Notice and Request for Comment – Application for an Exemption from the Marketplace Rules – LedgerEdge Limited

A. Background

LedgerEdge Limited (LedgerEdge) has applied for an exemption from National Instrument 21-101 Marketplace Operation (NI 21-101), National Instrument 23-101 Trading Rules (NI 23-101) and National Instrument 23-103 Electronic Trading and Direct Electronic Access to Marketplaces (NI 23-103 and, together with NI 21-101 and NI 23-103, the Marketplace Rules) in their entirety.

LedgerEdge is registered as a multilateral trading facility (MTF) with the U.K. Financial Conduct Authority (FCA). LedgerEdge operates and maintains an electronic trading platform that facilitates the trading of European and U.S. high-grade bonds and high-yield bonds, sovereign, supranational and agency bonds, non-Canadian government bonds and emerging market bonds.

B. Requested Relief

LedgerEdge requests relief from the Marketplace Rules. In the application, LedgerEdge has outlined how it meets the criteria for exemption from the Marketplace Rules set out in CSA Staff Notice 21-328 Regulatory Approach to Foreign Marketplaces Trading Fixed Income Securities.{1} The application and draft exemption order are attached as Annexes A and B, respectively, to this notice.

C. Comment Process

We are seeking public comment on all aspects of LedgerEdge's application and draft exemption order. Please provide your comments in writing, via e-mail, on or before June 13, 2022 to:

Market Regulation Branch

Ontario Securities Commission

20 Queen St. West, 22nd Floor

Toronto, ON, M5H 3S8

[email protected]

Questions may be referred to:

Emily Park

Legal Counsel

Market Regulation

Ontario Securities Commission

[email protected]Ruxandra Smith

Senior Accountant

Market Regulation

Ontario Securities Commission

[email protected]

{1} Available at https://www.osc.ca/en/securities-law/instruments-rules-policies/2/21-328/csa-staff-notice-21-328-regulatory-approach-foreign-marketplaces-trading-fixed-income-securities

ANNEX A

Ramandeep Grewal

Direct: 416 869-5265

[email protected]

|

May 4, 2022 |

By Email |

|

Ontario Securities Commission |

|

|

20 Queen Street West |

|

|

Suite 1900, Box 55 |

|

|

Toronto, Ontario M5H 3S8 |

|

|

Fax: (416) 593-2318 |

|

|

Attention: Secretary to the Commission |

|

Dear Sirs/Mesdames:

Re: LedgerEdge Limited ("LedgerEdge" or the "Applicant") -- Application for an exemption pursuant to Section 15.1(2) of National Instrument 21-101 Marketplace Operation ("NI 21-101") in whole, pursuant to Section 12.1(2) of National Instrument 23-101 Trading Rules ("NI 23-101") for an exemption from NI 23-101 in whole and pursuant to Section 10(2) of National Instrument 23-103 Electronic Trading and Direct Electronic Access to Marketplaces ("NI 23-103" and, together with NI 21-101 and NI 23-101, the "Marketplace Rules") for an exemption from NI 23-103 in whole, with respect to Marketplace Rules that apply to an Alternative Trading System ("ATS")

We are Canadian counsel to, and are filing this application (the "Application") with the Ontario Securities Commission (the "OSC") on behalf of the Applicant for an order granting the Requested Relief, as defined below.

Requested Relief

On behalf of LedgerEdge, we are applying for an order granting the following decisions under the Ontario securities legislation (the "Legislation"):

1) Pursuant to Section 15.1(2) of NI 21-101 for an exemption from NI 21-101 in whole;

2) Pursuant to Section 12.1(2) of NI 23-101 for an exemption from NI 23-101 in whole; and

3) Pursuant to Section 10(2) of NI 23-103 for an exemption from NI 23-103 in whole,

exempting LedgerEdge from the application of all provisions of the Marketplace Rules that apply to a person or company carrying on business as an alternative trading system ("ATS") (collectively, the "Requested Relief").

The Applicant is registered and regulated in the United Kingdom as a multilateral trading facility ("MTF"). LedgerEdge trading platform (the "Platform") facilitates trading in fixed income securities (corporate, government and public non-Canadian debt securities). Pursuant to the CSA Staff Notice 21-322 Applicability of Regulation to the Operation of MTFs or OTFs in Canada (the "CSA Staff Notice 21-322"), if an MTF offers or intends to offer access to Canadian participants, it is considered to be "carrying on business" in Canada and is subject to the requirement to register as an ATS, or seek recognition as an exchange, as applicable, in the jurisdictions of Canada where it has Canadian resident clients. LedgerEdge trading platform's operation and functionalities are akin to those of an ATS in that:

• the LedgerEdge MTF trading system is multilateral and brings together multiple third-party buying and selling interests in financial instruments;

• trading arrangements have a characteristic of a system, as the Platform operates in accordance with a set of defined rules setting the parameters through which orders can interact (as set out in the LedgerEdge Rulebook);

• the execution of transactions will take place on the trading system and in accordance with the rules of the trading system;

• once orders are matched in the trading system, a contract which is in accordance with the applicable legislation (i.e. Title II of MiFID) will be formed;

• orders will be matched on the trading system in accordance with non-discretionary rules and LedgerEdge as the operator of the trading system will have no discretion in relation to the matching of orders;

• LedgerEdge does not require any issuer to enter into an agreement to have its securities traded on the trading system;

• LedgerEdge does not provide, directly or through one or more subscribers, a guarantee of a two-sided market for a security or derivative on a continuous or reasonably continuous basis;

• LedgerEdge does not set requirements governing the conduct of participants, other than conduct in respect of the trading by those participants on the trading system; and

• LedgerEdge does not have any regulatory or enforcement powers over the participants on the trading system, other than the authority to terminate, suspend or limit the participants' access to the trading system in case of misconduct and does not discipline participants other than by exclusion from participation in the trading system.

The Applicant currently anticipates having Canadian clients resident in Ontario only. In Ontario, an ATS is regulated as a marketplace under NI 21-101. On March 5, 2020, the Canadian Securities Administrators ("CSA") published CSA Staff Notice 21-328 Regulatory Approach to Foreign Marketplaces Trading Fixed Income Securities (the "CSA Staff Notice 21-328") providing a regulatory framework that describes the approach to evaluate requests for, and determine whether to recommend, the granting of exemptions from the Marketplace Rules to foreign fixed income ATSs that request to carry on business in Canada. The CSA staff have provided a rationale that if a foreign fixed income ATS is subject to a comparable regulatory regime in its home jurisdiction that meets certain criteria and that can be relied on for investor protection and the promotion of a fair and efficient market, it would not be contrary to the public interest to allow for the foreign fixed income ATS to carry on activities with Canadian participants under its home jurisdiction regime without the need for regulatory duplication, provided that the foreign fixed income ATS complies with relevant terms and conditions imposed on its operations within Canada by the Canadian securities regulatory authorities. These terms and conditions are set out in Schedule A to the CSA Staff Notice 21-328. According to the Staff Notice 21-328, the ultimate aims of the proposed foreign fixed income ATS exemption regime are to avoid market fragmentation and reduce regulatory duplication and burden while facilitating investor protection and promoting a fair and efficient market.

The Applicant submits that the MTF regulatory regime of its home jurisdiction applicable to the Platform is sufficiently comprehensive and comparable to the ATS regulatory regime imposed by the Marketplace Rules in Ontario to justify granting an exemption from such requirements, such that the balance between having efficient capital markets and protecting public interest would be achieved and the granting of the Requested Relief would be warranted.

The CSA Staff Notice 21-328 prescribes criteria for a foreign fixed income ATS to obtain the Requested Relief. These criteria are listed in Appendix A to this Application and include, among other, how the foreign fixed income ATS is regulated in its home jurisdiction and what authority and procedures the home regulator has in place for oversight of the foreign fixed income ATS.

The Applicant submits that it has provided the information required by the OSC to determine that the Applicant is able to substantially meet or otherwise address the criteria listed in the CSA Staff Notice 21-328.

Reference will be made in this Application to the LedgerEdge Rulebook (the "LedgerEdge Rulebook"), which is available on the LedgerEdge website at: https://ledgeredge.com/legal-center/. The LedgerEdge rules are contained in the LedgerEdge Rulebook (the "LedgerEdge Rules") and are separated into 30 sections, each focusing on a specific area. The LedgerEdge Rulebook is the governing document for the system. In order to become users, applicants must undertake to be bound by the LedgerEdge Rules.

For convenience, this Application is divided into the following Parts, which address each of the criteria prescribed in the CSA Staff Notice 21-328:

Section 1 -- Background

Section 2 -- Application of Approval Criteria to the ATS

1. Regulation of the ATS

2. Governance

3. Regulation of Products

4. Access

5. Regulation of Participants on the ATS

6. Clearing and Settlement

7. Systems and Technology

8. Outsourcing

9. Transparency and Reporting

10. Record Keeping

11. Financial Viability

12. Fees

13. Information Sharing and Oversight Arrangements

14. IOSCO Principles

Section 3 -- Submissions

Section 4 -- Other Matters

SECTION 1 -- Background

1.1. Description of LedgerEdge and its business

1. LedgerEdge is a private company limited by shares, existing under the Companies Act 2006 of the United Kingdom (the "U.K."), with its head office located in London, England, U.K.

2. LedgerEdge was founded in 2020 and operates as the electronic service provider of a trading platform for institutional clients (the "Platform") that facilitates trading in European and U.S. high-grade bonds and high-yield bonds, sovereign, supranational and agency bonds, non-Canadian government bonds and emerging market bonds (collectively, the "Fixed Income Securities"). The Platform will use distributed ledger technology to manage pre-trade information flows. At the time of submitting the Application, LedgerEdge has 27 potential buy-side and sell-side institutional clients and will commence operating the Platform in May 2022. LedgerEdge does not provide access to any retail clients.

3. LedgerEdge has obtained permission to operate as an MTF in relation to corporate, government and public securities and to deal as agent from the U.K. Financial Conduct Authority (the "FCA"), a U.K. equivalent of the OSC. As such, LedgerEdge has obtained the following permissions:

(a) Agreeing to carry on a regulated activity pursuant to article 64 of the Financial Services and Markets Act 2000 (Regulated Activities) Order 2001 ("RAO");

(b) Operation of a MTF (article 25D RAO); and

(c) Dealing in investments as agent (article 21 RAO).

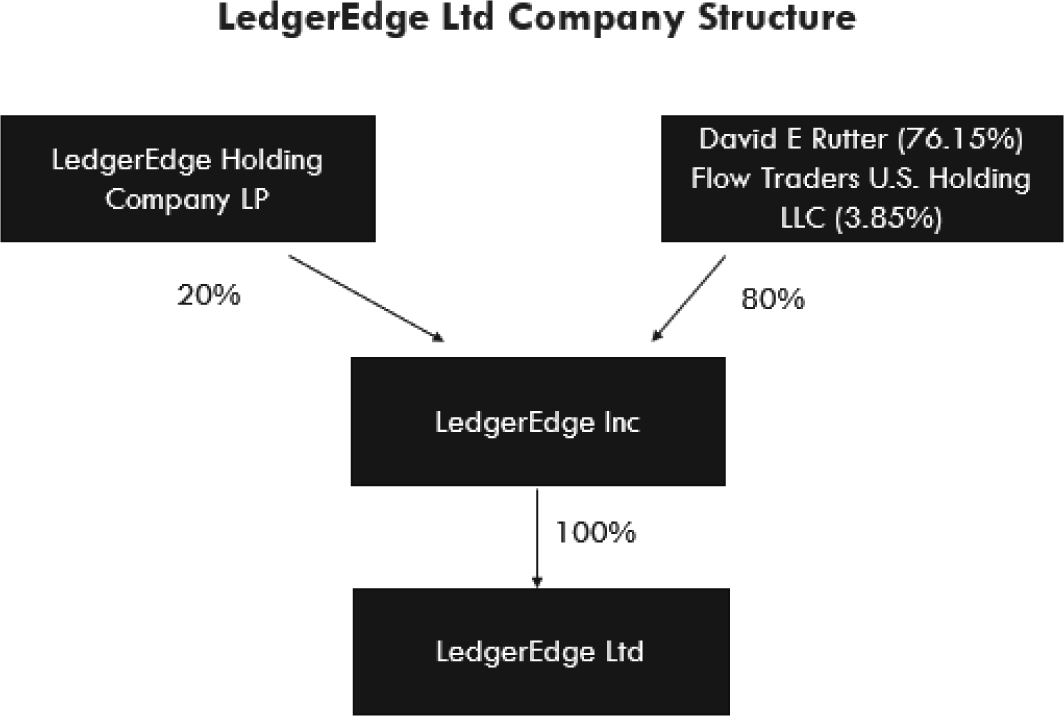

4. LedgerEdge operates as an MTF under FCA Rules. LedgerEdge is a wholly-owned subsidiary of LedgerEdge Inc., which is controlled 76.15% by Co-Founder David E. Rutter, 3.85% by Flow Traders U.S. Holding LLC and 20% by LedgerEdge Holding Company LP. All entities are under common management and control, and the corporate structure is as set out below.

5. Trading of Fixed Income Securities is facilitated through the Platform, which is intended to bring together multiple buyers and sellers of corporate, government and public securities in the European Union ("EU") and the U.K. The buying and selling of MiFID financial instruments (corporate, government and public security) will be governed by non-discretionary rules in a way that results in contracts on the Platform. LedgerEdge will have no discretion in determining how the members on the Platform interact with each other. However, LedgerEdge has established rules governing how the system operates and the characteristics of the quotes and orders that determine the resulting trades.

6. The onboarding documentation required by LedgerEdge includes an agreement signed by the onboarding client agreeing to the terms and conditions of the use of the Platform (the "Participation Agreement") and Operational Specifications that set out further technical information regarding the Platform to be read in conjunction with the LedgerEdge Rulebook and that are binding on participants on the Platform ("Participants").

7. The Platform offers access to multiple protocols which run in parallel on the LedgerEdge Platform. The Resting Protocol allows both liquidity providers and liquidity consumers to enter firm orders by submitting bids and offers. Orders are considered filled once the orders have matched and are captured in the central database. If an order is not accepted or rejected by the liquidity provider and the order is flagged as such, it shall expire and the liquidity provider would be required to resubmit that order on the Platform.

8. LedgerEdge also runs an Executable Streaming Price Protocol ("ESP Protocol"), that provides liquidity providers with the opportunity to offer an ESP. Liquidity Consumers are then able to stream bids and offers from other Participants. As ESP orders are subject to liquidity provider's confirmation, the liquidity provider must confirm or reject a trade request within a time period specified in the Operational Specifications.

9. LedgerEdge also runs a Request for Quote Protocol ("RFQ Protocol") through which liquidity providers can respond to the requests of liquidity consumers that are initiated as RFQ. When a liquidity consumer creates an RFQ, the liquidity providers to whom the request is submitted may respond with a quote. If the quote is accepted, the order is considered "filled" once it is captured in the central database.

10. Under the Volume Matching Protocol, LedgerEdge will set a volume matching price in respect of a particular product. The price will be based either on (i) the most recent trade on the Platform, or (ii) in the absence of a recent trade, pricing information regarding that instrument drawn from the Platform or market. When the volume matching session starts, Participants can then submit orders for that particular instrument at the volume matching price, specifying the volume that they wish to trade. An engine will match pairs of orders and create matched trades and send these to the counterparties and to the Company Settlement Partner (as defined below) for onward settlement. The length of the volume matching session is set by LedgerEdge (and may vary in length, at the sole decision-making authority of LedgerEdge as the operator of the Platform). Any unmatched order will be removed at the end of the volume matching session.

11. Finally, LedgerEdge also runs a Process Trades Protocol in which Participants may arrange a potential trade between themselves off venue in an Eligible Instrument (as defined in the LedgerEdge Rulebook) that is to be submitted to the Platform for execution pursuant to the LedgerEdge Rulebook (a "Process Trade"). The terms of a Process Trade must be submitted to the Platform in a manner prescribed from time to time by LedgerEdge. Both Participants shall confirm Process Trades on the Platform within fifteen (15) minutes of being arranged, or sooner, if technologically practicable. The transaction will not be deemed to become executed pursuant to the LedgerEdge Rules until it has been confirmed on the Platform.

12. Participants have the ability to disclose their identity, or to remain anonymous in the pre-trade and post-trade state depending on the type of Platform service utilised.

13. It is expected that certain Ontario institutional investors wish to become clients of LedgerEdge in order to access the liquidity afforded by the robust network of clients on the Platform.

14. LedgerEdge proposes to offer access to its Platform to prospective Participants in Ontario (the "Ontario Participants"). In order to obtain direct access to the Platform, an Ontario Participant must agree to abide by the LedgerEdge Rulebook. The LedgerEdge Rulebook provides clear and transparent access criteria and requirements for all market participants on the Platform. LedgerEdge applies these criteria to all Participants in an impartial manner.

15. There will be no retail clients on the Platform. LedgerEdge's institutional Participants include both buy side and sell side institutions, ranging from investment firms, hedge funds, banks and high frequency trading firms.

Ontario Participants and Requested Relief

16. Ontario Participants will be comprised of institutional investors that qualify as permitted clients as defined in Section 1.1 of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations ("NI 31-103").

17. LedgerEdge intends to provide Ontario Participants with direct access to the Platform. LedgerEdge is asking for the Requested Relief in order for Ontario Participants to be able to access trading on the Platform.

18. LedgerEdge has no physical presence in Ontario and does not otherwise carry on business in Ontario except as described herein.

Location

19. LedgerEdge is based at 64 Nile Street, London, England, N1 7SR, U.K.

Size

20. The majority of LedgerEdge's institutional clients are located in Europe. However, a number will be in jurisdictions which allow the Applicant to operate under foreign exemptions such as Canada. LedgerEdge expects the great majority of activity to continue to come from European clients.

Ownership and corporate structure

21. LedgerEdge is a wholly-owned subsidiary of LedgerEdge Inc., a company incorporated under the laws of the State of Delaware, U.S. LedgerEdge Inc. owns 100% of shares of LedgerEdge.

22. LedgerEdge Inc. is controlled 76.15 percent by Co-Founder David E. Rutter, 3.85% by Flow Traders U.S. Holding LLC and 20% by LedgerEdge Holding Company LP. All entities are under common management and control.

23. LedgerEdge has no subsidiaries, but it is affiliated with LedgerEdge Securities Inc., a U.S. incorporated company formed to conduct similar activities from the U.S., which has applied for registration as a broker-dealer and ATS regulation under U.S. securities legislation.

Third Party Clearance and Settlement Entity

24. In its capacity as the Company's settlement partner, Global Prime Partners Limited ("GPP" or the "Company Settlement Partner"), is responsible for clearing and settlement (GPP clears and settles).

Trading of Debt Securities

25. LedgerEdge provides its clients with access to trade in Fixed Income Securities as facilitated by the Platform, including trades in U.S. Treasuries for hedging purposes

Tradeable Securities

26. Participants on the Platform may choose to trade any of the Fixed Income Securities listed as Eligible Instruments in the LedgerEdge Rulebook. In order to trade, a Participant must enter a security's description or ISIN, desired direction, size and price.

27. LedgerEdge's Rulebook provides Rule 24 to address trade cancellations and error trades.

SECTION 2 APPLICATION OF APPROVAL CRITERIA TO THE ATS

1.1 REGULATION OF THE ATS

Regulation of the ATS -- The ATS is regulated in an appropriate manner in another jurisdiction by a foreign regulator (the Foreign Regulator)

1.1.1 A U.K. MTF (as defined in article 2(1)(14A) of MiFIR) means a multilateral system, operated by a U.K. investment firm or market operator, which:

(a) brings together multiple third-party buying and selling interests in financial instruments (in the system and in accordance with non-discretionary rules) in a way which results in a contract; and

(b) complies, as applicable, with:

(i) paragraph 9A of the Recognition Requirements Regulations;

(ii) the EU regulations specified in Schedule 2 of MiFIR;

(iii) rules made by the competent authority (U.K. FCA) governing the operating conditions of investment firms so far as they apply to MTFs,

1.1.2 Section 6.1 of NI 21-101 requires dealer firms, as well as their professional representatives, to be registered with the OSC and also be a member of Investment Industry Regulatory Organization of Canada ("IIROC") or a similar self-regulatory organization in order to operate their business as an ATS. In the U.K., entities permitted to deal in investments as agent are authorised and regulated by the U.K. Financial Conduct Authority ("FCA"). LedgerEdge has been granted the following permissions by FCA:

• Agreeing to carry on a regulated activity pursuant to article 64 of the Financial Services and Markets Act 2000 (Regulated Activities) Order 2001 ("RAO")

• Operation of a Multilateral Trading Facility (article 25D RAO)

• Dealing in investments as agent (article 21 RAO)

1.1.3 In the U.K., responsibility for regulating the conduct of investment businesses, providing investor protection, protecting and enhancing the integrity of the U.K. financial system and promoting effective competition rests with the FCA that imposes rules of conduct on the FCA regulated companies and maintains confidence in the probity of business and financial services in the U.K.

1.1.4 The principal legal provisions for investor protection in the U.K.'s financial services sector are contained in, and derived from, the Financial Services and Markets Act 2000 and the FCA fulfils its regulatory responsibilities within the framework established by this legislation.

1.1.5 In its enforcement capacity, the FCA has the power to take disciplinary actions against regulated individuals or companies that violate the industry's rules. The Financial Ombudsman Service ("FOS") is responsible for overseeing the mediation and arbitration processes for disputes between clients and FCA regulated companies.

1.2 Authority of the Foreign Regulator -- The Foreign Regulator has the appropriate authority and procedures for oversight of the ATS. This includes regular, periodic oversight reviews of the ATS by the Foreign Regulator.

The U.K. FCA was established by the Financial Services and Markets Act 2000, and is responsible for authorising and supervising firms in financial markets, as well as having powers of enforcement.

Scope of authority

1.2.1 The FCA enforces the financial services laws of the United Kingdom and regulates the majority of the financial services industry. Its regulatory coverage includes the U.K. stock exchanges, options markets and options exchanges as well as all other electronic exchanges and other electronic securities markets.

1.2.2 One of the FCA's functions is to oversee organizations and individuals in the securities markets, including securities exchanges, brokerage firms, dealers, investment advisors, and investment funds. Through established securities rules and regulations, the FCA promotes disclosure and sharing of market-related information, fair dealing, and protection against fraud. The FCA has the authority to bring civil actions to enforce its rules and works closely with other law enforcement agencies on matters requiring criminal enforcement. The FCA has an extensive range of disciplinary, criminal and civil powers to take action against regulated and non-regulated firms and individuals, who are failing or have failed to meet the standards it requires. It will investigate and, where appropriate, discipline the regulated company, if found to have acted in breach of its rules or other regulatory requirements.

1.2.3 The FCA establishes a regulatory structure for overseeing MTFs in MAR 5 of the FCA Handbook, which implemented the provisions of MIFID into U.K. law.. This regulatory structure includes

• transparent rules and procedures for fair and orderly trading,

• objective criteria for the efficient execution of orders which are established and implemented in non-discretionary rules

• arrangements for the sound management of the technical operations of the facility, including the establishment of effective contingency arrangements to cope with the risks of systems disruption

• transparent rules regarding the criteria for determining the financial instruments that can be traded under its systems

• published, transparent and non-discriminatory rules, based on objective criteria.

1.2.4 The rules regulating the operation of MTFs include, but are not limited to:

• the resilience of the firm's trading systems;

• its capacity to deal with peak order and message volumes;

• the ability to ensure orderly trading under conditions of severe market stress;

• the effectiveness of business continuity arrangements to ensure the continuity of the MTF's services if there is any failure of its trading systems, including the testing of the MTF's systems and controls;

• the ability to reject orders that exceed predetermined volume and price thresholds or which are clearly erroneous;

• the ability to ensure that algorithmic trading systems cannot create or contribute to disorderly trading conditions on the trading venue;

• the ability to limit and enforce the minimum tick size which may be executed on the MTF

• the requirement for members and participants to carry out appropriate testing of algorithms, including providing environments

• to facilitate that testing.

1.2.5 FCA also performs periodic audits of FCA regulated companies. These audits review companies' internal procedures and applications. Companies' books and records are also verified for compliance with applicable legislation and FCA's rules.

1.2.6 Entities permitted to deal in investments as agents also have ongoing duties of financial responsibility, customer protection, and good conduct. These duties are imposed through the rules such as the following:

• Customer protection rule. Customer funds and securities must be segregated from the entity's proprietary business operations.

• Record-keeping. Basic bookkeeping requirements include records of trades, receipts, positions held in different securities, trial balances, complaints, and compliance, together with reports to be filed periodically.

• Fair dealing. Execute client orders promptly, disclose information relevant to investors, charge prices in line with market conditions, and disclose conflicts of interest.

• Suitability of clients. Only recommend investments or strategies that are suitable for the clients concerned.

• Communication. Be fair, balanced, and not misleading in communications with clients, seeking approval before communication as needed.

• Gifts and contributions. Observe rules concerning maximum value of gifts made to clients and political contributions.

• Suspicious Transactions Reports (STRs). File reports of any suspicious activities noted by the entity, including investments over predefined monetary limits.

Source of authority to supervise the foreign ATS (including rules and policy statements)

1.2.7 FCA is authorised under the Financial Services and Markets Act 2000, and supervises MTFs via MAR 5 within the FCA Handbook, which can be found here: https://www.handbook.fca.org.uk/handbook/MAR/5.pdf.

1.2.8 In general, an MTF must continue to fulfil these obligations to maintain its status as an MTF.

1.2.9 The FCA is the authority charged with ensuring that MTFs (such as LedgerEdge) continue to comply with MAR 5. The FCA has the power under the Financial Services and Markets Act to, among other things,:

(i) Withdraw a firm's authorization;

(ii) Prohibit an individual from operating in financial services;

(iii) Prevent an individual from undertaking specific regulated activities;

(iv) Suspend a firm or authorised person from undertaking specific regulated activities;

(v) Censure firms and individuals through public statements;

(vi) Issue private warnings to make a person aware that they came close to being subject to formal action.

(vii) Impose financial penalties;

(viii) Seek injunctions;

(ix) Apply to court to freeze assets;

(x) Seek restitution orders; and

(xi) Prosecute firms and individuals who undertake regulated activities without authorization.

Accordingly, LedgerEdge is subject to the oversight of the FCA. LedgerEdge enjoys a good-standing relationship with its regulator.

1.2.10 The FCA exercises its supervisory responsibility by conducting an ongoing assessment of whether LedgerEdge's rules, procedures and practices are adequate for the protection of investors and for the maintenance of an orderly market in accordance with the requirements under MAR 5 and LedgerEdge's FCA-registered Rulebook. For this purpose, the FCA requires LedgerEdge and MTFs in general to report to it any material changes in their business and operation, including, materially adverse financial information or changes to its constitution. Further, MTFs must provide access to the FCA, upon request to, any records that an MTF is required to keep pursuant to SYSC 9.1 https://www.handbook.fca.org.uk/handbook/SYSC/9/1.html

Authorization, licensure or registration of the ATS

1.2.11 LedgerEdge has a statutory obligation to ensure that its business as an MTF is conducted in an orderly manner so as to afford proper protection to investors. Failure to comply with this obligation may mean that LedgerEdge could cease to be able to operate as an MTF.

1.2.12 LedgerEdge requires each client to make representations and warranties as to the following:

(i) it is in compliance with all applicable laws in all material respects;

(ii) all information provided by it in writing to LedgerEdge (including all information contained in applications, questionnaires and information forms, and including information delivered via electronic means) is true and accurate in all material respects;

(iii) it satisfactorily meets the Applicant's internal client on-boarding requirements, including any eligibility criteria or other requirements contained in the LedgerEdge Rules and is able to effect settlement of "Transactions" (as defined in the LedgerEdge Rulebook) in accordance with the LedgerEdge's Rules as set out in the LedgerEdge Rulebook and the Participation Agreement;

(iv) it is authorized to enter into the Transactions entered into by it through the Platform and each of such Transactions, as confirmed by the Platform, is the legal, valid and binding obligation of Participant, enforceable against the Participant in accordance with its terms and the terms thereof;

(v) it possesses the sophistication, experience, knowledge and expertise in financial and business matters to make its own investment decisions and to properly assess the merits, risks and suitability of investing in, and entering into Transactions in respect of, the Products;

(vi) the "Authorized User"(as defined in the LedgerEdge Rulebook) is (x) capable of evaluating investment risks independently, both in general and with regard to particular Transactions and investment strategies involving a security or securities and (y) will exercise independent judgment in evaluating the merits of all potential Transactions;

(vii) it acknowledges, agrees and understands that (w) all Transactions are unsolicited transactions, (x) no Transaction will be solicited or recommended by LedgerEdge or any of its representatives; (y) its decision to enter into any Transaction will be based on its own research and information, or on research and information obtained from a source other than LedgerEdge and its representatives, and neither LedgerEdge nor any of its representatives will have any input into its decision to enter into such Transaction; and (z) LedgerEdge does not provide a guarantee of a two-sided market for a security or derivative on a continuous or reasonably continuous basis;

(viii) it is and will continue to be either (x) an Eligible Counterparty or (y) a Professional Counterparty, as defined by the FCA;

(ix) it has implemented policies and procedures to ensure its compliance with all applicable laws related to anti-money laundering and sanctions and shall ensure that it follows such policies and procedures with respect to its use of and access to the Platform (and ensure that its Authorized Users follow such policies and procedures in accessing and using the Platform).

(x) it has adequate arrangements in place for entering into trades, order management, clearing (if relevant) and settlement of all orders submitted;

(xi) it will be able to provide (if requested) such information that the Applicant may require in relation to the validity of any order or trade;

(xii) it has adequate organizational procedures and controls to limit the submission of erroneous orders on the Platform; and

(xiii) it is able to satisfy the technical specifications and standards required by the Applicant for participation on the Platform.

The Applicant applies the above listed criteria during the onboarding process to any prospective Participant that submits an application to participate in the Platform. The Applicant also performs anti-money laundering and know-your-client checks and ensures that the Participant is based in a jurisdiction where the Applicant is permitted to carry on the Platform business or where it does not need to be further authorized to provide the Platform services. Furthermore, Participants covenant to notify the Applicant promptly in the event any of the foregoing representations and warranties become untrue at any time during the term of the Participation Agreement.

1.3 The foreign regulator's approach to the detection and deterrence of abusive trading practices, market manipulation, and other unfair trading practices or disruptions of the market

1.3.1 Pursuant to MAR 5.6 MTFs are required to comply with antifraud, antimanipulation and other applicable provisions of the U.K. version of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation).This entails the following:

(i) LedgerEdge's tech-operations team monitors system performance and usage in real-time;

(ii) All orders and trades on the LedgerEdge platform are sent in real-time to the Eventus Systems Inc Validus system, and reviewed by LedgerEdge's Market Surveillance team in real-time;

(iii) LedgerEdge's Compliance Officer reviews and signs off on trades and any surveillance alerts daily; and

(iv) LedgerEdge employs a third-party compliance consultant to review LedgerEdge's review (conducted weekly).

(v) orders and trades on LedgerEdge are subject to pre and post trade transparency reporting to the FCA. In addition, certain transactions are reportable to FCA dependant on the counterparties involved on each trade.

Chapter 5 of LedgerEdge's Rulebook further addresses the duties and responsibilities of Participants, to ensure compliance with all material laws. Lastly, LedgerEdge's internal policies address and prohibit employee trading on material non-public information.

Laws, rules, regulations and policies that govern the authorization and ongoing supervision and oversight of market intermediaries in the U.K.

Procedures for dealing with the failure of a market intermediary in order to minimize damage and loss to investors and to contain systemic risk for market intermediaries who may deal with members and other participants located in Canada

1.3.2 See section 1.2 above and the information set out under paragraphs 1.2.9 and 1.2.10, and part 5, sections 5.1 and 5.2 and section 7.2 below for further information in this regard.

2. GOVERNANCE

2.1 Governance -- The governance structure and governance arrangements of the ATS ensure:

(a) Effective oversight of the ATS operations,

2.1.1 LedgerEdge has independent departments handling product development, testing, change management (code deployment), infrastructure and system operation. Further, LedgerEdge employs real-time monitoring of the Platform with end of day checks by management. Trades, and trading in employee personal accounts, are also regularly reviewed by a third-party, compliance consulting firm.

2.1.2 LedgerEdge provides the trading environment for the trading of Fixed Income Securities. As an MTF conforming with U.K. regulatory requirements, LedgerEdge offers a legally safe forum for Fixed Income Securities trading. As an MTF, LedgerEdge comes under the direct jurisdiction of the FCA as discussed above.

2.1.3 LedgerEdge has a statutory requirement to ensure that business on its markets is conducted in an orderly manner, providing proper protection to investors. The LedgerEdge Rules have been designed to ensure compliance with all applicable legislation and to ensure a fair and orderly market. LedgerEdge has an internal compliance department and contracts with a third-party compliance consultant which, among other things, monitors LedgerEdge's compliance with all applicable legislation. LedgerEdge's Chief Compliance Officer is responsible for updating policies and procedures to comply with changes in regulation.

2.1.4 The Applicant's governance arrangements have been documented to ensure that all individuals are aware of and understand their obligations. LedgerEdge will assign responsibilities among senior management to ensure that everyone in the organization is clear on their responsibilities and importance of their respective roles in maintaining an effective systems and controls environment. This will assist in monitoring and maintaining control of operating and financial activities. LedgerEdge is organized into a Board of Directors, Management Committee, and Risk Committee. Day to day management of LedgerEdge is delegated by the Board to the Management Committee. A Risk Committee will be appointed and will be responsible for the Applicant's risk framework, risk appetite, risk strategy, controls, systems and policies.

(b) fair, meaningful and diverse representation on the board of directors and any committees of the board of directors, including:

(i) appropriate representation of independent directors, and

(ii) a proper balance among the interests of the different persons or companies using services and facilities of the ATS,

2.1.5 LedgerEdge's directors are appointed having regard to the need to have representation of a diverse range of skills and experience related to securities markets and debt trading. The Board of Directors comprises of David Rutter as chairman and executive officers of LedgerEdge. The Board of Directors will:

• Set LedgerEdge's strategy;

• Assume full responsibility for the oversight of LedgerEdge's operations, including the implementation and oversight of regulatory programs;

• Ensure the human and financial resources are available to meet strategic objectives;

• Review LedgerEdge's management performance;

• Monitor and maintain compliance with regulatory obligations, applicable rules and guidance;

• Establish, maintain and enforce written procedures to identify and mitigate conflicts of interest; and

• Ensure that LedgerEdge does not prioritize commercial interests over regulatory responsibilities.

(c) The ATS has policies and procedures to appropriately identify and manage conflicts of interest, and

2.1.6 LedgerEdge takes potential conflicts of interest and the associated consequences seriously and has implemented appropriate policies and procedures to mitigate the risk of such occurrences. LedgerEdge does not trade for its own account so it has no interests to be conflicted. Further, neither GPP, nor any GPP affiliate, conducts proprietary trading on LedgerEdge. These procedures supplement the legal duties on directors to avoid any situation in which he or she has, or could have, a direct or indirect interest that conflicts, or could conflict, with the interests of the Applicant.

2.1.7 In addition, LedgerEdge has taken into account conflicts of interest that could arise in its role as operator and a participant of the venue in connection with its broker activities. These conflicts of interests are not as heightened as in a model whereby the broker (when acting as agent) has discretion over which MTFs to use. LedgerEdge as a broker is being used to facilitate access to the Platform for clients who would otherwise not be able to do so easily, and is following such clients' specific instructions. It is not anticipated that this order flow will be a substantial or significant part of the Platform's volume. Notwithstanding this, a full conflict of interest analysis has been carried out focusing in particular on the following areas and action points:

• All orders will be treated the same whether entered directly by a participant or via direct electronic access ("DEA") coming in through LedgerEdge dealing as broker agent;

• LedgerEdge Broker will not be working its own orders or working the orders of clients, but following instructions;

• LedgerEdge will carefully monitor order flows on an ongoing basis to ensure that there is no difference between the treatment of order flow from a direct participant versus order flow via LedgerEdge as a broker;

• LedgerEdge as a broker will always act as pure agent for the client and in a passive capacity.

2.1.8 LedgerEdge is required to comply with article 2(3) of ITS 19 (EU Commission Implementing Regulation (EU) 2016/824) regarding any potential conflicts between the interest of the MTF, its operator or its owners and the sound functioning of the MTF.

2.1.9 LedgerEdge has identified a conflict of interest between David Rutter as chairman of LedgerEdge and the fact that he is also CEO of R3 LLC, whom LedgerEdge have engaged as provider of the Corda Enterprise platform used for the LedgerEdge digital ledger. All dealings with R3 LLC will be on an arms-length basis, and all contracts between LedgerEdge and R3 LLC must be approved by the boards of LedgerEdge and R3 LLC before they are put in place. LedgerEdge receives the same pricing and the same terms and conditions as any other firm contracting with R3 LLC at arm's length.

2.1.10 In addition, all LedgerEdge employees are subject to contractual restrictions that are designed to mitigate, manage and limit conflicts of interest. LedgerEdge also runs background checks on all of its employees.

2.1.11 LedgerEdge has also implemented a Conflicts of Interest, Independence and Impartiality Policy, as part of its Compliance Manual, which provides employees with an overview of LedgerEdge's key obligations and the controls implemented in order to identify, disclose and manage actual conflicts of interest.

2.1.12 Conflicts are also not expected to arise between one client of the Firm and another. LedgerEdge's compliance department will continuously monitor conflicts within the business and these will be identified and addressed in line with the Conflicts of Interest, Independence and Impartiality Policy. Any breaches of the policy will be logged in LedgerEdge's risk breach log.

(d) There are appropriate qualifications, remuneration, limitation of liability and indemnity provisions for directors, officers and employees of the ATS.

2.1.13 The LedgerEdge articles of association is LedgerEdge's principal governing document. LedgerEdge has adopted the Model articles for private companies limited by shares: https://www.gov.uk/government/publications/model-articles-for-private-companies-limited-by-shares, which include standard directors' appointment, qualification, remuneration, indemnity and insurance provisions.

2.2 Fitness -- The ATS has policies and procedures under which it will take reasonable steps, and has taken such reasonable steps, to ensure that each director and officer is a fit and proper person.

2.2.1 Each director is appointed on merit based on skills, qualifications and experience and is subject to detailed disclosure requirements under Companies Act 2006, which includes information as to criminal or civil sanctions and regulatory actions, and such disclosures are publicly accessible on the FCA's public register.

3. REGULATION OF PRODUCTS

3.1 Review and Approval of Products -- The products traded on the ATS and any changes thereto are reviewed by the Foreign Regulator, and are either approved by the Foreign Regulator or are subject to requirements established by the Foreign Regulator that must be met before implementation of a product or changes to a product

3.1.1 FCA is responsible for regulating securities, including Fixed Income Securities and as such all products traded on LedgerEdge fall under the jurisdiction of FCA. LedgerEdge is required to have any products they wish to trade included within their FCA authorisation, and can only add new products following a variation of permission from FCA.

3.2 Product Specifications -- The terms and conditions of trading the products are in conformity with the usual commercial customs and practices for the trading of such products.

3.2.1 The FCA establishes a range of requirements that must be met before any new product is admitted for trading on the Platform. New products must be capable of being traded in a fair, orderly and efficient manner and the Platform must be designed so as to allow for its orderly pricing.

3.2.2 Initially, the Applicant will populate the data system of the Platform with the information on the specific Fixed Income Securities to be admitted to trading on the Platform (provided they have passed the scrutiny of the LedgerEdge Risk Committee). Where a specific Fixed Income Security is not admitted to trading on the Platform, a Participant may request that the Applicant add that instrument. The requested Fixed Income Security will be added to the Platform if it passes an internal review process comprising of the Applicant's Management Committee and Risk Committee review to establish whether the proposed new instrument is appropriate and can be safely traded on the Platform.

3.3 Risks Associated with Trading Products -- The ATS maintains adequate provisions to measure, manage and mitigate the risks associated with trading products on the ATS.

3.3.1 LedgerEdge maintains adequate provisions to measure, manage and mitigate the risks associated with trading products on the Platform as required by the legislation or as instituted by the Company Settlement Partner. These include, but are not limited to, conformance to daily trading limits, 'market access' controls and internal controls. Appendix B to this Application sets out a description of all such controls.

4. ACCESS

4.1 Fair Access

(a) The ATS has established appropriate written standards for access to its services including requirements to ensure:

(i) Participants are appropriately registered as applicable under the Legislation, or exempted from or not subject to these requirements,

(ii) The competence, integrity and authority of systems users, and

(iii) Systems users are adequately supervised.

(b) The access standards and the process for obtaining, limiting and denying access are fair, transparent and applied reasonably.

(c) The ATS shall not unreasonably prohibit, condition or limit access by a person or company to services offered by it.

(d) The ATS does not

(i) permit unreasonable discrimination among participants, or

(ii) impose any burden on competition that is not reasonably necessary and appropriate.

4.1.1 An MTF is required to have published, transparent and non-discriminatory rules, based on objective criteria, governing access to its facility and which must provide that its members or participants are investment firms, CRD credit institutions or other persons who:

(a) are of sufficient good repute;

(b) have a sufficient level of trading ability, competence and experience;

(c) where applicable, have adequate organisational arrangements; and

(d) have sufficient resources for the role they are to perform, taking into account the different financial arrangements that the firm operating the MTF may have established in order to guarantee the adequate settlement of transactions.

These rules are governed by MAR 5.3 and implement MIFID articles 18(3), 19(2), and 53(3).

Access requirements

4.1.2 As a regulated MTF, LedgerEdge is subject to U.K. marketplace regulatory requirements that are closely aligned with EU MIFID requirements outlined above. LedgerEdge is obligated under the MAR 5.3 https://www.handbook.fca.org.uk/handbook/MAR/5/3.html to ensure that access to its facilities is fair and non-discriminatory.

4.1.3 LedgerEdge's access to the Platform criteria are outlined in the LedgerEdge Rulebook and Operational Specifications and applied equally to all Participants. Chapters 3 to 6 of the LedgerEdge Rulebook set out the requirements for access to and use of the Platform, as well as requirements relating to provision of information. Access requirements for prospective Participants on the Platform are set out in Chapter 3 and 4 of the LedgerEdge Rulebook. Chapter 4 specifies the requirements that are applicable to each Participant, including, for instance, the prospective Participant's regulatory status and the obligations of Participants to promptly provide information reasonably requested by LedgerEdge. Chapter 20 sets out the ability of LedgerEdge to investigate and suspend or terminate a Participant's access to the Platform for suspected breaches of the Rules.

4.1.4 When a potential participant applies for access to the Platform, the participant must confirm its regulatory status, and this is confirmed as part of LedgerEdge's Know-Your-Client (KYC) and anti-money laundering (AML) on-boarding process. A similar process is proposed to be implemented for Ontario Participants.

4.1.5 The LedgerEdge Rulebook does not allow a person to enter into a trade on the Platform unless that person can validly enter into trades in accordance with the law or regulation applicable to that person.

4.1.6 LedgerEdge is regulated in the U.K. by the FCA. It is therefore familiar with regulators imposing particular requirements as a result of local law and regulation. LedgerEdge's rules are designed to ensure that its Participants comply with these requirements through section 5.7 of the LedgerEdge Rulebook.

Due diligence and on-going supervision

4.1.7 LedgerEdge conducts a robust due diligence procedure to ensure that LedgerEdge's Participants are fit and proper, in order to protect the integrity of the Platform and the orderliness of its business. Once a Participant has been admitted, controls are also applied to any additional system users. System users are also subject to supervision on an on-going basis.

4.1.8 LedgerEdge performs regular due diligence on LedgerEdge's client list to ensure none appear on applicable restricted lists.

5. REGULATION OF PARTICIPANTS ON THE ATS

Regulation -- LedgerEdge has the authority, resources, capabilities, systems and processes to set requirements governing only the conduct in respect of the trading by the participants on the Platform.

5.1 Participants are required to demonstrate their compliance with these requirements

5.1.1 Participants attest to their compliance with the Applicant's requirements via execution of their onboarding and related documentation. The onboarding documentation required by LedgerEdge includes collection of a Participation Agreement and completion of an on-boarding/Wolfsberg questionnaire (see https://www.wolfsberg-principles.com/wolfsbergcb). Additional information is collected and verified through KYC process.

5.1.2 The financial resource requirements, standards, guides or thresholds required of Participants are set out in Chapter 4 of the LedgerEdge Rulebook (the "Eligibility Criteria"). Participants attest to these criteria in their signed documentation and financial information is collected and verified through the KYC process.

5.1.3 All Participants are required by LedgerEdge to satisfy the Eligibility Criteria on an ongoing basis. The Participants are required to notify LedgerEdge of anything that LedgerEdge might reasonably expect to be disclosed. This would include all legal, financial and regulatory matters that are material to their standing as Participants. Participants must also provide the information necessary to confirm their continued compliance with the eligibility criteria set out in the LedgerEdge Rulebook.

5.1.4 In addition, the LedgerEdge Rules have provisions regarding the conduct of Participants. These include provisions relating to "conduct rules" (in Chapter 6 of the LedgerEdge Rulebook), which are designed to prevent fraudulent and manipulative acts and practices. Generally, the provisions of Chapter 6 (Conduct Rules) and Chapter 20 (Suspension or Termination of Participation) are designed to set out how trading on the Platform should take place in a fair and orderly manner and have been designed to ensure just and equitable principles of trade and to foster co-operation and co-ordination with persons or companies engaged in regulating, clearing, settling, processing information with respect to, and facilitating transactions in products traded on the Platform.

5.2 Client Advisory and Member Services

5.2.1 LedgerEdge employs a team of client-facing employees to ensure all Participants and their Authorized Users are familiar with the Platform protocols, new releases or enhancements, and/or for any market-related matter where assistance may be needed in real-time.

5.3 Regulation and Enforcement of LedgerEdge Rules on Participants

5.3.1 LedgerEdge is not recognized as a national security exchange in the U.K. and, therefore, does not have any regulatory or enforcement powers over its Participants and does not discipline the Participants, other than by exclusion from participation in the trading system. It does, however, have the authority to terminate, suspend or limit the Participants' access to the Platform in case of misconduct, as provided in Chapter 20 of the LedgerEdge Rulebook.

5.3.2 LedgerEdge also has certain summary powers that are set out in Section 10.15 of the LedgerEdge Rulebook (including an absolute discretion to prohibit, remove, suspend, terminate or cancel orders or instruments on the Platform), to deal with any occurrence or circumstance which threatens or may threaten such matters as the fair and orderly trading on the Platform.

5.4 LedgerEdge's capacity to detect, investigate, and sanction persons who violate LedgerEdge Rules

5.4.1 Chapter 20 of the LedgerEdge Rulebook sets out LedgerEdge's capacity to investigate and sanction persons who violate LedgerEdge Rules. Chapter 6 of the LedgerEdge Rulebook prohibits fraud and abuse as well as other trading practices and market abuses.

5.4.2 LedgerEdge has sufficient personnel, and sufficient software tools, to monitor the Platform. The trading operations and technology operations teams monitor the real time market for orderly trading on the Platform. Part of this monitoring includes enforcement of LedgerEdge's policies in respect of error trades and erroneous submissions. As a result of daily monitoring of the real-time market, trading operations may identify activity or behaviour which warrants further investigation or analysis (examples include but are not limited to: unusual price movements in the real-time market, or order behaviour which may be detrimental to the integrity of the market).

6. CLEARING AND SETTLEMENT

6.1 Clearing Arrangements -- The ATS has appropriate arrangements for the clearing and settlement of transactions through a clearing house.

6.2 Regulation of the Clearing House -- The clearing house is subject to acceptable regulation.

6.2.1 LedgerEdge's responsibility is to ensure the efficient settlement of transactions. The rules governing the settlement of transactions executed on the Platform are set out at Rule 13 of the LedgerEdge Rulebook. All transactions shall be settled promptly and efficiently between the parties in the relevant settlement system associated with the relevant bond market in compliance with the rules and regulations promulgated by such service in respect of the clearance and settlement of transactions. Participants on the Platform are made aware of their responsibilities in relation to settlement by Rule 13 of the LedgerEdge Rulebook. The most current, up to date version of the Rulebook is published and freely available to the general public on LedgerEdge's website.

6.2.2 LedgerEdge has contracted with GPP to serve as the Company Settlement Partner for the Platform. GPP has appropriate arrangements for the clearing and settlement of Transactions through a clearing and settlement agent. LedgerEdge creates and sends transaction details to GPP and each counterparty to the transaction.

6.2.3 Broadly there are two primary ways of carrying out settlement on the Platform. Firstly, Participants may trade bilaterally between themselves when a trade is executed on the Platform. In such trades, the two parties will settle the trade directly with each other. Secondly, LedgerEdge appointed the Company Settlement Partner (GPP), to facilitate settlement between the Participants where they do not wish to be disclosed as trading parties to one another.

6.2.4 GPP is regulated by the FCA as an investment firm, with FCA firm reference number 533039. It provides clearing services into various central securities depositories including Depository Trust & Clearing Corporation ("DTCC") and Euroclear.

6.3 Access to the Clearing House

(a) The clearing house has established appropriate written standards for access to its services.

(b) The access standards for clearing members and the process for obtaining, limiting and denying access are fair, transparent and applied reasonably.

6.3.1 As noted above, clearing is undertaken through an independent third party, GPP.

6.4 Sophistication of Technology of Clearing House -- The ATS has assured itself that the information technology used by the clearing house has been adequately reviewed and tested and provides at least the same level of safeguards as required of the ATS.

6.4.1 LedgerEdge has direct integration with GPP for the passing of settlement instructions, and GPP in turn has direct access to the relevant securities depository.

6.5 Testing

6.5.1 All releases (both major and minor/patches) undergo similar testing regimens:

6.5.2 Testing of a release includes: developer testing of each feature on a local build, peer review and automated testing of new code, code merging into test environments, automated regression testing, quality assurance and manual regression testing, quality assurance signoff, product development signoff, and production release, as set out below:

(a) Developer testing: Each developer tests his/her own code to ensure proper functionality on a local machine (sandboxed environment).

(b) Peer review: Other developers review the writer's code to ensure optimization and proper function.

(c) Automated testing of new code to ensure proper functionality

(d) Merging of new code into a test environment

(e) Automated testing of merged code to ensure proper functionality of new code and proper functionality of previously existing code.

(f) Quality assurance and manual regression testing to ensure proper functionality of new code and proper functionality of previously existing code.

(g) Quality assurance signoff

(h) Product development signoff

(i) Production release.

6.6 Risk Management of Clearing House -- The ATS has assured itself that the clearing house has established appropriate risk management policies and procedures, contingency plans, default procedures and internal controls

6.6.1 As noted above, LedgerEdge has contracted with GPP to serve as Company Settlement Partner for the Platform. GPP, as an FCA regulated entity, has appropriate arrangements for the clearing and settlement of transactions through a clearing house.

6.7 Custody Functions -- Whether the ATS performs custody functions and if so, how

6.7.1 LedgerEdge does not perform custody functions.

7. SYSTEMS AND TECHNOLOGY

7.1 Systems and Technology -- Each of the ATS's critical systems has appropriate internal controls to ensure completeness, accuracy, integrity and security of information, and, in addition, has sufficient capacity and business continuity plans to enable the ATS to properly carry on its business. Critical systems are those that support the following functions:

(a) order entry,

(b) order routing,

(c) execution,

(d) trade reporting,

(e) trade comparison,

(f) data feeds,

(g) market surveillance,

(h) trade clearing, and

(i) financial reporting.

7.1.1 LedgerEdge's critical systems that have appropriate internal controls as applicable to its trading functionality include:

(a) security selection and reference data,

(b) order entry,

(c) fat finger controls,

(d) order matching,

(e) trade reporting,

(f) trade routing,

(g) data feeds, and

(h) market surveillance.

Please see Appendix B for detailed description of the Platform's system controls.

Regulatory Requirements

Description of the matching system -- Manner of Operation of the LedgerEdge ATS

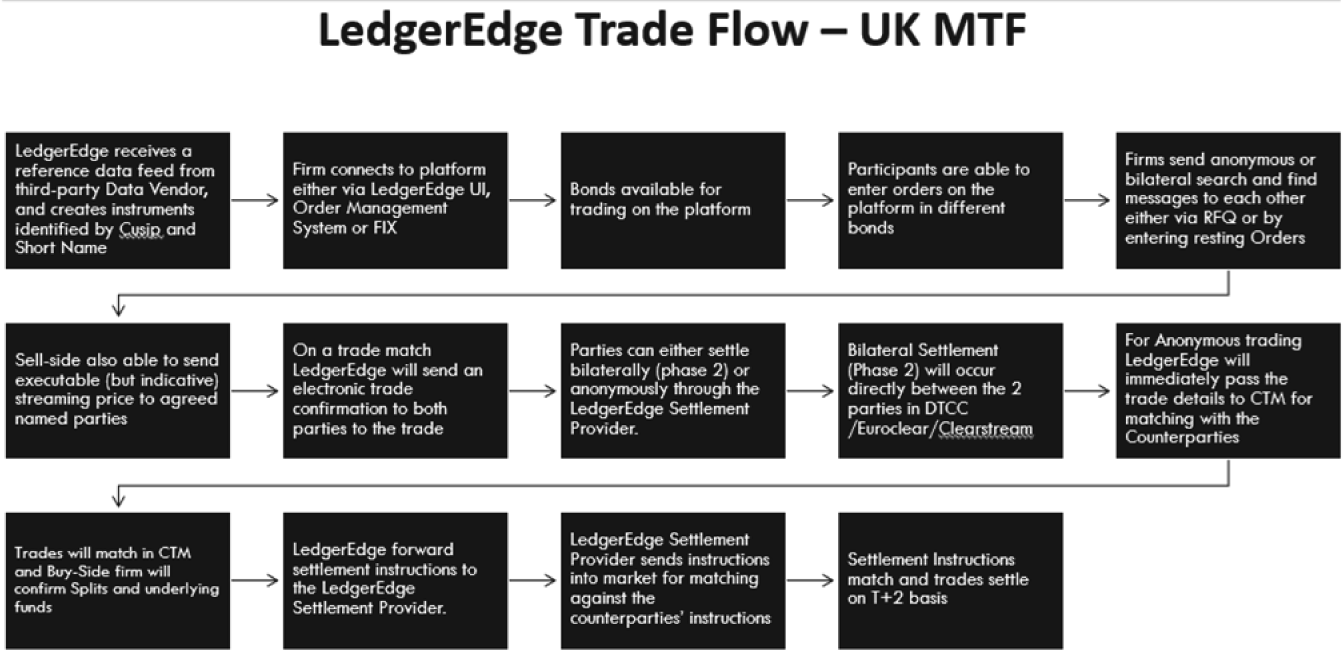

7.1.2 The Platform will facilitate trades between large, sophisticated professional and eligible counterparties in a range of debt instruments including bonds issued by governments, government agencies, supra-nationals and corporates. In each case, pre-trade anonymity (of both identity and price/volume) is considered vital by clients. The presence or absence of such anonymity directly influences Participants' willingness to put up prices (and sizes) and, as a consequence, their contribution to market liquidity. This is particularly the case where they wish to deal in larger than normal sizes (in liquid bonds) or any size at all (in less liquid or illiquid bonds). A summary of the trade flow on the Platform is displayed in the diagram below.

*CTM is DTCC's Central Trade Matching system, which is used extensively in the fixed income and equities markets for trade matching and provision of split allocations.

7.1.3 The Platform will operate different trading protocols:

(a) the "RFQ Protocol", a request-for-quote trading system;

(b) the "ESP Protocol", a quote-driven trading system;

(c) the "Resting Protocol", a continuous auction order book trading system; and

(d) the "Volume Matching".

Trading Operation

RFQ (Request for Quote) Protocol

7.1.4 The RFQ will be sent to participants who have indications that they are holding the same bonds (i.e. are matched). A conditional quote will be provided, which will be firmed up by a negotiation between the two parties upon pricing and volume been agreed. Once agreed the order will be executed if neither party rejects the match for a defined short period. The platform also permits resting orders (with conditional or unconditional visibility) and a price streaming flow for liquidity providers. The quotes will be made pre-trade transparent if a pre-trade transparency waiver is not relied upon.

ESP (Executable Streaming Price) Protocol

Participants have the opportunity to offer streaming price/quotes. These Participants who opt to provide streaming price/quotes will act as forms of liquidity provider to other Participants. Receiving Participants can accept such streamed prices, and the trade will then be executed following confirmation by both parties. The streaming prices would be made pre-trade transparent where not reliant upon a pre-trade transparency waiver. The ESP Protocol therefore has the characteristics of the quote driven trading system set out in Annex 1 of Commission Delegated Regulation (EU) 2017/583 ("RTS 2") https://ec.europa.eu/finance/securities/docs/isd/mifid/rts/160714-rts-2-annex_en.pdf with the caveat that the streaming prices can be indicative as well as firm.

Resting Protocol

7.1.5 Participants have the ability to enter firm orders by submitting bids and offers. This resting protocol functions as a continuous limit order book where quotes are submitted and matched on the basis of time priority. The system would make the orders submitted into the resting protocol pre-trade transparent were it not for a pre-trade transparency waiver. As the Resting Protocol is a continuous system which matches orders, it has the characteristics of the continuous auction order book trading system set out in Annex 1 of MIFID RTS 2.

Volume Matching

7.1.6 Participants may also participate in volume matching sessions. Prior to such session commencing, LedgerEdge will set the volume matching price in respect of a particular bond on screen, based either on (i) the most recent trade on the Platform or (ii) in the absence of a recent trade, pricing information regarding that instrument drawn from the Platform or market. Participants can submit orders at the volume matching price, specifying the volume that they wish to trade. An engine will match pairs of orders. The length of the volume matching session is set by LedgerEdge (and may vary in length, at the sole decision-making authority of LedgerEdge as the operator of the Platform). Volume matching therefore has the characteristics of the periodic auction trading system set out in Annex 1 of MIFID RTS 2.

7.1.7 The rules in relation to the functioning of the Platform trading system in relation to each of the above are set out at Rule 10 of the LedgerEdge Rulebook.

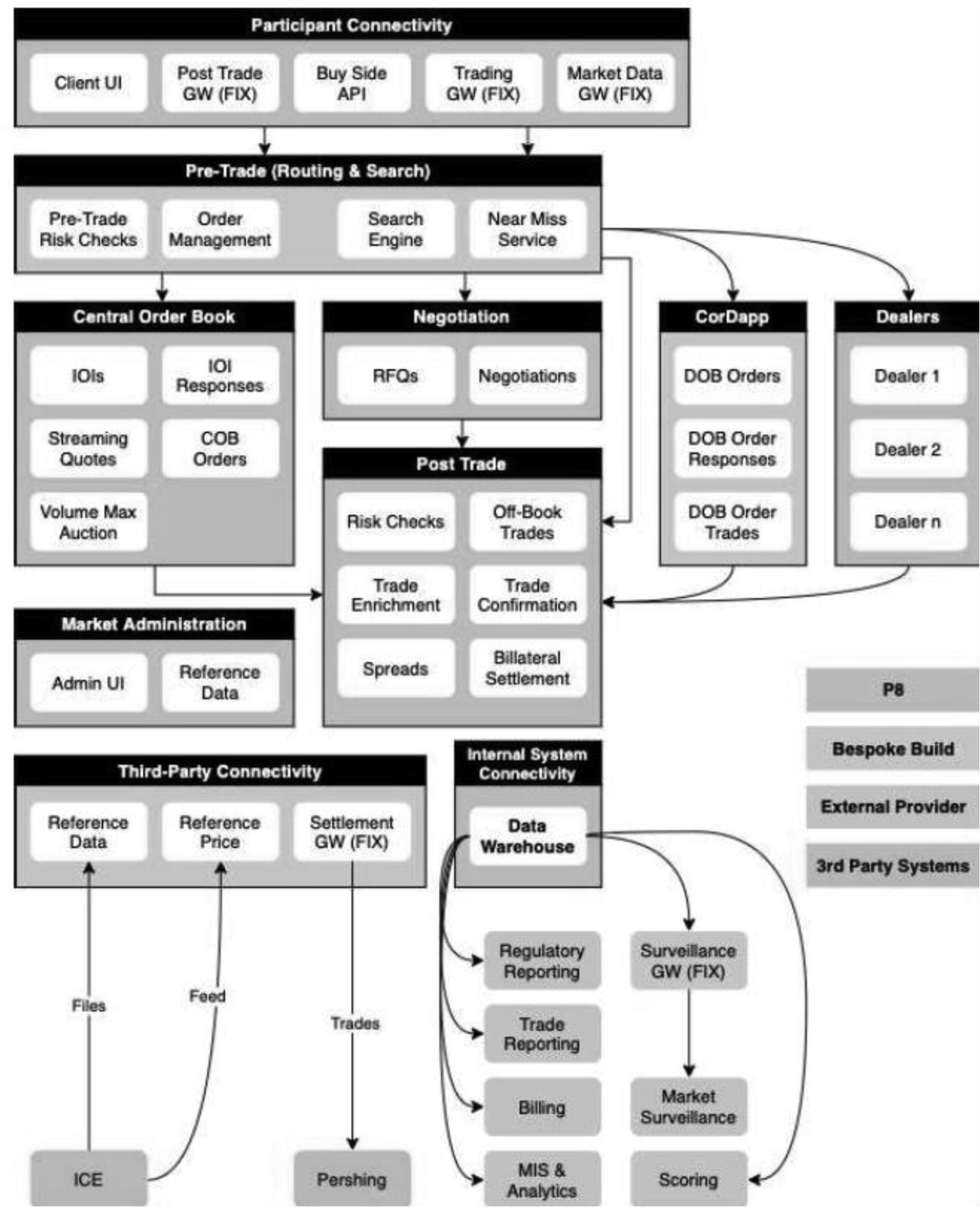

Description of the architecture of the systems, including hardware and distribution network, as well as any pre-- and post-trade risk-management controls

7.1.8 LedgerEdge ensures that the risk management controls are in place. The pre and post-trade risk management controls include:

(a) Fat finger checks ensuring bids and offers are within a reasonable tolerance away from prior execution prices, ensuring maximum order sizes are hard coded to prevent outsized orders, administrative portals to provide client administrators with direct access for trader limits.

(b) Trade cancellation: LedgerEdge has the capability and is permitted, per the LedgerEdge Rulebook, to cancel any trade that it determines detrimental to market integrity.

(c) Participant-level permissions: Trading credentials are provided only after documentation is completed and risk limits are assigned.

(d) Volume and price limiting functionality: Automated limit controls enforce risk limits imposed on clients by the client's administrators.

The following diagram represents the high level architecture of the platform:

Market continuity provision

7.1.9 LedgerEdge's systems must be compliant with the EU Recovery and Resolution Directive and ensure staff are aware of the business continuity arrangements, which must be adequately documented. The Applicant has detailed business continuity and disaster recovery plans and procedures for the Platform's operations.

7.1.10 The Platform systems run in two availability zones within a single geography (Ireland) within Amazon Web Services (AWS). These are designated as Primary Site & Backup Site.

The processes within the Platform systems are broken down into two categories; ones that would immediately impact the safe trading process if they went down -- these processes are deemed to be critical. The other category of process are those that have no immediate impact on the system or clients -- these are deemed as non-critical.

Critical Processes:

• Have a standby process within the primary site

• The backup process is automatically invoked if the primary process fails

• Technical Operations will be notified

• The primary process failure will be investigated, and appropriate action will be taken

• The primary process will be restarted when it is safe to do so

Non-Critical Processes:

• There is a single instance of the process in each site

• The state of the backup process is maintained

• If the process on the primary site fails, the partner process in the backup site will be invoked

• The primary process failure will be investigated, and appropriate action will be taken

• The primary process will be restarted when it is safe to do so

7.2 Information Technology Risk Management Procedures -- The ATS has appropriate risk management procedures in place including those that handle trading errors, trading halts and circuit breakers.{2}

7.2.1 LedgerEdge takes steps to ensure that a fair and orderly market is maintained with regard to the submission of orders, and to protect both the Platform and Participants' own systems and infrastructure from inappropriate activity. LedgerEdge performs ongoing monitoring of the Platform, including, without limitation, performance and capacity, orders sent by Participants on an individual and aggregated basis, message flow, and the concentration flow of orders, to detect potential threats to the orderly functioning of the market.

7.2.2 In addition to measures listed in Appendix B, LedgerEdge has arrangements to prevent disorderly trading and breaches of capacity limits, including those set out in section 7.1.9.

7.2.3 In terms of LedgerEdge's approach to foster system resiliency, integrity, reliability and cybersecurity, LedgerEdge follows best practices for cybersecurity and utilizes LedgerEdge-implemented firewalls to ensure the integrity of LedgerEdge's infrastructure. LedgerEdge regularly conducts penetration tests and vulnerability scans to ensure those best practices are reviewed and validated by third party experts. Further, LedgerEdge's disaster recovery facility has real-time data replication, along with hourly off-site data backups. Finally, LedgerEdge conducts a regular fail over test to the disaster recovery location each quarter.

Trade Halts

7.2.4 Rule 10.15 of the LedgerEdge Rulebook states that LedgerEdge may, in its reasonable judgment and without liability to any Participant, Authorized User or other party, suspend or cancel an order, a security, a market or the platform.

Error Trades

7.2.5 Rule 24.1 of the LedgerEdge Rulebook states that LedgerEdge may cancel any trade or order that it determines would be detrimental to market integrity. All determinations of LedgerEdge to cancel a trade, or to decline to cancel a trade, shall be final, and LedgerEdge shall not have any liability for losses arising out of determinations made by LedgerEdge pursuant to this Rule.

Upon a determination by LedgerEdge that a trade shall be cancelled, that decision will be implemented. The cancelled trade shall be reflected as cancelled in LedgerEdge's official records and, if applicable, shall be reported by LedgerEdge to the applicable counterparties and the Company Settlement Partner.

8. OUTSOURCING

8.1 Outsourcing -- Where the ATS has outsourced any of its key services or systems to a service provider, it has appropriate and formal arrangements and processes in place that permit it to meet its obligations, and that are in accordance with industry best practices.

8.1.1 LedgerEdge has implemented a specific outsourcing policy, that sets out the organisational measures taken by LedgerEdge to identify risks in relation to outsourced activities, and in relation to appropriate monitoring of outsourced activities. LedgerEdge considers any arrangements of any form between itself and a service provider by which that service provider performs a process, service or activity which LedgerEdge would otherwise undertake itself. Outsourced contracts are subject to review.

8.1.2 LedgerEdge has identified the following outsourcings:

• a critical outsourcing agreement with Yaala Labs (Private) Ltd for the provision of technological support, that will be closely monitored to ensure compliance and tested from a disaster recovery point of view to ensure continuous operations;

• a critical outsourcing agreement with MilleniumIT ESP (Private) Ltd for the day-to-day managed services and provision of a Security Operations Centre for the platform;

• an agreement in place with R3 for use of the Corda DLT platform (LedgerEdge's Chief Technology Officer will be responsible for managing the relationship with R3 and Yaala Labs, and will ensure that all change management, testing and release procedures are fully followed);

• an outsourcing agreement in place with the London Stock Exchange for transaction reporting, with Tradeweb for transparency reporting, and reporting of reference data); and

• an outsourcing agreement in place with Eventus Systems Inc for the provision of the Validus market abuse surveillance platform.

8.1.3 LedgerEdge's Directors will be responsible for oversight of the outsourced services. Potential risks in relation to outsourcing providers include technical failures, inadequate resources, failure of the provider and inadequate financial resources. These will be mitigated by LedgerEdge through:

• an annual review by the LedgerEdge Management Committee of the Service Level Agreement(s) in place against actual services being received;

• the identification of suitable alternative provider(s) for technology and other support services in the event an outsourcing provider should no longer be able to fulfil the terms of a Service Level Agreement; and

• the allocation of capital (fixed overhead requirement) for operational risk.

8.1.4 In accordance with paragraph 5.1 of LedgerEdge's Risk Management Policy, monthly review of outsourced providers with relation to specified key performance indicators will be undertaken, and reports made to the LedgerEdge Risk Committee.

9. TRANSPARENCY AND REPORTING

9.1 Transparency -- The ATS has adequate arrangements to record and publish accurate and timely trade and order information. This information is provided to all participants on an equitable basis.

9.1.1 Section 8.2 of NI 21-101 imposes certain pre-trade and post-trade information transparency requirements on ATSs displaying orders of Fixed Income Securities. Section 10.1 requires disclosure by a marketplace (including an exchange and an ATS) on its website of certain information reasonably necessary to enable a person or company to understand the marketplace's operations or services it provides, including information related to the system's protocols and Rulebook. Further, revisions to OSC Staff Notice 21-703 align the transparency requirements for ATSs with those imposed on exchanges in the areas where the two marketplaces compete.

Pre-Trade Transparency

9.1.2 LedgerEdge is required under Article 8 of MiFIR and RTS 2 to immediately publish trading interests in instruments admitted to trading on the Platform, unless a pre-trade transparency waiver applies. Where a pre-trade transparency waiver does not apply, all orders will be made available by Tradeweb on the website operated on behalf of LedgerEdge. LedgerEdge will, in all cases, ensure that data is made available five (5) minutes after publication (where no pre-trade transparency waiver applies).

9.1.3 It is the intention for the Platform to obtain pre-trade transparency waivers under Article 9 of MiFIR, specifically:

• the waiver for illiquid instruments ("Illiquid Waiver") under Article 9(1)(c);

• the waiver for orders that are large in scale ("LIS Waiver") under Article 9(1)(a); and

• the waiver in respect of actionable indications of interest in request-for-quote that are above a size specific to the financial instrument under Article 9(1)(b).

9.1.4 Operationally, in terms of priority, if a bond traded on the Platform is deemed illiquid, the Illiquid Waiver would apply, and if the bond is considered liquid, the LIS Waiver would apply. Where an instrument traded on the Platform is not caught by the waiver, LedgerEdge will make public the current bid and offer prices and the depth of trading interests through live streams on the Platform on a continuous basis during normal market trading hours in the U.K.

9.1.5 The rules that will govern the application of waivers to pre-trade transparency are set out at Rule 15 of the Rulebook.

Post-Trade Transparency

9.1.6 LedgerEdge will, in accordance with Article 10 of MiFIR and RTS 2, immediately publish through an APA details of relevant trades executed on the Platform (including price, volume and trade time), unless a post-trade deferral applies. LedgerEdge will apply for post-trade deferrals. Where the post-trade deferrals do not apply, LedgerEdge will ensure that all data is made available free of charge 5 minutes after publication and is available on a reasonable commercial basis before the 5 minute time period in line with ESMA's guidelines.

9.1.7 It is the intention for the Platform to obtain the following post-trade transparency deferrals under Article 11 of MiFIR. Details of trades subject to the following deferrals are not published under Rule 16.1 until no later than 19:00 U.K. time on the second trading day after the date of the execution of the trade as set out in MiFIR Article 11(1) and Article 8(1) of RTS 2:

• the deferral for illiquid instruments under Article 11(1)(b);

• the deferral for orders that are large in scale under Article 11(1)(a); and