CSA and CCIR Joint Notice and Request for Comment – Proposed Amendments to National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations and to Companion Policy 31-103CP Registration Requirements, Exemptions and Ongoing Registrant Obligations and Proposed CCIR Individual Variable Insurance Contract Ongoing Disclosure Guidance Total Cost Reporting for Investment Funds and Segregated Funds

CSA and CCIR Joint Notice and Request for Comment – Proposed Amendments to National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations and to Companion Policy 31-103CP Registration Requirements, Exemptions and Ongoing Registrant Obligations and Proposed CCIR Individual Variable Insurance Contract Ongoing Disclosure Guidance Total Cost Reporting for Investment Funds and Segregated Funds

Introduction

The Canadian Securities Administrators (the CSA) and the Canadian Council of Insurance Regulators (the CCIR, together, the Joint Regulators or we), are publishing, for a 90-day comment period, proposed enhanced cost disclosure reporting requirements for investment funds and new cost and performance reporting requirements for individual variable insurance contracts or IVICs (referred to here as Segregated Fund Contracts), as described below (collectively, the Proposals).

The Proposals have been developed by a joint project committee composed of members from the CSA, CCIR, Canadian Insurance Services Regulatory Organizations (CISRO), Investment Industry Regulatory Organization of Canada (IIROC) and the Mutual Fund Dealers Association of Canada (MFDA) (together referred to as the SROs) (the Project Committee). The Proposals follow on work securities regulators began after the completion of the Client Relationship Model, Phase 2 (CRM2) project in 2016 and recommendations published by the CCIR in a December 2017 position paper on segregated funds, as revised in June 2018 (CCIR Segregated Funds Position Paper).

The Proposals for the securities sector (the Proposed Securities Amendments) are for amendments to National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103 or the Instrument) and Companion Policy 31-103CP Registration Requirements, Exemptions and Ongoing Registrant Obligations (31-103CP or the Companion Policy).

The Proposals for the insurance sector are for an Individual Variable Insurance Contract Ongoing Disclosure Guidance (the Proposed Insurance Guidance) -- an enhanced disclosure framework for Segregated Fund Contracts. The CCIR expects each of its member jurisdictions will adopt the framework by local guidance or, in certain jurisdictions, regulation. In addition to including cost and performance reporting guidance, the Proposed Insurance Guidance also includes additional ongoing performance disclosure guidance designed to bring the insurance sector into closer harmony with the securities sector, as well as guidance with respect to ongoing disclosure with respect to Segregated Fund Contract guarantees.

The Proposed Securities Amendments would apply to all registered dealers, advisers and investment fund managers. The Proposed Insurance Guidance would apply to all insurers offering Segregated Fund Contracts to their policy holders.

This notice contains the following annexes:

• Annex A -- Specific questions regarding the Proposed Securities Amendments

• Annex B -- Specific questions regarding the Proposed Insurance Guidance

• Annex C -- Proposed Amendments to NI 31-103

• Annex D -- Proposed changes to 31-103CP

• Annex E -- Blackline showing changes to NI 31-103 under the Proposed Amendments

• Annex F -- Blackline showing changes to 31-103CP under the Proposed Amendments

• Annex G -- Sample prototype statement and report for the securities sector

• Annex H -- Sample prototype report for the insurance sector

• Annex I -- Local matters

• Annex J -- Proposed Insurance Guidance

• Annex K -- Segregated funds and investment funds: differences between products, distribution channels and regulation

This notice will be available on the following websites of CSA jurisdictions:

This notice will also be available on the CCIR website: https://www.ccir-ccrra.org.

Substance and Purpose

The Proposals are part of the Joint Regulators' harmonized response to concerns we have identified relating to current cost disclosure and product performance reporting requirements for investment funds and segregated funds. The Proposed Insurance Guidance also addresses concerns about ongoing disclosure regarding Segregated Fund Contract guarantees. We seek to enhance investor protection by improving investors' and policy holders' awareness of the ongoing embedded fees such as management fund expense ratios (MER) and trading expense ratios (TER) that form part of the cost of owning investment funds and segregated funds. The Proposed Insurance Guidance also seeks to enhance policy holder protection by improving policy holders' awareness of their rights to guarantees under their Segregated Fund Contracts and how their actions might affect their guarantees.

One important concern is that there are currently no requirements for securities industry registrants or insurers to provide ongoing reporting to investors and policy holders on the amount of such costs after the initial sale of the investment product, in a form which is specific to the individual's holdings and easily understandable. While fund facts and ETF facts documents required to be delivered at the point of sale for some investment funds contain certain disclosure concerning the ongoing costs of ownership of those funds, those documents are not tailored to the individual's holdings or required to be delivered on an ongoing basis and this requirement only applies to a subset of investment funds{1}.

Research carried out by the Ontario Securities Commission's (OSC) Investor Office and the Behavioural Insights Team){2} in connection with the adoption of CRM2 shows that Canadian investors presented with a sample annual charges and compensation report, assumed that it included embedded fees associated with investment funds, when it does not include such fees.{3}

We believe it is important that investors and policyholders be aware of all of the costs associated with the investment funds and segregated funds they hold, as these fees can impact their returns and have a compounding effect over time. Furthermore, transparency about costs may encourage more competition, which would benefit investors and policyholders.

The Proposals would require disclosure of the ongoing costs of owning Segregated Fund Contracts and investment funds, both as a percentage, for each fund or segregated fund, and as an aggregate amount, in dollars, for all investment funds or investments in a Segregated Fund Contract held during the year.

The Proposals are as consistent as possible between the securities and insurance sectors with respect to disclosure of the ongoing costs of owning Segregated Fund Contracts and investment funds, taking into account the material differences among those products and in the ways the two sectors and their regulatory regimes operate. Differences include who provides cost disclosure to clients, how often account statements are typically sent, distribution channels and product features, as indicated in the table in Annex K.

Summary of Proposals

Securities sector

The Proposed Securities Amendments would add the following new elements to client reporting under NI 31-103:

• in the account statement (s.14.14) or additional statement (s.14.14.1) as appropriate, the fund expense ratio, stated as a percentage for each investment fund held by the client; and

• in the annual report on charges and other compensation (s.14.17) for the account as a whole:

• the aggregate amount of fund expenses, in dollars, for all investment funds held during the year; and

• the aggregate amount of any direct investment fund charges (e.g., short-term trading fees or redemption fees), in dollars.

Fund expenses would be calculated by reference to the fund expense ratio, which would be defined as the sum of the MER and the TER. This definition is consistent with how that term is used in the context of a mutual fund's fund facts document and with how the term "ETF expenses" is used in the ETF Facts document.{4} The methodology for determining the information included in the reports would be prescribed in order to ensure comparability for investors and a level playing field for registrants. Explanatory notes, substantially in a prescribed form tested with investors, would be included as appropriate.

The Proposed Securities Amendments would apply to all registrants to which the requirements to deliver an account statement, additional statement or annual cost and compensation report currently apply,{5} in respect of all investment funds owned by their clients, including scholarship plans, labour sponsored funds, foreign funds, mutual funds, non-redeemable investment funds, prospectus-exempt investment funds and exchange-traded funds.

Existing exemptions for statements and reports provided to non-individual permitted clients (including, for example, many different institutional investors), pursuant to subsections 14.14.1(6) and 14.17(5) of NI 31-103, would continue to apply. SRO rules would be amended to be uniform in substance with final amendments to NI 31-103.

Registered investment fund managers would be required to provide the registered dealers and registered advisers with certain information that the dealers and advisers would require in order to prepare the enhanced statements and reports for their clients.

The Proposed Securities Amendments would allow investment fund managers to rely on publicly available information disclosed in an investment fund's most recently published fund facts document, ETF facts document, prospectus or management report of fund performance, unless this information is outdated, or the investment fund manager reasonably believes that doing so would cause the information reported in the statement or report to be misleading.

If advisers or dealers are unable to rely on information provided by investment fund managers or believe that doing so would cause the information reported in the statement or report to be misleading, they would be required to rely on the most recent publicly available information in the relevant fund facts document, ETF facts document, prospectus or management report of fund performance, and if they cannot do so, would be required to make reasonable efforts to obtain that information by other means.

We believe this approach would adequately balance the need for investors to receive information about the ongoing costs of owning investments funds, while avoiding imposing an undue regulatory burden on registrants.

Insurance sector

The Proposed Insurance Guidance would express the CCIR's expectation that insurers would provide certain information to clients who own Segregated Fund Contracts at least once each year. The full list of these elements of disclosure is found in Annex J.

With respect to costs of holding Segregated Fund Contracts, these elements include:

• the fund expense ratio, stated as a percentage for each segregated fund held by the client within their Segregated Fund Contract during the statement period; and

• for the Segregated Fund Contract as a whole:

• the aggregate amount of fund expenses, in dollars, for all segregated funds held during the statement period;

• the aggregate cost of insurance guarantees under the Segregated Fund Contract, in dollars, for the statement period; and

• the aggregate amount of all other expenses under the Segregated Fund Contract, in dollars, for the statement period.

The statement period would be no more than one year.

The fund expense ratio would be defined as the sum of the MER and the TER. The methodology for determining the information included in the statements would be prescribed in order to ensure comparability for investors and a level playing field for insurers and agents. Explanatory notes, substantially in a prescribed form tested with investors, would be included as appropriate.

The remaining elements of the ongoing disclosure would reflect the expectations set out in the CCIR Segregated Funds Position Paper, except as follows:

• insurers would be expected to report the total deposits, withdrawals and the change in value of segregated funds since the Segregated Fund Contract began and since the start of the previous statement period.

• In contrast, the CCIR Segregated Funds Position Paper recommended reporting the aggregated dollar value change in net asset value of the Segregated Fund Contract.

• with respect to the amount the client would receive upon redeeming the entire Segregated Fund Contract, insurers would be expected to:

• include a notice, substantially in a prescribed form, that explains the total net asset value for the contract is not necessarily the amount the client would receive if they ended their contract, and explains how the client could obtain more details about the amount of money they would receive, and

• if the costs incurred at the redemption would be significant, include a notice, substantially in a prescribed form, that explains these costs.

• insurers would be expected to indicate whether a deferred sales charge may apply to each segregated fund; and

• when a Segregated Fund Contract provides a guaranteed income payment, insurers would be expected to state how long the guaranteed payment would be payable.

Insurance regulators in each jurisdiction will implement this initiative in line with their respective regulatory requirements.

Prior Consultations

In developing the Proposals, the Joint Regulators conducted extensive consultations with investor advocates and market participants, notably at a meeting of the Joint Forum of Financial Market Regulators{6} held on June 10, 2021, as well as through informal technical consultations with industry associations and service providers.

Prior to beginning the joint project, CCIR consulted with stakeholders with respect to disclosure of fees and performance through an Issues Paper released for public consultation in May 2016 and discussion directly with stakeholders. These consultations led to the 2017/2018 CCIR Segregated Funds Position Paper, which set out CCIR's expectations regarding cost disclosure. CCIR continued related research, including through investor focus groups, between the release of the Position Paper and the start of the joint project.

The Project Committee also worked with OSC Investor Office Research and Behavioural Insights Team (IORBIT), drawing in part on earlier research commissioned by the MFDA, to design seven prototype disclosure documents for the securities sector, which differed both in terms of substantive content and presentation. Four prototypes were developed for the insurance sector. IORBIT then tested the prototypes to determine which ones would be most effective in maximizing investor or policyholder's comprehension of cost information. The Proposed Amendments reflect the findings from IORBIT's research. The final prototypes are included in Annex G and H as illustrative examples, showing what statements and reports could look like if the Proposed Amendments were adopted, with the new information highlighted.{7}

Transition

We recognize that developing and implementing system enhancements to implement the Proposals will require a significant investment of time and resources by industry stakeholders. However, we firmly believe that providing both investors and policyholders with essential information about the ongoing embedded costs of investment funds and segregated funds at the earliest possible date is a priority. We therefore intend to adopt a short transition period for both the securities sector and the insurance sector.

We are proposing that both sectors move forward in lockstep, with final amendments coming into effect at the same time in September 2024, as further detailed below, assuming that final publication would occur and ministerial approvals be obtained during the second quarter of 2023. This would represent a transition period of approximately 18 months. Registrants and insurers would be required to deliver statements and reports compliant with the Proposals as of the first reporting periods that fall entirely after this date.

In practical terms, this means that

• for the securities sector, investors would receive the first quarterly account statements containing the newly required information for the reporting period ending in December 2024, and the first annual reports containing the newly required information for the reporting period ending in December 2025; and

• for the insurance sector, policyholders would receive an annual report containing the newly required information for the reporting period ending in December 2025, and a half-yearly statement containing the newly required information for the reporting period ending in June 2025, in the case where such statements are delivered.

We are proposing this approach considering the importance of this initiative for investors and policyholders and the fact that pre-consultations with industry stakeholders and investor advocacy groups have taken place and will continue. We strongly encourage registrants and insurers to begin reviewing their systems and conduct advanced planning as soon as possible in order to have all of the resources necessary for implementation in place on time, following the final publication and ministerial approvals. If you have comments on this transition period proposal, please provide detailed discussion of the comments in your submission.

Request for Comments

We welcome your comments on the Proposals and questions in Annexes A and B.

We cannot keep submissions confidential because securities legislation in certain provinces requires publication of a summary of the written comments received during the comment period. All comments with respect to the Proposed Securities Amendments will be posted on the websites of each of the OSC at www.osc.ca, the Alberta Securities Commission at www.albertasecurities.com and the Autorité des marchés financiers at www.lautorite.qc.ca. Therefore, you should not include personal information directly in comments to be published. It is important you state on whose behalf you are making the submissions.

Similarly, all comments with respect to the CCIR Guidance may be posted on the CCIR website.

Deadline for Comments

Please submit your comments in writing on or before July 27, 2022. If you are not sending your comments by email, please send a CD containing the submissions in Microsoft Word format.

Comments on Proposed Securities Amendments:

Address your submission to the CSA jurisdictions as follows:

Alberta Securities Commission

Autorité des marchés financiers

British Columbia Securities Commission

Financial and Consumer Services Commission (New Brunswick)

Financial and Consumer Affairs Authority of Saskatchewan

Manitoba Securities Commission

Nova Scotia Securities Commission

Nunavut Securities Office

Office of the Superintendent of Securities, Newfoundland and Labrador

Ontario Securities Commission

Office of the Superintendent of Securities, Northwest Territories

Office of the Yukon Superintendent of Securities

Superintendent of Securities, Department of Justice and Public Safety, Prince Edward Island

Deliver your comments only to the addresses listed below. Your comments will be distributed to the remaining CSA jurisdictions.

Me Philippe Lebel

Corporate Secretary and Executive Director, Legal Affairs

Autorité des marchés financiers

Place de la Cité, tour Cominar

2640, boulevard Laurier, bureau 400

Québec (Québec) G1V 5C1

Fax: 514-864-6381

[email protected]

The Secretary

Ontario Securities Commission

20 Queen Street West

22nd Floor, Box 55

Toronto, Ontario

M5H 3S8

Fax: 416-593-2318

Comments on Proposed Insurance Guidance:

Address and deliver your comments to:

Mr. Tony Toy, Policy Manager

Canadian Council of Insurance Regulators

National Regulatory Coordination Branch

25 Sheppard Avenue West, Suite 100

Toronto, Ontario

M2N 6S6

[email protected]

Your comments will be delivered to member jurisdictions of the CCIR.

Questions

If you have any questions, please contact the staff members listed below.

With respect to securities questions:

Gabriel Chénard

Jan Bagh

Senior Policy Analyst

Senior Legal Counsel

Supervision of Intermediaries

Alberta Securities Commission

Autorité des marchés financiers

Corporate Finance

(514) 395-0337, ext. 4482

(403) 355-2804

Toll-free: 1 800 525-0337, ext. 4482

Chad Conrad

Kathryn Anthistle

Senior Legal Counsel

Senior Legal Counsel, Legal Services

Alberta Securities Commission

Capital Markets Regulation Division

Corporate Finance

British Columbia Securities Commission

(403) 297-4295

(604) 899-6536

Curtis Brezinski

Clayton Mitchell

Compliance Auditor

Registration and Compliance Manager

Financial and Consumer Affairs Authority of Saskatchewan

Financial and Consumer Services Commission (New Brunswick)

(306) 787-5876

(506) 658-5476

Nick Doyle

Brian Murphy

Compliance Officer

Manager, Registration

Financial and Consumer Services Commission (New Brunswick)

Nova Scotia Securities Commission

(506) 635-2450

(902) 424-4592

Chris Jepson

Senior Legal Counsel

Ontario Securities Commission

(416) 593-2379

With respect to insurance questions:

Mr. Tony Toy, Policy Manager

Chantale Bégin CPA auditor, CA

Canadian Council of Insurance Regulators

Senior Accountant, Standardization of Financial Institutions

National Regulatory Coordination Branch

Capital Oversight of Financial Institutions

416-590-7257

Autorité des marchés financiers

Tel : 418 525-0337, ext 4595

Toll free : 1 877 525-0337, ext 4595

{1} Other continuous disclosure documents prepared by investment funds, such as annual statements or management reports of fund performance, are not prepared by all investment funds, present information in a form which may be complex for retail investors to understand and do not allow investors to understand their total costs of investing, as they present information which is specific to a single issuer or group of issuers.

{2} Behavioural Insights Team is a social purpose company part-owned by the U.K. Government.

{3} See OSC Staff Notice 11-787 Improving Fee Disclosure Through Behavioural Insights, August 19, 2019, p. 11.

{4} See item 1.3 of Part II of Form 81-101F3 in National instrument 81-101 Mutual Fund Prospectus Disclosure.

{5} See sections 14.14, 14.14.1 and 14.17 of NI 31-103.

{6} https://www.securities-administrators.ca/news/joint-forum-of-financial-market-regulators-engages-with-industry-and-investor-groups-on-investment-fee-transparency/

{7} The final prototype cost and compensation report developed for the securities sector will also be included as an appendix to 31-103CP.

ANNEX A

SPECIFIC QUESTIONS REGARDING THE PROPOSED SECURITIES AMENDMENTS

1. Do you anticipate implementation issues related to the inclusion of any of the following in the Proposed Securities Amendments,

(a) exchange-traded funds,

(b) prospectus-exempt investment funds,

(c) scholarship plans,

(d) labour-sponsored funds,

(e) foreign investment funds?

2. Would you consider it acceptable if, instead of information about each investment fund's fund expense ratio (MER + TER), the MER alone was disclosed in account statements and additional statements and used in the calculation of the fund expenses for the purposes of the annual report on charges and other compensation?

3. For the purpose of subsection 14.14.1(2), is the use of net asset value appropriate, or would it be more appropriate to use market value or another input? Would it be better to use different inputs for different types of funds?

4. Do you anticipate any other implementation issues related to the Proposed Securities Amendments?

5. Do you anticipate any issues specifically related to the proposed transition period?

ANNEX B

SPECIFIC QUESTIONS REGARDING THE PROPOSED INSURANCE GUIDANCE

This annex has been prepared by the Canadian Council of Insurance Regulators (CCIR). Please send comments relating to it to the CCIR National Regulatory Coordination Branch at the address indicated under "Comments on Proposed Insurance Guidance".

[Editor's Note: This annex is reproduced on the following separately numbered pages. Bulletin pagination resumes at the end of this annex.]

ANNEX B

SPECIFIC QUESTIONS REGARDING THE PROPOSED INSURANCE GUIDANCE

1. Do you anticipate implementation issues related to the inclusion of any of the following in the Proposed Insurance Guidance,

(a) Segregated Fund Contracts which are no longer available for sale, but to which customers can still make deposits;

(b) Segregated Fund Contracts which are no longer available for sale and to which customer can no longer make deposits;

(c) Segregated Fund Contracts that have the potential to have funds in more than one phase at one time (i.e. Accumulation Phase, Withdrawal Phase, Benefits Phase);

(d) Segregated Fund Contracts that may include insurance fees that are paid both directly (i.e. from money outside a segregated fund, such as where units are cashed out to pay the insurance fee) and indirectly (i.e. from assets held within a fund in which the client holds units)?

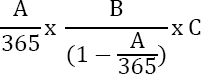

2. The Proposed Insurance Guidance does not yet include a method insurers must follow when calculating the fund expenses for each Segregated Fund Contract. Please comment on the advantages and disadvantages of calculating the fund expenses for each segregated fund the client holds each day as follows.

Option 1:

Option 2:

In each option

A = fund expense ratio of the applicable class or series of the segregated fund;

B = the net asset value of a unit of the applicable class or series of the segregated fund for the day; and

C = the number of units owned by the client for the day.

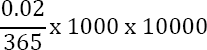

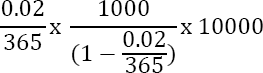

The difference between these two options is that Option 1 bases the allocation of fund expenses on the net value of assets in the fund after they are reduced to reflect the fund expenses for the day. Option 2 bases the allocation of fund expenses on the gross assets before they are reduced to reflect these expenses.

For example, suppose that A = 2%, B = $1,000 and C = 10,000.

Under Option 1, the fund expenses for the client for that segregated fund for the year would be $547.95:

Under Option 2, the fund expenses would be $547.98:

3. Should all insurers be required to use the same formula to calculate the dollar amount of fund expenses? Please comment on the advantages and disadvantages of:

a. Requiring all insurers to use the same calculation; or

b. Allowing an insurer to use a different calculation method if the insurer can create a more precise approximation.

4. For the purpose of the calculation described in question 2, what are the costs, benefits and risks of using the following to calculate fund expense ratio (i.e. MER + TER):

a. MER from the most recent Fund Facts document published before the year in question begins and a TER calculated at the same time on similar basis;

b. MER and TER calculated for the year in question after the year ends; or

c. Other estimated MER and TER for the year (please explain how this MER and TER would be calculated if you discuss this option)?

5. For the purpose of the calculation described in question 2, what are the costs, benefits and risks of using:

a. 365 days;

b. The actual number of days in the calendar year in question; or

c. Another number that reflects the number of days on which the NAV is calculated for the fund rather than the number of days in the year?

Note that the proposed calculation for securities assumes 365 days.

6. Would you consider it acceptable if, instead of information about each segregated fund's fund expense ratio (MER + TER), the MER alone was:

a. disclosed in annual statements for each fund; and

b. used in the calculation of the total fund expenses for the Segregated Fund Contract for the year?

What are the costs, benefits and risks of using (MER + TER) versus only using MER?

7. Might Segregated Fund Contract customers incur significant costs, other than for deferred sales charges, if they withdraw all funds from their Segregated Fund Contracts? If so, what are those costs?

8. The guidance describes annual statements. Do you anticipate any issues in connection with the guidance as drafted in cases where an insurer provides semi-annual statements to customers?

9. Do you anticipate any other implementation issues related to the Proposed Insurance Guidance?

10. Do you anticipate any issues specifically related to the proposed transition period?

ANNEX C

PROPOSED AMENDMENTS TO NATIONAL INSTRUMENT 31-103 REGISTRATION REQUIREMENTS, EXEMPTIONS AND ONGOING REGISTRANT OBLIGATIONS

1. National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations is amended by this Instrument.

2. Section 1.1 is amended by adding the following definitions:

"direct investment fund charge" means an amount charged, by an investment fund or an investment fund manager, to a client if the client buys, holds, sells or switches units or shares of an investment fund, including any federal, provincial or territorial sales taxes paid on that amount, other than, for greater certainty, an amount included in the investment fund's fund expenses;

"ETF facts document" has the same meaning as in section 1.1 of National Instrument 41-101 General Prospectus Requirements;

"fund expense ratio" means the sum of an investment fund's management expense ratio and trading expense ratio, expressed as a percentage;

"fund facts document" has the same meaning as in section 1.1 of National Instrument 81-101 Mutual Fund Prospectus Disclosure;

"management expense ratio" has the same meaning as in section 1.1 of National Instrument 81-106 Investment Fund Continuous Disclosure;

"management report of fund performance" has the same meaning as in section 1.1 of National Instrument 81-106 Investment Fund Continuous Disclosure;

"trading expense ratio" means the ratio, expressed as a percentage, of the total commissions and other portfolio transaction costs incurred by an investment fund to its average net asset value, calculated in accordance with paragraph 12 of item 3 Financial Highlights of Part B of Form 81-106F1 of National Instrument 81-106 Investment Fund Continuous Disclosure;"

3. Section 14.1.1 is replaced with the following:

"14.1.1. Duty to provide information -- investment fund managers

(1) A registered investment fund manager of an investment fund must, within a reasonable period of time, provide a registered dealer or a registered adviser that has a client that owns securities of the investment fund with the information that is required by the dealer or adviser, in order for the dealer or adviser to comply with paragraph 14.12(1)(c), subsections 14.14(4) and (5), 14.14.1(2) and 14.14.2(1) and paragraphs 14.17(1)(h) and (i) and (j), or with a reasonable approximation of such information.

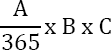

(2) For the purpose of subsection (1), with respect to the information required in respect of paragraph 14.17(1)(i), the registered investment fund manager must provide the daily cost per unit or share of the relevant class or series of an investment fund calculated in dollars, determined using the following formula:

A/365xB=C, where

A = fund expense ratio of the applicable class or series of the investment fund;

B = the net asset value of a share or unit of the applicable class or series of the investment fund for the day;

C = the daily dollar cost per unit for the investment fund class or series.

(3) For the purpose of subsection (1), and paragraph 14.14(5)(c.1) or 14.14.1(2)(c.1), if a registered investment fund manager provides an approximation, the approximation must be determined based on information disclosed in an investment fund's most recently disclosed fund facts document, ETF facts document, prospectus or management report of fund performance, making any reasonable assumptions, unless

(a) the information was disclosed more than 12 months before the end of the period covered by the statement or report which is required to be delivered by the registered dealer or registered adviser under subsection 14.14(1), 14.14.1(1) or 14.17(1), or

(b) the investment fund manager reasonably believes that doing so would cause the information disclosed in the statement or report to be misleading."

4. Subsection 5 of section 14.14 is amended by adding the following, after paragraph (c):

"(c.1) the fund expense ratio of each class or series of each investment fund in the account;

(c.2) if information reported under paragraph (c.1) is based on an approximation or any other assumption, a description of the assumption or approximation;"

5. Subsection 5 of section 14.14 is amended by adding the following, after paragraph (g):

"(h) if there are investment funds in the account, the following notification or a notification that is substantially similar:

"Fund expenses are made up of the management fee, operating expenses and trading costs. You don't pay these expenses directly. They are periodically deducted from the value of your investments by the companies that manage and operate those funds. Different funds have different fund expenses. They affect you because they reduce the fund's returns. These expenses add up over time. Fund expenses are expressed as an annual percentage of the total value of the fund. They correspond to the sum of the fund's management expense ratio (MER) and trading expense ratio (TER). These costs are already reflected in the current values reported for your fund investments.""

6. Subsection 2 of section 14.14.1 is amended by adding the following after paragraph (c):

"(c.1) the fund expense ratio of each class or series of each investment fund;

(c.2) if information reported under paragraph (c.1) is based on an approximation or any other assumption, a description of the assumption or approximation;"

7. Subsection 2 of section 14.14.1 is amended by adding the following after paragraph (h):

"(i) if the statement includes information under paragraph (c.1), the following notification or a notification that is substantially similar:

"Fund expenses are made up of the management fee, operating expenses and trading costs. You don't pay these expenses directly. They are periodically deducted from the value of your investments by the companies that manage and operate those funds. Different funds have different fund expenses. They affect you because they reduce the fund's returns. These expenses add up over time. Fund expenses are expressed as an annual percentage of the total value of the fund. They correspond to the sum of the fund's management expense ratio (MER) and trading expense ratio (TER). These costs are already reflected in the current values reported for your fund investments."

8. Subsection 1 of section 14.17 is amended by adding the following, after paragraph (h):

"(i) the total amount of fund expenses, in relation to securities of investment funds owned by the client during the period covered by the report, either:

(a) charged to the client by an investment fund, its investment fund manager or any other party, or;

(b) charged to an investment fund by its investment fund manager or any other party;

(j) the total amount of direct investment fund charges charged to the client by an investment fund, investment fund manager or any other party, in relation to securities of investment funds owned by the client during the period covered by the report, excluding any charges included in the amounts under paragraph (c) or (f);

(k) the total amount of the fund expenses reported under paragraph (i) and the direct investment fund charges reported under paragraph (j);

(l) the total amount of the registered firm's charges reported under paragraph (d) and the investment fund fees reported under paragraph (k);

(m) if the client owned investment fund securities during the period covered by the report, the following notification or a notification that is substantially similar:

"Fund expenses are made up of the management fee, operating expenses and trading costs. You don't pay these expenses directly. They are periodically deducted from the value of your investments by the companies that manage and operate those funds. Different funds have different fund expenses. They affect you because they reduce the fund's returns. These expenses add up over time. Fund expenses are expressed as an annual percentage of the total value of the fund. They correspond to the sum of the fund's management expense ratio (MER) and trading expense ratio (TER). These costs are already reflected in the current values reported for your fund investments.

The number shown here is the total dollar amount you paid in management fees, trading fees and operating expenses for all the investment funds you owned last year. This amount depends on each of your funds' fund expenses and the amount you invested in each fund. Your account statements show the fund expenses as a percentage for each fund you hold."

(n) if the client owned investment fund securities during the period covered by the report and any deferred sales charges were paid by the client, the following notification or a notification that is substantially similar:

"You paid this cost because you redeemed your units or shares of a fund purchased under a deferred sales charge option (DSC) before the end of the redemption fee schedule and a redemption fee was payable to the investment fund company. Information about these and other fees can be found in the prospectus or fund facts document for each investment fund. The redemption fee was deducted from the redemption amount you received."

(o) if the client owned investment fund securities during the period covered by the report and direct investment fund charges, other than redemption fees, were charged to the client, a short explanation of the type of fees which were charged;

(p) if the information reported under paragraph (i) or (j) is based on an approximation or any other assumption, a description of the assumption or approximation."

9. Section 14.17 of the Instrument is amended by adding the following subsection:

"(6) For the purposes of determining the total amount of fund expenses under paragraph (1)(i), the fund expenses for each class or series of each investment fund owned by the client during the reporting period must be added together after using the following formula to calculate the fund expenses for each fund for each day that the client owned it,

(A x B) where

A = the daily cost per unit or share of the relevant class or series of an investment fund calculated in dollars using the formula in subsection 14.1.1(2), and

B = the number of shares or units owned by the client for the day."

10. The Instrument is amended by adding the following section, after section 14.17:

"14.17.1 Reporting of fund expenses and direct investment fund charges

(1) Subject to subsection (2), for the purposes of paragraphs 14.14(5)(c.1), 14.14.1(2)(c.1), and 14.17(1)(i) and (j), the information required to be delivered to clients by a registered dealer or registered adviser must be based on the information provided under section 14.1.1.

(2) Subject to subsection (3), if no information is provided under section 14.1.1, or the registered firm reasonably believes that any part of the information provided pursuant to section 14.1.1 is incomplete or that relying on it would cause information required to be delivered to a client to be misleading, the registered firm must rely on the most recent information disclosed in the relevant fund facts document, ETF facts document, prospectus or management report of fund performance, as applicable;

(3) If there is no publicly available information or if the information referred to in subsection (2) was disclosed more than 12 months before the end of the period covered by the statement or report required to be delivered to the client, or the registered firm reasonably believes that relying on the publicly available information would cause information required to be delivered to the client to be misleading, the registered firm must not rely on the publicly available information and must

(a) make reasonable efforts to obtain the information referred to in subsection (1) by other means, and

(b) subject to subsection (4), rely on the information obtained under paragraph (a).

(4) If the registered firm reasonably believes it cannot obtain information under paragraph (3) that is not misleading, the registered firm must exclude the information from the calculation of the amount of fund expenses or of the direct investment fund charges reported to the client, as the case may be, or, in the case of a fund expense ratio, must not report the fund expense ratio, and must disclose the fact that the information is excluded or not reported in the relevant statement or report."

11. This Instrument comes into force on [•].

ANNEX D

PROPOSED CHANGES TO 31-103CP

NOT PUBLISHED IN ONTARIO -- SEE ANNEX F: BLACKLINE SHOWING

PROPOSED CHANGES TO COMPANION POLICY 31-103CP NATIONAL INSTRUMENT 31-103 REGISTRATION REQUIREMENTS, EXEMPTIONS AND ONGOING REGISTRANT OBLIGATIONS

ANNEX E

BLACKLINE SHOWING PROPOSED AMENDMENTS TO NATIONAL INSTRUMENT 31-103 REGISTRATION REQUIREMENTS, EXEMPTIONS AND ONGOING REGISTRANT OBLIGATIONS

1.1 Definitions of terms used throughout this Regulation

In this Instrument (...)

"direct investment fund charge" means an amount charged, by an investment fund or an investment fund manager, to a client if the client buys, holds, sells or switches units or shares of an investment fund, including any federal, provincial or territorial sales taxes paid on that amount, other than, for greater certainty, an amount included in the investment fund's fund expenses;

"ETF facts document" has the same meaning as in section 1.1 of National Instrument 41-101 General Prospectus Requirements;

"fund expense ratio" means the sum of an investment fund's management expense ratio and trading expense ratio, expressed as a percentage;

"fund facts document" has the same meaning as in section 1.1 of National Instrument 81-101 Mutual Fund Prospectus Disclosure;

"management expense ratio" has the same meaning as in section 1.1 of National Instrument 81-106 Investment Fund Continuous Disclosure;

"management report of fund performance" has the same meaning as in section 1.1 of National Instrument 81-106 Investment Fund Continuous Disclosure;

"trading expense ratio" means the ratio, expressed as a percentage, of the total commissions and other portfolio transaction costs incurred by an investment fund to its average net asset value, calculated in accordance with paragraph 12 of item 3 Financial Highlights of Part B of Form 81-106F1 of National Instrument 81-106 Investment Fund Continuous Disclosure;

(...)

14.1.1 Duty to provide information -- investment fund managers

(1) A registered investment fund manager of an investment fund must, within a reasonable period of time, provide a registered dealer or a registered adviser that has a client that owns securities of the investment fund with the information that is required by the dealer or adviser, in order for the dealer or adviser to comply with paragraph 14.12(1)(c), subsections 14.14(4) and (5), 14.14.1(2) and 14.14.2(1) and paragraphs 14.17(1)(h) and (i) and (j), or with a reasonable approximation of such information.

(2) For the purpose of subsection (1), with respect to the information required in respect of paragraph 14.17(1)(i), the registered investment fund manager must provide the daily cost per unit or share of the relevant class or series of an investment fund calculated in dollars, determined using the following formula:

A/365x B= C , where

A = fund expense ratio of the applicable class or series of the investment fund;

B = the net asset value of a share or unit of the applicable class or series of the investment fund for the day;

C = the daily dollar cost per unit for the investment fund class or series.

(3) For the purpose of subsection (1), and paragraph 14.14(5)(c.1) or 14.14.1(2)(c.1), if a registered investment fund manager provides an approximation, the approximation must be determined based on information disclosed in an investment fund's most recently disclosed fund facts document, ETF facts document, prospectus or management report of fund performance, making any reasonable assumptions, unless

(a) the information was disclosed more than 12 months before the end of the period covered by the statement or report which is required to be delivered by the registered dealer or registered adviser under subsection 14.14(1), 14.14.1(1) or 14.17(1), or

(b) the investment fund manager reasonably believes that doing so would cause the information disclosed in the statement or report to be misleading.

(...)

14.14. Account statements

(1) A registered dealer must deliver to a client a statement that includes the information referred to in subsections (4) and (5)

(a) at least once every 3 months, or

(b) if the client has requested to receive statements on a monthly basis, for each one-month period.

(2) A registered dealer must deliver to a client a statement that includes the information referred to in subsections (4) and (5) after the end of any month in which a transaction was effected in securities held by the dealer in the client's account, other than a transaction made under an automatic withdrawal plan or an automatic payment plan, including a dividend reinvestment plan.

(2.1) Paragraph 1(b) and subsection (2) do not apply to a mutual fund dealer in connection with its activities as a dealer in respect of the securities listed in paragraph 7.1(2)(b).

(3) A registered adviser must deliver to a client a statement that includes the information referred to in subsections (4) and (5) at least once every 3 months, except that if the client has requested to receive statements on a monthly basis, the adviser must deliver a statement to the client for each one-month period.

(3.1) (paragraph revoked).

(4) If a registered dealer or registered adviser made a transaction for a client during the period covered by a statement delivered under subsection (1), (2) or (3), the statement must include the following:

(a) the date of the transaction;

(b) whether the transaction was a purchase, sale or transfer;

(c) the name of the security;

(d) the number of securities purchased, sold or transferred;

(e) the price per security if the transaction was a purchase or sale;

(f) the total value of the transaction if it was a purchase or sale.

(5) If a registered dealer or registered adviser holds securities owned by a client in an account of the client, a statement delivered under subsection (1), (2) or (3) must indicate that the securities are held for the client by the registered firm and must include the following information about the client's account determined as at the end of the period for which the statement is made:

(a) the name and quantity of each security in the account;

(b) the market value of each security in the account and, if applicable, the notification in subsection 14.11.1(2);

(c) the total market value of each security position in the account;

(c.1) the fund expense ratio of each class or series of each investment fund in the account;

(c.2) if information reported under paragraph (c.1) is based on an approximation or any other assumption, a description of the assumption or approximation;

(d) any cash balance in the account;

(e) the total market value of all cash and securities in the account;

(f) whether the account is eligible for coverage under an investor protection fund approved or recognized by the securities regulatory authority and, if it is, the name of the investor protection fund;

(g) which securities in the account might be subject to a deferred sales charge if they are sold;

(h) if there are investment funds in the account, the following notification or a notification that is substantially similar:

"Fund expenses are made up of the management fee, operating expenses and trading costs. You don't pay these expenses directly. They are periodically deducted from the value of your investments by the companies that manage and operate those funds. Different funds have different fund expenses. They affect you because they reduce the fund's returns. These expenses add up over time. Fund expenses are expressed as an annual percentage of the total value of the fund. They correspond to the sum of the fund's management expense ratio (MER) and trading expense ratio (TER). These costs are already reflected in the current values reported for your fund investments.";

(6) (paragraph revoked).

(7) For the purposes of this section, a security is considered to be held by a registered firm for a client if

(a) the firm is the registered owner of the security as nominee on behalf of the client, or

(b) the firm has physical possession of a certificate evidencing ownership of the security.

14.14.1. Additional statements

(1) A registered dealer or registered adviser must deliver a statement that includes the information referred to in subsection (2) to a client if any of the following apply in respect of a security owned by the client that is held or controlled by a party other than the dealer or adviser:

(a) the dealer or adviser has trading authority over the security or the client's account in which the security is held or was transacted;

(b) the dealer or adviser receives continuing payments related to the client's ownership of the security from the issuer of the security, the investment fund manager of the issuer or any other party;

(c) the security is issued by a scholarship plan, a mutual fund or an investment fund that is a labour-sponsored investment fund corporation, or labour-sponsored venture capital corporation, under legislation of a jurisdiction of Canada and the dealer or adviser is the dealer or adviser of record for the client on the records of the issuer of the security or the records of the issuer's investment fund manager.

(2) A statement delivered under subsection (1) must include the following in respect of the securities or the account referred to in subsection (1), determined as at the end of the period for which the statement is made:

(a) the name and quantity of each security;

(b) the market value of each security and, if applicable, the notification in subsection 14.11.1(2);

(c) the total market value of each security position;

(c.1) the fund expense ratio of each class or series of each investment fund;

(c.2) if information reported under paragraph (c.1) is based on an approximation or any other assumption, a description of the assumption or approximation;

(d) any cash balance in the account;

(e) the total market value of all of the cash and securities;

(f) disclosure in respect of the party that holds or controls each security and a description of the way it is held;

(g) whether the securities are, or the account is, eligible for coverage under an investor protection fund approved or recognized by the securities regulatory authority;

(h) which of the securities might be subject to a deferred sales charge if they are sold;

(i) if the statement includes information under paragraph (c.1), the following notification or a notification that is substantially similar:

"Fund expenses are made up of the management fee, operating expenses and trading costs. You don't pay these expenses directly. They are periodically deducted from the value of your investments by the companies that manage and operate those funds. Different funds have different fund expenses. They affect you because they reduce the fund's returns. These expenses add up over time. Fund expenses are expressed as an annual percentage of the total value of the fund. They correspond to the sum of the fund's management expense ratio (MER) and trading expense ratio (TER). These costs are already reflected in the current values reported for your fund investments."

(...)

14.17. Report on charges and other compensation

(1) For each 12-month period, a registered firm must deliver to a client a report on charges and other compensation containing the following information, except that the first report delivered after a client has opened an account may cover a period of less than 12 months:

(a) the registered firm's current operating charges which might be applicable to the client's account;

(b) the total amount of each type of operating charge related to the client's account paid by the client during the period covered by the report, and the total amount of those charges;

(c) the total amount of each type of transaction charge related to the purchase or sale of securities paid by the client during the period covered by the report, and the total amount of those charges;

(d) the total amount of the operating charges reported under paragraph (b) and the transaction charges reported under paragraph (c);

(e) if the registered firm purchased or sold debt securities for the client during the period covered by the report, either of the following:

(i) the total amount of any mark-ups, mark-downs, commissions or other service charges the firm applied on the purchases or sales of debt securities;

(ii) the total amount of any commissions charged to the client by the firm on the purchases or sales of debt securities and, if the firm applied mark-ups, mark-downs or any service charges other than commissions on the purchases or sales of debt securities, the following notification or a notification that is substantially similar:

"For debt securities purchased or sold for you during the period covered by this report, dealer firm remuneration was added to the price you paid (in the case of a purchase) or deducted from the price you received (in the case of a sale). This amount was in addition to any commissions you were charged.";

(f) if the registered firm is a scholarship plan dealer, the unpaid amount of any enrolment fee or other charge that is payable by the client;

(g) the total amount of each type of payment, other than a trailing commission, that is made to the registered firm or any of its registered individuals by a securities issuer or another registrant in relation to registerable services to the client during the period covered by the report, accompanied by an explanation of each type of payment;

(h) if the registered firm received trailing commissions related to securities owned by the client during the period covered by the report, the following notification or a notification that is substantially similar:

"We received $[amount] in trailing commissions in respect of securities you owned during the 12-month period covered by this report.

Investment funds pay investment fund managers a fee for managing their funds. The managers pay us ongoing trailing commissions for the services and advice we provide you. The amount of the trailing commission depends on the sales charge option you chose when you purchased the fund. You are not directly charged the trailing commission or the management fee. But, these fees affect you because they reduce the amount of the fund's return to you. Information about management fees and other charges to your investment funds is included in the prospectus, fund facts document or ETF Facts document for each fund.";

(i) the total amount of fund expenses, in relation to securities of investment funds owned by the client during the period covered by the report, either:

(a) charged to the client by an investment fund, its investment fund manager or any other party, or;

(b) charged to an investment fund by its investment fund manager or any other party;

(j) the total amount of direct investment fund charges charged to the client by an investment fund, investment fund manager or any other party, in relation to securities of investment funds owned by the client during the period covered by the report, excluding any charges included in the amounts under paragraph (c) or (f);

(k) the total amount of the fund expenses reported under paragraph (i) and the direct investment fund charges reported under paragraph (j);

(l) the total amount of the registered firm's charges reported under paragraph (d) and the investment fund fees reported under paragraph (k);

(m) if the client owned investment fund securities during the period covered by the report, the following notification or a notification that is substantially similar:

"Fund expenses are made up of the management fee, operating expenses and trading costs. You don't pay these expenses directly. They are periodically deducted from the value of your investments by the companies that manage and operate those funds. Different funds have different fund expenses. They affect you because they reduce the fund's returns. These expenses add up over time. Fund expenses are expressed as an annual percentage of the total value of the fund. They correspond to the sum of the fund's management expense ratio (MER) and trading expense ratio (TER). These costs are already reflected in the current values reported for your fund investments.

The number shown here is the total dollar amount you paid in management fees, trading fees and operating expenses for all the investment funds you owned last year. This amount depends on each of your funds' fund expenses and the amount you invested in each fund. Your account statements show the fund expenses as a percentage for each fund you hold."

(n) if the client owned investment fund securities during the period covered by the report and any deferred sales charges were paid by the client, the following notification or a notification that is substantially similar:

"You paid this cost because you redeemed your units or shares of a fund purchased under a deferred sales charge option (DSC) before the end of the redemption fee schedule and a redemption fee was payable to the investment fund company. Information about these and other fees can be found in the prospectus or fund facts document for each investment fund. The redemption fee was deducted from the redemption amount you received."

(o) if the client owned investment fund securities during the period covered by the report and direct investment fund charges, other than redemption fees, were charged to the client, a short explanation of the type of fees which were charged;

(p) if the information reported under paragraph (i) or (j) is based on an approximation or any other assumption, a description of the assumption or approximation.

(2) For the purposes of this section, the information in respect of securities of a client required to be reported under subsection 14.14(5) must be delivered in a separate report on charges and other compensation for each of the client's accounts.

(3) For the purposes of this section, the information in respect of securities of a client required to be reported under subsection 14.14.1(1) must be delivered in a report on charges and other compensation for the client's account through which the securities were transacted.

(4) Subsections (2) and (3) do not apply if the registered firm provides a report on charges and other compensation that consolidates, into a single report, the required information for more than one of a client's accounts and any securities of the client required to be reported under subsection 14.14(5) or 14.14.1(1) and if the following apply

(a) the client has consented in writing to the form of disclosure referred to in this subsection;

(b) the consolidated report specifies the accounts and securities with respect to which information is required to be reported under subsection 14.14.1(1).

(5) This section does not apply to a registered firm in respect of a permitted client that is not an individual.

(6) For the purposes of determining the total amount of fund expenses under paragraph (1)(i), the fund expenses for each class or series of each investment fund owned by the client during the reporting period must be added together after using the following formula to calculate the fund expenses for each fund for each day that the client owned it,

(A x B)

where

A = the daily cost per unit or share of the relevant class or series of an investment fund calculated in dollars using the formula in subsection 14.1.1(2), and

B = the number of shares or units owned by the client for the day.

14.17.1 Reporting of fund expenses and direct investment fund charges

(1) Subject to subsection (2), for the purposes of paragraphs 14.14(5)(c.1), 14.14.1(2)(c.1), and 14.17(1)(i) and (j), the information required to be delivered to clients by a registered dealer or registered adviser must be based on the information provided under section 14.1.1.

(2) Subject to subsection (3), if no information is provided under section 14.1.1, or the registered firm reasonably believes that any part of the information provided pursuant to section 14.1.1 is incomplete or that relying on it would cause information required to be delivered to a client to be misleading, the registered firm must rely on the most recent information disclosed in the relevant fund facts document, ETF facts document, prospectus or management report of fund performance, as applicable;

(3) If there is no publicly available information or if the information referred to in subsection (2) was disclosed more than 12 months before the end of the period covered by the statement or report required to be delivered to the client, or the registered firm reasonably believes that relying on the publicly available information would cause information required to be delivered to the client to be misleading, the registered firm must not rely on the publicly available information and must

(a) make reasonable efforts to obtain the information referred to in subsection (1) by other means, and

(b) subject to subsection (4), rely on the information obtained under paragraph (a).

(4) If the registered firm reasonably believes it cannot obtain information under paragraph (3) that is not misleading, the registered firm must exclude the information, from the calculation of the amount of fund expenses or of the direct investment fund charges reported to the client, as the case may be, or, in the case of a fund expense ratio, must not report the fund expense ratio, and must disclose the fact that the information is excluded or not reported in the relevant statement or report.

ANNEX F

BLACKLINE SHOWING PROPOSED CHANGES TO COMPANION POLICY 31-103CP NATIONAL INSTRUMENT 31-103 REGISTRATION REQUIREMENTS, EXEMPTIONS AND ONGOING REGISTRANT OBLIGATIONS

Division 1 Investment fund managers

Section 14.1 sets out the limited application of Part 14 to investment fund managers. The sections of Part 14 that apply to investment fund managers when performing their investment fund manager activities include section 14.1.1, section 14.5.2, section 14.5.3, section 14.6, section 14.6.1, section 14.6.2, subsection 14.12(5) and section 14.15. An investment fund manager that is also registered as a dealer or adviser (or both) is subject to all relevant sections of Part 14 in respect of that firm's dealer or adviser activities.

Section 14.1.1 requires investment fund managers to provide information that is known to them or which is required to be calculated by them concerning position cost, fund expense ratio, fund expenses, deferred sales charges and any other charges deducted from the net asset value of the securities, and trailing commissions to dealers and advisers who have clients that own the investment fund manager's funds. This information must be provided within a reasonable period of time, in order that the dealers and advisers may comply with their client reporting obligations. This is a principles-based requirement.

When relying on information disclosed in an investment fund's previous disclosure documents, we would expect investment fund managers to inform the advisers or dealers of any assumptions or approximations in the information reported to the advisers or dealers.

An investment fund manager must work with the dealers and advisers who distribute fund products to determine what information they need from the investment fund manager in order to satisfy their client reporting obligations. The information and arrangements for its delivery may vary, reflecting different operating models and information systems. The information and arrangements for its delivery may vary, reflecting different operating models and information systems.

(...)

14.14. Account statements

Section 14.14 requires registered dealers and advisers to deliver statements to clients at least once every 3 months. There is no prescribed form for these statements but they must contain the information referred to in subsections 14.14(4) and (5). The types of transactions that must be disclosed in an account statement include any purchase, sale or transfer of securities, dividend or interest payment received or reinvested, any fee or charge, and any other account activity. The fund expense ratio of each series of each investment fund in the account and a description of any assumptions or approximations used to calculate this ratio must also be disclosed. A firm must deliver an account statement with the information referred to in subsection (4) if any transaction was made for the client in the reporting period. A firm is only required to provide the account position information referred to in subsection (5) if it holds securities owned by a client in an account of the client.

There is no provision for consolidated statements in section 14.14 (or 14.14.1), so a registered firm must provide every client with an applicable statement for each of their accounts. Firms may provide supplementary reporting that they think a client might find useful. For example, a firm might provide a consolidated year-end statement where a client has requested a consolidated performance report under subsection 14.18(4).

14.14.1. Additional statements

A firm is required to deliver additional statements if the circumstances described in subsection 14.14.1(1) apply. The additional statements must be delivered once every 3 months, except that an adviser must deliver the statements on a monthly basis if requested by the client as provided in subsection 14.14.1(3). The requirements set out for the frequency of delivering account statements and additional statements are minimum standards. Firms may choose to provide the statements more frequently.

Paragraph 14.14.1(2)(g) requires disclosure about applicable investor protection funds. However, subsection 14.14.1(2.1) exempts a firm from this requirement where a client's securities are held or controlled by an IIROC or MFDA member. SRO rules require members to be participants in specified investor protection funds and prescribe client disclosures about them. To avoid the potential that clients may be confused or misinformed, registrants that are not participants in an investor protection fund should refrain from discussing its terms and conditions with clients.

Firms may choose to include securities that must be reported under the additional statement requirement in a document that it refers to as an account statement, consistent with their clients' expectations that their accounts are not limited to securities held by the firm, provided it satisfies the requirements for content of statements set out in sections 14.14 and 14.14.1.

(...)

14.17. Report on charges and other compensation

Registered firms must provide clients with an annual report on the firm's charges and other compensation received by the firm in connection with their investments. Examples of operating charges and transaction charges are provided in the discussion of the disclosure of charges and other compensation in section 14.2 of this Policy Statement. The annual report must include information about all of the firm's current operating charges that might be applicable to a client's account. A firm is only required to include the charges for those of its services that it would reasonably expect the particular client to utilize in the coming 12 months.

The discussion of debt security disclosure requirements in section 14.12 of this Policy Statement is also relevant with respect to paragraph 14.17(1)(e).

Scholarship plans often have enrolment fees payable in instalments in the first few years of a client's investment in the plan. Paragraph 14.17(1)(f) requires that scholarship plan dealers include a reminder of the unpaid amount of any such fees in their annual reports on charges and other compensation.

Payments that a registered firm or its registered representatives receive from issuers of securities or other registrants in relation to registerable services to a client must be reported under paragraph 14.17(1)(g). This disclosure requirement includes any form of payment to the firm or a representative of the firm linked to sales or other registerable services to the client receiving the report. Examples of payments that would be included in this part of the report on charges and other compensation include some referral fees, success fees on the completion of a transaction, or finder's fees. This part of the report does not include trailing commissions, as they are specifically addressed in paragraph 14.17(1)(h).

Registered firms must disclose the amount of trailing commissions they received related to a client's holdings. The disclosure of trailing commissions received in respect of a client's investments must be included with a notification prescribed in paragraph 14.17(1)(h). The notification must be in substantially the form prescribed, so a registered firm may modify it to be consistent with the actual arrangements. For example, a firm that receives a payment that falls within the definition of "trailing commission" in section 1.1 in respect of securities that are not investment funds can modify the notification accordingly. The notification set out is the required minimum and firms can provide further explanation if they believe it will be helpful to their clients.

Registered firms should not include in the total amount of direct investment fund charges required to be reported under paragraph 14.17(1)(j), the amount of a charge, including a sales commission, which is required to be reported by the registered firm to the client under paragraph 14.17(1)(c), concerning transaction charges, or (f), specific to scholarship plan dealers, in order to avoid any potential double counting of such charge in the total cost amount required to be reported under paragraph 14.17(1)(l).

Registered firms may want to organize the annual report on charges and other compensation with separate sections showing the charges paid by the client to the firm, and the other compensation received by the firm in respect of the client's account.

Appendix D of this Policy Statement includes a sample Report on Charges and Other Compensation, which registered firms are encouraged to use as guidance.

14.17.1 Reporting of fund expenses and direct investment fund charges

Dealers and advisers are required to rely on information provided by registered investment fund managers pursuant to section 14.1.1. However, they may be unable to rely on such information in certain circumstances, including if:

• there is no registered investment fund manager

• such information is not required to be provided for a fund (for example, as in the case of certain non-Canadian investment funds)

• an investment fund manager does not comply with section 14.1.1 for any reason, or

• the dealer or adviser reasonably believes that relying on this information would cause the information delivered to a client to be misleading.

In cases where paragraph 14.17.1(3)(a) applies, the registered firm must make reasonable efforts to obtain information about the investment fund's fund expenses, fund expense ratio or direct investment fund charges by other means. Those other means may include:

• relying on information disclosed in disclosure documents of the investment fund other than those referred to in paragraph 14.17.1(2), including documents prepared according to the reporting requirements applicable in a foreign jurisdiction

• requesting that the information be provided in writing by the investment fund or investment fund manager, or

• relying on information reported by a reliable third-party service provider.

We expect registered firms to use their professional judgement in determining what other means of obtaining the information would be appropriate, notably taking into account that doing so must not cause the information reported to clients to be misleading.

(...)

Appendix D Annual Charges and Compensation Report is replaced by [TCR sample account statement and cost report]

ANNEX G

SAMPLE PROTOTYPE STATEMENT AND REPORT FOR THE SECURITIES SECTOR

Highlighting shows new information

Dealer ABC Inc.

Your Account Number: 123-4567

Holdings in your account

On December 31, 2020

Portfolio Assets

|

Description |

Shares Owned |

Book Cost |

Market Value |

Current gain or loss |

Fund Expenses{1} |

% of your holdings |

|

|

||||||

|

Investment Funds |

|

|

|

|

|

|

|

|

||||||

|

ABC Management Monthly Income Fund, Series A FE |

250.00 |

$17,000.00 |

$19,500.00 |

$2,500.00 |

1.00% |

41.49% |

|

|

||||||

|

ABC Management Canadian Equity, Series A FE |

450.00 |

$19,500.00 |

$22,500.00 |

$3,000.00 |

2.00% |

47.87% |

|

|

||||||

|

Equities |

|

|

|

|

|

|

|

|

||||||

|

Company A N/A |

100.00 |

$2,000.00 |

$3,000.00 |

$1,000.00 |

|

6.88% |

|

|

||||||

|

Company B N/A |

50.00 |

$1,500.00 |

$2,000.00 |

$500.00 |

|

4.26% |

|

|

||||||

|

Totals |

|

$40,000.00 |

$47,000.00 |

|

|

100.00% |

{1} Fund expenses are made up of the management fee, operating expenses and trading costs. You don't pay these expenses directly. They are periodically deducted from the value of your investments by the companies that manage and operate those funds. Different funds have different fund expenses. They affect you because they reduce the fund's returns. These expenses add up over time. Fund expenses are expressed as an annual percentage of the total value of the fund. They correspond to the sum of the fund's management expense ratio (MER) and trading expense ratio (TER). These costs are already reflected in the current values reported for your fund investments.

Dealer ABC Inc.

Your Account Number: 123-4567

Your Cost of Investing and Our Compensation

This report shows for 2021

• your cost of investing, including what you paid to us and to investment fund companies

• our compensation

Your Cost of Investing

Costs reduce your profits and increase your losses

Your total cost of investing was $815 last year

What you paid

|

Our charges: Amounts that you paid to us by withdrawals from your account or by other means such as cheques or transfers from your bank. |

|

|

|

|

|

Account administration and operating fees -- you pay these fees to us each year |

$100.00 |

|

|

|

|

Trading fees -- you pay these fees to us when you buy or sell some investments |

$20.00 |

|

|

|

|

Total you paid to us |

$120.00 |

|

|

|

|

Investment fund company fees: Amounts you paid to investment fund companies that operate the investment funds (e.g., mutual funds) in your account. |

|

|

|

|

|

Fund Expenses -- See the fund expenses % shown in the holdings section of your account statement{1} |

$645.00 |

|

|

|

|

Redemption fees on deferred sales charge (DSC) investments{2} $50.00 |

|

|

|

|

|

Amount you paid to investment fund companies |

$695.00 |

|

|

|

|

Your total cost of investing |

$815.00 |

{1} Fund expenses. Fund expenses are made up of the management fee, operating expenses and trading costs. You don't pay these expenses directly. They are periodically deducted from the value of your investments by the companies that manage and operate those funds. Different funds have different fund expenses. They affect you because they reduce the fund's returns. These expenses add up over time. Fund expenses are expressed as an annual percentage of the total value of the fund. They correspond to the sum of the fund's management expense ratio (MER) and trading expense ratio (TER). These costs are already reflected in the current values reported for your fund investments.