OSC Staff Notice: 81-716 - Summary Report for Investment Fund Issuers

OSC Staff Notice: 81-716 - Summary Report for Investment Fund Issuers

OSC Staff Notice 81-716

2011 Summary Report for Investment Fund Issuers

Introduction

This report provides an overview of the key activities and initiatives of the Ontario Securities Commission for 2010/2011 that impact investment fund issuers and the fund industry, including:

• key policy initiatives,

• disclosure and compliance reviews, and

• recent developments in staff practices.

This report provides information about the status of some of the initiatives the OSC is undertaking to promote clear and concise disclosure in order to assist investors to make more informed investment decisions. The report also provides information about our work to address the sufficiency of regulatory coverage across all investment fund products. It highlights recent product and market developments, as well as our regulatory response to these developments, in order to assist the investment fund industry in understanding and complying with current regulatory requirements.

The OSC is responsible for overseeing over 3000 publicly-offered investment funds. Ontario based publicly-offered investment funds hold approximately 80% of the over $800 billion in publicly-offered investment fund assets in Canada.

We administer the regulatory framework for investment funds, including:

• reviewing and assessing product disclosure for all types of investment funds, including prospectuses and continuous disclosure filings,

• considering applications for discretionary relief from securities legislation and rules, and

• taking a leadership role in developing new rules and policies to adapt to the changing environment in the investment fund industry.

We also monitor and participate in investment fund regulatory developments globally, primarily through our work with the International Organization of Securities Commissions (IOSCO). OSC staff participation on IOSCO SC5 Investment Management technical committee informs both our operational and policy work. We discuss our participation with IOSCO further on our website at www.osc.ca at About the OSC -- Co-operation

The investment fund products we oversee include both conventional mutual funds and non-conventional investment funds. Non-conventional funds include non-redeemable investment funds such as closed-end funds, mutual funds listed and posted for trading on a stock exchange (ETFs), commodity pools, scholarship plans, labour-sponsored or venture capital funds and flow-through limited partnerships. We discuss the different types of funds further on our website at Investment Funds -- Fund Operations

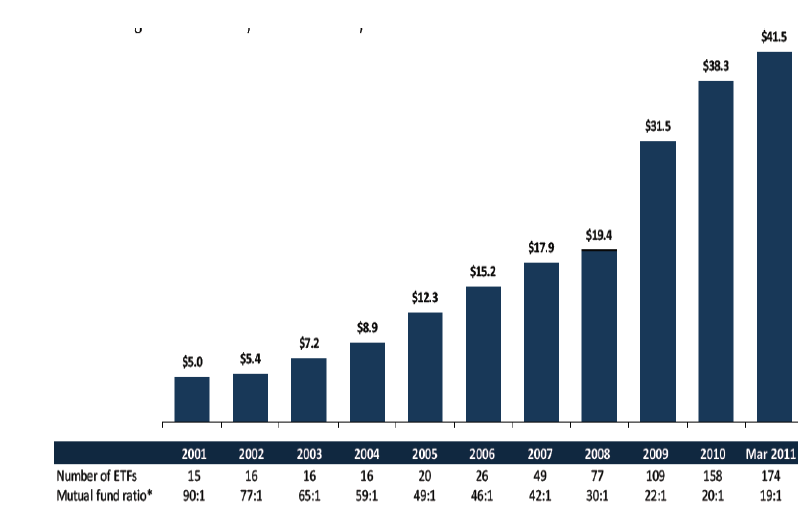

While non-conventional funds remain small relative to the conventional fund industry in terms of number and assets under management, they continue to grow at a faster rate than conventional funds. Offerings of non-conventional funds, particularly ETFs, continue to proliferate. In 2011, assets under management by ETF providers exceeded $40 billion for the first time.{1} As of June 2011 the number of exchange-traded products listed on the Toronto Stock Exchange (TSX) topped 200.{2} These products include 187 ETFs and 14 exchange-traded notes.{3} The number of listed ETF products on the TSX has more than doubled in the past two years, bringing the total market cap to approximately $49 billion.{4}

The closed-end fund industry has also recently seen renewed growth exceeding over $30 billion in assets under management for the first time since December 2007.{5}

As these and other non-conventional investment products, such as linked note derivative offerings, increase in number, the OSC will continue to assess and respond to product developments and innovations with a view to promoting investor protection and assessing the sufficiency and consistency of regulatory treatment of different investment fund products.

1. Key Policy Initiatives

The OSC continues to play a leading role in several significant policy initiatives with other securities regulators in Canada through the Canadian Securities Administrators (the CSA). This section reports on the status of significant policy initiatives including:

• the CSA's project to modernize investment fund product regulation, and

• the point of sale project.

We also report on other projects that impact investment funds and the fund industry including:

• National Instrument 41-101 -- General Prospectus Requirements, and

• OSC Staff Notice 81-715 -- Cross-listings by Foreign Exchange Traded Funds.

1.1 Modernization of Investment Fund Product Regulation

The modernization project's mandate is to review the regulation of publicly offered investment funds with a view to developing rules that recognize product developments and trends in the investment fund industry. The project is being carried out in two phases.

The first phase of this CSA initiative is proposed amendments to National Instrument 81-102 Mutual Funds (NI 81-102) and National Instrument 81-106 Investment Fund Continuous Disclosure (NI 81-106), which were published for comment on June 25, 2010. Phase 1 involves amending existing rules to update certain regulatory requirements for mutual funds in order to keep pace with market and product developments, particularly with respect to ETFs. The amendments also introduce new liquidity and term restrictions on money market fund holdings. The comment period for these proposals expired on September 24, 2010 and 24 comment letters were received. The CSA have reviewed and considered all of the comments and expect to publish final amendments for this first phase of the project by the end of 2011.

On May 26, 2011, the CSA published CSA Staff Notice 81-322 -- Status Report on the Implementation of the Modernization of Investment Fund Product Regulation Project and Request for Comment on Phase 2 Proposals (the Notice). The Notice provides an update on the status of the Modernization project generally, including an anticipated timeline for the stages of the project. It also seeks specific feedback from investors and industry stakeholders on the CSA's proposal to focus next on developing an operational rule for non-redeemable investment funds. This second phase of the initiative aims to introduce certain core investment restrictions and operational requirements for non-redeemable investment funds that are analogous to those applicable to mutual funds under NI 81-102. The purpose of Phase 2 would be to address investor protection and fairness concerns the CSA have identified. The CSA's goal in making these proposals is to achieve more consistent, fair and functional regulation across the investment fund product spectrum.

The comment period on the Phase 2 proposal discussed in the Notice expired on July 25, 2011. The CSA continue to review and consider all the comments received and aim to publish a proposed rule for comment in 2012.

1.2 Point of Sale (POS)

On August 12, 2011, the CSA published proposed amendments to NI 81-101 Mutual Fund Prospectus Disclosure (NI 81-101) that set out Stage 2 of the CSA's implementation of the POS disclosure initiative for mutual funds. You can find out more about the CSA's decision to proceed with a staged implementation of the POS project in CSA Staff Notice 81-319 Status Report on the Implementation of Point of Sale Disclosure for Mutual Funds (the Staff Notice).

The Fund Facts document is central to the POS disclosure project. The CSA designed the Fund Facts to make it easier for investors to find and use key information, including past performance, risks and the costs of investing in a mutual fund. The document provides investors with key information about the mutual fund, followed by a concise explanation of its expenses and fees, adviser compensation and the investor's rights. Stage 1, which came into force January 1, 2011, requires a mutual fund to produce and file the Fund Facts and for it to be available on the mutual fund's or mutual fund manager's website.

The Stage 2 proposed amendments will require delivery of the Fund Facts within two days of buying a mutual fund. The proposed amendments will also permit delivery of the Fund Facts to satisfy the current prospectus delivery requirements under securities legislation. Although delivery of the simplified prospectus will no longer be required, it must continue to be available to investors upon request.

On February 24, 2011, we published CSA Staff Notice 81-321 Early Use of the Fund Facts to Satisfy Prospectus Delivery Requirements, which provides guidance on the key terms and conditions that the CSA will look for when considering applications for exemptive relief to permit the early use of the Fund Facts to satisfy delivery while Stage 2 is underway.

Once the CSA has completed its review and consideration of the issues related to point of sale delivery for mutual funds, in Stage 3 the CSA will publish for further comment any proposed requirements that would implement point of sale delivery for mutual funds. As part of Stage 3, we will also consider point of sale delivery for other types of publicly offered investment funds.

1.3 National Instrument 41-101 -- General Prospectus Requirements

The CSA published proposed amendments to NI 41-101 on July 15, 2011. The purpose of the amendments is to enhance the effectiveness of prospectus disclosure standards, clarify the requirements, address significant identified gaps, and eliminate or modify ineffective or unduly burdensome requirements. The amendments are based on CSA experience with the rule to date, feedback from the public and requests for relief from issuers.

Key amendments that impact investment funds include:

• A specific requirement to describe maximum and minimum amounts of leverage through use of derivatives,

• A new requirement to disclose trading expense ratio,

• Expansion of the disclosure requirement concerning ownership interests in a fund and the manager, and

• A requirement for management to disclose bankruptcies and cease trade orders in respect of all issuers (not just investment fund issuers).

1.4 OSC Staff Notice 81-715 -- Cross-listings by Foreign Exchange Traded Funds

We published OSC Staff Notice 81-715 on August 26, 2011 in response to inquiries we have received in recent years from U.S. based ETFs. The notice sets out OSC staff's view regarding the applicable securities regulatory requirements in connection with potential cross-listings by U.S. based ETFs.

The notice confirms staff's view that a cross-listing by a foreign based ETF would generally be a distribution in Ontario and, consequently, that foreign ETF providers must file a prospectus to qualify their securities and comply with product regulation in Ontario before applying to cross-list on an exchange in Ontario. The notice further confirms staff's view that foreign providers of other products that are comparable to ETFs and use a similar distribution structure to ETFs, such as some exchange traded notes (ETNs), must also file a prospectus before applying to cross-list their securities on an exchange in Ontario.

2. Disclosure and Compliance Reviews

On an ongoing basis, OSC staff review the prospectus and continuous disclosure filings of Ontario-based investment funds. Risk-based criteria are used to select investment funds for reviews of their disclosure documents. We may also choose to conduct targeted reviews of a particular industry segment or on a particular topic. In addition to our prospectus and continuous disclosure reviews, the Investment Funds (IF) Branch works closely with staff in the Compliance and Registrant Regulation (CRR) Branch on issues related to fund manager compliance and identifying possible emerging issues. This can sometimes lead to us conducting joint reviews.

This section discusses some observations, findings and themes from:

• our prospectus reviews of non-redeemable investment funds and ETFs,

• our prospectus reviews of hypothetical pro-forma performance data,

• our focused continuous disclosure reviews of money market funds, ETFs and investment portfolio holdings, and

• our focused disclosure reviews of Independent Review Committees.

2.1 Non-redeemable Investment Funds

We reviewed a high number of prospectuses for non-redeemable investment funds as a result of the renewed growth in this industry segment over the past year. These funds are non-conventional investment funds, and are often referred to as closed-end funds. They are generally not redeemable on demand for net asset value and list their securities for trading on an exchange. In addition, they are generally not in continuous distribution, relying on cash from limited underwritten offerings to acquire their initial assets.

We will continue to monitor developments in this industry through our prospectus reviews with a view to informing what regulatory changes may be appropriate in connection with Phase 2 of our Modernization project discussed above.

2.1.1 OSC Staff Notice 81-711 Closed-end Investment Fund Conversions to Open-end Mutual Funds

We published OSC Staff Notice 81-711 on October 29, 2010, in response to the increasing use of a built-in conversion feature by which a closed-end fund converts to an open-end mutual fund.

Closed-end fund securities typically trade on an exchange, but often at a discount to their net asset value (NAV). Historically, the industry has attempted to manage this discount by providing investors with an annual redemption right at NAV. The annual redemption right has resulted in significant redemptions and early fund terminations in some instances. A key objective of the conversion feature is to provide investors in the closed-end fund with enhanced liquidity through a more frequent redemption feature at NAV after the fund converts to an open-end mutual fund.

The notice sets out the views of OSC staff on the regulatory issues related to closed-end fund conversions and the types of comments staff will generally raise in the course of a review of a built-in conversion feature. As discussed in the notice, we have focused on whether the funds continue to have the same or substantially similar investment objectives, strategies and fees before and after the conversion. We have generally taken the view that these products should be compliant with the regulatory requirements applicable to conventional mutual funds from inception if they intend to convert to a mutual fund within a relatively short timeframe. Our prospectus reviews have focused on key areas of disclosure such as:

• the potential that these products will trade at a discount to NAV up to the time of conversion,

• fees payable by investors both before and after the fund converts to a mutual fund,

• the risks associated with the conversion, and

• performance disclosure for periods before and after conversion.

2.1.2 Long-term Warrant Offerings

We noted a continued resurgence in the use of long-term warrant offerings by closed-end funds. These offerings appear unique to closed-end funds that rely on them to replenish their asset base after experiencing redemptions at an annual redemption date. We discussed these offerings previously in last year's branch report and the OSC Investment Funds Practitioner. Our concerns relate primarily to prospectus delivery on exercise of the warrants and dilution.

OSC staff continue to raise comments on long-term warrant offerings with a view to:

• promoting the disclosure of any unique risks, such as dilution,

• confirming that the investor that pays the subscription price receives a prospectus, and

• better understanding the use of this method of capital raising for investment funds.

2.2 OSC Staff Notice 81-714 Compliance with Form 41-101F2 -- Information Required in an Investment Fund Prospectus

We published OSC Staff Notice 81-714 on March 4, 2011, in response to the increasing number of closed-end fund prospectuses that were not complying with the Form 41-101F2 requirements relating to the use of plain language, brevity and the ordering of information and use of headings. In particular, we noted that closed-end funds were providing increasing amounts of information on the cover page and in the summary of their prospectuses.

The Notice sets out the types of comments staff will generally raise as part of our reviews to encourage presentation to investors of information about the investment fund in a clear, concise and comparable format that assists them in making informed investment decisions. For example, IF staff may ask that cover page disclosure be reduced or request that certain disclosure be removed. In instances where the investment fund has complex or unique risks, features or costs, staff ask for additional, tailored disclosure that is specific to the securities to be distributed. The disclosure should be added to the cover page or the prospectus summary disclosure so that investors are provided with full, true and plain disclosure of all material facts. Staff may also ask the fund or its fund manager to include a plainly worded, brief warning presented in bold type or in text boxes.

The Notice also states that OSC staff will raise comments when the investment objective does not clearly set out the fundamental features of the investment fund that distinguish it from other funds. In addition, it sets out staff's view that the number of investment funds offered in a single long form prospectus should be limited to those investment funds with substantially similar investment objectives, strategies and features, with a view to facilitating full, true and plain disclosure to investors.

2.3 Exchange-traded Funds and Index Participation Units

We note that over the past few years there has been a proliferation in the number of product offerings from index providers. We also recognize that there is an interest on the part of ETF providers to differentiate themselves in the market by branching out beyond the traditional indices. Staff are of the view that the term "market index" should be interpreted in a manner that is consistent with the investment restrictions set out in NI 81-102.

We have been raising comments on some ETF prospectuses where the ETF describes its securities as being index participation units (IPUs) under NI 81-102 in instances where they did not appear to be tracking a market index as contemplated under NI 81-102 because:

• the index provides exposure to asset classes or strategies that a mutual fund would not be able to engage in directly,

• the index tracks the price of a commodity,

• the index purports to track the performance of hedge funds, real property, or incorporates leverage or shorting strategies,

• the index is designed to terminate at a specified time, and

• the index is overly concentrated in a few issuers.

We also discussed market indices and IPUs in the May, 2011 edition of the Investment Funds Practitioner.

2.4 Hypothetical Pro-forma Performance Data

We continue to raise comments regarding the use of hypothetical pro-forma performance data by all investment funds and other products such as linked notes. We have discussed the use of performance data and yield disclosure in offering documents previously in the November 30, 2007 and January 8, 2010 editions of the Investment Funds Practitioner. Our CRR Branch, along with the CSA, also published CSA Staff Notice 31-325 -- Marketing Practices of Portfolio Managers on July 8, 2011. The notice discusses some of the concerns with the use of hypothetical performance data including that many investors may not have sophisticated investment knowledge sufficient to fully understand its inherent risks and limitations. In order to address this concern, we generally request the removal of hypothetical pro-forma performance data disclosure.

2.5 Continuous Disclosure Reviews

The IF Branch continued our continuous disclosure review program this year by applying risk based criteria to select investment funds for reviews of their disclosure documents. We also conducted targeted reviews of particular industry segments and topics. This section discusses some of our reviews and findings in connection with:

• money market funds,

• ETFs,

• investment portfolio holdings, and

• fund facts risk rankings.

2.5.1 Money Market Funds

In response to recent global regulatory developments related to money market funds and to further inform our own CSA proposals (see Modernization of Investment Fund Product Regulation above), we commenced a targeted review of money market funds focused on their risk and liquidity profiles. We anticipate the reviews will provide us with a better understanding of the makeup of the industry's capitalization (i.e. retail vs. institutional), redemption experience, and any differences between the different types of money market funds (e.g. Premium and T-Bill). The reviews will also look at differences in exposure between money market funds offered in Canadian and U.S. currencies.

To this point, the reviews have provided OSC staff with some initial insights on how the Canadian money market industry competes and how money market funds are dealing with various market risks, including sovereign default risks in Greece and their potential effect on short term paper issued by European banks and businesses. We also used the reviews to quickly assess the potential exposure of Canadian and U.S. money market funds to potential U.S. government debt defaults in the event the debt ceiling issue was not resolved in the U.S.

2.5.2 ETFs

In response to the continued growth of the ETF industry and the growing complexity of ETF products, we completed targeted reviews of ETFs. The reviews were primarily focused on the valuation of illiquid assets and the use of proprietary derivatives, such as forwards. We reviewed a total of 40 ETFs from 11 fund managers, which represent approximately 70% of the ETF industry.

We will continue to monitor developments in this industry through our prospectus reviews with a view to informing what regulatory changes or guidance may be appropriate in connection with the Modernization project discussed above.

2.5.3 Investment Portfolio Holdings

We are currently engaged in a focused review of the investment portfolio holdings disclosed in the management reports of fund performance (MRFPs), financial statements and in the Fund Facts. As part of this focused review, staff intend to examine: (1) whether the summarized investment portfolio in the MRFP and Fund Facts provides information classified into appropriate sub-groups and provides meaningful information to investors about the fund's portfolio, and (2) whether the investment portfolio in the financial statements provides sufficiently organized information for investors to assess consistency and performance against the fund's stated investment objectives and strategies.

Our review is intended to examine how closely a fund's stated investment objectives and strategies are implemented over time. Following the review, we will consider providing guidance around the presentation of a fund's investment portfolio disclosure and how the fund's discussion of its investment strategy can be updated and improved based on how the fund has been investing. We anticipate completing the review by fall, 2011.

2.5.4 Fund Facts Risk Ranking Reviews

We also currently have under way a focused review of the investment risk classification methodology in the simplified prospectus. Following amendments to the simplified prospectus form which added a requirement to describe the methodology by which the fund manager identifies the investment risk level of a mutual fund, we have noticed that such disclosure in the simplified prospectus may be overly brief. As part of this focused review, staff are asking for a copy of the methodology which the manager is required to make available to investors, in order to assess: (1) whether the prospectus disclosure is adequate; and (2) whether the investment risk classifications in the simplified prospectus and Fund Facts documents seem to be appropriate.

2.6 OSC Staff Notice 81-713 Focused Disclosure Review National Instrument 81-107 Independent Review Committee for Investment Funds

As discussed in last year's annual report, the IF Branch completed targeted reviews of NI 81-107 related disclosure. We reported our findings in OSC Staff Notice 81-713 which we published on March 25, 2011.

3. Outreach and Consultation

We continue our efforts to be transparent regarding practices and procedures that impact investment fund issuers in as timely a manner as possible. Our intent in doing so is to better enable fund managers and their advisors to avoid potential regulatory issues when they are at the planning stage for a new fund or transaction.

3.1 Investment Funds Product Advisory Committee (IFPAC)

The OSC announced the members of our first ever Investment Funds Product Advisory Committee on August 11, 2011.

In an environment of rapid product growth and increasing complexity of investment fund products, we recognize the unique perspective that market participants, particularly product manufacturers and portfolio advisors, may have in identifying and anticipating market and product trends.

The IFPAC will advise OSC staff specifically on emerging product developments and innovations occurring in the investment fund industry. The committee will discuss the impact of these developments and emerging issues. The IFPAC may also act as one source of feedback to OSC staff on the development of policy and rule-making initiatives to promote investor protection, fairness and market efficiency across all types of publicly offered investment fund products.

The initial IFPAC members are:

|

Ghassan (Jason) Agaby |

Dynamic Funds |

|

Tom Bradley |

Steadyhand Investment Funds |

|

Darren Farkas |

Fidelity Investments Canada ULC |

|

Adam Felesky |

Horizons Exchange Traded Funds (ETFs) |

|

Goshka Folda |

Investor Economics |

|

Kevin Gopaul |

BMO Asset Management |

|

Ed Jackson |

RBC Capital Markets |

|

Oliver McMahon |

Blackrock Asset Management Canada |

|

Marian Passmore |

Canadian Foundation for Advancement of Investor Rights |

|

Jeff Ray |

Manulife Investments |

|

Mary Taylor |

Mackenzie Investment |

|

Mark Yamada |

PUR Investing Inc. |

IFPAC members will serve a two year term. IFPAC will meet quarterly and be chaired initially by Rhonda Goldberg, Director of the Investment Funds Branch.

In addition to IFPAC, OSC staff continue to meet frequently with stakeholders, including investment fund managers and their advisors, investor advocates and subject matter experts on various topics to inform our policy and operational work. For example, in July, 2011 we brought together a range of product specialists, which included ETF manufacturers, asset managers on both the buy and sell side as well as academics to discuss with OSC staff the use of derivatives and synthetic ETFs.

3.2 The OSC Investment Funds Practitioner

The Practitioner is an overview of recent issues arising from applications for discretionary relief, prospectuses and continuous disclosure documents that investment funds file with the OSC and that are reviewed by the IF Branch. It is intended to assist investment fund managers and their advisors who regularly prepare public disclosure documents and applications for exemptive relief on behalf of investment funds.

The Practitioner is also intended to make fund managers more broadly aware of some of the issues we have raised in connection with our reviews and how we have resolved them. The Practitioner can be found on our website www.osc.gov.on.ca at Information for Investment Funds.

In May, we published the fifth edition of the Investment Funds Practitioner. Topics included:

• Requirements to Calculate Daily NAV

• Split Shares -- Relief from s. 119 of the Act

• Split Shares -- Secondary Offerings

• Forward Agreement Fee Disclosure

• PIFs for CCO

• Short Form Prospectus Eligibility

• Relief from 90-Day Prospectus Filing Requirement

• Definition of Index Participation Unit

• Point of Sale FAQs

We intend to publish the sixth edition of the Investment Funds Practitioner this fiscal year. We welcome suggestions for future topics.

4. Feedback and Contact Information

If you have any questions regarding, or feedback on, our second Annual Report, please send them to [email protected].

You can find additional information regarding investment funds and the IF Branch on our website.

We have also attached a list of IF Branch staff at the end of this report.

INVESTMENT FUNDS BRANCH

|

NAME |

|

|

|

|

|

Goldberg, Rhonda --Director |

|

|

|

|

|

Chan, Raymond -- Manager |

|

|

|

|

|

McKall, Darren --Manager |

|

|

|

|

|

Nunes, Vera --Manager |

|

|

|

|

|

Alamsjah, Rosni -- Administrative Assistant |

|

|

|

|

|

Asadi, Mostafa -- Legal Counsel |

|

|

|

|

|

Bahuguna, Shaill -- Database Clerk |

|

|

|

|

|

Barker, Stacey -- Senior Accountant |

|

|

|

|

|

Bent, Christopher -- Legal Counsel |

|

|

|

|

|

Buenaflor, Eric -- Financial Examiner |

|

|

|

|

|

De Leon, Joan -- Review Officer |

|

|

|

|

|

Follegot, Daniela -- Legal Counsel |

|

|

|

|

|

Fuller, Patricia -- Administrative Assistant |

|

|

|

|

|

Gerra, Frederick -- Legal Counsel |

|

|

|

|

|

Huang, Pei-Ching -- Senior Legal Counsel |

|

|

|

|

|

Joshi, Meenu -- Accountant |

|

|

|

|

|

Kearsey, Ian -- Legal Counsel |

|

|

|

|

|

Kwan, Carina -- Legal Counsel |

|

|

|

|

|

Lee, Irene -- Legal Counsel |

|

|

|

|

|

Leonardo, Tracey -- Administrative Assistant |

|

|

|

|

|

Mainville, Chantal -- Senior Legal Counsel |

|

|

|

|

|

Nandacumar, Parbatee -- Administrative Assistant |

|

|

|

|

|

Nania, Viraf -- Senior Accountant |

|

|

|

|

|

Oseni, Sarah -- Senior Legal Counsel |

|

|

|

|

|

Paglia, Stephen -- Senior Legal Counsel |

|

|

|

|

|

Park, Rose -- Legal Counsel |

|

|

|

|

|

Persaud, Violet -- Review Officer |

|

|

|

|

|

Russo, Nicole -- Review Officer |

|

|

|

|

|

Schofield, Melissa -- Senior Legal Counsel |

|

|

|

|

|

Thomas, Susan -- Senior Legal Counsel |

|

|

|

|

|

Welsh, Doug -- Senior Legal Counsel |

|

|

|

|

|

Yu, Sovener -- Accountant |

|

|

|

|

|

Zaman, Abid -- Accountant |

|

{1} Investor Economics ETF and Index Funds Report First Quarter 2011

{2} TSX News Release June 1, 2011

{3} TSX News Release June 1, 2011

{4} TSX News Release June 1, 2011

{5} Investor Economics Insight Monthly Update May 2011