Register today for OSC Dialogue 2024: Inviting, thriving and secure capital markets

Notice of Proposed Change and Request for Comment – Proposed Fee Model for TSX and TSXV Listed Securities Trading on the CSE – Canadian Securities Exchange

Staff of the Ontario Securities Commission (OSC) and British Columbia Securities Commission (Staff or we) are publishing this Notice and Proposed Changes and Request for Comment (Notice) in conjunction with a request for comment on a proposal for a change in trading fees for TSX and TSXV listed securities trading on the Canadian Securities Exchange (CSE) (the 2021 Fee Proposal).

Under the 2021 Fee Proposal, as described in the Notice, trading fees applicable to resting orders of TSX and TSXV listed securities that are executed on the CSE will be calculated based on the nature of the incoming orders against which they execute.

The same fee proposal was published for comment by the OSC on July 7, 2016 (2016 Fee Proposal).{1} At the time, OSC staff requested specific comment on the entire proposal, in particular the impact on fair access and leakage of information. Five public comment letters were received.{2} Following the comment period the CSE decided to withdraw the 2016 Fee Proposal. CSE has now elected to revisit the 2016 Fee Proposal and has, in substantially the same form, filed the 2021 Fee Proposal.

We are requesting comment on the entire 2021 Fee Proposal including in particular the following:

1. Fair access -- how would the Fee Proposal, which entails the passive side of a trade paying trading fees depending on the nature of an incoming order, impact fair access to such passive participants?

2. Informational advantage -- would the passive participant on the CSE have an informational advantage over other market participants since they would have information about the nature of the incoming order flow and, specifically, about the nature of the counterparties to their trades, that is not available to other market participants?

Comments on this Notice should be in writing and submitted by January 24th, 2022 to:

Market Regulation Branch

Ontario Securities Commission

20 Queen St. West, 22nd Floor

Toronto, ON

M5H 3S8

And to:

Michael Grecoff

Securities Market Specialist

British Columbia Securities Commission

701 West Georgia Street

P.O. Box 10142, Pacific Centre

Vancouver, BC V7Y 1L2

Email: [email protected]

And to:

Mark Faulkner

Vice President, Listings and Regulation

CNSX Markets Inc.

100 King Street West, Suite 7210,

Toronto, ON, M5X 1E1

Email: [email protected]

Comments received will be made public on the OSC and BCSC website. Upon completion of the review by Staff, and in the absence of any regulatory concerns, notice will be published to confirm the completion of Staff's review and the intended implementation date of the changes.

Notice: 2021-006

CANADIAN SECURITIES EXCHANGE

SIGNIFICANT CHANGE SUBJECT TO PUBLIC COMMENT

AMENDMENT TO TRADING FEES

NOTICE AND REQUEST FOR COMMENT

December 9, 2021

The Canadian Securities Exchange ("CSE" or the "Exchange") proposes to implement a significant change to its trading fee schedule. The Exchange is publishing this Notice in accordance with the process for the Review and Approval of Rules and the Information Contained in Form 21-101F1 and the Exhibits Thereto attached as Appendix B to the Exchange's recognition orders.

Description of the Change

Background -- In March 2016, the CSE proposed a new fee model on TSX/TSXV listed symbols which was published for comment in CSE Notice 2016-010 (the "2016 Proposal"). Comments received were generally supportive, however in light of specific concerns expressed, the Exchange did not seek regulatory approval to implement the proposed model. Please see "Consultation and Comments Received", below.

Canadian marketplaces have introduced incentives and rules to encourage liquidity providers to be more aggressive on size and price. These include inverted fee mechanisms, speed bumps which apply to only some members of the trading community, and variable fee mechanisms, including some designed to encourage "dark sweeps" before an order is worked in the lit market.

The 2016 Proposal was intended to achieve similar objectives, those being increased liquidity provision size, improved priced discovery and lower execution costs. There are no material differences between the 2016 Proposal and the current proposal.

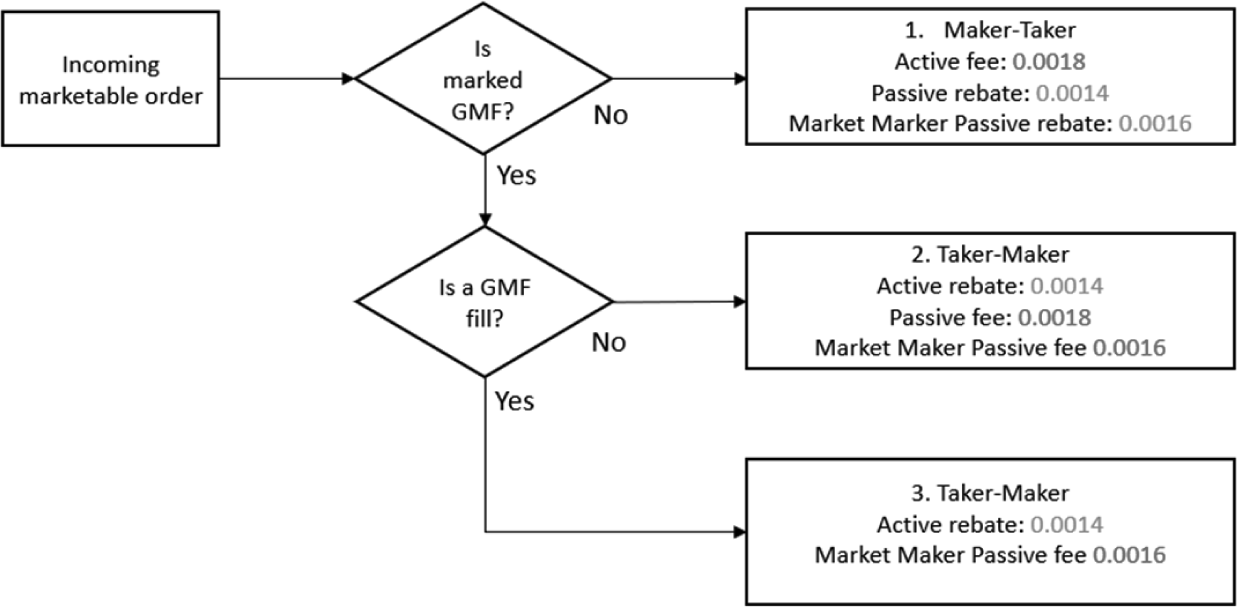

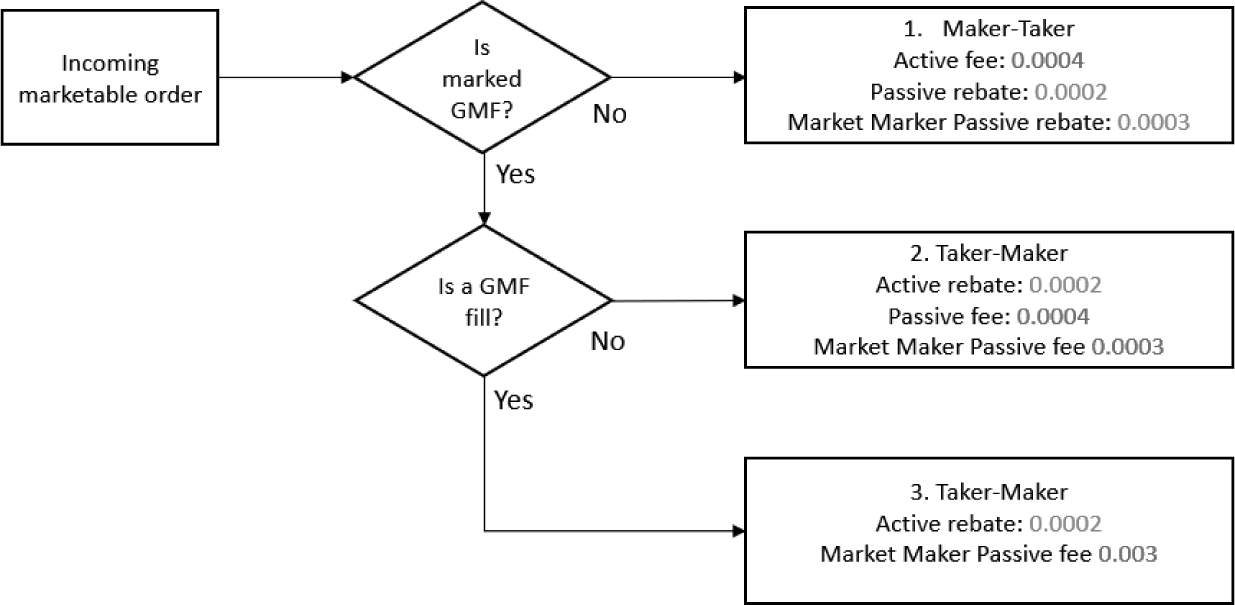

Proposed Fee Model -- Applicable to TSX and TSXV listed securities trading on the CSE:

1. Incoming order is not GMF (Guaranteed Minimum Fill) eligible -- if the incoming order is not marked as GMF eligible then a Maker-Taker pricing model is applied whereby the active side is assessed a fee ($0.0018 if >= $1 and $0.0004 if <$1) and the passive side is given a rebate (-$0.0014 if >=$1 and --$0.0002 if <$1).

2. Incoming order is GMF eligible with a trade occurring in the continuous auction market -- if the incoming order is marked GMF eligible and trades with a resting order, then a Taker-Maker pricing model is applied whereby the active side is given a rebate (-$0.0014 if >=$1 and --$0.0002 if <$1) and the passive side is assessed a fee ($0.0018 if >=$1 and $0.0004 if <$1).

3. Incoming order is GMF eligible and the residual volume trades on the GMF facility -- if the incoming order is marked GMF eligible and the trade occurs against the GMF facility then a Taker-Maker pricing model is applied whereby the active side is given a rebate (-$0.0014 if >=$1 and --$0.0002 if <$1) and the passive side is assessed a fee ($0.0016 if >=$1 and $0.0003 if <$1).

Pricing Model Flow Chart -- To assist in explaining the model a Fee Flow Chart is provided with the proposed pricing for both TSX and TSXV securities.

Greater than or equal to $1

Less than $1

Pricing Model Scenarios

|

Scenario 1: GMF eligible Securities Order Flow on >= $1 |

||||||||||||

|

|

||||||||||||

|

QUOTE |

|

|

|

|

|

|||||||

|

|

||||||||||||

|

SYMBOL |

BID SIZE |

BID |

ASK |

ASK SIZE |

GMF SIZE |

|

|

|||||

|

|

||||||||||||

|

ABC |

400 |

10.00 |

10.01 |

500 |

1000 |

|||||||

|

|

|

|

|

|

|

|

|

|||||

|

An incoming GMF eligible client order is received for the purchase of 600 shares. 500 shares will fill at the offer price of 10.01. The balance of 100 shares will fill against the Market Maker ("MM") in the GMF facility. |

||||||||||||

|

|

||||||||||||

|

A Taker-Maker fee model applies. |

||||||||||||

|

|

||||||||||||

|

GMF client: Bought 500 shares at $10.01 from resting passive order, active order rebate $-0.0014. |

|

|||||||||||

|

Resting passive order: Sold 500 shares at $10.01, there will be a passive order fee of $0.0018, or, if the order was posted by the MM, then a passive fee of $0.0016. |

||||||||||||

|

|

||||||||||||

|

GMF client: Bought 100 shares at $10.01 from MM in GMF facility, active order rebate $-0.0014. |

||||||||||||

|

|

||||||||||||

|

GMF Market Maker: Sold 100 shares at $10.01, passive order fee $0.0016. |

||||||||||||

|

Scenario 2: Non-GMF eligible Securities Order Flow on >= $1 |

||||||||||||

|

|

||||||||||||

|

QUOTE |

|

|

|

|

|

|||||||

|

|

||||||||||||

|

SYMBOL |

BID SIZE |

BID |

ASK |

ASK SIZE |

GMF SIZE |

|

|

|||||

|

|

||||||||||||

|

XYZ |

300 |

10.00 |

10.01 |

200 |

500 |

|||||||

|

|

|

|

|

|

|

|

|

|||||

|

A non-GMF eligible order to purchase 200 shares is entered. The order is filled by the 200 shares at the posted offer price of $10.01. |

||||||||||||

|

|

||||||||||||

|

A Maker-Taker fee model applies. |

||||||||||||

|

|

||||||||||||

|

Incoming order: Bought 200 shares at $10.01, active order fee $0.0018 |

||||||||||||

|

|

||||||||||||

|

Resting booked order: Sold 200 shares at $10.01, passive order rebate --$0.0014, or, if the order was posted by the MM, then a rebate of --$0.0016. |

||||||||||||

|

|

||||||||||||

|

GMF Market Maker: no interaction, non-GMF eligible order |

||||||||||||

|

Scenario 3: GMF eligible Securities Order Flow on <$1 |

|||||

|

|

|||||

|

QUOTE |

|||||

|

|

|||||

|

SYMBOL |

BID SIZE |

BID |

ASK |

ASK SIZE |

GMF SIZE |

|

|

|||||

|

EFG |

4000 |

0.80 |

0.81 |

5000 |

8000 |

|

|

|||||

|

An incoming GMF eligible client order is received for the purchase of 6000 shares. 5000 shares will fill at the offer price of 0.81. The balance of 1000 shares will fill against the Market Maker ("MM") in the GMF facility. |

|||||

|

|

|||||

|

A Taker-Maker fee model applies. |

|||||

|

|

|||||

|

GMF client: Bought 5000 shares at $0.81 from a resting passive order, active order rebate $-0.0002. |

|||||

|

|

|||||

|

Resting passive order: Sold 500 shares at $0.81, passive order fee of $0.0004, or, if the order was posted by the MM, then a fee of $0.0003. |

|||||

|

|

|||||

|

GMF client: Bought 100 shares at $0.81 from MM in the GMF facility, active order rebate $-0.0002. |

|||||

|

|

|||||

|

GMF Market Maker: Sold 100 shares at $0.81, passive order fee $0.0003. |

|||||

|

Scenario 4: Non-GMF eligible Securities Order Flow on <$1 |

|||||

|

|

|||||

|

QUOTE |

|||||

|

|

|||||

|

SYMBOL |

BID SIZE |

BID |

ASK |

ASK SIZE |

GMF SIZE |

|

|

|||||

|

QWE |

3000 |

0.50 |

0.51 |

2000 |

5000 |

|

|

|||||

|

A non-GMF eligible order to purchase 2000 shares is entered. The order is filled by the 2000 shares at the posted offer price of $0.51. |

|||||

|

|

|||||

|

A Maker-Taker fee model applies. |

|||||

|

|

|||||

|

Incoming order: Bought 2000 shares at $0.51, active order fee of $0.0004. |

|||||

|

|

|||||

|

Resting booked order: Sold 2000 shares at $0.51, a passive order rebate of --$0.002, or, if the order was posted by the MM, then a rebate of --$0.0003. |

|||||

|

|

|||||

|

GMF: no interaction, non-GMF eligible order |

|||||

Expected Implementation Date:

The proposed fee changes are expected to be implemented upon receipt of regulatory approval.

Rationale and Analysis

The rationale and analysis is largely unchanged since the 2016 Proposal.

Specifically, the CSE seeks to:

• Improve fill quality and fill size per agency order which will, in turn, lower dealer back-office costs and reduce information leakage caused by the current practice of multiple sweeps.

• Protect passive liquidity providers against specific proprietary trading strategies, allowing visible quotes to persist long enough to interact with incoming GMF eligible orders.

• Maintain reduced execution costs for investment dealers managing GMF-eligible orders by continuing to provide a rebate for active orders on the TSX and TSXV listed securities.

Expected Impact

The CSE anticipates the following outcomes if the proposal is adopted:

1) by improving the economics of trading with GMF eligible Orders the CSE expects to see an increase in the number of firms willing to participate on the CSE, resulting in an increase in posted liquidity at the NBBO and a better outcome for marketable inbound GMF eligible order flow.

2) Increased execution quality and average trade size on the CSE, resulting in fewer executions to satisfy each client order across multiple marketplaces, less information leakage to alternate marketplaces, and less opportunity for quote fade.

3) by using standard maker-taker pricing for resting orders trading against orders that are likely generated from clients executing proprietary strategies (i.e., non-GMF Orders), a measure of protection for the providers of liquidity is provided against proprietary trading strategies. This measure should encourage third party liquidity providers to layer the CSE book with resting orders and encourage the Market Maker to increase the size of their GMF commitment.

Compliance with Securities Law

There will be no impact on the CSE's compliance with Ontario or British Columbia securities law. The changes will not adversely affect fair access or the maintenance of fair and orderly markets. The changes are consistent with the fair access requirements set out in section 5.1 of NI21-101 as they are not confined to a limited number of marketplace participants and all marketplace participants will remain subject to the same rules and conditions.

Consultation & Comments Received

The CSE has consulted extensively, including with current and prospective Market Makers and investment dealers executing agency order flow. Most dealers support the goal of assisting in the execution of agency orders in ways that encourage larger average trade size and overall improved execution quality, while limiting information leakage and potential "quote fade". Dealers consulted also support the notion of achieving these goals through the use of price incentives, instead of through the introduction of complicated order types, speed bumps or separate and segregated books.

The 2016 Proposal and Request for Comments

The 2016 Proposal was published by the OSC on July 7, 2016. In response to the request for comments, CSE received five comment letters from industry participants{3}. Four of the comment letters came from the dealer community (Leede Jones Gable (LJB), CIBC World Markets (CIBC), RBC Dominion Securities (RBC), and Scotia Capital (BNS)), and one from the Trading Issues Committee of the Canadian Security Traders Association (CSTA). In addition, two other dealers, TD Securities (TD) and ITG Canada (ITG), commented on the CSE's proposals in client publications devoted to developments in Canadian markets.

OSC Market Regulation Staff ("Staff") requested specific comment{4} on:

Fair Access -- Staff question whether the Fee Proposal would be unfair to passive participants because their fees are determined by the nature of an incoming order and not by their own actions or decisions.

Leakage of Information -- Staff are concerned that the Fee Proposal would allow for passive participants in the CSE to have an informational advantage over other marketplace participants, as they would know, based on the fee they pay, whether they are trading against GMF Orders (i.e., "agency" or "non-agency") orders. This information is not available to any other marketplace participant. We note CSE's assertions against the "real time" information leakage, but remain concerned that passive participants would have information that allows them to determine the type of counterparty to the trade.

Comments Specific to Fair Access:

• Three commenters (LJG, BNS and CIBC) did not have any concerns with the variable pricing for passive participants, although BNS did express general concerns about the effort required by a dealer to track the fees applicable to specific trades across all markets. The three dealers agreed with the CSE's view that the participants posting orders to the CSE's book were capable of measuring the impact of the variable pricing model.

• One commenter (RBC), while expressing no particular view on the fairness question, expressed concerns about the technological impact on dealers of order types and identifiers being introduced by marketplaces.

• One commenter (CSTA) submitted that the CSE's proposal would violate fair access principles. The concern appears to be based mainly on the danger of the precedent being set if the CSE proposal is approved. Although an agency account could currently avoid the impact of the CSE's approach by posting on another marketplace, if marketplaces with a significant market share were permitted to implement a similar model, the ability to avoid the impact of the model would be sharply reduced. On that basis, the CSTA committee submitted, the fact that the CSE has a non-material amount of resting agency orders in its book is not relevant to the analysis.

CSE Response to Comments on Fair Access

We belatedly thank the five commenters for submitting their views on the CSE's proposal. As set out in the 2016 Proposal, the object of the pricing model is to encourage better priced and larger sized orders being committed to the CSE book. Both objectives contribute to the overall goal of assisting firms seeking better quality and more cost-effective execution for their retail orders. Canadian market structure rules have long provided for the segmentation of orders for the purposes of execution priority, access to automated execution facilities, price improvement and many other advantages. The variable fee model proposed may be seen in the same light: by reducing the costs to the dealer executing the order (whether the benefit is shared with a client or not), the model will make the Canadian visible market more competitive versus other execution modalities available. These would include US wholesalers and dark markets, neither of whom contribute to the price discovery provided by the continuous auction market.

The Exchange is sensitive to concerns from the community about the impact on dealers to both access and administer the new trading fee model. In devising the model, the CSE sought to minimize the impact by using standard message tags and leveraging its existing service for reporting fees on a daily basis to dealers on a fully granular basis.

CSE was also reminded that institutional orders do rest, from time to time, in the CSE book. As with the 2016 Proposal, the current proposal does not in any way restrict entry of such orders.

Knowledge and analysis of the fee model of a marketplace is an integral part of the decision to post an order at a specific marketplace and participants devote considerable research effort to determine the most cost-effective way to pursue different trade execution strategies. Market participants will continue to assess the risks and opportunities associated with the CSE's fee structure in advance of booking any orders for TSX/V securities on CSE and therefore posting liquidity on the CSE for TSX/V listed securities is done on an opt-in basis. No passive orders for TSX or TSX Venture listed securities are or will be routed or otherwise entered on the CSE without the participant making the informed, strategic choice to do so. In a vast array of order execution alternatives, the CSE proposal does not restrict access in any way but rather provides additional options for marketplace participants to pursue their trading objectives. This fee model is intended to increase price-improvement competition with greater commitment to order size and market making capital, which will directly improve the best/bid offers available to interact with marketable in-bound orders. With a plethora of alternatives available to post resting orders, any fee outcome based on an informed decision and a transparent fee schedule should be considered fair.

Comments Specific to Leakage of Information:

• Three commenters (LJG, BNS and CIBC) either believed that the benefits of the 2016 Proposal outweighed any concerns about information leakage or that there were no information advantages in fact conferred on the market maker in view of the fact that the information was only made available at the end of day.

• One commenter (BNS) indicated a preference for real-time information and supported the availability of information being made publicly available "if there are fairness concerns about only the counterparty having access to this information."

• One commenter (RBC) expressed no opinion on the question.

• One commenter (CSTA) expressed the view that the CSE model would provide fee data that "may be indicative of large directional multi-day orders and allow those particular participants to construct a mosaic of institutional activity." This advantage could result in an increase in trading costs to the institutional client, presumably (the CSTA submission is not detailed on the point) because they would not be taking advantage of the inverted fee model available to GMF-eligible clients, and through some form of adverse selection opportunities afforded to the liquidity provider in view of the information advantage. CSTA objected to the proposal on the basis that any informational advantage is not appropriate and should be prevented.

CSE Response to Comments on Information Leakage

The CSE will not provide a real-time mechanism that could be used to identify if an active order was GMF eligible. The only order type classifications that will be available (same as currently) are: provided liquidity (P), took liquidity (T), cross (C) and dark (D). To learn whether a counterparty on a particular trade was for a GMF eligible Order or not, the liquidity provider would need to collate its daily fill report with their daily billing report (each being available in the evening at approximately 6:30 p.m. each trading day).

The Exchange distributes an end-of-day fee file to each Dealer between 6-7 PM every day. Within this file is contained a record of all the Dealer trades for the day, whether the Dealer was active or passive on any particular trade, and the fee/rebate associated with the trade. Important information which is not contained in this end-of-day file is the counterparty to any trade. A Dealer would be able to determine whether, based on only their subset of passive orders, the percentage of active flow they traded against which was GMF eligible or non-GMF eligible. A Dealer could potentially reconcile the fee for each trade with the public tape to determine the Dealer on the opposite side of the trade and know whether the order was marked as GMF eligible, but could not identify the account type, volume or limit price of the order. The resulting collation would provide the participant number for the passive side of the trade and an indication as to whether the contra side of the trade was marked GMF eligible. This information would be unlikely to cause either party to the trade to materially alter their strategies. Further, GMF fills can already be distinguished with a reasonable degree of certainty from non-GMF trades due to their nature of being printed once visible liquidity is exhausted.

In considering whether the fee data represents information leakage to the point at which fair access is a concern, CSE notes the following:

GMF eligibility on any specific order does not definitively indicate the intention, or type of participant, behind the order.

For an order to be GMF eligible it must be a marked as 'client' and be at or below the GMF guarantee size on any security to be eligible for execution in the GMF facility. Although it is more likely that GMF eligible orders will be on behalf of retail clients, this is not a certainty. GMF eligible orders can also be managed institutional client flow which fall within the GMF size.

The CSE has some of the largest GMF sizes per symbol among Canadian marketplaces. GMF size is not retractable by the Market Maker during the trading day, making it a suitable tool for institutions (because of the size of the commitments) to get complete fills and reduced execution costs on smaller orders. Large orders can already be estimated by other participants to be institutional in nature. A GMF-eligible tag on orders within the GMF size gives no additional information as to who the participant is or what their strategy might be, especially when that information is not available until after the market close on a given day.

There is no indication the information in the end-of-day file would be actionable to anyone in developing or implementing a trading strategy.

Similar information has been provided by all marketplaces for some time and are accepted features of the Canadian marketplace. See, for example, the two examples below, which, despite potential misuse, have been accepted because the obvious benefits outweigh the potential risks.

• Speedbumps have increased quote fade on certain venues, and should qualify as actionable information leakage, but they also have the positive effect of increasing the quoted displayed volume and improving price discovery.

• Resting dark orders with a minimum quantity allow a participant to gauge the size of other participant's active orders, resulting in information leakage, but at the same time they also protect dark posters from getting hit by toxic order flow probing for liquidity which encourages better liquidity provision.

The concern previously described in the CSTA comment letter{5} only suggests the information may be indicative and may allow a participant to determine institutional activity. The possible analysis described in the CSTA letter would be inconclusive because it only permits the passive liquidity provider to make assumptions of overall activity based on counterparties to only its own trades, not all trades or orders. Further, the simple distinction between retail and institutional orders made in that comment letter is not accurate, as those are not the criteria for the proposed pricing mechanism.

There is no evidence that the proposed fee structure would directly or indirectly provide any meaningful information that could reasonably be incorporated into a viable trading strategy.

Additional Comments Received

Segmentation of Order Flow:

Following the submission of the 2016 Proposal the CSE has participated in additional formal and informal discussions with industry participants on the pricing model. Participants with an institutional equity trading orientation have tended to criticize the CSE's approach on the basis that it promotes an additional layer of "order segmentation". In other words, they believe restricting institutional client access to the predominately retail order flow represented by "GMF eligibility", will result in increased trading costs for their clients and potential harm to the price discovery process. As discussed above, order segmentation is already deeply engrained in Canadian equity market structure. The minimum guarantee fill facility at the Toronto Stock Exchange dates back decades and provides for automated execution of eligible retail orders against the responsible registered trader's book. The CSE's GMF facility operates in similar fashion. We also permit segmentation of flow by dealer (the broker preference rule) and by size (the client order handling rule). Institutional clients have seen an enormous amount of investment over the years in systems that are designed to permit them to locate the trade size they need without suffering the consequences of exposing their trading intentions to the broader market. There are no complaints, to our knowledge, that retail clients aren't somehow able to access these pools of potential liquidity.

The application of different rules, prices and trading modalities to the various kinds of orders present in the market is a well-accepted principle of Canadian equity market structure.

Complexity:

The Exchange has also been made aware of concerns, expressed most clearly in the comment letter from RBC, about the continuing increase in the complexity of Canadian equity market structure. While many dealers support continued investment in innovation from the marketplaces designed to improve liquidity and reduce costs, a number of parties have expressed concern about the impact of these changes on the dealers (and supporting vendors) who have to integrate these services into their order routing, order management, risk and compliance systems.

As the CSE has discussed in this comment summary and in the 2016 Proposal, the design of the CSE's variable fee model was intended to lessen the operational impact on the trading community. The Exchange has sought to deliver the benefits of the variable pricing programme to retail accounts by using existing message tags, trade reporting and information systems. It is an unfortunate reality that some level of increased complexity is inevitable as marketplace operators seek to distinguish themselves from their competitors. In designing the variable pricing programme to deliver key benefits to the retail-oriented dealers and their clients, CSE has taken every possible step to minimize the impact on its client base.

Application of Fee Change to Participants

The proposed fee model will apply to all participants, for all TSX and TSX Venture listed securities traded on CSE. There is no differential treatment across marketplace participants and all participants can place GMF eligible orders where the order meets the GMF eligibility requirements.

In certain circumstances participants may benefit by receiving a rebate and in others they will incur a cost. The mechanism by which this occurs is detailed in Section A.

Expected impact of the Rule or Change on the systems of members and service vendors

There is little, or no, expected impact on the systems of members and service vendors. Trading members already have the capability to mark orders as GMF eligible before sending them to the marketplace. There is no additional development work required.

Alternatives

Other Canadian marketplaces have achieved similar goals through the introduction of separate books with distinct fee structures and unique market features. These marketplaces have introduced order types and features (like speedbumps) offering protection to passive liquidity providers from unwanted inbound order flow, this has resulted in quote fade to the detriment of all participants in Canada.

There has been little support in Canada from market participants for the introduction of new market venues where there is little in the way of innovation as participants and vendors are forced to incur connection costs along with increased complexity in determining order management strategies.

The CSE is proposing price methods to achieve similar goals. This has the net benefit of not needing to introduce additional market venues and complexity or increase the opportunities for quote fade by passive participants.

Other Markets or Jurisdictions

Both quote and order driven systems around the world have struggled to find ways to encourage market makers to increase their quoted size while broadening the range of stocks covered by their liquidity provision efforts.

To summarize, these efforts have typically involved one or more of the following models:

• Participation preference for market makers on incoming marketable orders.

• Pricing advantages or incentives over other resting orders in a book.

• Queue priority advantages based on participant category.

• Protection against interaction with proprietary or other "non-natural" order flow.

Comments

In concept and intent, these models are no different from the pricing model proposed in this submission.

Please submit comments on the proposed amendments no later than January 24th, 2022 to:

CSE

Mark Faulkner

Vice President, Listings and Regulation

CNSX Markets Inc.

100 King Street West, Suite 7210

Toronto, ON, M5X 1E1

Fax: 416.572.4160

Email: [email protected]

Ontario Securities Commission

Market Regulation Branch

Ontario Securities Commission

20 Queen Street West, 20th Floor

Toronto, ON, M5H 3S8

Fax: 416.595.8940

Email: [email protected]

British Columbia Securities Commission

Michael Grecoff

Securities Market Specialist

British Columbia Securities Commission

701 West Georgia Street

P.O. Box 10142, Pacific Centre

Vancouver, BC V7Y 1L2

Email: [email protected]

{1} Available at https://www.osc.ca/en/industry/market-regulation/marketplaces/exchanges/recognized-exchanges/canadian-securities-exchange-cse-rule-review-notices/notice-proposed-change

{2} Available at https://www.osc.ca/en/industry/market-regulation/marketplaces/exchanges/recognized-exchanges/canadian-securities-66/comments-received

{3} Comments for: Notice of Proposed Change and Request for Comment -- CNSX Markets Inc. | OSC (gov.on.ca)

{4} Notice of Proposed Change and Request for Comment -- CNSX Markets Inc. | OSC (gov.on.ca)

{5} https://www.osc.ca/sites/default/files/2021-01/com_20160802_csta.pdf