Summary Report for Investment Fund and Structured Product Issuers - 2014

Summary Report for Investment Fund and Structured Product Issuers - 2014

Summary Report for Investment Fund and Structured Product Issuers - 2014

Investment Funds & Structured Products Branch

February 18, 2015

Table of Contents

|

Introduction |

1 |

||

|

|

|||

|

1. |

Key Policy Initiatives |

6 |

|

|

1.1 |

|

Mutual Fund Fees |

6 |

|

1.2 |

|

Pre-Sale Delivery for Mutual Funds, Risk Classification Methodology for Fund Facts, and Summary Disclosure for ETFs |

7 |

|

1.3 |

|

Accredited Investor Exemption for Investment Funds |

8 |

|

1.4 |

|

Amendment to Securities Act (Ontario) Relating to Insider Trading and Self-Dealing |

8 |

|

|

|||

|

2. |

Emerging Issues and Trends |

11 |

|

|

2.1 |

|

Update on Linked Note Offerings |

11 |

|

2.2 |

|

Mutual Fund Distributions in Deferred or Low Load Sales Charge Series |

11 |

|

2.3 |

|

Fee-Based Series with Dual Dealer Compensation |

12 |

|

2.4 |

|

Changes to Short Term Trading Fees |

13 |

|

|

|||

|

3. |

Disclosure and Compliance Reviews |

16 |

|

|

3.1 |

|

Continuous Disclosure Reviews |

16 |

|

3.2 |

|

Compliance and Registrant Regulation Branch and Investment Fund Manager Compliance Reviews |

19 |

|

|

|||

|

4. |

Outreach, Consultation and Education |

22 |

|

|

4.1 |

|

Investment Funds Product Advisory Committee (IFPAC) |

23 |

|

4.2 |

|

The Investment Funds Practitioner |

23 |

|

4.3 |

|

International Organization of Securities Commissions -- Committee 5 -- Investment Management (IOSCO C5) |

24 |

|

|

|||

|

5. |

Feedback and Contact Information |

26 |

|

Introduction

This, our fifth annual Summary Report for Investment Fund and Structured Product Issuers, provides an overview of the key activities and initiatives of the Ontario Securities Commission for 2014 that impact investment fund and structured product issuers and the fund industry, including:

• key policy initiatives,

• emerging issues and trends,

• continuous disclosure and compliance reviews, and

• recent developments in staff practices.

This report provides information about the status of some of the initiatives the OSC is undertaking to promote clear and concise disclosure in order to assist investors to make more informed investment decisions, as well as our work to address the sufficiency of regulatory coverage across all investment fund products. It also highlights recent product and market developments, and our regulatory response to these developments, in order to assist the investment management industry in understanding and complying with current regulatory requirements.

The OSC is responsible for overseeing over 3,700 publicly-offered investment funds. Ontario-based publicly-offered investment funds hold approximately 80% of the just over $1.2 trillion in publicly-offered investment fund assets in Canada.

We administer the regulatory framework for investment funds, including:

• reviewing and assessing product disclosure for all types of investment funds, including prospectuses and continuous disclosure filings,

• considering applications for discretionary relief from securities legislation and rules, and

• taking a leadership role in developing new rules and policies to adapt to the changing environment in the investment fund industry.

We also monitor and participate in investment fund regulatory developments globally, primarily through our work with the International Organization of Securities Commissions (IOSCO). OSC staff participation on the IOSCO C5 Investment Management Committee informs our operational and policy work. In this report, we highlight some of the recent work by IOSCO C5 that we think will be of interest to investment fund issuers.

Over the last few years there has been an increase in the number and types of structured products that are sold to retail investors. In order to better reflect the expansion of these product offerings in the market and the work of the branch, the OSC Investment Funds branch formally changed its name to Investment Funds and Structured Products, effective May 26, 2014. The name change was also intended to signal that the OSC will treat comparable products sold to retail investors in a consistent way, despite their respective technical definitions in the Securities Act (Ontario). In this regard, amendments to National Instrument 81-102 Investment Funds (NI 81-102), which came into force in September 2014, introduce core investment and operational requirements for publicly offered non-redeemable investment funds. The title of NI 81-102 changed from Mutual Funds to Investment Funds to reflect the broader application of the national instrument.

The investment fund products we oversee include both conventional mutual funds and non-conventional investment funds. Non-conventional funds include non-redeemable investment funds such as closed-end funds, mutual funds listed and posted for trading on a stock exchange (ETFs), commodity pools, scholarship plans, labour-sponsored or venture capital funds and flow-through limited partnerships. We discuss the different types of funds further on our website at www.osc.gov.on.ca Investment Funds -- Fund Operations.

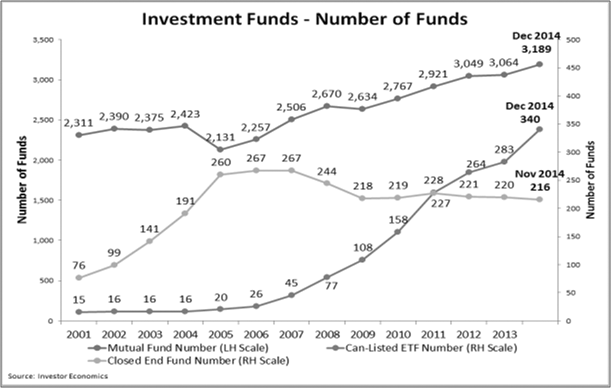

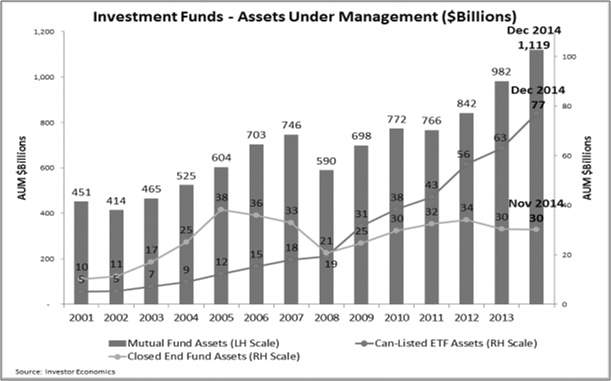

The ETF market has continued to grow steadily over the last few years. As at the end of December 2014, there were 340 ETFs in Canada with assets of approximately $77 billion. In comparison, as at December 2013, there were 283 ETFs with assets of approximately $63 billion, representing an increase in assets of approximately 22%. Over the same period, conventional fund assets increased approximately $137 billion, or by around 14%, with total assets as at December 2014 of approximately $1.1 trillion. As at November 2014, closed-end fund assets remained unchanged from the previous December, at approximately $30 billion.

As these and other investment and structured products increase in number, and as the use of ETFs by retail investors continues to grow, the OSC will continue to assess and respond to product developments and innovations with a view to promoting investor protection and assessing the sufficiency and consistency of the regulatory treatment of different investment fund products.

1. Key Policy Initiatives

1.1

Mutual Fund Fees

1.2

Pre-Sale Delivery for Mutual Funds, Risk Classification Methodology for Fund Facts, and Summary Disclosure for ETFs

1.3

Accredited Investor Exemption for Investment Funds

1.4

Amendment to Securities Act (Ontario) Relating to Insider Trading and Self-Dealing

The OSC continues to play a leading role in several significant policy initiatives with other securities regulators in Canada through the Canadian Securities Administrators (the CSA). This section reports on the status of significant policy initiatives including:

• mutual fund fees

• pre-sale delivery for mutual funds, risk classification methodology for Fund Facts, and summary disclosure for ETFs

• accredited investor exemption for investment funds

This section also highlights the recent change to the Securities Act (Ontario) relating to investment fund insider trading and self-dealing.

1.1 Mutual Fund Fees

In February 2014, in order to advance a policy decision on mutual fund fees, the CSA decided to undertake third-party research that would help determine the extent to which embedded advisor compensation and other forms of tied compensation influence advisor behaviour and impact investor outcomes.

This work followed stakeholder consultations, held by the CSA, in the summer and fall of 2013 to further the discussion of the issues raised in CSA Discussion Paper and Request for Comment 81-407 Mutual Fund Fees (the Fund Fees Paper). The themes that emerged from these earlier consultations were set out in CSA Staff Notice 81-323 Status Report on Consultation under CSA Discussion Paper and Request for Comment 81-407 Mutual Fund Fees published in December, 2013.

In April 2014, CSA staff invited the submission of proposals for two independent pieces of research to evaluate the extent, if any, to which: (i) sales and trailing commissions influence fund sales, and (ii) the use of fee-based vs. commission-based compensation changes the nature of advice and investment outcomes over the long term.

The request for proposals resulted in the hiring of Douglas J. Cumming, Professor of Finance and Entrepreneurship at the Schulich School of Business, York University, to conduct the first piece of research, and The Brondesbury Group to conduct the second piece of research. While Professor Cumming's research requires the review and analysis of specific mutual fund data, The Brondesbury Group's research consists of the review of the relevant literature.

In November 2014, Professor Cumming sent requests for specific data to all investment fund managers offering public mutual funds across Canada, asking them to respond to the data request by January, 2015.

The Brondesbury Group's and Professor Cumming's final research reports are expected to be published in the spring of 2015, which will be key inputs to CSA staff deliberations on policy recommendations. Individual funds and individual fund company information will not be identified in either report.

1.2 Pre-Sale Delivery for Mutual Funds, Risk Classification Methodology for Fund Facts, and Summary Disclosure for ETFs

On December 11, 2014, Stage 3 of the Point of Sale (POS) disclosure initiative was completed with the publication of final amendments to implement pre-sale delivery of Fund Facts for mutual funds. Under current securities legislation, a Fund Facts is required to be delivered to investors within two days of buying a mutual fund. The Amendments change the timing of delivery by requiring delivery of the most recently filed Fund Facts to a purchaser before a dealer accepts an instruction for the purchase of a mutual fund. The requirement for pre-sale delivery of Fund Facts takes effect on May 30, 2016.

The CSA is proceeding with 2 remaining work streams as part of the POS disclosure initiative: (i) the development of a CSA mutual fund risk classification methodology, and (ii) the development of a summary disclosure document for ETFs, similar to the Fund Facts, and a requirement to deliver the summary disclosure document within two days of an investor buying an ETF.

(i) Development of a CSA mutual fund risk classification methodology

The CSA published CSA Notice 81-324 and Request for Comments Proposed CSA Mutual Fund Risk Classification Methodology for Use in Fund Facts, which set out a proposed risk classification methodology (the Proposed Methodology) to be used to calculate and disclose a fund's volatility risk on the risk scale in the Fund Facts document. Prior to publication, the CSA held consultations with industry representatives, academics and investor advocates to seek feedback on the CSA's proposed risk classification methodology. The comment period ended on March 12, 2014.

The CSA received 56 comment letters in response to the Proposed Methodology which addressed a number of aspects of the Proposed Methodology including, but not limited to, the metric chosen to calculate volatility risk, the performance time period to be used, and the proposal to move from a five category scale to a six category scale in the Fund Facts document. The comment letters can be found on our website.

On January 29, 2015, CSA staff published CSA Staff Notice 81-325 Status Report on Consultation under CSA Notice 81-324 and Request for Comment on Proposed CSA Mutual Fund Risk Classification Methodology for Use in Fund Facts which provided an update on the status of this work stream and outlined the key themes that arose from the comments on the Proposed Methodology.

Later in 2015, the CSA aims to publish for comment proposed rule amendments that implement a standardized risk classification methodology. A more detailed summary of comments received in response to CSA Notice 81-324, along with CSA responses to those comments, will also be published at that time.

(ii) Development of a summary disclosure document for ETFs

Investor focus-testing of a draft summary disclosure document for ETFs was completed in fall 2014. The draft summary disclosure document for ETFs is based on the Fund Facts, with modifications to reflect the specific attributes of ETFs. The CSA expect to publish for comment proposed amendments mandating the form of a summary disclosure document for ETFs as well as requiring its delivery within two days of buying an ETF, in spring or early summer 2015. The proposed amendments codify exemptive relief orders granted by the CSA which took effect on September 1, 2013 and cover all ETF manufacturers and bank-owned dealers, which account for approximately 80% of all ETF trades.

1.3 Accredited Investor Exemption for Investment Funds

As part of the OSC's broader exempt market initiative, we are amending the accredited investor exemption to permit fully managed accounts, where the adviser has a fiduciary relationship with the investor, to purchase any securities on an exempt basis, including investment fund securities. Currently, in Ontario, investment funds are carved out of the managed account category of the accredited investor exemption. Removing the carve-out would harmonize the managed account category of the accredited investor exemption in all Canadian jurisdictions. In February 2014, the CSA published for comment amendments to the review of accredited investor and minimum amount exemptions. We expect final publication in February 2015, and this amendment to come into effect, subject to Ministerial approval, in spring 2015.

1.4 Amendment to Securities Act (Ontario) Relating to Insider Trading and Self-Dealing

Part XXI of the Act, Insider Trading and Self-Dealing, contains conflict of interest investment restrictions which, until July 24, 2014, only applied to mutual funds. In July 2014, Part XXI of the Act was amended to extend the conflict of interest investment restrictions to all investment funds, so that they apply to non-redeemable investment funds and mutual funds.

After the Act was amended on July 24, 2014, some questions arose about the application of Part XXI to non-redeemable investment funds, and about the impact of the amendments on the existing requirements for mutual funds. Staff responded to these questions by setting out its views in OSC Staff Notice 81-725 Recent Amendments to Part XXI Insider Trading and Self-Dealing of the Securities Act (Ontario) -- Transition Issues on August 7, 2014. In particular, staff provided guidance on the interaction between Part XXI of the Act and the Modernization amendments to NI 81-102 that came into force in September 2014.

2. Emerging Issues and Trends

2.1

Update on Linked Note Offerings

2.2

Mutual Fund Distributions in Deferred or Low Load Sales Charge Series

2.3

Fee-Based Series with Dual Dealer Compensation

2.4

Changes to Short Term Trading Fees

2.1 Update on Linked Note Offerings

The OSC reviews novel linked note supplements filed for pre-clearance under National Instrument 44-102 Shelf Distributions and CSA Staff Notice 44-304 Linked Notes Distributed under the Shelf Prospectus System (SN 44-304).

In January 2015, the CSA published CSA Staff Notice 44-305 Structured Notes Distributed under the Shelf Prospectus System (SN 44-305). SN 44-305 updates and supplements the CSA's views from SN 44-304 regarding disclosure and other issues that issuers should consider when structuring and administering their note programs.

Key topics covered in SN 44-305 include:

• The disclosure of the issuer's estimate of the note's fair value with a view to improving transparency regarding the estimated profit that may be embedded into the note.

• Disclosure issuers should consider providing to investors on an on-going basis.

• Our views regarding the use of investment funds and managed portfolios as reference assets.

• Reminders of and updates to the process to be followed when filing structured note pricing supplements.

OSC staff will continue to review structured notes filed for pre-clearance and monitor the development of the structured note industry generally. We will continue to consider what gaps may exist under our regulatory approach to structured notes and whether more formal regulatory requirements may become necessary to ensure we are regulating like products in a consistent way to achieve investor protection and fair and efficient capital markets. In the interim, the CSA will continue to provide updates regarding our views, concerns or initiatives in connection with structured notes, as necessary.

2.2 Mutual Fund Distributions in Deferred or Low Load Sales Charge Series

In the course of our prospectus reviews, we are placing a greater emphasis on the various practices that currently exist for mutual funds regarding distributions paid in the form of reinvested units instead of cash. More specifically, we are focused on funds that are designed to pay regular distributions. Of particular concern are those mutual funds that set the payment of distributions in the form of reinvested units as the default option, if investors do not specifically request distributions in cash.

Staff's view is that where a choice to receive distributions in cash or in reinvested units is available, a fund manager should ensure that an investor has, in fact, made that election, rather than proceeding with a default option in the absence of instructions. This is particularly so where that default option could result in additional fees being paid by an investor. For example, if a fund is purchased under a deferred sales charge (DSC), fees may be payable on redemption of those reinvested units, whereas no fees would apply to cash distributions.

Staff's emphasis is part of a larger focus on the more general use by the mutual fund industry of default options, in the absence of receiving instructions from investors. We are concerned that these default options could interfere with the client/advisor relationship since they permit transactions to proceed whether or not investors have been able to discuss and understand their options with their advisor. In addition, there is a concern with potential conflicts of interest associated with distributions being automatically reinvested in additional units. This distribution option arguably benefits the fund manager and the advisor more than cash distributions, since assets that remain in the fund would attract additional management fees and trailing commissions, as applicable.

We expect to continue to review fund distribution policies generally, with a particular emphasis on those mutual funds that seek to make regular distributions. Our reviews will include examining default options and the differing treatment of reinvested distributions versus cash with respect to redemption fees payable in a DSC series. For existing funds, this may result in a request for enhanced disclosure in the prospectus or the Fund Facts. We also expect to seek feedback from fund managers with respect to a reasonable time period to transition towards the removal of any default options, as well as the steps involved in doing so.

We may provide further guidance as we continue to review this issue. Filers should note, however, that in light of the foregoing concerns, we will closely examine and question any new funds being launched that have a default feature that causes distributions to be automatically reinvested in additional units of the fund. Filers and their counsel are encouraged to contact staff in the planning stages of a new fund structure that gives rise to questions relating to the issues identified above.

2.3 Fee-Based Series with Dual Dealer Compensation

During the year, staff became aware of certain investment fund series intended for fee-based accounts that had a trailing commission embedded in the ongoing cost of the fund series.

In staff's view, a series intended for fee-based accounts with this type of dual compensation structure is inconsistent with a critical attribute of the fee-based series, namely the negotiation of the dealer's compensation, which is intended to provide investors with heightened transparency of the cost of the dealer's services and a clear expectation of the services to be rendered in exchange for the negotiated fee. Having a trailing commission embedded in a fee-based series blurs the lines between the attributes of a fee-based series and the embedded fee (trailing commission) series and is potentially misleading for investors.

The November 2014 issue of the Investment Funds Practitioner highlights staff's expectations going forward. In particular, staff's expectation that any new funds with fee-based series not have an embedded trailing commission.

We will continue to review and monitor developments on mutual fund fee structures and dealer compensation models in our prospectus reviews, and will provide further guidance as needed. Issuers and their counsel are encouraged to contact staff in the planning stage of any structure that may give rise to questions concerning this issue.

2.4 Changes to Short Term Trading Fees

Item 6(5) of Form 81-101F1 -- Contents of Simplified Prospectus requires, among other disclosure, a description of the short term trading activities in a mutual fund that are considered to be inappropriate or excessive, and restrictions, if any, that a mutual fund may impose on an investor to deter such short-term trades.

During the year, we became aware of some fund managers who had changed their short term trading fee practices and policies. The changes in practice resulted in short term trading fees applying when redemptions occurred within 7 days of purchase, instead of within a 30 day period as was previously the case.

Short-term trading fees are commonly used as one of the measures to discourage short-term trading and to compensate funds for the additional costs incurred as a result of this practice. Currently, most Canadian investment fund managers impose short-term trading fees ranging between 1% and 2% on redemptions made within 30 to 90 days of purchase.

If a fund manager changes their practice relating to the applicability of short term trading fees, staff will seek clarification regarding the rationale for the change. In particular, staff will seek to understand:

• how the change is considered an effective means to deter short-term trades and remains consistent with the fund manager's statutory duty under s.116 of the Securities Act (Ontario) to act in the best interest of the funds and their securityholders;

• what other policies and procedures the manager has in place to monitor, detect and deter short-term trading, in particular,

• whether the fund manager varied its short-term trading policies and procedures in relation to the two different types of short-term trading activities, namely market timing and excessive trading; and

• for trade monitoring, regardless of the reduction of the redemption fee period from 30 days to 7 days, whether the fund manager will continue with the previously used time frame to monitor these trading activities and to apply the appropriate action;

• how effective the manager's policies and procedures have been to date in monitoring, deterring and detecting short-term trading activities and;

• whether the reduction of the redemption free period was reviewed by the independent review committee and any other governance bodies of the funds, and the frequency with which the fund manager will evaluate the effectiveness of its short-term trading policies going forward.

As staff continues to review and further consider this issue, we remind investment fund managers of their fiduciary duty to maintain effective policies to deter short term trading. As part of the OSC's ongoing review, issuers can expect staff to continue to seek clarification around any changes that are made to short-term trading fees by asking them to answer the above questions. Attention will also be given to the information required by Part A, Item 6(5) of Form 81-101F1 -- Contents of Simplified Prospectus and Item 12(9) of Form 81-101F2 -- Contents of Annual Information Form when reviewing annual filings to ensure that policies and procedures relating to short term trading fees are fully and plainly disclosed.

3. Disclosure and Compliance Reviews

3.1

Continuous Disclosure Reviews

3.1.1

IFRS

3.1.2

High MERs

3.1.3

Fixed Income Volatility

3.1.4

Senior Loans

3.1.5

Direct Payment of Ongoing Dealer Service Fees -- Default Rate Feature

3.1.6

Review of Fees and Expenses Disclosure

3.2

Compliance and Registrant Regulation Branch and Investment Fund Manager Compliance Reviews

On an ongoing basis, the OSC reviews the prospectus and continuous disclosure filings of Ontario-based investment funds. Risk-based criteria are used to select investment funds for reviews of their disclosure documents. Staff may also choose to conduct targeted reviews of a particular industry segment or on a particular topic. For its prospectus reviews, staff continues to focus on three areas: fees and expenses; investment objectives and strategies; and conflicts of interest. Further details on this can be found in the November 2013 issue of the Investment Funds Practitioner.

In addition to prospectus and continuous disclosure reviews, the Investment Funds and Structured Products Branch works closely with staff in the Compliance and Registrant Regulation (CRR) Branch on issues related to fund manager compliance and identifying possible emerging issues. This sometimes leads to us conducting joint reviews.

3.1 Continuous Disclosure Reviews

This section discusses some of our reviews and findings in connection with:

• IFRS

• high MERs

• fixed income volatility

• senior loans

• direct payment of ongoing dealer service fees -- default rate feature

• review of fees and expenses disclosure

3.1.1 IFRS

Investment funds that are subject to National Instrument 81-106 Investment Fund Continuous Disclosure (NI 81-106) are required to adopt International Financial Reporting Standards (IFRS) for financial years beginning on or after January 1, 2014. In early September 2014, we commenced an issue-oriented review of interim financial reports for the period ended June 30, 2014, being the first IFRS financial statements that were required to be filed. Our review focused on the transition requirements set out in IFRS and in NI 81-106. Our review encompassed 90 investment fund managers with head offices in Ontario that managed investment funds with calendar year-end reporting periods.

In order to provide feedback to the industry on the outcome of the reviews, as well as to provide guidance to investment funds that had yet to file their first IFRS financial statements, staff issued a number of IFRS Releases -- IFRS Release No. 1, IFRS Release No. 2, and IFRS Release No. 3 -- during fall 2014. The Releases outlined the most common issues that had been identified during the review.

IFRS Release No.4 was issued in January 2015 and took the form of a "tip sheet" to assist investment fund issuers with some of the key elements in a set of first IFRS annual financial statements.

Staff may expand the reviews by examining the interim financial reports of investment funds with non-calendar year-end periods, or the first IFRS audited annual financial statements. Additional guidance will be issued, as needed, in order to assist investment funds and their advisers with their IFRS filings.

3.1.2 High MERs

During the year, we conducted a targeted review of investment funds that had: (i) management expense ratios (MERs) in excess of 5%; and (ii) absorbed a high level of expenses in order to present MERs after absorptions consistent with the industry average. Our focus was on whether these funds could sustain the above scenarios.

We were informed that new funds tend to fall into both categories and each fund manager's plan was to make fund assets grow in order to reduce MERs before absorptions in the future. For funds with high MERs, if such funds are not able to demonstrate that they are viable after a reasonable period of time, we conveyed our expectation for fund managers to consider all options available to them in order to improve performance, increase fund size, manage costs, achieve efficiencies of scale and, ultimately, reduce MER. For funds with high absorptions, we cautioned fund managers of setting a pattern of absorbing expenses for many years which may influence investor expectations, and reminded managers to ensure that investors understand that waivers or absorptions could cease in the future, potentially resulting in a higher MER. The July 2014 Investment Funds Practitioner provides a summary of the results of this review.

3.1.3 Fixed Income Volatility

As a result of observing significant redemptions from fixed income funds during the second half of 2013, OSC staff conducted a review in 2014 to assess the adequacy of their processes around portfolio risk management, and to determine whether the disclosure relating to risk and market events was sufficient for investors in fixed income funds to make informed investment decisions.

Findings from this review are highlighted in the March 2014 Investment Funds Practitioner.

While our initial review was focused on the fixed income segment, staff has expanded the reviews to focus on other asset classes that may also be susceptible to liquidity issues, in particular, funds with exposure to high yield fixed income, small cap equity funds, and emerging market issuers.

As part of this expanded review, we are seeking clarification from fund managers regarding their policies and procedures around evaluation of liquidity levels of individual fund holdings, and how the fund holdings fit within the restrictions concerning illiquid assets, as set out in Part 2.4 of NI 81-102. In particular, we are:

• asking about any stress testing and scenario analysis the fund managers may have conducted for their fund portfolios;

• enquiring about the valuation of illiquid assets, the valuation policies and procedures more generally, and whether there is any oversight by the independent review committee;

• reviewing risk disclosure in offering and CD documents.

We anticipate publishing an OSC Staff notice in spring 2015 that outlines the findings of these reviews. In this notice, staff expects to communicate its views on best practices for liquidity assessment protocol, portfolio risk management, and disclosure.

3.1.4 Senior Loans

As part of our ongoing reviews focused on fixed income investment funds, staff is also looking at the liquidity of senior loans and how such liquidity fits within the context of the mutual fund regulatory framework, including ETFs, given that senior loans are not investment grade debt and often have longer transaction settlement times than traditional debt securities.

The November 2014 issue of the Investment Fund Practitioner identifies the key areas that staff will be focusing on when reviewing investment funds that have exposure to senior loans.

3.1.5 Direct Payment of Ongoing Dealer Service Fees -- Default Rate Feature

In the course of our prospectus reviews, staff became aware of certain investment fund series that have a default rate feature attached to the direct payment by investors of ongoing dealer service fees. As a part of our continued focus on mutual fund fee structures and dealer compensation models, staff conducted a targeted review of the disclosure documents of several fund families to evaluate and better understand this practice and its extent.

Staff's understanding is that fund managers may have introduced the default rate feature to help optimize the administrative efficiency of dealer back offices and assist dealers who may wish to transition from the embedded fee (i.e., trailing commission) model to a direct payment model of paying ongoing dealer service fees.

While staff generally does not object to fund managers facilitating direct payment arrangements, and expects that a maximum rate is disclosed where the fund manager facilitates such payments, staff's view is that no such payment should be made pursuant to the application of a default rate.

Staff communicated its views to the fund managers that were involved in the targeted review. We also reiterated our views in the July 2014 issue of the Investment Funds Practitioner, which set out staff's expectations regarding the disclosure of these direct payment arrangements and ongoing dealer service fees in the prospectus and by dealers to their clients. In the same article, we also set out our expectations going forward with regard to fund managers transitioning away from the default rate feature for existing funds and series, and our expectation that new funds and series will not include this feature.

3.1.6 Review of Fees and Expenses Disclosure

In our 2013 Annual Report for Investment Fund Issuers we reported that staff had commenced a targeted review of the allocation of overhead expenses between fund managers and their funds. In particular, the review focused on how fund managers address conflicts of interest and whether sufficient disclosure is provided to investors in prospectuses, financial statements, and MRFPs regarding these related party transactions.

On May 8, 2014, we issued OSC Staff Notice 81-724 Report on Staff's Continuous Disclosure Review of the Fees and Expenses Disclosure by Investment Funds which sets out staff's recommendations based on our observations of the fees and expenses disclosure practices of investment funds.

3.2 Compliance and Registrant Regulation Branch and Investment Fund Manager Compliance Reviews

In September 2014, staff of the CRR Branch published OSC Staff Notice 33-745 Annual Summary Report for Dealers, Advisers and Investment Fund Managers. This Notice summarizes new and proposed rules and initiatives impacting registrants, current trends in deficiencies from compliance reviews of registrants (as well as acceptable practices to address them and unacceptable practices to prevent them), and current trends in registration issues.

Section 4.4 of OSC Staff Notice 33-745 contains information specifically for investment fund managers derived from the reviews carried out by the CRR Branch. Topics that were covered in this section include:

• Repeat common deficiencies, including inappropriate expenses charged to funds, inadequate oversight of outsourced functions and service providers, and non-delivery of net asset value adjustments.

• Inadequate sales practices involving promotional items and business promotion activities.

• Inappropriate organizational structure.

• Discussion of a targeted sweep of large impact investment fund managers.

• Discussion of a sweep of newly registered investment fund managers.

• New and proposed rules and initiatives impacting investment fund managers.

4. Outreach, Consultation and Education

4.1

Investment Funds Product Advisory Committee (IFPAC)

4.2

The Investment Funds Practitioner

4.3

International Organization of Securities Commissions -Committee 5 -- Investment Management (IOSCO C5)

We continue our efforts to be transparent regarding practices and procedures that impact investment fund issuers in as timely a manner as possible. Our intent in doing so is to better enable fund managers and their advisors to avoid potential regulatory issues when they are at the planning stage for a new fund or transaction. As indicated at various points earlier in this report, we publish guidance and updates for the investment fund industry periodically.

During the year, staff published four IFRS Releases which discussed the findings from our review of the first IFRS interim financial reports filed by calendar year-end investment funds that are reporting issuers. Early in 2015, staff discussed this topic at a webinar hosted by CPA Canada and attended by over 1,700 CPAs, as well as at an event organized by a national accounting firm. Staff continues to act as an observer on the Investment Funds Standing Committee at CPA Canada.

We also continue to engage in periodic discussions with other regulators such as the Mutual Fund Dealers Association of Canada and the Investment Industry Regulatory Organization of Canada. Additionally, on an ongoing basis, we sought input from the OSC's Investor Advisory Panel, as well as other industry and investor organizations and stakeholders.

At the annual OSC Dialogue, held on October 16, 2014, Rhonda Goldberg, Director of the Investment Funds and Structured Products Branch, participated on a panel that discussed the rapid innovation in products and distribution, as it applies to the long term needs of investors. An audio presentation of the panel discussion is available on the OSC's website.

As in past years, we met with staff from the Investment Management and Derivatives divisions of the Securities and Exchange Commission to discuss investment fund trends, novel products and emerging issues that are common to our respective jurisdictions. These meetings help ensure that our regulatory approaches to product development are consistent and that opportunities for regulatory arbitrage between our markets are minimized.

In an effort to ensure effective national oversight of the investment fund industry, the CSA's Investment Funds Committee holds monthly conference calls. The Committee provides a forum for discussing novel applications, policy interpretation and initiatives, and operational matters in a timely fashion. It ensures that regulatory requirements are nationally applied consistently, fairly, and effectively, pursuant to the Passport system. Rhonda Goldberg is currently Chair of the Committee.

4.1 Investment Funds Product Advisory Committee (IFPAC)

The OSC's IFPAC was established in August, 2011. The IFPAC, which is currently comprised of 11 external members, advises OSC staff specifically on emerging product developments and innovations occurring in the investment fund industry, and discusses the impact of these developments and emerging issues. The IFPAC also acts as one source of feedback to OSC staff on the development of policy and rule-making initiatives to promote investor protection, fairness and market efficiency across all types of investment fund products. The IFPAC typically meets quarterly and members serve a two year term. You can find a list of current IFPAC members on the OSC website.

Topics of discussion with IFPAC this year have included, among others, the pre-sale delivery of Fund Facts; measuring, managing and regulating for risk; and alternative investments becoming an increasing part of the retail investment landscape. We also discussed with IFPAC the continuous disclosure reviews we carried out throughout the year relating to fund fees and expenses, and high yield fixed income and senior loan funds.

4.2 The Investment Funds Practitioner

The Investment Funds Practitioner is an overview of topical issues arising from applications for discretionary relief, prospectuses and continuous disclosure documents that investment fund issuers file with the OSC and that are reviewed by the Investment Funds and Structured Products Branch. It is intended to assist investment fund managers and their advisors who prepare public disclosure documents and applications for discretionary relief on behalf of investment funds. The Practitioner is also intended to make fund managers more broadly aware of some of the issues we have raised in connection with our reviews and how we have resolved them. In this regard, we encourage investment fund managers and their advisors to review the Practitioner. The Investment Funds Practitioner can be found on our website www.osc.gov.on.ca at Information for Investment Funds.

In mid-2014, we posted to the OSC website a Table of Contents of prior editions of the Practitioner, organized by topic. The Table of Contents will be updated concurrently with the publication of each new edition of the Practitioner. We hope that the Table of Contents can be used as a quick reference guide for locating topics discussed in previous editions of the Practitioner.

We published 3 editions of the Investment Funds Practitioner since last year's summary report: March 2014, July 2014 and November 2014. We welcome suggestions for future topics.

4.3 International Organization of Securities Commissions -- Committee 5 -- Investment Management (IOSCO C5)

Staff continued their participation in IOSCO C5 during 2014. This committee is focussed on investment management issues and is comprised of representatives from 30 regulators. The international developments and priorities discussed at C5 inform our policy and operational work, which is also guided by the principles and best practices published by IOSCO.

During the year, IOSCO C5 finalized a report outlining good practices for reducing reliance on credit ratings in the asset management sector. C5 also participated in two reviews in conjunction with IOSCO's Assessment Committee. The first was a review of the principles relating to continuous disclosure, which examined the frequency and timeliness of periodic reporting, including financial statements and material change updates, to investors. The second review followed up on the 2012 report outlining policy recommendations for money market funds (MMFs) and assessed the progress of IOSCO jurisdictions in adopting any necessary rules in relation to MMFs. Amendments to Canadian rules relating to MMFs were already in place by the end of 2012.

Current C5 initiatives include completing the consultation on proposed methodologies for identifying systemically important non-bank non-insurance financial institutions. C5 is also conducting work in the areas of fees and expenses (updating prior IOSCO work in this area), custody arrangements for collective investment schemes, and best practices applicable to the voluntary termination of an investment fund, including fund mergers and reorganizations.

In addition to C5, OSC staff also participated on IOSCO Committee 8 -- Retail Investors during 2014. In particular, staff led C8's effort in the development of a strategic framework document that set out IOSCO's niche in investor education and financial literacy, current thinking and research, a strategy for program development, proposed work streams and best practices. The framework document for best practices was published for consultation in May 2014. The final report, published in November 2014, can be found on the IOSCO website at www.iosco.org.

5. Feedback and Contact Information

If you have any questions regarding, or feedback on, our fifth annual summary report, please send them to <[email protected]>.

You can find additional information regarding investment funds and the Investment Fund and Structured Products Branch on the OSC website.

We have also attached a list of Investment Funds and Structured Products Branch staff at the end of this report.

Investment Funds and Structured Products Branch Contact Information

|

NAME |

|

|

|

|

|

Goldberg, Rhonda -- Director |

|

|

|

|

|

Chan, Raymond -- Manager |

|

|

|

|

|

McKall, Darren -- Manager |

|

|

|

|

|

Nunes, Vera -- Manager |

|

|

|

|

|

Abdurazzakov, Bekhzod -- Legal Counsel |

|

|

|

|

|

Alamsjah, Rosni -- Administrative Assistant |

|

|

|

|

|

Asadi, Mostafa -- Senior Legal Counsel |

|

|

|

|

|

Bahuguna, Shaill -- Administrative Support Clerk |

|

|

|

|

|

Barker, Stacey -- Senior Accountant |

|

|

|

|

|

Bent, Christopher -- Legal Counsel |

|

|

|

|

|

Buenaflor, Eric -- Financial Examiner |

|

|

|

|

|

De Leon, Joan -- Review Officer |

|

|

|

|

|

Gerra, Frederick -- Legal Counsel |

|

|

|

|

|

Huang, Pei-Ching -- Senior Legal Counsel |

|

|

|

|

|

Jaisaree, Parbatee -- Administrative Assistant |

|

|

|

|

|

Joshi, Meenu -- Accountant |

|

|

|

|

|

Kalra, Ritu -- Senior Accountant |

|

|

|

|

|

Kwan, Carina -- Legal Counsel |

|

|

|

|

|

Lee, Bryana -- Legal Counsel |

|

|

|

|

|

Lee, Irene -- Senior Legal Counsel |

|

|

|

|

|

Mainville, Chantal -- Senior Legal Counsel |

|

|

|

|

|

Marcovici, Harald -- Legal Counsel |

|

|

|

|

|

Nania, Viraf -- Senior Accountant |

|

|

|

|

|

Paglia, Stephen -- Senior Legal Counsel |

|

|

|

|

|

Papini, Andrew -- Legal Counsel |

|

|

|

|

|

Persaud, Violet -- Review Officer |

|

|

|

|

|

Rana, Marilyn -- Administrative Assistant |

|

|

|

|

|

Russo, Nicole -- Review Officer |

|

|

|

|

|

Schofield, Melissa -- Senior Legal Counsel |

|

|

|

|

|

Thomas, Susan -- Senior Legal Counsel |

|

|

|

|

|

Tong, Louisa -- Administrative Assistant |

|

|

|

|

|

Welsh, Doug -- Senior Legal Counsel |

|

|

|

|

|

Yu, Sovener -- Accountant |

|

|

|

|

|

Zaman, Abid -- Accountant |

|