Application for an Exemption from the Marketplace Rules – Notice and Request for Comment – Dealerweb Inc.

A. Background

Dealerweb Inc. (Dealerweb) has applied for an exemption from National Instrument 21-101 Marketplace Operation (NI 21-101), National Instrument 23-101 Trading Rules (NI 23-101) and National Instrument 23-103 Electronic Trading and Direct Electronic Access to Marketplaces (NI 23-103 and, together with NI 21-101 and NI 23-103, the Marketplace Rules) in their entirety.

Dealerweb is registered as an alternative trading system (ATS) with the Securities and Exchange Commission (SEC) and is an SEC registered broker-dealer, a member of the Financial Industry Regulatory Authority (FINRA) and the Municipal Securities Rulemaking Board. Dealerweb operates and maintains an electronic trading platform that facilitates the trading of various US government securities including United States treasury securities, United States treasury bills, United States treasury floating rate notes and overnight and term repurchase transactions.

B. Requested Relief

Dealerweb requests relief from the Marketplace Rules. In the application, Dealerweb has outlined how it meets the criteria for exemption from the Marketplace Rules set out in CSA Staff Notice 21-328 Regulatory Approach to Foreign Marketplaces Trading Fixed Income Securities.{1} The application and draft exemption order are attached as Annexes A and B, respectively, to this notice.

C. Comment Process

We are seeking public comment on all aspects of Dealerweb's application and the draft exemption order. Please provide your comments in writing, via e-mail, on or before March 21, 2022, to:

Market Regulation Branch

Ontario Securities Commission

20 Queen St. West, 22nd Floor

Toronto, ON, M5H 3S8

[email protected]

Questions may be referred to:

Heather Cohen

Senior Legal Counsel, Market Regulation

Ontario Securities Commission

[email protected]Ruxandra Smith

Senior Accountant, Market Regulation

Ontario Securities Commission

[email protected]

{1} Available at https://www.osc.ca/en/securities-law/instruments-rules-policies/2/21-328/csa-staff-notice-21-328-regulatory-approach-foreign-marketplaces-trading-fixed-income-securities

ANNEX A

Norton Rose Fulbright Canada LLP

222 Bay Street, Suite 3000, P.O. Box 53

Toronto, Ontario M5K 1E7 Canada

F: +1 416.216.3930

Andrew Grossman\

+1 416.216.2312

[email protected]

Mark Bissegger

+1 416.212.6719

[email protected]

December 21, 2021

Sent by Email

Ontario Securities Commission

20 Queen St. West, 22nd Floor

Toronto, Ontario M5H 3S8

Autorité des marchés financiers

Place de la Cité, tour Cominar

2640, boulevard Laurier, bureau 400

Québec, Québec G1V 5C1

Nova Scotia Securities Commission

Ste. 400, Duke Tower, 5251 Duke St.

Halifax, NS B3J 1P3

Dear Sirs/Mesdames:

RE: Dealerweb Inc. -- Application for Exemption From Certain Marketplace Rules That Apply to an Alternative Trading System

We are Canadian counsel to, and are filing this coordinated review application (the Application) on behalf of, Dealerweb Inc. (Dealerweb or the Applicant) pursuant to Section 3.4 of National Policy 11-203 -- Process for Exemptive Relief Applications in Multiple Jurisdictions (NP 11-203). We are filing this Application on behalf of Dealerweb in Ontario, Quebec and Nova Scotia (the Jurisdictions).

In accordance with the guidelines set out in Section 3.6 of NP 11-203, the Ontario Securities Commission (the OSC) has been selected as the principal regulator for the purposes of this Application on the basis that Dealerweb has the most significant connection to Ontario. In accordance with Section 5.2(3) of NP 11-203, this Application is being filed with each of the securities regulatory authorities in the Jurisdictions (the ATS Relief Decision Makers) for relief from the securities legislation of each of those Jurisdictions (the Legislation). In accordance with section 3.4 of NP 11-203, the Applicant is filing this Application with, and paying fees to, each of the ATS Relief Decision Makers.

On behalf of Dealerweb, we hereby request that the ATS Relief Decision Makers grant a decision under the Legislation pursuant to Section 15.1 of National Instrument 21-101 -- Marketplace Operation (NI 21-101), Section 12.1 of National Instrument 23-101 -- Trading Rules (NI 23-101) and Section 10 of National Instrument 23-103 -- Electronic Trading and Direct Access to Marketplaces (NI 23-103 and, together with NI 21-101 and NI 23-101, the Marketplace Rules) exempting Dealerweb from the application of all provisions of the Marketplace Rules that apply to a person or company carrying on business as an alternative trading system (ATS) in the Jurisdictions (the Requested Relief).

Dealerweb is not in default of securities legislation in its home jurisdiction nor in any of the Jurisdictions with the exception that between October 5, 2016 and December 13, 2021, without being registered as an ATS or receiving exemptive relief, Dealerweb permitted one Quebec participant to access the Platform (as defined below). Dealerweb became aware of this access on November 18, 2021 and, after prompt internal investigation and review, brought it to the attention of the OSC and the Autorité des marchés financiers (the AMF) on December 7 and 8, 2021, respectively. Dealerweb removed this access on December 13, 2021 and is taking steps to ensure compliance with the securities legislation in Quebec.

The Requested Relief sought is not novel and similar exemptions have previously been granted by the ATS Decision Makers to ATSs based in the United States of America (the US) (see Section 14.1.8 of this Application for further details).

Terms defined in National Instrument 14-101 -- Definitions and NI 21-101 have the same meaning if used in this Application, unless otherwise defined.

Dealerweb submits that it has provided in this Application for an exemption from the Marketplace Rules the information requested by the Canadian Securities Administrators (the CSA) in CSA Staff Notice 21-328 -- Regulatory Approach to Foreign Marketplaces Trading Fixed Income Securities (Staff Notice 21-328) to assist staff in the Jurisdictions in evaluating whether it is appropriate for Dealerweb to be granted the Requested Relief. Dealerweb further submits that it should be permitted to offer direct access to Canadian Participants (as defined below) without having to establish a Canadian-based affiliate as it is able to substantially meet or otherwise address the criteria set out in Staff Notice 21-328 and address the regulatory framework in Staff Notice 21-328, including the proposed terms and conditions for granting an exemption from the Marketplace Rules. In particular, the Applicant submits that it is subject to a regulatory regime in its home jurisdiction that is substantially similar to that applied to an ATS in each Jurisdiction.

In addition, Dealerweb submits that the Application demonstrates that it satisfies the criteria provided in the CSA's regulatory framework and exemption model. Further, Dealerweb submits that the balance between avoiding market fragmentation and reducing regulatory duplication and burden, and facilitating investor protection and promoting a fair and efficient market, is met. For these reasons and the reasons provided in the Application, the Applicant submits that granting the Requested Relief is warranted.

For convenience, this Application is divided into the following Parts:

PART I -- BACKGROUND

PART II -- APPLICATION OF APPROVAL CRITERIA TO THE ALTERNATIVE TRADING SYSTEM

1. Regulation of Dealerweb

2. Governance

3. Regulation of Products

4. Access

5. Regulation of Participants on the ATS

6. Clearing and Settlement

7. Systems and Technology

8. Financial Viability and Reporting

9. Recordkeeping

10. Outsourcing

11. Fees

12. Information Sharing and Oversight Arrangements

13. IOSCO Principles

Part III -- Submissions by Dealerweb

14. Submissions Concerning the Requested Relief

Part IV -- Fees and Other Matters

15. Fees and Other Matters

Appendix A -- Draft Decision

Appendix B -- Authorization and Verification Statement

PART I -- BACKGROUND

1. Dealerweb is a private corporation incorporated under the laws of New York whose registered and head office is located at 1177 Avenue of the Americas, New York, NY, 10036. Dealerweb was founded in 1975 as Hilliard Farber & Co., Inc.

2. Dealerweb does not have any offices or maintain a physical presence in the Jurisdictions or any other Canadian province or territory.

3. Dealerweb is an ATS and a broker-dealer registered with the US Securities and Exchange Commission (the SEC) (SEC# 8-38103) pursuant to Section 15 of the Securities Exchange Act of 1934, as amended (the Exchange Act), and is registered as an introducing broker pursuant to the Commodity Exchange Act (CEA). Dealerweb is also a member of the Financial Industry Regulatory Authority (FINRA) (CRD#: 19662), the Municipal Securities Rulemaking Board (MSRB) and the National Futures Association (NFA). FINRA is a US equivalent of the Investment Industry Regulatory Organization of Canada (IIROC).

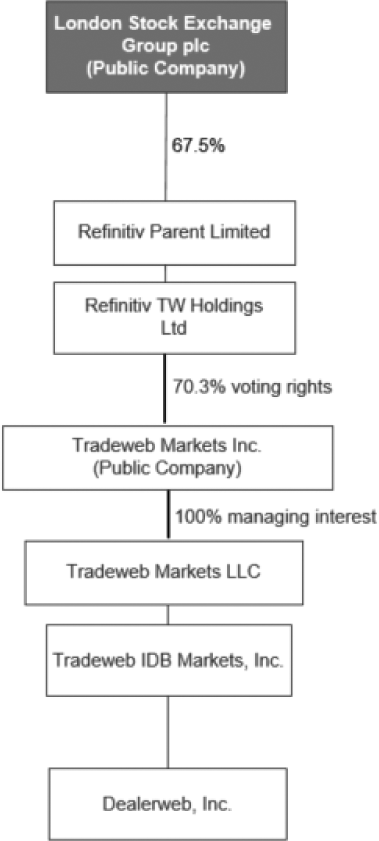

4. Dealerweb is a wholly-owned subsidiary of Tradeweb Markets LLC (Tradeweb), a private limited liability company incorporated under the laws of Delaware. Dealerweb has no subsidiaries. Tradeweb is wholly-owned by Tradeweb Markets Inc., a public company that is majority owned by Refinitiv Holdings Ltd., a company that is currently indirectly wholly-owned by London Stock Exchange Group plc. (LSEG) as set out in the corporate structure chart below. The voting rights of Tradeweb Markets Inc. not controlled by LSEG are held by public shareholders.

5. Dealerweb and Tradeweb are party to an inter-affiliate service agreement pursuant to which Tradeweb provides certain services including product and technology development and support, quality assurance, network support, system and application security, legal and risk management. Dealerweb maintains responsibility for the personnel and operations provided by Tradeweb.

6. Dealerweb operates a fully-electronic platform (the Platform) which facilitates the trading of various US government securities. The Platform facilitates trades of: (i) on-the-run United States treasury securities (OTR Treasuries); (ii) off-the-run United States treasury securities (OFTR Treasuries); (iii) United States treasury bills (T-Bills); (iv) United States treasury floating rate notes (Floating Rate Notes); and (v) overnight and term repurchase transactions (Repos and, collectively with OTR Treasuries, OFTR Treasuries, T-Bills and Floating Rate Notes, the Treasury Products).

7. In offering the Platform, Dealerweb acts as an interdealer broker. Participants on the Platform include many of the world's largest commercial and investment banks and principal trading firms. The Platform facilitates trades only on an electronic basis with the exception of trades on the OFTR CLOB which are executed in a hybrid model as set out in further detail in paragraph 12 below. Dealerweb also offers a voice trading desk (the Treasury Voice Desk) which facilitates trades for OFTR Treasuries, T-Bills, Floating Rate Notes and treasury inflation-protected securities (TIPS) and a voice trading desk for Repos (the Repo Voice Desk).

OTR Treasuries

8. The Platform facilitates trades in OTR Treasuries in two distinct ways. The central limit order book for OTR Treasuries (the OTR CLOB) was launched in 2014 and currently has approximately 25 participants. The OTR CLOB offers an all-to-all trading model composed of a variety of liquidity takers and makers. The liquidity takers and makers on the OTR CLOB are primarily registered broker-dealers, banks, registered hedge funds and investment advisors, with the majority being registered broker-dealers and banks. Execution on the OTR CLOB is fully anonymous and market data is disseminated to all counterparties. Price increments on the OTR CLOB are standard across the market. The minimum trading size for all participants on the OTR CLOB is US$1 million. Execution on the OTR CLOB occurs on a price and time priority basis.

9. The Platform also facilitates trades in OTR Treasuries under a direct streaming mechanism which was launched in 2017 (Direct Streams). Direct Streams offer access to competitive prices at potentially greater size while limiting market impact. Liquidity providers continuously send two-way prices and sizes to preferred counterparties for trading on a disclosed or anonymous basis. Direct Streams provides participants with the connectivity, counterparty arrangements and data analytics to create custom trading networks of liquidity providers in OTR Treasuries. The liquidity takers and makers in Direct Streams are primarily registered broker-dealers, banks, registered hedge funds and investment advisors, with the majority being registered broker-dealers and banks. Many participants have access to both the OTR CLOB and Direct Streams. The minimum trading size for all participants in Direct Streams is US$1 million.

10. Preferred counterparties participating in Direct Streams are identified and ranked based on the best price provided via the specific stream. After best price, ranking in Direct Streams is determined based on the participants' preferences on whom they wish to transact with. Participants can participate in Direct Streams either on a disclosed or anonymous basis. Over 80% of the trading activity in Direct Streams is done on a disclosed basis. Each participant determines based on its preferences whether it wants to trade on a disclosed or anonymous basis in Direct Streams.

11. Under the Direct Streams mechanism, prices aggregate from direct streams onto a single screen to simplify and streamline access to liquidity. The functionality centralizes all points of connectivity, allowing participants to efficiently evaluate available prices and sizes as well as route orders across Direct Streams and the OTR CLOB. Under Direct Streams, execution market data is only disseminated to the counterparties to the trade. Price increments are 1/16th of 1/32nd across all tenors.

OFTR Treasuries

12. The Platform facilitates trades in OFTR Treasuries via a hybrid model where a voice broker will receive an indication of interest from a subscriber to either buy or sell which is then entered into the central limit order book for OFTR Treasuries (the OFTR CLOB) and if a match occurs, the trade will be executed in the same manner as on the OTR CLOB, on a price and time priority basis. The OFTR CLOB was launched in November 2011 and has approximately 53 active firms and 167 users setup to trade OFTR Treasuries. The subscriber base consists primarily of registered broker-dealers, banks, and registered investment advisors and hedge funds. The minimum order size is between US$25 million to US$5 million, depending on the maturity and type of OFTR Treasury and the minimum increments are US$1 million.

13. The Platform also facilitates trades in OFTR Treasuries through a session-based "sweep" protocol (OFTR Sweep). OFTR Sweep trading sessions take place at predetermined times: Monday through Thursday at 9:30 A.M. and 3:30 P.M.; Friday at 9:30 A.M. and then during month end week on Monday through Friday at 9:30 A.M. and 3:30 P.M. Participants can upload or manually input the OFTR Treasuries that they wish to purchase or sell directly into Dealerweb's order entry panel for execution on the Platform. Based on these inputs, orders are matched once the OFTR Sweep session starts at the specific time in the morning and afternoon based on the offsetting positions that have been entered for the OFTR Treasury against the Tradeweb Composite mid-price. The Tradeweb Composite mid-price is established by the pricing and market data submitted by 20 specific dealers for specific OFTR Treasuries and is considered proprietary information. The OFTR Sweep trading sessions offer liquidity and price transparency in less liquid OFTR Treasuries. OFTR Sweep is primarily used by participants for portfolio rebalancing and inventory management and provides an important source of liquidity for the participants and their respective customers. The first OFTR Sweep session took place in June 2014 and presently there are 38 active firms, including 162 users who participate in OFTR Sweep trading sessions. The subscriber base participating in OFTR Sweep trading sessions consists of registered broker dealers, banks, and registered investment advisors and hedge funds.

T-Bills

14. T-Bills are traded on the Platform through a central limit order book (the T-Bill CLOB) and sweep trading sessions (T-Bill Sweep), each of which is substantially similar to the OFTR CLOB and OFTR Sweep trading sessions, respectively. The minimum size requirements for T-Bills traded on the T-Bill CLOB is between US$5 million and US$25 million. T-Bills traded on the T-Bill CLOB trade at a rate, not price, but the functionality for matching is the same, based on the rate and time priority similar to the OFTR CLOB. The T-Bill CLOB was launched in June 2010.

Floating Rate Notes

15. Floating Rate Notes are traded on the Platform through both the CLOB (the FRN CLOB) and sweep trading sessions (FRN Sweep). Floating Rate Notes traded on the FRN CLOB trade on a discount margin. The functionality for Floating Rate Notes executed through the FRN CLOB is similar to the OFTR CLOB and T-Bill CLOB as trades are matched based on the price (discount margin) and time priority. The minimum size requirement of Floating Rate Notes on the FRN CLOB is US$5 million and the minimum increment is US$1 million. The FRN Sweep trading sessions function in the same manner as the OFTR Sweep and T-Bill Sweep trading sessions. The subscriber base for both the FRN CLOB and FRN Sweep trading session consists of registered broker-dealers, banks, and registered investment advisors and hedge funds. The FRN CLOB was launched in February 2014.

Repos

16. The Platform facilitates the trading of overnight and term Repos through a central limit order book (the Repo CLOB). Trades executed on the Repo CLOB can be for specific collateral, general collateral, and general collateral financing, which consist of T-Bills, treasury notes, treasury bonds, agency bonds, Floating Rate Notes, agency mortgage backed securities and adjustable rate mortgages. The primary Repo trading activity on the Platform is for specific collateral and general collateral, which consist of U.S. Treasury securities. General collateral financing can utilize agency bonds, agency mortgage backed securities and adjustable rate mortgages as collateral, but these are rarely traded on the Platform. The Repo CLOB functions in a similar capacity as the rest of the trading activity on the Platform's other central limit order books as trades are matched on a price and time priority basis. Repos are priced based on a rate and the minimum size for all Repos excluding general collateral Repos is US$25 million and the minimum size for general collateral Repos is US$50 million. The Repo CLOB began trading in June 2016. Only Fixed Income Clearing Corporation (FICC) members are allowed to trade Repos on the Platform. Dealerweb does not facilitate and is not involved with the transfer of the collateral utilized in Repo transactions. Dealerweb introduces both counterparties to the transaction to FICC for settlement, but the counterparties to the trade are responsible for the facilitation of the collateral that is part of the Repo transaction.

17. Repos are transactions where securities are used to borrow cash, or vice versa. The principal participants in these transactions are broker-dealers and banks, which are FICC members. In these transactions, cash is exchanged for collateral, which consists of T-Bills, treasury notes, treasury bonds, Floating Rate Notes, agency bonds, agency mortgaged securities and adjustable rate mortgages. Agency bonds, agency mortgage-backed securities and adjustable rate mortgages are primarily used for general collateral financing Repo transactions, which are executed primarily through the Repo Voice Desk. Repo transactions are driven by a need to lend/borrow specific securities or to lend/borrow cash. Cash lenders use Repos as a way to securely invest cash. Typical cash lenders include money market funds, central banks and others. Securities lenders enter into Repos to finance their securities positions or to obtain leverage. Typical cash borrowers/securities lenders are hedge funds, mortgage real estate investment trusts, pension funds, asset managers, insurance companies and sovereign wealth funds.

Voice Desks

18. Dealerweb also operates the Treasury Voice Desk which trades OFTR Treasuries, T-Bills, Floating Rate Notes and TIPS. OFTR Treasuries are the primary Treasury Product traded on the Treasury Voice Desk. The Repo Voice Desk offers trading in the same products as the Repo CLOB. The Repo Voice Desk only executes trades on behalf of FICC members. The majority of trading on the Repo Voice Desk is in general collateral and general collateral financing Repos. Trades submitted through the Treasury Voice Desk and the Repo Voice Desk are sent to a broker who looks for a matching order on the other side of the transaction.

Participants, Clearing and Settlement

19. When approved as a new participant on the Platform, the participant does not automatically receive access to all of the Treasury Products traded on the Platform. Each participant determines which Treasury Products it wishes to trade as well as the specific ways it wishes to trade such Treasury Products (i.e. CLOB, Direct Streams or Sweep, as applicable).

20. It is expected that certain institutional investors in the Jurisdictions wish to become clients of Dealerweb and utilize the Platform in order to access the liquidity afforded by the robust, existing network of clients. There are currently no Canadian clients trading on the Platform.

21. Dealerweb proposes to offer access to its Platform to participants in the Jurisdictions (Canadian Participants). In order to obtain access to the Platform, a Canadian Participant will need to abide by the terms and conditions set out in Dealerweb's Participant Agreement (the Participant Agreement). The Participant Agreement provides clear and transparent access criteria and requirements for all market participants on the Platform to maintain the integrity of the Platform. Dealerweb applies these criteria to all Platform participants in an impartial manner. Dealerweb does not regulate participants on the Platform, other than by denying them access.

22. Canadian Participants will have access to all Treasury Products traded on the Platform and to all forums for trading such Treasury Products on the Platform, including as a liquidity taker or as a liquidity maker, or both (as applicable).

23. There are no retail clients on the Platform and no Canadian Participants will be retail investors. Dealerweb's current institutional participants are primarily made up of dealers, banks, hedge funds and asset managers. The majority of participants are located in the US; however, a number are in jurisdictions which allow Dealerweb to operate under foreign exemptions, such as Switzerland. To date, the majority of trading volume on the Platform originates from US participants. Dealerweb expects the majority of trading to continue to come from US participants. Dealerweb expects that Canadian Participants will be sophisticated investors with a working knowledge of the fixed-income markets. Dealerweb intends to make training available for each person who has access to trade on the Platform.

24. Canadian Participants will be comprised of institutional investors that qualify as permitted clients as defined in Section 1.1 of National Instrument 31-103 -- Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103).

25. The trading hours on the Platform are 8:30 a.m. (Japan Standard Time) to 5:30 p.m. (Eastern Time), Monday through Friday, excluding the Securities Industry and Financial Markets Association's recommended full and early holiday closings.

26. The clearing flow for all Treasury Products on the Platform depends on whether the participant is a member of FICC or a non-FICC member, regardless of whether the trades are generated from a CLOB, Sweep session or Direct Streams. Trades involving a FICC member are submitted to FICC for comparison and novation. Trades involving non-FICC members are sent to SG Americas Securities, LLC (SG Americas), a third party clearer and FICC member, who settles them on Dealerweb's behalf at Fedwire on the settlement date. Dealerweb has entered into a fully disclosed clearing relationship with SG Americas which was approved by FINRA. This clearing relationship is not a sponsored arrangement with SG Americas. Each of Dealerweb and SG Americas maintains netting, repo netting and general collateral finance (GCF) services with FICC. Dealerweb is a member of FICC. The OSC and the AMF have each issued an order exempting FICC from the requirement to be recognized as a clearing agency.

27. For those transactions which are cleared through Fedwire via Dealerweb's relationship with SG Americas, Dealerweb opens a Delivery-Versus-Payment (DVP) account for each such participant. The DVP accounts record a buy and/or sell depending upon the specific type of trading activity and then facilitate the delivery and/or receipt of the security to the participant's clearing firm. There are no balances or securities held in these DVP accounts as they remain flat at all times. Dealerweb stands in the middle of each transaction from a riskless principal standpoint regardless of how trades are settled (i.e. whether directly through FICC or on behalf of non-FICC members through SG Americas).

28. Dealerweb actively monitors the settlement of trades with non-FICC members on an almost real time basis. Throughout each trading day, Dealerweb's Operations Department, Regulatory Compliance Department, and Finance Department receive multiple reports provided by SG Americas which provide a breakdown of all trades that are outstanding and all deliveries and receipt of securities from a settlement perspective. In addition, at the end of each trading day, a settlement date activity report is generated and emailed to Dealerweb's Operations, Regulatory Compliance, and Finance Departments, which provides a summary breakdown of all outstanding trades for each participant pending settlement with non-FICC members through SG Americas. In addition, as part of the onboarding process, all participants are required to receive know-your-client (KYC) and anti-money laundering (AML) approval from Regulatory Compliance and Credit Risk Approval from Tradeweb's Enterprise Risk Management Group. As part of the credit risk review, all participants receive an approved credit limit based on their financial status. The Enterprise Risk Management Group monitors all exposure against approved credit limits on a real time basis and an end of day summary report is generated which provides a breakdown of all outstanding trades against the approved credit limits.

29. The CLOB matching process is based on a first-in first-out market with no locked markets and no last-look. Hidden size orders are available but shown size orders take priority in the matching process. The Direct Streams matching process is based first on best price, second on ranking preference by the counterparty and third on a random tie-breaker. Liquidity takers have the ability to rank their liquidity providers as a tie-breakers. If no ranking is provided, a random tie-breaker is used.

30. The CLOB facilitates "fill and kill" as well as "fill and store" orders. Direct Streams facilitates "fill and kill", "fill and store" and "fill or kill" orders. Orders on the CLOB and Direct Streams default to "fill and store" orders.

PART II -- APPLICATION OF APPROVAL CRITERIA TO THE ALTERNATIVE TRADING SYSTEM

Article 1 REGULATION OF DEALERWEB AND THE PLATFORM

1.1. Regulation of the alternative trading system -- The alternative trading system is regulated in an appropriate manner in another jurisdiction by a foreign regulator (the Foreign Regulator)

1.1.1. In the Jurisdictions, an ATS is required by section 6.1 of NI 21-101 to be registered as an investment dealer and be a member of IIROC in order to operate a business as an ATS in the Jurisdictions. In addition, an ATS is subject to registration requirements under applicable Canadian securities law when engaging in the business of trading. Similarly, in the US, all broker-dealers and their associated persons must be registered with the SEC (or FINRA in the case of associated persons) pursuant to section 15 of the Exchange Act and are subject to its regulations. They must as well be a member of at least one securities self-regulatory organization (SRO), which is further delegated some regulatory authority. Most broker-dealers in the US are members of FINRA.

1.1.2. Dealerweb is subject to a comprehensive regulatory regime in the US, both as a registered broker-dealer and as an operator of an ATS. In such capacity, Dealerweb is registered with the SEC, FINRA, and the MSRB in the US, and is also subject to regulation under state securities rules and regulations (collectively, the US Regulators). The US Regulators set rules, conduct compliance reviews and perform surveillance and enforcement. The US regulatory structure for broker-dealers such as Dealerweb includes: financial and other fitness criteria for subscribers; reporting and record-keeping requirements; procedures governing the treatment of customer funds and property and business conduct standards; provisions designed to protect the integrity of the markets; and statutory prohibitions on fraud, abuse and market manipulation.

1.1.3. In the US, broker-dealers are primarily governed by the Exchange Act, and the rules and regulations promulgated thereunder. Section 4 of the Exchange Act provides for the creation of the SEC, which was established in 1934. The Exchange Act empowers the SEC with broad authority over all aspects of the securities industry. This includes the power to register, regulate, and oversee brokerage firms, transfer agents, and clearing agencies as well as US SROs, including FINRA. The Exchange Act also identifies and prohibits certain types of conduct in the markets and provides the SEC with examination and disciplinary powers over regulated entities and persons associated with them. As an SRO, FINRA has significant authority over broker-dealers, delegated to them by the SEC and consented to by their members, to adopt and enforce rules; impose fines and other sanctions; and conduct examinations and investigations.

1.1.4. In the US, investors are protected by comprehensive regulation that governs the conduct of broker-dealers, including Dealerweb, and other market participants. These regulatory frameworks include, but are not limited to, the Securities Act of 1933 (the Securities Act), the Exchange Act (including Regulation ATS, as described below), the Investment Company Act of 1940, the Investment Advisers Act of 1940, the rules and regulations of the US Commodities Futures Trading Commission, the rules of FINRA, the MSRB, and the NFA, the AML and KYC rules and regulations of the US Department of the Treasury (US Treasury) Financial Crimes Enforcement Network (FinCEN), and state securities rules and regulations.

1.1.5. With respect to the agencies and organizations that regulate broker-dealers and ATSs, the SEC, FINRA, and the MSRB share common goals of protecting investors and other market participants, maintaining fair, orderly, and efficient markets, and facilitating capital formation. Of these goals, investor protection is the primary focus.

1.2. Authority of the Foreign Regulator -- The Foreign Regulator has the appropriate authority and procedures for oversight of the ATS. This includes regular, periodic oversight reviews of the alternative trading systems by the Foreign Regulator.

Scope of authority and authorizing statutes

1.2.1. The SEC has delegated certain of its day-to-day regulatory oversight responsibilities of broker-dealers to FINRA. FINRA's rules, which are approved by the SEC, allow for disciplining member firms, including Dealerweb, for improper conduct and for establishing measures to ensure market integrity and investor protection. Further, FINRA conducts surveillance programs that collect and integrate trading data across ATSs to detect abusive activity and conducts an examination program to review how alternative trading systems handle orders, including how they keep order information and other sensitive client information confidential. The program also assesses certain firm's financial and operational condition.

1.2.2. As set forth in greater detail below, broker-dealers in the US are subject to routine and for-cause examinations by the SEC and FINRA. Broker-dealers are also subject to periodic financial and operational reporting (monthly and annually) through the filing of Financial and Operational Combined Uniform Single (FOCUS) Reports, which are filed with FINRA. Further, a broker-dealer is subject to a number of self-reporting obligations imposed by the SEC and FINRA, including the requirement to: self-report certain events pursuant to FINRA Rule 4530 (as discussed in greater detail below); file and keep current certain information with respect to the broker-dealer's business and operations on Form BD; and to file and keep current information with respect to registered representatives employed with, or terminated by, the broker-dealer (including with respect to certain reportable events, such as certain criminal charges or convictions) on Form U4 and Form U5. In addition, Broker-dealers are subject to market surveillance by the SEC and FINRA, which is largely accomplished through various trade-reporting forms and systems, including: Order Audit Trail System (OATS) (order, quote, and trade information for all National Market System (NMS) stocks and over-the-counter (OTC) equity securities); TRACE (mandatory reporting of over-the-counter secondary market transactions in eligible fixed-income securities); Automated Confirmation of Transactions (ACT) (OTC and NASDAQ securities); Consolidated Audit Trail (CAT) (NMS stocks, OTC equity securities, and exchange listed options); and SEC Form 13H (large trader reporting). Subject to certain exemptions, broker-dealers are also required to file quarterly reports with the SEC on Form 17-H (Risk Assessment Reports for Brokers and Dealers), which includes information with respect to the broker-dealer and the financial and securities activities of certain affiliates of a broker-dealer that are reasonably likely to have a material impact on the financial or operational condition of the broker-dealer. Tradeweb Direct, LLC files the Form 17-H on behalf of Dealerweb with the SEC each quarter.

1.2.3. In addition to the above, broker-dealers that operate an ATS are subject to additional oversight and reporting under Regulation ATS (as described below), including the requirements to file and keep current Form ATS.

1.2.4. In addition the SEC and the ATS Relief Decision Markets are parties to a memorandum of understanding related to securities market oversight and enforcement.{2} The OSC and the AMF are also parties to a memorandum of understanding with FINRA related to securities market oversight and enforcement.{3}

US regulation of broker-dealers and ATSs -- Source of its authority to supervise the ATS

1.2.5. Pursuant to Section 15(a) of the Exchange Act, subject to certain exceptions, all persons that use the mails or any means or instrumentality of interstate commerce to effect securities transactions must register with the SEC and become members of a national securities association, of which there is only one, FINRA. ATS status and registration is a supplement to broker-dealer registration; in other words an ATS can only be operated by a registered broker-dealer. Therefore, as an ATS, Dealerweb is subject to all applicable rules and regulations to which broker-dealers are subject, as well as specific rules and regulations applicable to the operation of an ATS.

1.2.6. ATSs are subject to a comprehensive regulatory framework in the US. As an initial matter, subject to certain limited exceptions, all US ATSs must be registered with the SEC as a broker-dealer and be a member of FINRA. In this regard, ATSs are subject to extensive regulation and oversight by the SEC and FINRA, not only with respect to ATS operation, but also with respect to the broker-dealer's operations as a whole. Further, in becoming a member of FINRA, each broker-dealer must enter into a bespoke membership agreement that sets forth the parameters of the broker-dealer's operations, not only with respect to business lines, but also with respect to minimum net capital requirements, number of offices, and number of client-facing registered representatives that the broker-dealer may employ.

1.2.7. In addition to the foregoing, to acquire and maintain its status as an ATS, Dealerweb must satisfy several statutorily-prescribed requirements set out in Regulation ATS (17 C.F.R. § 242.300 et seq.) (Regulation ATS), which sets forth additional guidelines and requirements with respect to: (i) broker-dealer registration; (ii) notice; (iii) order display and execution access; (iv) fees; (v) fair access; (vi) capacity, integrity, and security of automated systems; (vii) recordkeeping; (viii) reporting obligations; and (ix) compliance and controls.

1.2.8. Broker-dealer registration. As noted above, pursuant to Exchange Act Rule 301(b)(1), an ATS must be registered as a broker-dealer under Section 15 of the Exchange Act. When the SEC adopted Regulation ATS in 1998 it revised the definition of "exchange" to clarify that electronic communication networks (ECNs) were in fact deemed exchanges. However, the SEC then in turn provided flexibility to these ECNs by permitting them to be regulated as a broker-dealer, rather than as a traditional stock exchange. This means that the operator of an ATS is regulated as a broker-dealer, which this Application describes in greater detail.

1.2.9. Notice. Pursuant to Rule 301(b)(2), an ATS (through its broker-dealer operator) must file a report with the SEC under five circumstances:

i. Rule 301(b)(2)(i) requires an initial operations report to be filed on Form ATS with the SEC at least 20 days prior to commencing operation of its ATS.

ii. Form ATS requires Dealerweb to provide the SEC with details relating to the operation of the ATS, including (but not limited to):

(a) the type of subscribers (e.g. retail, broker-dealers, institutional clients, etc.) that will be permitted to access the ATS, and any differences in access that will be offered by the ATS to the different groups of subscribers, if applicable;

(b) a list of the types of securities the ATS trades (e.g. debt, equity, etc.) and whether such securities will not be registered under Section 12(a) of the Exchange Act;

(c) a list of the securities (as opposed to the "types") the ATS trades;

(d) the manner of operation of the ATS, procedures governing orders, means of access, procedures governing execution, reporting, clearing and settlement of securities transactions effected through the ATS;

(e) system guidelines and any other manuals or other materials provided to the subscriber relating to the ATS; and

(f) the ATS' procedures for reviewing systems capacity, security and contingency planning.

iii. Rule 301(b)(2)(ii) requires an amendment to Form ATS be filed with the SEC at least 20 days prior to implementing a material change to the operation of its ATS;

iv. Rule 301(b)(2)(iii) requires a quarterly filing be made with the SEC in the event that any information previously provided in the initial operations report becomes inaccurate;

v. Rule 301(b)(2)(iv) requires that a filing be made with the SEC promptly in order to correct information previously reported on Form ATS pursuant to Rules 301(b)(2)(i), (ii) or (iii) becomes inaccurate; and

vi. Rule 301(b)(2)(v) requires that a filing be made with the SEC promptly in the event that the ATS ceases operations.

1.2.10. Order display and execution access. Section 8.1 of NI 21-101 imposes certain pre-trade and post-trade information transparency requirements on ATSs displaying orders of debt-securities. Section 10.1 of NI 21-101 requires disclosure by a marketplace (including an exchange and an ATS) on its website of certain information reasonably necessary to enable a person or company to understand the marketplace's operations or services it provides, including information related to the system's protocols and rulebook. Further, Staff Notice 21-328 requires that a foreign ATS provide information regarding its transparency of operations, including disclosure relating to order execution, fees and order priority.

1.2.11. While Rule 301(b)(3) of Regulation ATS in the US imposes similar market transparency requirements, this Rule is not applicable to the Platform as the Platform is not a NMS stock ATS, nor does the Platform make NMS stock available. However, Dealerweb provides various presentations to potential participants which provide an overview of the Platform. Further, all approved participants are granted access to Dealerweb Online Help which provides details of the various functions for each specific trading product, trading hours and order types. The Participant Agreement provides further details on Dealerweb's operations and services.

1.2.12. Fees. Exchange Act Rule 301(b)(4) is inapplicable to the Platform, however, in practice, Dealerweb generally complies with the rules or standards of practice governing fees established by FINRA, including FINRA Rule 2010 (Standards of Commercial Honor and Just and Equitable Principles of Trade) and FINRA Rule 2121 (Fair Prices and Commissions (also known as the 5% Rule)). While neither rule proscribes a specific limitation on the amount of fees that may be charged to a client with respect to effecting a securities transaction either as agent or principal, each rule requires that fees are implemented in a manner that is fair and reasonable under the circumstances. Fees are imposed based on Dealerweb's standard fee schedule that is provided to all clients at the time of onboarding and is available on its website.

1.2.13. Fair access. While the Platform is not currently required to comply with the "Fair Access" requirements of Exchange Act Rule 301(b)(5), Dealerweb monitors on an ongoing basis the level of trading activity that occurs on its ATS to ensure that it complies with the relevant rules relating to "Fair Access". More specifically, Exchange Act Rule 301(b)(5) requires an ATS that meets the trading volume thresholds to establish written standards for granting access to its system and apply those standards in a fair and non-discriminatory manner. With respect to the Platform, the "Fair Access" requirements are not applicable because the Platform is limited to the Treasury Products. Once the volume thresholds are met, the ATS, pursuant to Exchange Act Rule 301(b)(5)(C), is required to make and keep records of all grants and denials of access, including for all subscribers, the reason for granting or denying such access to the ATS. Such information is required to be filed with the SEC on a quarterly basis on Form ATS-R (see subsection 1.2.16 below). Dealerweb would maintain updated information regarding Canadian Participants who were provided with direct access and Canadian applicants for status as a Canadian Participant who were denied such status, and submit such information in a manner and form acceptable to the ATS Relief Decision Makers on a scheduled basis.

1.2.14. Capacity, integrity, and security of automated systems. Exchange Act Rule 301(b)(6) is not applicable because the Platform is limited to the trading of the Treasury Products. However, Dealerweb monitors on an ongoing basis the level of trading activity that occurs on its ATS to ensure that it complies with the relevant requirements of Exchange Act Rule 301(b)(6). More specifically, Exchange Act Rule 301(b)(6) requires an ATS that meets the trading thresholds to establish reasonable capacity estimates (both current and future), develop and implement procedures to review system development and testing methodology, review system vulnerability from external and internal threats, physical hazards and natural disasters and establish adequate contingency and disaster recovery plans. With respect to the last two items, Dealerweb, as a broker-dealer, is separately subject to such requirements; please see Section 7 of this Application for further information. While the Rule 301(b)(6) requirements are not applicable to Dealerweb as trading on the Platform is limited to the Treasury Products, Dealerweb adheres to certain key elements of this Rule as it conducts capacity testing, has processes and procedures in place to maintain the integrity of the Platform and implements security and access controls.

1.2.15. Recordkeeping. Pursuant to Exchange Act Rule 301(b)(8) as an ATS, Dealerweb shall make, keep and preserve certain records relating to the operation of its ATSs, including those records required to be maintained pursuant to Exchange Act Rule 302 and in the manner provided in Exchange Rule 303. For further detail, please see "Recordkeeping" at Section 9 below. Further, as a registered broker-dealer, Dealerweb is required pursuant to Section 17(a)(1) to make, keep, furnish and disseminate records and reports as prescribed by the SEC. The SEC's books and records rules applicable to broker-dealers, Exchange Act Rules 17a-3 and 17a-4, specify minimum requirements with respect to the records that broker-dealers must make, how long those records and other documents relating to a broker-dealer's business must be kept and in what format they may be kept. The SEC requires that broker-dealers create and maintain certain records so that, among other things, the SEC and self-regulatory organizations can use such records in the conduct of their examinations.

1.2.16. Reporting. Pursuant to Exchange Act Rule 301(b)(9), an ATS is required to file with the SEC on a quarterly basis the information required by Form ATS-R.

1.2.17. Form ATS-R (Quarterly Report of Alternative Trading System Activities) requires Dealerweb to provide the SEC with details relating to the operation of the ATS during the previous calendar quarter, including (but not limited to): (i) the total unit and dollar volume of transaction in various categories of securities; and (ii) a list of all persons granted, denied, or limited access to the ATS during the period covered by the report.

1.2.18. Written procedures to protect confidential trading information. Pursuant to Exchange Act Rule 301(b)(10) as an ATS, Dealerweb is required to establish adequate written safeguards and written procedures to protect subscribers' confidential trading information. Such written safeguards and written procedures must include:

i. limiting access to the confidential trading information of subscribers to those employees of the ATS who are operating the system or responsible for its compliance with these or any other applicable rules;

ii. implementing standards controlling employees of the ATS trading for their own accounts; and

iii. adopting and implementing adequate written oversight procedures to ensure that the written safeguards and procedures established are followed.

1.2.19. Finally, broker-dealers and ATSs that provide market access, including Dealerweb, are subject to an additional layer of regulatory oversight under Exchange Act Rule 15c3-5 (17 C.F.R. 240.15c3-5) (the Market Access Rule), which imposes additional financial and regulatory risk management controls and supervisory procedure requirements on the ATS or broker-dealer. This includes the requirement for Dealerweb to establish, maintain and ensure compliance with risk management and supervisory controls, policies, and procedures that are reasonably designed to manage, in accordance with prudent business practices, the financial, regulatory and other risks associated with market access or providing clients with market access. These risk management and supervisory controls, policies and procedures are required to be reasonably designed to ensure that all orders are monitored and include pre-trade controls and regular post-trade review. Under the Market Access Rule, a broker-dealer must preserve a copy of its supervisory procedures and a written description of its risk management controls as part of its books and records obligations under SEC Rule 17a-4.

1.2.20. Additionally, the risk management controls and supervisory procedures required pursuant to the Market Access Rule must be reasonably designed to systematically limit the financial exposure of the broker-dealer (e.g., preventing the entry of one or more orders that exceed pre-determined price or size parameters); ensure compliance with the broker-dealer's regulatory obligations (e.g., restricting access to trading systems and technology that provide market access to persons and accounts pre-approved and authorized by the broker-dealer); and ensure that the entry of orders does not interfere with fair and orderly markets.

1.2.21. A broker-dealer's risk management controls and supervisory procedures should be reasonably designed to:

(a) prevent the entry of orders that exceed appropriate pre-set credit or capital thresholds in the aggregate for each customer and the broker or dealer and, where appropriate, more finely-tuned by sector, security, or otherwise by rejecting orders if such orders would exceed the applicable credit or capital thresholds; and

(b) prevent the entry of erroneous orders, by rejecting orders that exceed appropriate price or size parameters, on an order-by-order basis or over a short period of time, or that indicate duplicative orders.

1.2.22. Under the Market Access Rule, a broker-dealer must (a) regularly assess and document the adequacy and effectiveness of its risk management and supervisory controls, policies and procedures; and (b) document any material deficiencies in the adequacy or effectiveness of a risk management or supervisory control, policy or procedure and promptly remedy these deficiencies.

1.2.23. Broker-dealers are also subject to the general supervision and monitoring requirements of FINRA Rule 3110, which requires broker-dealers to establish and maintain a system to supervise the broker-dealer's business and the activities of each associated person employed by the broker-dealer that is reasonably designed to achieve compliance with applicable securities laws and regulations, and with applicable FINRA rules.

1.2.24. Dealerweb must continue to fulfil these obligations to maintain its registration and ability to operate the Platform. Among other things, Dealerweb is required to:

(a) have systems and controls in place to monitor transactions on the Platform;

(b) retain sufficient financial resources for the performance of its functions as ATS operator;

(c) operate the Platform with due heed to the protection of investors;

(d) ensure that trading is conducted in an orderly and fair manner;

(e) maintain suitable arrangements for trade reporting;

(f) maintain suitable arrangements for the clearing and settlement of contracts;

(g) monitor compliance with the SEC, FINRA, and MSRB rules, and the rules of the Platform;

(h) investigate complaints with respect to its business;

(i) maintain high standards of integrity and fair dealing; and

(j) prevent abuse.

1.2.25. On July 25, 1987 the SEC approved Dealerweb as a broker-dealer and on January 23, 2009 Dealerweb was approved as an ATS. Dealerweb remains compliant with its regulatory requirements as demonstrated by its continued status as an ATS.

1.2.26. FINRA and the SEC are the authorities charged with ensuring that ATSs (such as Dealerweb) continue to comply with their regulatory requirements. FINRA and the SEC have the power to direct any ATS that is failing, or has failed, to comply with any applicable rules or regulations to take action to remedy such non-compliance. It also has the power to revoke or suspend the registration of any ATS that fails to meet its regulatory requirements. Accordingly, Dealerweb is subject to the oversight of FINRA and the SEC.

1.2.27. Regulation ATS was most recently amended in 2018, such amendment being a significant tightening of the regulation and a signal from the SEC that strict ATS regulation is among the SEC's regulatory priorities.

Rules and policy statements

1.2.28. As noted above, the primary regulatory frameworks governing broker-dealer activity in the US include the Securities Act and the Exchange Act (and the rules and regulations promulgated thereunder, including Regulation ATS), FINRA and MSRB rules, FinCEN AML and KYC rules and regulations, and state securities rules and regulations. SEC and FINRA also publish guidance and regulatory interpretations, including through SEC no-action letters, and FINRA regulatory notices.

Financial protections afforded to customer funds

1.2.29. The Platform operated by Dealerweb does not hold any customer funds or securities.

Authorization, licensure or registration of the alternative trading system

1.2.30. As noted above, ATSs, including Dealerweb are subject to a comprehensive regulatory framework in the US. Subject to certain limited exceptions, all US ATSs must be registered with the SEC as a broker-dealer and be a member of FINRA. In this regard, ATSs are subject to extensive regulation and oversight by the SEC and FINRA, not only with respect to ATS operation, but also with respect to the broker-dealer's operations as a whole. Failure to comply with the obligations pursuant to this regulatory framework can lead to suspension, fines, and other sanctions, including the cessation of the operations of an ATS operated by a broker-dealer.

1.2.31. As set forth in greater detail below, broker-dealers in the US are subject to routine and for-cause examinations by the SEC and FINRA. Broker-dealers are also subject to periodic financial and operational reporting (monthly and annually) through the filing of FOCUS Reports, which are filed with FINRA. Further, a broker-dealer is subject to a number of self-reporting obligations imposed by the SEC and FINRA, including the requirement to self-report certain events pursuant to FINRA Rule 4530 (as discussed in greater detail below) and file and keep current certain information with respect to the broker-dealer's business and operations on Form BD and Form ATS. In addition, pursuant to FINRA Rule 3110 and 3130, a broker-dealer's chief executive officer (or equivalent officer) must certify annually that the broker-dealer has in place processes to establish, maintain, review, test and modify written compliance policies and written supervisory procedures reasonably designed to achieve compliance with applicable FINRA rules, MSRB rules, and federal securities laws and regulations. This report must be supported by an underlying report and discussion with the broker-dealer's chief compliance officer with respect to the same. FINRA Rule 3130 also requires the compliance report underlying this certification be submitted to the broker-dealer's board of directors and audit committee.

The foreign regulator's approach to the detection and deterrence of abusive trading practices, market manipulation, and other unfair trading practices or disruptions of the market

1.2.32. To begin, pursuant to FinCEN rules and regulations, broker-dealers are required to file with FinCEN, a Suspicious Activity Report (SAR) to report any suspicious transaction or pattern of transactions relevant to a possible violation of law or regulation, including, but not limited to, transactions involving market manipulation, wash trading, or insider trading.

1.2.33. Additionally, broker-dealers and market participants are subject to a number of rules and regulations with respect to securities fraud, market manipulation, and abusive trading practices. Section 10(b) of the Exchange Act and SEC Rule 10b-5 promulgated thereunder prohibits any act, practice, or course of business which operates or would operate as a fraud or deceit upon any person. More specific conduct is also addressed in other SEC and FINRA rules and regulations, including, but not limited to: Exchange Act Section 9 (prohibition against manipulation of security prices); FINRA Rule 5210 (which prohibits the publication of manipulative and deceptive quotations, self-trades, disruptive quoting and trading activity); and FINRA Rule 6140 (which outlines certain prohibitions with respect to the sale of NMS securities).

1.2.34. As noted above, the SEC and FINRA conduct surveillance programs that collect and integrate trading data across broker-dealers (including ATSs) to detect abusive activity and conduct an examination program to review how broker-dealers handle orders, including how they keep order information and other sensitive client information confidential. This examination, supervision, and reporting framework also assesses financial and operational condition of broker-dealers.

1.2.35. Further, broker-dealers in the US are also subject to certain best execution obligations under FINRA Rule 5310, which generally requires that in any transaction for or with a customer or a customer of another broker-dealer, a broker-dealer and persons associated with the broker-dealer, must use reasonable diligence to ascertain the best market for the subject security, and buy or sell in such market so that the resultant price to the customer is as favorable as possible under prevailing market conditions.

1.2.36. Dealerweb has implemented post trade monitoring reports, which are triggered when certain types of trading activity may have occurred on the Platform, e.g., wash trading and spoofing.

Laws, rules, regulations and policies that govern the authorization and ongoing supervision and oversight of market intermediaries in the US

1.2.37. The US has a comprehensive financial services regime. The laws, rules, regulations and policies that govern the authorization and ongoing supervision and oversight of market intermediaries, include, but are not limited to, the Securities Act and the Exchange Act (and the rules and regulations promulgated thereunder), the Investment Company Act of 1940, the Investment Advisers Act of 1940, the rules and regulations of the US Commodities Futures Trading Commission, the rules of FINRA, the MSRB, and the NFA, FinCEN AML and KYC rules and regulations, and state securities rules and regulations.

1.2.38. Of the participants that have trading rights, and could therefore deal with customers located in the Jurisdictions, the vast majority are companies incorporated in the US.

Procedures for dealing with the failure of a market intermediary in order to minimize damage and loss to investors and to contain systemic risk for market intermediaries who may deal with members and other participants located in the Jurisdictions

1.2.39. FINRA members, such as Dealerweb, are required to maintain membership with the Securities Investor Protection Corporation (SIPC). SIPC was created under the Securities Investor Protection Act of 1970 (SIPA) as a non-profit membership corporation. SIPC oversees the liquidation of member firms that close when the firm is bankrupt or in financial trouble, and customer assets are missing. In a liquidation under the SIPA, SIPC and a court-appointed trustee work to return customers' funds and securities as quickly as possible. Within limits, SIPC expedites the return of missing customer property by protecting each customer up to $500,000 for funds and securities (including a $250,000 limit for cash only).

Examination and reporting requirements

1.2.40. As set forth above, the SEC and FINRA exercise their supervisory responsibility by conducting examinations of whether Dealerweb's rules, procedures and practices are adequate for the protection of investors and for the maintenance of an orderly market.

1.2.41. Broker-dealers in the US, including Dealerweb, are subject to periodic examinations by FINRA and the SEC. Types of examinations include: (i) cause examinations, which are initiated in order to investigate some particular issue or event; (ii) sweep examinations, in which multiple firms receive, and must respond to, written inquiries regarding a particular issue; and (iii) cycle examinations, which occur periodically over the life of the broker-dealer. Both FINRA and the SEC conduct examinations of these kinds, and both have considerable resources, and staff, to conduct such examinations.

1.2.42. During examinations, the examination staff seek to determine whether the entity being examined is: conducting its activities in accordance with the federal securities laws and rules adopted under these laws, as well as the rules of self-regulatory organizations, such as FINRA; adhering to the disclosures it has made to its clients, customers, the general public and/or the SEC and FINRA; and implementing supervisory systems and/or compliance policies and procedures that are reasonably designed to ensure that the entity's operations are in compliance with applicable legal requirements.

1.2.43. In addition, as described above, pursuant to Regulation ATS, each ATS, including Dealerweb, must file an initial operation report with the SEC on Form ATS, prior to commencing operations. Form ATS requires detailed disclosures regarding a wide range of information concerning the ATS, its owners, its businesses, and its operating procedures, including disclosure to the applicable regulators (FINRA and the SEC) of the subscriber terms (and/or user guide(s)). Form ATS serves as a supplement to Form BD, which is filed by firms seeking registration with the SEC as broker-dealers, and the new membership application process, which is required for broker-dealers to become members of FINRA. Information required to be provided in these forms and applications include ownership and corporate governance information, affiliate information, details regarding the manner of operation of the ATS and its associated functions, including the structure, means of access, description of trade reporting procedures, contingency planning, and marketplace participants, similar to the information that is required to be provided to the Canadian securities regulators in a Form 21-101F2.

1.2.44. Form ATS and Form BD must be amended, as necessary, to correct any previously provided information that becomes inaccurate for any reason. Amendments include changes to information regarding Dealerweb's ownership, corporate governance information, affiliate information, details regarding the manner of operation of the ATS and its associated functions, including the structure, means of access, description of trade reporting procedures, contingency planning and marketplace participants, similar to the information that is required to be provided to the Canadian securities regulators in a Form 21-101F2.

1.2.45. In addition, as noted above, pursuant to FINRA Rule 3110 and 3130, a broker-dealer's chief executive officer (or equivalent officer) must certify annually that the broker-dealer has in place processes to establish, maintain, review, test and modify written compliance policies and written supervisory procedures reasonably designed to achieve compliance with applicable FINRA rules, MSRB rules, and federal securities laws and regulations. This report must be supported by an underlying report and discussion with the broker-dealer's chief compliance officer with respect to the same. FINRA Rule 3130 also requires the compliance report underlying this certification be submitted to the broker-dealer's board of directors and audit committee.

1.2.46. Pursuant to SEC and FINRA rules, broker-dealers are subject to periodic financial and operational reporting (monthly and annually) through the filing of FOCUS Reports, which are filed with FINRA. The net capital rule, Exchange Act Rule 15c3-1 (17 C.F.R. §240.15c3-1), is the principal rule by which the financial health of US broker-dealers, including Dealerweb, is regulated and monitored. The net capital rule requires US broker-dealers to maintain "net capital" (i.e., capital in excess of liabilities) in specified amounts that are determined by the types of business conducted by the broker-dealer. The net capital rule requires broker-dealers to compute net worth based on US generally accepted accounting principles (GAAP), as modified by the various provisions and interpretations of the rule.

1.2.47. Regulation ATS also requires Dealerweb, as an ATS, to permit the examination and inspection of its premises, systems, and records, and cooperate with the examination, inspection, or investigation of subscribers, whether such examination is being conducted by the SEC or by a self-regulatory organization of which such subscriber is a member.

1.2.48. Regulation ATS also requires that Dealerweb, as an ATS, report information regarding marketplace activity on a quarterly basis on Form ATS-R, including for example, general trading activity, fixed income activity, and traded fixed income securities, similar to certain information a Canadian ATS is required to provide in Form 21-101F3 Quarterly Report of Marketplace Activities (Form 21-101F3).

1.2.49. Finally, a FINRA-member broker-dealer is required under FINRA Rule 4530 to report to FINRA certain specified events, including the broker-dealer's conclusion that it has discovered significant, widespread, or systemic violations of securities and investment related laws by the broker-dealer or any of its associated persons. Rule 4530 not only requires self-reporting of violations of securities law and regulation, but also of specified events, such as certain criminal convictions, certain customer complaints, and ongoing regulatory actions. Finally, the self-reporting and reporting rule also requires that a broker-dealer report to FINRA certain statistical and summary information regarding written customer complaints on a quarterly-basis.

1.2.50. Regulation ATS requires that an ATS, including Dealerweb, that intends to cease carrying on business as an ATS must file a cessations report with the SEC promptly upon ceasing to operate as an ATS. This requirement is similar to the requirement for a Canadian ATS to provide prior notice to the regulator of an intention to cease carrying on business as an ATS and the requirement to file a Form 21-101F4 Cessation of Operations Report for Alternative Trading System.

The protection of customer funds and securities by market intermediaries who may deal with Canadian Participants

1.2.51. The Exchange Act Rule 15c3-3, which is commonly known as the "customer protection rule," is intended to protect customers' funds held by their broker-dealers and prohibit broker-dealers from using customer funds and securities to finance any part of their business that is unrelated to servicing securities customers. The rule requires a broker-dealer that maintains custody of customer securities and cash to comply with two primary requirements. First, the rule requires broker-dealers to maintain physical possession or control over customers' fully paid and excess margin securities. For purposes of the first requirement, physical possession or control means that the broker-dealer must hold fully paid and excess margin securities in certain specified locations and that the securities shall remain free of any liens or other security interests. One such permissible location is a US bank; another such location is on the books and records of a registered clearing agency, such as certain subsidiaries and affiliates of the DTC. As a practical matter, most fixed-income securities are held by DTC (or an affiliate of DTC). A broker-dealer can establish possession and control for purposes of the customer protection rule by holding securities in non-US control locations (called "foreign control locations"); provided that the non-US custodian provides certain representations to the US broker-dealer regarding the status of the securities and the absence of liens.

1.2.52. Second, the broker-dealer must maintain a reserve of cash or qualifying securities in an account at a bank that is at least equal in value to the net cash the broker-dealer owes to customers. The calculation of net cash set forth in the customer protection rule requires that the broker-dealer add all customer credit items (such as an amount equal to any free cash in customer securities accounts) and deduct from such credit items, any customer debit items (such as margin loans). The net amount by which customer credit items exceed customer debit items, if any, must be on deposit in the broker-dealer's customer reserve account.

1.2.53. Deposits in the broker-dealer's customer reserve account must take the form of cash or certain qualifying securities. Generally, weekly computations of the reserve are required. The reserve account is for the exclusive benefit of customers, and as such, funds may not be withdrawn unless an updated reserve formula calculation reflects that the reserve requirement has decreased.

1.2.54. As noted above, an additional layer of customer protection, FINRA members, such as Dealerweb, are required to maintain membership with SIPC.

Article 2 GOVERNANCE

2.1. Governance -- the governance structure and governance arrangements of the alternative trading system ensure:

(a) Effective oversight of Dealerweb and the Platform

2.1.1. Dealerweb has independent departments handling product development, testing, change management (code deployment), infrastructure and system operation. Further, Dealerweb employs real-time monitoring of the ATS with end-of-day checks by management. Trades, and trading in employee personal accounts, are also regularly reviewed by a third-party, compliance consulting firm.

2.1.2. The Dealerweb Technology Support and Development Departments are responsible for all new development, upgrades, product development and management, quality assurance, production support, network, and system administration of the Platform, including its applications, the matching engine, market data systems, networks and environments. The development group is responsible for development of new products, maintenance of existing products, and resolution of any systems issues. Within the Technology Support and Development Departments, the Quality Assurance group is responsible for testing of all new code, bug fixes, and patches produced by the development teams. The Dealerweb Production Support Department is solely responsible for all migration of new code, bug fixes, patches, configuration changes, upgrades, etc. to the production environment.

2.1.3. Internal control processes are monitored on an ongoing basis. This monitoring helps to determine whether control deficiencies identified are addressed and includes regular management and supervisory activities.

2.1.4. Dealerweb's controls provide reasonable assurance that application and system processing on the Platform relevant to clients' internal control over financial reporting are authorized and executed in a complete, accurate, and timely manner and deviations, problems, and errors that may affect clients' internal control over financial reporting are identified, tracked, recorded, and resolved in a complete, accurate, and timely manner.

2.1.5. Dealerweb is a wholly-owned subsidiary of Tradeweb Markets LLC, a leading operator of electronic marketplaces.

(b) Appropriate provisions for directors and officers

2.1.6. The Dealerweb board of directors is comprised of three individuals. Each director is an employee of Tradeweb Markets Inc., the parent company of Dealerweb and, because of this, none of the directors are independent.

2.1.7. The directors are elected at each annual meeting of shareholders of Dealerweb and in accordance with the terms of Dealerweb's constating documents and applicable corporate law. Dealerweb takes reasonable steps to ensure: (i) appropriate qualifications, remuneration, limitation of liability and indemnity provisions for directors and officers; and (ii) each officer and director is a fit and proper person. While FINRA does not review or approve the directors, each director is registered with FINRA and is subject to all FINRA rules and requirements. The directors are subject to the duties and obligations imposed under New York law. The directors and officers of Dealerweb also have the benefit of directors' and officers' liability insurance.

2.1.8. Each director has experience in the financial and securities markets and is nominated on the basis of his or her skills, qualifications and experience. The directors have extensive experience in fixed-income trading and the operation of electronic marketplaces. Each director is subject to detailed disclosure requirements under Form BD, which includes information as to criminal or civil sanctions and regulatory actions, and such disclosures are publicly accessible on Dealerweb's Form BD filing.

(c) Dealerweb has policies and procedures to appropriately identify and manage conflicts of interest

2.1.9. Dealerweb has established, maintains and reviews compliance with policies and procedures that identify and manage any conflicts of interest arising from the operation of the marketplace or the services it provides.

2.1.10. Further, there is no proprietary trading on the Platform by Dealerweb or any of its affiliates which reduces the possibility that Dealerweb will have a conflict of interest with a participant.

2.1.11. Directors, officers and employees of Dealerweb are prohibited from acting as directors, employees or consultants of any competitor to Dealerweb. All employees of Dealerweb are subject to Dealerweb's Code of Conduct which sets out the controls implemented to identify, manage and disclose conflicts of interest.

2.1.12. To ensure compliance with FINRA Rules 3110 and 3310, MSRB Rules G-27 and G-41, Dealerweb has implemented compliance policies and procedures outlining its regulatory obligations and written supervisory procedures and designed to achieve compliance with applicable securities laws and regulations. As a broker-dealer, Dealerweb has an obligation to identify and respond to existing material conflicts of interest and any material conflicts of interest it expects to arise between Dealerweb, including each individual acting on Dealerweb's behalf, and a subscriber or other party. Further, Dealerweb must design its organizational structures, lines of reporting and physical locations to control conflicts of interest. Dealerweb must ensure that before or at the time it provides a service that gives rise to a conflict, that it discloses the conflict. Dealerweb also produces an annual compliance report which addresses these issues.

2.1.13. Dealerweb has implemented effective oversight procedures, including compliance monitoring and testing, internal and external risk assessments, and annual internal, external and regulatory audits, to ensure that the safeguards and procedures established by Dealerweb are followed.

Article 3 REGULATION OF PRODUCTS

3.1. Review and Approval of Products -- Business lines must be approved by the Foreign Regulator

3.1.1. The SEC and FINRA establish a range of requirements that must be met before any new product is admitted for trading on the Platform. New products must be capable of being traded in a fair, orderly and efficient manner and the ATS must be designed so as to allow for its orderly pricing.

3.1.2. Business lines, including the operation of an ATS, must be approved by FINRA, listed on a broker-dealer's Form BD, as filed with the SEC, and listed on the broker-dealer's membership agreement with FINRA. Any addition of business lines to Dealerweb must be approved by FINRA prior to implementation by the broker-dealer.

3.1.3. Pursuant to Regulation ATS, when filing its initial operation report on Form ATS, an ATS is required to provide the SEC with a list of the types of securities the ATS trades or expects to trade, as well as a list of the securities the ATS trades or expects to trade. As noted above, an ATS is required to update its Form ATS, as necessary, to correct any previously provided information that becomes inaccurate for any reason. Canadian Participants will only be able to trade the Treasury Products on the Platform.

3.1.4. Pursuant to FINRA Rule 3110, each broker-dealer must establish, maintain, and enforce written procedures to supervise the activities of its registered representatives and associated persons that are reasonably designed to achieve compliance with applicable securities laws and regulations and with applicable FINRA rules. In this regard, Dealerweb must ensure that the operation of the Platform, as well as the Operating Procedures, comply with applicable securities laws and regulations and with applicable FINRA rules. In addition, the Market Access Rule, which Dealerweb is subject to, imposes additional financial and regulatory risk management controls and supervisory procedure requirements on the ATS or broker-dealer. This includes the requirement for Dealerweb to establish, maintain and ensure compliance with risk management and supervisory controls, policies, and procedures that are reasonably designed to manage, in accordance with prudent business practices, the financial, regulatory and other risks associated with market access or providing clients with market access.

3.1.5. Dealerweb maintains adequate provisions to measure, manage and mitigate the risks associated with trading products on the ATS as required by regulation. These include, but are not limited to, conformance to daily trading limits, 'market access' controls (SEC 15c3-5) and internal controls.

Article 4 ACCESS

4.1. The requirements of the ATS relating to access to the facilities of the ATS are fair, transparent and reasonable

a) has written standards for granting access to trading on its facilities to ensure users have appropriate integrity and fitness;

b) has and enforces financial integrity standards for those persons who enter orders for execution on the system, including, but not limited to, credit or position limits and clearing membership;

c) does not unreasonably prohibit or limit access by a person or company to services offered by it;