure of a fund's proxy voting policies and procedures can provide clarity to investors about the ways in which proxy voting is used by ESG Funds to achieve their ESG-related investment objectives, including the scope and limits of their use.

If a fund uses proxy voting as an ESG investment strategy, the prospectus and/or AIF, as applicable, is required to include a summary of the ESG aspects of the fund's proxy voting policies and procedures. This summary would provide clarity about how the voting rights attached to the fund's portfolio securities will be used to further the fund's ESG-related investment objectives, or in the case of a fund that does not have ESG-related investment objectives but that uses proxy voting as an ESG strategy, how the ESG-related proxy voting strategy is implemented.

In order to provide investors with greater transparency, staff also encourage investment funds to make the most recent copy of their proxy voting policies and procedures available on their designated websites.

(b) Shareholder engagement

Staff recognize that there is currently no requirement for investment funds to make their shareholder engagement policies and procedures publicly available. However, staff encourage all funds that use shareholder engagement as an ESG strategy to do so in order to provide investors with greater transparency into the scope and nature of the fund's use of shareholder engagement as an ESG strategy.

As stated above, while staff acknowledge that for some IFMs, proxy voting and shareholder engagement are conducted at the IFM level rather than at the fund level, the above guidance is intended to apply specifically to funds that use proxy voting or shareholder engagement as an ESG investment strategy.

V. Risk disclosure

An investment fund is required to describe, in its prospectus, any material risks associated with an investment in the fund,{28} including any risks associated with any particular aspect of the fundamental investment objectives and investment strategies.{29}

Risk disclosure enables investors to better understand the potential material risks associated with investing in the fund, including the impact of those risks on a fund's performance.

(a) Risk disclosure by ESG-Related Funds

The risk disclosure of ESG-Related Funds enables investors to better understand the challenges faced by the fund in meeting its ESG-related investment objectives, if applicable, or using its ESG strategies.

An ESG-Related Fund should consider whether there are any material risk factors that are applicable to the fund as a result of the fund's ESG-related investment objectives and/or its use of ESG strategies and disclose such risk factors where applicable. Examples may include concentration risk, risk of underperformance due to the fund's ESG-related focus, and risk arising from potential over-reliance on third-party ESG ratings in assessing the ESG performance of underlying holdings.

(b) ESG-related risk disclosure by all funds

The disclosure of material ESG-related risks by all types of funds, regardless of whether they are ESG-Related Funds, may assist investors with making informed investment decisions about how ESG issues can impact their investments.

All investment funds, regardless of whether they are ESG-Related Funds, should consider whether there are any material ESG-related risk factors that are applicable to the fund and disclose such risk factors where applicable. Examples of such risk factors may include climate change risk and bribery and corruption risks.

In order to be able to provide useful ESG-related risk disclosure, staff remind IFMs to ensure that their risk management framework takes ESG-related risks into account.

VI. Suitability

An investment fund must include, in its Fund Facts or ETF Facts, as applicable, a brief statement of the suitability of the fund for particular investors, including describing the characteristics of the investor for whom the fund may or may not be an appropriate investment, and the portfolios for which the fund is and is not suited.{30} If the fund is particularly suitable for investors who have particular investment objectives, this can be disclosed.{31}

Similar to fund names, investment objectives and fund types, in order to avoid greenwashing, the suitability statement should accurately reflect the extent of the fund's focus on ESG as well as the particular aspect(s) of ESG that the fund is focused on, but only if applicable.

Where appropriate, an ESG Fund may wish to state that it is particularly suitable for investors who have ESG-related investment objectives. However, if the fund is only focused on a particular aspect of ESG, such as gender diversity in leadership or the reduction of carbon emissions, staff's view is that any suitability statement that indicates that the fund is particularly suitable for investors who have ESG-related investment objectives should accurately reflect the particular aspect of ESG that the fund is focused on.

However, staff's view is that an ESG Strategy Fund should not state that the fund is particularly suitable for investors who have ESG-related investment objectives, as the fund does not have ESG-related investment objectives.

VII. Continuous disclosure

An investment fund must include, in its MRFP, a summary of the results of operations of the investment fund for the financial year to which the MRFP pertains, including a discussion of how the composition and changes to the composition of the investment portfolio relate to the fund's fundamental investment objective and strategies.{32} Staff note, however, that funds are only required to disclose information that is material.{33}

Continuous disclosure, including the MRFP, enables investors to monitor a fund's performance and evaluate its ability to meet its objectives on an ongoing basis. For funds that have ESG-related investment objectives, continuous disclosure can help prevent greenwashing by allowing investors to monitor the fund's ESG performance and therefore evaluate the fund's progress in terms of meeting its ESG-related investment objectives.

An ESG-Related Fund is required to disclose in its MRFP how the composition and changes to the composition of the investment portfolio relate to the fund's ESG-related investment objectives and/or strategies. For example, if a fund that excludes companies that have had severe ESG-related controversies divests of its holdings in a company because the company has recently had a harassment scandal that is deemed by the fund to be a severe ESG-related controversy, the fund should disclose its divestment and the reason for the divestment in the MRFP. Another example would be a fund that uses a best-in-class strategy that has divested its holdings in a company that no longer meets the fund's criteria. In addition to divestment, a fund may also choose to increase or decrease its holdings in a company in order to meet the fund's ESG-related investment objectives and this should be disclosed.

Funds with ESG-related investment objectives, unlike other types of funds, typically aim to achieve ESG-related outcomes in addition to financial performance. In order to provide investors with meaningful disclosure about those ESG-related outcomes, staff encourage funds that have ESG-related investment objectives to disclose, as part of the summary of the results of the fund's operations in the MRFP, the ESG-related aspects of those operations. This would include the fund's progress or status with regard to meeting its ESG-related investment objectives. For example, in the case of a fund whose investment objectives state that the fund will invest in companies that contribute to the fight against climate change, investors would benefit from continuous disclosure that explains which companies the fund has invested in during the relevant period and how they have contributed to the fight against climate change.

In addition, staff encourage funds that intend to generate a measurable ESG outcome to report in their MRFPs on whether the fund is achieving that outcome. For example, where a fund's investment objectives refer to the reduction of carbon emissions, investors would benefit from disclosure in the fund's MRFP that includes the quantitative key performance indicators for carbon emissions.

Staff acknowledge that websites and non-regulatory documents are being increasingly used to provide ongoing information about the ESG performance and metrics of funds, as well as other ESG-related information. In addition to the required disclosure in the MRFP, staff encourage funds to provide investors with additional periodic information on how they are meeting their ESG-related investment objectives. We remind funds that websites and such non-regulatory documents are considered sales communications under National Instrument 81-102 Investment Funds (NI 81-102), which are discussed further below under "Sales communications".

In order to be able to provide useful disclosure about the fund's progress or status with regard to meeting its ESG-related investment objectives, staff encourage IFMs to regularly assess, measure and monitor the ESG performance of the funds that they manage.

(a) Funds that use proxy voting as an ESG strategy

An investment fund is required to maintain a proxy voting record{34} and make its most recent annual proxy voting record available on its designated website, as well as promptly send it to any securityholder upon request.{35}

Staff acknowledge that a fund is only required to make its most recent annual proxy voting record available on its designated website and to promptly send it to any securityholder upon request. However, staff encourage all funds, particularly funds that use proxy voting as an ESG strategy, to make all of their annual proxy voting records, including historical records from previous years, available on their designated websites. For funds that use proxy voting as an ESG strategy to meet their ESG-related investment objectives, such disclosure would provide greater transparency into how the fund has historically used proxy voting to meet the fund's ESG-related investment objectives. In the case of a fund that does not have ESG-related investment objectives but that uses proxy voting as an ESG strategy, this disclosure would provide greater transparency into how the fund's ESG-related proxy voting strategy has historically been implemented.

In addition, for the reasons stated above, staff encourage all funds that use proxy voting as an ESG strategy to include, as part of the summary of the results of the fund's operations in the MRFP, disclosure about how the past proxy voting records during that period align with the ESG-related investment objectives and/or strategies of the fund.

(b) Funds that use shareholder engagement as an ESG strategy

Staff acknowledge that there are currently no continuous disclosure requirements relating to a fund's past shareholder engagement activities.

However, staff encourage all funds that use shareholder engagement as an ESG strategy to provide disclosure about their past shareholder engagement activities on their designated websites, for the same reasons discussed above in relation to the disclosure of past proxy voting records.

In addition, similarly, staff encourage all funds that use shareholder engagement as an ESG strategy to include, as part of the summary of the results of the fund's operations in the MRFP, disclosure about how the fund's past shareholder engagements during that period align with the ESG-related investment objectives and/or strategies of the fund.

VIII. Sales communications

A sales communication pertaining to an investment fund is prohibited from including a statement that conflicts with information that is contained in the fund's regulatory offering documents.{36} In addition, a sales communication pertaining to an investment fund is also prohibited from being untrue or misleading.{37}

The Companion Policy to NI 81-102 lists some of the circumstances in which, in the view of the Canadian securities regulatory authorities, a sales communication would be misleading. One such circumstance is if the sales communication contains a statement that lacks explanations, qualifications, limitations or other statements necessary or appropriate to make the statement in the sales communication not misleading.{38} Another circumstance is if the sales communication contains a statement about the characteristics or attributes of an investment fund that makes exaggerated or unsubstantiated claims about management skill or techniques, characteristics of the investment fund or an investment in securities issued by the fund.{39}

In addition, staff are of the view that sales communications should not contain statements that are vague or exaggerated, or that cannot otherwise be verified.{40}

Sales communications, including websites, play a key role in providing information about the investment objectives, investment strategies and performance of funds that investors may consider investing in. Therefore, sales communications relating to ESG that are not untrue or misleading and that are consistent with a fund's regulatory offering documents are important in order to prevent greenwashing.

(a) Sales communications that indicate that the fund is focused on ESG

A sales communication pertaining to an investment fund should accurately reflect the extent to which the fund is focused on ESG, as well as the particular aspect(s) of ESG that the fund is focused on.

In staff's view, a fund should not include statements in its sales communications that indicates that it is focused on ESG unless the fund references ESG in its investment objectives.

A fund that does not reference ESG in its investment objectives but that discloses in its investment strategies prospectus disclosure that it uses an ESG strategy may include statements in its sales communications that accurately reflect the extent to which that strategy is used. However, such funds should not exaggerate the extent of the fund's focus on ESG in their sales communications.

In contrast, while a fund that does not reference ESG in either its investment objectives or investment strategies may provide factual information about the ESG characteristics of its portfolio (such as fund-level ESG ratings, scores or rankings), it should not include any ESG-related claims about what the fund is trying to achieve. In staff's view, such sales communications would both conflict with the investment objectives and investment strategies disclosure in the fund's regulatory offering documents, which do not reference ESG at all, and be misleading.

In general, in staff's view, a sales communication that does not accurately reflect the extent to which a fund is focused on ESG, as well as the particular aspect(s) of ESG that the fund is focused on, would both be misleading and conflict with the information in the fund's regulatory offering documents. Examples of such sales communications may include those that do any of the following:

• suggest that a fund is focused on ESG when it is not;

• suggest that a fund is focused on all three components of ESG when it is only focused on one component, such as governance;

• misrepresent the extent and nature of the fund's use of ESG strategies, including:

• in the case of a fund that has a discretionary or optional screening strategy, stating that the fund uses a negative or exclusionary screening strategy without clearly disclosing that the screening is discretionary or optional; or

• failing to:

• disclose that there is a maximum limit to the fund's use of those strategies;

• actually use the advertised ESG strategies, including using different types of ESG strategies altogether; or

• prominently disclose material aspects of the ESG strategies.

Staff have noticed that some ESG-Related Funds provide more detail about the fund's ESG strategies in their sales communications than they do in their prospectuses. Staff remind funds that a prospectus must provide full, true and plain disclosure of all material facts, including the investment strategies of the fund.

(b) Sales communications that reference a fund's ESG performance

A fund must not include misleading statements in its sales communications about the ESG performance of the fund. Examples of such sales communications may include those that:

• make inaccurate claims about the fund's ESG performance or results;

• make inaccurate claims about the existence of a direct causal link between the fund's investment strategies and ESG performance or results; or

• manipulate elements of disclosure to present the fund's ESG performance or results in a positive light, such as cherry-picking data.

(c) Sales communications that include fund-level ESG ratings, scores or rankings

Staff understand that some IFMs may wish to include fund-level ESG ratings, scores or rankings on their websites or other sales communications. These would include, but are not limited to, fund-level ESG ratings or scores that are primarily weighted averages of the company-level ESG ratings or scores of the underlying portfolio holdings of the fund (Portfolio-Based ESG Ratings), and fund-level ESG rankings based solely on Portfolio-Based ESG Ratings (Portfolio-Based ESG Rankings).

While staff are of the view that the Portfolio-Based ESG Ratings and Portfolio-Based ESG Rankings that staff have observed to date are not "performance data" and "performance ratings or rankings" within the context of Part 15 of NI 81-102 (Part 15), other types of fund-level ESG ratings, scores and rankings that are not Portfolio-Based ESG Ratings and Portfolio-Based ESG Rankings may be considered "performance data" or "performance ratings or rankings". Similarly, while staff are of the view that the comparison of Portfolio-Based ESG Ratings and Portfolio-Based ESG Rankings that staff have observed to date are not comparisons of performance within the context of Part 15,{41} the comparison of other types of fund-level ESG ratings, scores and rankings that are not Portfolio-Based ESG Ratings and Portfolio-Based ESG Rankings may be considered to be comparisons of performance.

If a type of fund-level ESG rating, score or ranking is considered "performance data" or a "performance rating or ranking", or a comparison of that type of fund-level ESG rating, score or ranking is considered to be a comparison of performance, sales communications that include this type of fund-level ESG rating, score or ranking, or a comparison thereof, may not be able to comply with some of the provisions of Part 15 that relate to "performance data", "performance ratings or rankings" and comparisons of performance (the Performance Requirements). Staff remind IFMs to review and consider the Performance Requirements to determine whether such sales communications are in compliance and encourage IFMs that wish to include other types of fund-level ESG ratings, scores and rankings in their sales communications to contact staff of their principal regulator as needed.

In addition, any sales communication that includes fund-level ESG ratings, scores or rankings, including Portfolio-Based ESG Ratings and Portfolio-Based ESG Rankings, must not be misleading. In staff's view, a sales communication that includes fund-level ESG ratings, scores or rankings may be misleading for a number of reasons, including any of the following:

• there are conflicts of interest involving the provider that prepares the fund-level ESG rating, score or ranking;

• the selection of the specific fund-level ESG rating, score or ranking is the result of cherry-picking fund-level ESG ratings, scores or rankings in order to present the fund's ESG characteristics or performance in a positive light;

• the selected fund-level ESG rating, score or ranking is not representative of the ESG characteristics or performance of the fund;

• the sales communication does not include explanations, qualifications, limitations or other statements necessary or appropriate to make the inclusion of the fund-level ESG ratings, scores or rankings in the sales communication not misleading.

Guidance on how to avoid these four issues is provided below.

Staff note, however, that a sales communication that includes fund-level ESG ratings, scores or rankings may also be misleading for reasons that have not been identified in this Notice and remind IFMs to review and consider the requirements under Part 15 when preparing sales communications.

Conflicts of interest

To address conflicts of interest, staff's view is that the fund-level ESG rating, ranking or score that is included in the sales communication should be prepared by a provider that:

(a) rates, scores or ranks the ESG characteristics or performance of the fund through an objective methodology that is (i) applied consistently to all funds rated, scored or ranked by it, and (ii) disclosed on the provider's website;

(b) is not a member of the organization of the fund;{42} and

(c) is not paid to assign a fund-level ESG rating, score or ranking to the fund by the promoter, manager, portfolio adviser, principal distributor or participating dealer of any fund or any of their affiliates.

In addition, for a fund-level ESG ranking, the ranking should be based on a published category of funds, such as Canadian equity funds, that is not established or maintained by a member of the organization of the fund.

Selection of fund-level ESG rating, score or ranking

To help ensure that the selection of the fund-level ESG rating, score or ranking is not the result of cherry-picking, staff are of the view that the selection of the rating, score or ranking should be consistent with the following parameters:

(a) the IFM should consider whether the selected fund-level ESG rating, score or ranking is an accurate representation of the fund (and its portfolio, if the fund-level ESG rating, score or ranking is based on the fund's portfolio) during the time period that the sales communication appears or is in use and therefore, whether the inclusion of the selected fund-level ESG rating, score or ranking in a sales communication may be misleading;

(b) for a fund-level ESG ranking, the ranking should be based on a published category of funds, such, as for example, Canadian fixed income funds, that provides a reasonable basis for evaluating the ESG characteristics or performance of the fund;

(c) if a fund-level ESG rating, score or ranking is disclosed on the website of a fund that is not an ESG Fund, the IFM should disclose the same type of fund-level ESG rating, score or ranking from the same provider, if available, for all of the funds that it manages; and

(d) if a fund-level ESG rating, score or ranking is disclosed on the website of an ESG Fund, the IFM should disclose the same type of fund-level ESG rating, score or ranking from the same provider, if available, for all of the ESG Funds that it manages.

However, staff would not view paragraph (d) as applicable to an ESG Fund that has a specialized ESG focus, such as a fund focused on climate change, if the fund-level ESG rating, score or ranking that is being disclosed is specific to the specialized ESG focus of the fund, such as a rating relating to carbon emissions.

In addition, staff encourage funds that wish to disclose fund-level ESG ratings, scores or rankings in their sales communications to disclose fund-level ESG ratings, scores or rankings from at least 2 different providers.

Representativeness of fund's ESG characteristics or performance

Furthermore, for a Portfolio-Based ESG Rating, if only a certain percentage of a fund's underlying portfolio is covered by the Portfolio-Based ESG Rating (i.e. if less than 100% of the fund's underlying portfolio has been rated), staff's view is that the IFM should consider whether the portion of the portfolio that has not been rated has substantially similar ESG characteristics to the rest of the portfolio and therefore, whether the Portfolio-Based ESG Rating is an accurate representation of the ESG characteristics or performance of the entire portfolio. If the portion of the portfolio that has not been rated does not have substantially similar ESG characteristics as compared to the rest of the portfolio, the Portfolio-Based ESG Rating may not be an accurate representation of the entire portfolio and therefore, the inclusion of the Portfolio-Based ESG Rating in a sales communication may be misleading.

The above also applies to Portfolio-Based ESG Rankings that are based on Portfolio-Based ESG Ratings where less than 100% of the fund's underlying portfolio has been rated.

Accompanying disclosure

Finally, to avoid being misleading, staff are of the view that a sales communication that includes fund-level ESG ratings, scores or rankings should include the following disclosure:

(a) the name of the provider that prepared the fund-level ESG rating, score or ranking;

(b) the date or time period covered by the fund-level ESG rating, score or ranking:

(i) if the fund-level ESG rating, score or ranking is as of a specific point in time, the date of the specific point in time;

(ii) if the fund-level ESG rating, score or ranking covers a time period:

(A) the period of time; and

(B) a brief explanation of how the fund-level ESG rating, score or ranking was determined for the specified time period (e.g. if the fund-level ESG rating, score or ranking is based on an average of the monthly fund-level ESG ratings, scores or rankings from the past 12 months);

(c) how often the fund-level ESG rating, score or ranking is updated by the provider (e.g. on a monthly basis);

(d) cautionary language stating that the fund's ESG characteristics and performance may differ from time to time;

(e) for Portfolio-Based ESG Ratings, the percentage of the fund's underlying portfolio holdings that has been rated;

(f) for Portfolio-Based ESG Rankings, the percentage of the fund's underlying portfolio holdings that has been rated for the purpose of the Portfolio-Based ESG Rating on which the Portfolio-Based ESG Ranking is based;

(g) for fund-level ESG ratings or scores, the range of the fund-level ESG rating or score (e.g. AAA to CCC);

(h) for fund-level ESG rankings:

(i) the classification of the peer group used for the ranking (e.g. Canadian equity); and

(ii) the number of funds in the peer group;

(i) if the fund is not an ESG Fund, cautionary language that states that the fund does not have ESG-related investment objectives;

(j) if applicable, cautionary language that states that the fund-level ESG rating or score (or in the case of a fund-level ESG ranking, the fund-level ESG rating or score on which the ranking is based) does not evaluate the ESG-related investment objectives of, or any ESG strategies used by, the fund and is not indicative of how well ESG factors are integrated by the fund;

(k) a one or two sentence summary explaining what the fund-level ESG rating, score, or ranking measures or assesses, including:

(i) for a fund-level ESG ranking, language identifying the fund-level ESG rating or score that the ranking is based on;

(ii) for a Portfolio-Based ESG Rating or Portfolio-Based ESG Ranking, language that states that the fund-level ESG rating or score (or in the case of a fund-level ESG ranking, the fund-level ESG rating or score on which the ranking is based) is a weighted average ESG rating or score of the company-level ESG ratings or scores of the underlying portfolio holdings of the fund; and

(iii) for a fund-level ESG rating, score or ranking that is not a Portfolio-Based ESG Rating or Portfolio-Based ESG Ranking, an explanation of what the fund-level ESG rating or score (or in the case of a fund-level ESG ranking, the fund-level ESG rating or score on which the ranking is based) measures or assesses;

(l) if the sales communication is online, a link to the full methodology of the fund-level ESG rating or score (or in the case of a fund-level ESG ranking, the fund-level ESG rating or score on which the ranking is based);

(m) if the sales communication is not an online sales communication, language explaining how to easily access, free of charge, the full methodology of the fund-level ESG rating or score (or in the case of a fund-level ESG ranking, the fund-level ESG rating or score on which the ranking is based);

(n) if applicable, a statement indicating that other providers may also prepare fund-level ESG ratings or scores (or in the case of fund-level ESG rankings, the fund-level ESG ratings or scores on which the rankings are based) using their own methodologies, which may differ from the methodology used by the provider;

(o) if the sales communication is online, a link to the fund's website containing the same type of fund-level ESG ratings, scores or rankings for the fund on the same periodic basis as updated by the provider over the past 12 months;

(p) if the sales communication is not an online sales communication, language explaining how to easily access, free of charge, the same type of fund-level ESG ratings, scores or rankings for the fund on the same periodic basis as updated by the provider over the past 12 months; and

(q) a cross-reference to the fund's prospectus for further information about the fund's investment objectives and strategies.

In addition, staff encourage funds to disclose separate fund-level ratings, scores or rankings, as applicable, for each of the three components of ESG.

The above accompanying disclosure should be clear and not buried within fine print.

Staff note that while the above list of accompanying disclosure has been provided to assist IFMs in the preparation of sales communications for their funds, the list is non-exhaustive and a sales communication that includes fund-level ESG ratings, scores or rankings and the above accompanying disclosure may still be misleading for other reasons.

IX. ESG-related changes to existing funds

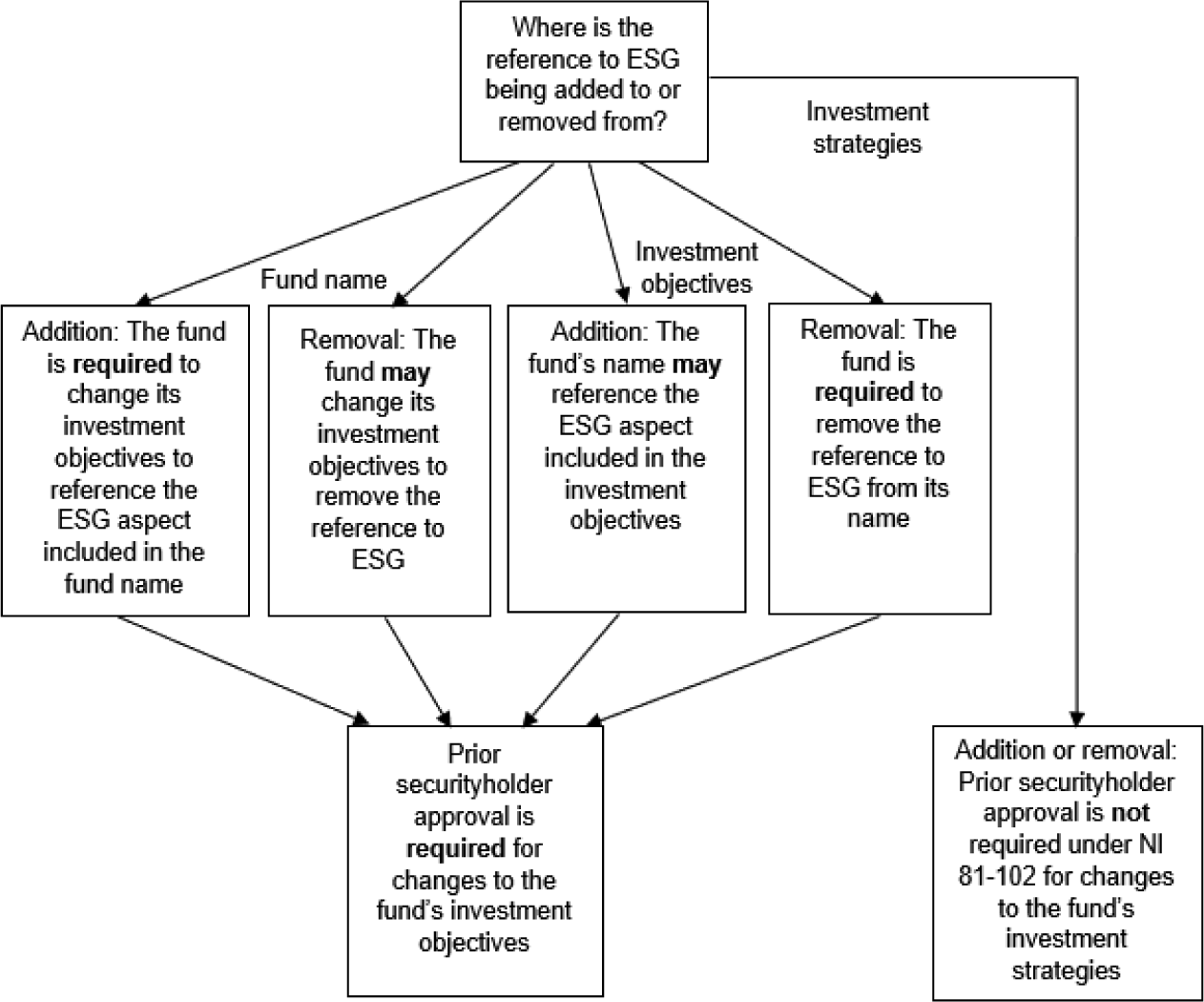

As noted above under "Investment objectives and fund names", where a fund's name references ESG, the fundamental investment objectives of the fund are required to reference the aspect of ESG included in the name of the fund.

Accordingly, where a fund intends to change its name to add or remove a reference to ESG, the fund should consider whether it is also required to change its fundamental investment objectives.

Staff remind funds that an investment fund that changes its fundamental investment objectives is required to obtain the prior approval of its securityholders.{43} Consequently, the addition or removal of references to ESG in the fundamental investment objectives of a fund is subject to the requirement to obtain prior securityholder approval.

Staff note that a fund that does not have ESG-related investment objectives may still use ESG strategies and may therefore reference ESG in its investment strategies disclosure without referencing ESG in its name or indicating that the fund is focused on ESG in its sales communications. Where an ESG strategy is not a material or essential aspect of a fund and is therefore not included in the fund's fundamental investment objectives, a fund that adds or removes disclosure about the ESG strategy in its investment strategies disclosure is not subject to the securityholder approval requirement in NI 81-102.

The guidance above is illustrated in Figure 2.

X. ESG-related terminology

As discussed earlier, there is currently a lack of consistency in ESG-related terminology and definitions used throughout the investment fund industry, especially with regard to ESG strategies, which increases the potential for investor confusion around ESG-Related Funds.

A fund's description of the ESG strategies that it uses must be written using plain language in order to ensure that investors are able to understand the fund's investment strategies. In addition, if a fund's prospectus includes other ESG-related terms that are not commonly understood, it should provide a clear explanation of those terms using plain language in accordance with the requirement that the prospectus provide full, true and plain disclosure of all material facts.

Staff encourage industry participants, including IFMs, to develop common ESG-related terms and definitions, particularly with regard to ESG strategies, which would enable investors to better understand ESG-Related Funds and make informed investment decisions about them.

XI. IFM-level commitments to ESG-related initiatives

Staff recognize that some IFMs are signatories to international or regional ESG-related entity-level initiatives, such as the United Nations Principles for Responsible Investment and Task Force on Climate-related Financial Disclosures, and publicly disclose this information. For IFMs that are signatories to such initiatives, it is important for the disclosure of their signatory status or commitment to these initiatives to be clear that the commitment is at the entity-level rather than at the fund-level and where applicable, that the funds managed by the IFM may not be focused on ESG.

H. Conclusion

Full, true and plain disclosure is essential to maintaining and strengthening investor confidence and efficient capital markets. In addition, it is important that investment funds be marketed to investors using sales communications that are not untrue or misleading, and that are consistent with a fund's regulatory offering documents. Staff will continue to monitor the regulatory disclosure documents and sales communications of ESG-Related Funds and any other funds that market themselves as being focused on ESG and consider future policy initiatives as needed.

We encourage IFMs to consider the guidance in this Notice when preparing the regulatory disclosure documents and sales communications of investment funds, particularly ESG-Related Funds.

Questions

Please refer your questions to any of the following:

British Columbia Securities Commission

James Leong

Senior Legal Counsel

Legal Services, Corporate Finance

Phone: 604-899-6681

E-mail: <<[email protected]>>

Alberta Securities Commission

Jan Bagh

Senior Legal Counsel

Corporate Finance

Phone: 403-355-2804

E-mail: <<[email protected]>>

Chad Conrad

Senior Legal Counsel

Corporate Finance

Phone: 403-297-4295

E-mail: <<[email protected]>>

Financial and Consumer Affairs Authority of Saskatchewan

Heather Kuchuran

Director

Corporate Finance, Securities Division

Phone: 306-787-1009

E-mail: <<[email protected]>>

Manitoba Securities Commission

Patrick Weeks

Analyst

Corporate Finance

Phone: 204-945-3326

E-mail: <<[email protected]>>

Ontario Securities Commission

Bryana Lee

Legal Counsel

Investment Funds and Structured Products

Phone: 416-593-2382

E-mail: <<[email protected]>>

Ritu Kalra

Senior Accountant

Investment Funds and Structured Products

Phone: 416-593-8063

E-mail: <<[email protected]>>

Stephen Paglia

Manager

Investment Funds and Structured Products

Phone: 416-593-2393

E-mail: <<[email protected]>>

Autorité des marchés financiers

Olivier Girardeau

Senior Analyst

Investment Funds Oversight

Phone: 514-395-0337 ext. 4334

E-mail: <<[email protected]>>

Marie-Aude Gosselin

Analyst

Investment Funds Oversight

Phone: 514-395-0337 ext. 4456

E-mail: <<[email protected]>>

Financial and Consumer Services Commission, New Brunswick

Ella-Jane Loomis

Senior Legal Counsel

Securities

Phone: 506-453-6591

E-mail: <<[email protected]>>

Nova Scotia Securities Commission

Jack Jiang

Securities Analyst

Phone: 902-424-7059

E-mail: <<[email protected]>>

Peter Lamey

Legal Analyst

Phone: 902-424-7630

E-mail: <<[email protected]>>

{1} Where this Notice provides best practices, staff have used the language "staff encourage".

{2} Global Sustainable Investment Alliance, "Global Sustainable Investment Review 2020", accessible at: http://www.gsi-alliance.org/wp-content/uploads/2021/08/GSIR-20201.pdf.

{3} Responsible Investment Association, "2020 Canadian Responsible Investment Trends Report" (November 2020), accessible at: https://www.riacanada.ca/content/uploads/2021/01/2020-RI-Trends-Report-FINAL-Jan-21-UPDATED.pdf.

{4} The Globe and Mail, "Investment firms are shifting their businesses as interest in ESG rises" (June 30, 2021), accessible at: https://www.theglobeandmail.com/investing/globe-advisor/advisor-news/article-investment-firms-are-shifting-their-businesses-as-interest-in-esg/.

{5} International Organization of Securities Commissions, "Recommendations on Sustainability-Related Practices, Policies, Procedures and Disclosure in Asset Management: Final Report" (November 2021), accessible at: https://www.iosco.org/library/pubdocs/pdf/IOSCOPD688.pdf.

{7} Subsection 4.1(1) of National Instrument 81-101 Mutual Fund Prospectus Disclosure; General Instruction (5) to Form 41-101F2 Information Required in an Investment Fund Prospectus (Form 41-101F2); subsection 3B.2(1) of National Instrument 41-101 General Prospectus Requirements. Also see, amongst others, subsection 113(1) of the Securities Act (Alberta), subsection 63(1) of the Securities Act (British Columbia), subsection 56(1) of the Securities Act (Ontario) and section 13 of the Securities Act (Québec).

{8} For example, see the European Union's "Sustainable Finance Disclosure Regulation" (Regulation 2019/2088, accessible at: https://eur-lex.europa.eu/eli/reg/2019/2088/oj), France's "Information to be Provided by Collective Investment Schemes Incorporating Non-Financial Approaches" (AMF Position DOC-2020-03, accessible at: https://www.amf-france.org/en/regulation/policy/doc-2020-03), Hong Kong's "Circular to management companies of SFC-authorized unit trusts and mutual funds -- ESG funds" (accessible at: https://apps.sfc.hk/edistributionWeb/gateway/EN/circular/products/product-authorization/doc?refNo=21EC27) and Malaysia's "Guidelines on Sustainable and Responsible Investment Funds" (SC-GL/4-2017, accessible at: https://www.sc.com.my/api/documentms/download.ashx?id=9a455914-71db-4982-a34b-9a8fc7df79b5). For an overview of regulatory requirements and guidance pertaining to sustainability-related product disclosure, see Chapter 3 of the IOSCO Report.

{9} The Ontario Securities Commission is the co-lead of Workstream 2, along with the Securities and Futures Commission of Hong Kong. Workstream 1 is focused on sustainability-related disclosures for corporate issuers while Workstream 3 is focused on ESG ratings and data providers. The Ontario Securities Commission is a member of Workstream 1 and the Autorité des marchés financiers is a member of Workstream 3.

{10} The other recommendations relate to: (a) asset manager practices, policies, procedures and firm-level disclosure; (b) supervision and enforcement; and (c) financial and investor education.

{11} CFA Institute, "Global ESG Disclosure Standards for Investment Products" (2021), accessible at: https://www.cfainstitute.org/-/media/documents/ESG-standards/Global-ESG-Disclosure-Standards-for-Investment-Products.pdf.

{12} Canadian Investment Funds Standards Committee, "CIFSC Responsible Investment Identification" (October 2020), accessible at: https://www.cifsc.org/the-cifsc-proposes-to-adopt-an-ri-fund-identification-framework/.

{13} Canadian Investment Funds Standards Committee, "RE: CIFSC response to public comments regarding the RI Fund Identification Proposal" (March 19, 2021), accessible at: https://www.cifsc.org/wp-content/uploads/2021/03/CIFSC-response-to-comments-regarding-RI-fund-identification-proposal-1.pdf.

{14} Staff note that a fund that references ESG in its name or investment objectives may be permitted to invest in companies that appear to be inconsistent with ESG values; see the discussion below under G. III. Investment strategies disclosure.

{15} Item 4(1) of Part B of Form 81-101F1 Contents of Simplified Prospectus (Form 81-101F1); Item 5.1(1) of Form 41-101F2.

{16} Item 3(1) of Part I of Form 81-101F3 Contents of Fund Facts Document (Form 81-101F3); Item 3(1) of Part I of Form 41-101F4 Information Required in an ETF Facts Document (Form 41-101F4).

{17} Instruction (3) to Item 4 of Part B of Form 81-101F1 states that if a particular investment strategy is a material aspect of the fund, as evidenced by the name of the fund or the manner in which it is marketed, this strategy must be disclosed as an investment objective. Similarly, Instruction (3) to Item 5 of Form 41-101F2 states that if a particular investment strategy is an essential aspect of the fund, as evidenced by the name of the fund or the manner in which it is marketed, this strategy must be disclosed as an investment objective

{18} Instruction (2) to Item 3 of Part I of Form 81-101F3; Instruction (2) to Item 3 of Part I of Form 41-101F4.

{19} Instruction (2) to Item 4 of Part B of Form 81-101F1 states that a mutual fund's fundamental investment objectives must indicate if the mutual fund primarily invests, or intends to primarily invest, or if its name implies that it will primarily invest, in a particular type of issuer or industry segment. Similarly, Instruction (2) to Item 5 of Form 41-101F2 states that if a fund primarily invests, or intends to primarily invest, or if its name implies that it will primarily invest, in a particular type of issuer or particular industry segment, the fundamental investment objectives should so indicate.

{20} Instruction (1) to Item 3 of Part I of Form 81-101F3; Instruction (1) to Item 3 of Form 41-101F4.

{21} Item 3(a) of Part B of Form 81-101F1.

{22} Instruction (2) to Item 3(a) of Part B of Form 81-101F1.

{23} Item 5(1)(a) and (b) of Part B of Form 81-101F1; Item 6.1(1)(a) and (c) of Form 41-101F2.

{24} However, staff's view is that such a focus should be clearly disclosed in the investment objectives and strategies disclosure; also see the discussion below under G. VI. Suitability.

{25} Staff also remind funds and their IFMs that index mutual funds are required to, as part of their fundamental investment objectives, (a) disclose the name or names of the permitted index or permitted indices on which the investments of the index mutual fund are based and (b) briefly describe the nature of that permitted index or those permitted indices, under Item 4(5) of Part B of Form 81-101F1.

{26} Item 30.1 of Form 41-101F2; Item 4.15(5) of Part A of Form 81-101F1; Item 12(7) of Form 81-101F2.

{27} Subsection 10.4(3) of National Instrument 81-106 Investment Fund Continuous Disclosure (NI 81-106).

{28} Item 9 of Part B of Form 81-101F1; Item 12 of Form 41-101F2.

{29} Instruction (2) to Item 9 of Part B of Form 81-101F1; Item 12.1(1) of Form 41-101F2.

{30} Item 7(1) of Part I of Form 81-101F3; Item 7(1) of Part I of Form 41-101F4.

{31} Instruction to Item 7 of Part I of Form 81-101F3; Instruction (1) to Item 7 of Part I of Form 41-101F4.

{32} Items 2.3(1) of Part B and 2.1 of Part C of Form 81-106F1 Contents of Annual and Interim Management Report of Fund Performance (Form 81-106F1).

{33} Item 1(d) of Part A of Form 81-106F1.

{34} Section 10.3 of NI 81-106.

{35} Section 10.4 of NI 81-106.

{36} Paragraph 15.2(1)(b) of NI 81-102.

{37} Paragraph 15.2(1)(a) of NI 81-102.

{38} Paragraph 13.1(1)1 of Companion Policy 81-102CP to National Instrument 81-102 Investment Funds (81-102CP).

{39} Subparagraph 13.1(1)3(b) of 81-102CP.

{40} OSC Staff Notice 81-720 Report on Staff's Continuous Disclosure Review of Sales Communications by Investment Funds.

{41} See, for example, subsection 15.3(1) and sections 15.7 and 15.7.1 of NI 81-102.

{42} See the definition of "member of the organization" in section 1.1 of National Instrument 81-105 Mutual Fund Sales Practices.

{43} Paragraph 5.1(1)(c) of NI 81-102.