Amendments to NI 45-106 Prospectus Exemptions

Amendments to NI 45-106 Prospectus Exemptions

AMENDMENTS TO

NATIONAL INSTRUMENT 45-106 PROSPECTUS EXEMPTIONS

1. National Instrument 45-106 Prospectus Exemptions is amended by this Instrument.

2. Section 1.1 is amended

(a) in paragraph (b) of the definition of "eligibility adviser" by deleting "Saskatchewan or",

(b) in paragraph (h) of the definition of "eligible investor" by adding "in Manitoba, Northwest Territories, Nunavut, Prince Edward Island and Yukon," before "a person that has obtained advice".

3. The Instrument is amended by adding the following section:

1.1.1 In this Instrument, in Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan

"date of transition to IFRS" has the same meaning as in National Instrument 51-102 Continuous Disclosure Obligations;

"exempt market dealer" has the same meaning as in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

"first IFRS financial statements" has the same meaning as in National Instrument 51-102 Continuous Disclosure Obligations;

"investment dealer" has the same meaning as in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

"new financial year" means the financial year of an issuer that immediately follows a transition year;

"old financial year" means the financial year of an issuer that immediately precedes a transition year;

"OM marketing materials" means a written communication, other than an OM standard term sheet, intended for prospective purchasers regarding a distribution of securities under an offering memorandum delivered under section 2.9 [Offering memorandum] that contains material facts relating to an issuer, securities or an offering;

"OM standard term sheet" means a written communication intended for prospective purchasers regarding a distribution of securities under an offering memorandum delivered under section 2.9 [Offering memorandum] that

(a) is dated,

(b) includes the following legend, or words to the same effect, on the first page:

"This document does not provide disclosure of all information required for an investor to make an informed investment decision. Investors should read the offering memorandum, especially the risk factors relating to the securities offered, before making an investment decision.",

(c) contains only the following information in respect of the issuer, the securities or the offering:

(i) the name of the issuer;

(ii) the jurisdiction or foreign jurisdiction in which the issuer's head office is located;

(iii) the statute under which the issuer is incorporated, continued or organized or, if the issuer is an unincorporated entity, the laws of the jurisdiction or foreign jurisdiction under which it is established and exists;

(iv) a brief description of the business of the issuer;

(v) a brief description of the securities;

(vi) the price or price range of the securities;

(vii) the total number or dollar amount of the securities, or range of the total number or dollar amount of the securities;

(viii) the names of any agent, finder or other intermediary, whether registered or not, involved with the offering and the amount of any commission, fee or discount payable to them;

(ix) the proposed or expected closing date of the offering;

(x) a brief description of the use of proceeds;

(xi) the exchange on which the securities are proposed to be listed, if any, provided that the OM standard term sheet complies with the requirements of securities legislation for listing representations;

(xii) in the case of debt securities, the maturity date of the debt securities and a brief description of any interest payable on the debt securities;

(xiii) in the case of preferred shares, a brief description of any dividends payable on the securities;

(xiv) in the case of convertible securities, a brief description of the underlying securities into which the convertible securities are convertible;

(xv) in the case of exchangeable securities, a brief description of the underlying securities into which the exchangeable securities are exchangeable;

(xvi) in the case of restricted securities, a brief description of the restriction;

(xvii) in the case of securities for which a credit supporter has provided a guarantee or alternative credit support, a brief description of the credit supporter and the guarantee or alternative credit support provided;

(xviii) whether the securities are redeemable or retractable;

(xix) a statement that the securities are eligible, or are expected to be eligible, for investment in registered retirement savings plans, tax-free savings accounts or other registered plans, if the issuer has received, or reasonably expects to receive, a legal opinion that the securities are so eligible;

(xx) contact information for the issuer or any registrant involved, and

(d) for the purposes of paragraph (c), "brief description" means a description consisting of no more than three lines of text in type that is at least as large as that used generally in the body of the OM standard term sheet;

"portfolio manager" has the same meaning as in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

"SEC issuer" has the same meaning as in National Instrument 51-102 Continuous Disclosure Obligations;

"specified derivative" has the same meaning as in National Instrument 44-102 Shelf Distributions;

"structured finance product" has the same meaning as in National Instrument 25-101 Designated Rating Organizations;

"transition year" means the financial year of an issuer in which the issuer has changed its financial year end;

"U.S. laws" has the same meaning as in National Instrument 51-102 Continuous Disclosure Obligations..

4. Section 2.9 is amended

(a) in subsection (1) by deleting ", New Brunswick, Nova Scotia",

(b) in subsection (2) by replacing "In Alberta, Manitoba, Northwest Territories, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon" with "In Manitoba, Northwest Territories, Nunavut, Prince Edward Island and Yukon",

(c) by adding the following subsections:

(2.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, the prospectus requirement does not apply to a distribution by an issuer of a security of its own issue to a purchaser if

(a) the purchaser purchases the security as principal,

(b) the acquisition cost of all securities acquired by a purchaser who is an individual under this section in the preceding 12 months does not exceed the following amounts:

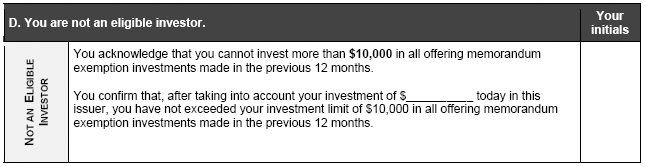

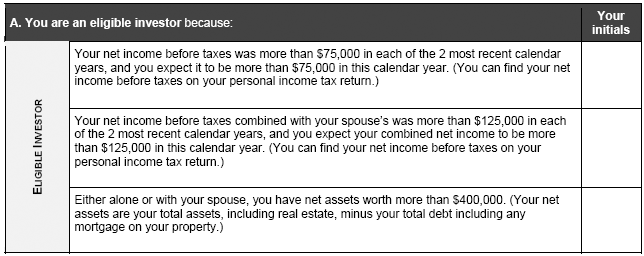

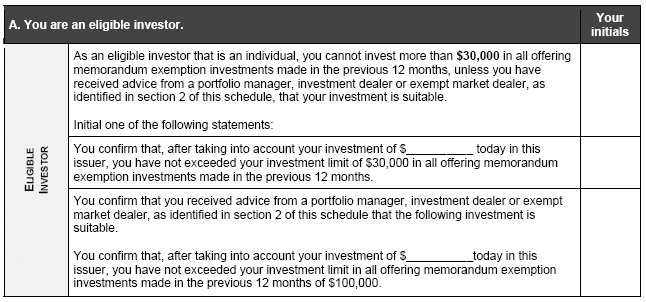

(i) in the case of a purchaser that is not an eligible investor, $10 000;

(ii) in the case of a purchaser that is an eligible investor, $30 000;

(iii) in the case of a purchaser that is an eligible investor and that received advice from a portfolio manager, investment dealer or exempt market dealer that the investment is suitable, $100 000,

(c) at the same time or before the purchaser signs the agreement to purchase the security, the issuer

(i) delivers an offering memorandum to the purchaser in compliance with subsections (5) to (13), and

(ii) obtains a signed risk acknowledgement from the purchaser in compliance with subsection (15), and

(d) the security distributed by the issuer is not either of the following:

(i) a specified derivative;

(ii) a structured finance product.

(2.2) The prospectus exemption described in subsection (2.1) is not available

(a) in Alberta, Nova Scotia and Saskatchewan, to an issuer that is an investment fund, unless the issuer is a non-redeemable investment fund or a mutual fund that is a reporting issuer, or

(b) in New Brunswick, Ontario and Québec, to an issuer that is an investment fund.

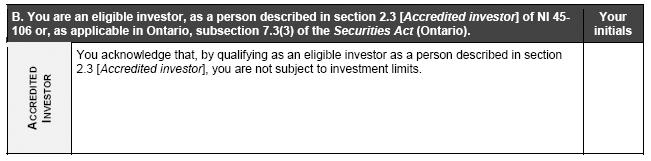

(2.3) The investment limits described in subparagraphs (2.1)(b)(ii) and (iii) do not apply if the purchaser is

(a) an accredited investor, or

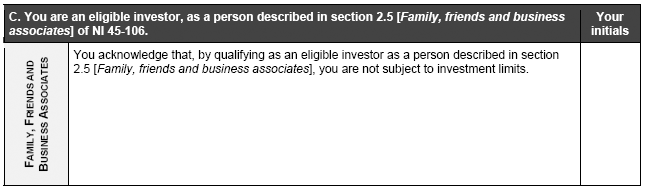

(b) a person described in subsection 2.5(1) [Family, friends and business associates].,

(d) in subsection (3) by replacing "In Alberta, Manitoba, Northwest Territories, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon" with "In Manitoba, Northwest Territories, Nunavut, Prince Edward Island and Yukon",

(e) by adding the following subsection:

(3.0.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, this section does not apply to a distribution of a security to a person that was created, or is used, solely to purchase or hold securities in reliance on the exemption from the prospectus requirement set out in subsection (2.1).,

(f) in subsection (3.1) by replacing "Subsections (1) and (2)", with "Subsections (1), (2) and (2.1)",

(g) in subsection (4) by deleting ", Saskatchewan",

(h) by adding the following subsections:

(5.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, an offering memorandum delivered under subsection (2.1)

(a) must incorporate by reference, by way of a statement in the offering memorandum, OM marketing materials related to each distribution under the offering memorandum and delivered or made reasonably available to a prospective purchaser before the termination of the distribution, and

(b) is deemed to incorporate by reference OM marketing materials related to each distribution under the offering memorandum and delivered or made reasonably available to a prospective purchaser before the termination of the distribution.

(5.2) A portfolio manager, investment dealer or exempt market dealer must not distribute OM marketing materials unless the OM marketing materials have been approved in writing by the issuer.,

(i) in subsections (15) and (16) by replacing "(1) or (2)" with "(1), (2) or (2.1)" wherever the phrase appears, and

(j) by adding the following subsections:

(17.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, the issuer must file with the securities regulatory authority a copy of all OM marketing materials required or deemed to be incorporated by reference into an offering memorandum delivered under this section,

(a) if the OM marketing materials are prepared on or before the filing of the offering memorandum, concurrently with the filing of the offering memorandum, or

(b) if the OM marketing materials are prepared after the filing of the offering memorandum, within 10 days of the OM marketing materials being delivered or made reasonably available to a prospective purchaser.

(17.2) OM marketing materials filed under subsection (17.1) must include a cover page clearly identifying the offering memorandum to which they relate.

(17.3) Subsections (17.4) to (17.21) apply to issuers that rely on subsection (2.1) and that are not reporting issuers in any jurisdiction of Canada.

(17.4) In Alberta, an issuer must, within 120 days after the end of each of its financial years, file with the securities regulatory authority annual financial statements and make them reasonably available to each holder of a security acquired under subsection (2.1).

(17.5) In New Brunswick, Ontario, Québec and Saskatchewan, an issuer must, within 120 days after the end of each of its financial years, deliver annual financial statements to the securities regulatory authority and make them reasonably available to each holder of a security acquired under subsection (2.1).

(17.6) In Nova Scotia, an issuer must, within 120 days after the end of each of its financial years, make reasonably available annual financial statements to each holder of a security acquired under subsection (2.1).

(17.7) Despite subsections (17.4), (17.5) and (17.6), as applicable, if an issuer is required to file, deliver or make reasonably available annual financial statements for a financial year that ended before the issuer distributed securities under subsection (2.1) for the first time, those annual financial statements must be filed in Alberta, delivered in New Brunswick, Ontario, Québec and Saskatchewan or made reasonably available in Nova Scotia, as applicable, on or before the later of

(a) the 60th day after the issuer first distributes securities under subsection (2.1), and

(b) the deadline in subsection (17.4), (17.5) or (17.6), as applicable, to file, deliver or make reasonably available the annual financial statements.

(17.8) The annual financial statements of an issuer referred to in subsections (17.4), (17.5) and (17.6) must include

(a) a statement of comprehensive income, a statement of changes in equity, and a statement of cash flows for

(i) the most recently completed financial year, and

(ii) the financial year immediately preceding the most recently completed financial year, if any,

(b) a statement of financial position as at the end of each of the periods referred to in paragraph (a),

(c) in the following circumstances, a statement of financial position as at the beginning of the financial year immediately preceding the most recently completed financial year:

(i) the issuer discloses in its annual financial statements an unreserved statement of compliance with IFRS, and

(ii) the issuer

(A) applies an accounting policy retrospectively in its annual financial statements,

(B) makes a retrospective restatement of items in its annual financial statements, or

(C) reclassifies items in its annual financial statements,

(d) in the case of the issuer's first IFRS financial statements, the opening IFRS statement of financial position at the date of transition to IFRS, and

(e) notes to the annual financial statements.

(17.9) If the annual financial statements referred to in subsection (17.8) present the components of profit or loss in a separate income statement, the separate income statement must be displayed immediately before the statement of comprehensive income referred to in subsection (17.8).

(17.10) The annual financial statements referred to in subsection (17.8) must be audited.

(17.11) Despite subsection (17.10), for the first annual financial statements of an issuer referred to in subsections (17.4), (17.5) and (17.6), comparative information relating to the preceding financial year is not required to be audited if it has not been previously audited.

(17.12) Any period referred to in subsection (17.8) that has not been audited must be clearly labelled as unaudited.

(17.13) In Alberta, New Brunswick, Ontario, Québec and Saskatchewan, if an issuer decides to change its financial year end by more than 14 days, it must deliver to the securities regulatory authority and make reasonably available to each holder of a security acquired under subsection (2.1) a notice containing the information set out in subsection (17.15) as soon as practicable and, in any event, no later than the earlier of

(a) the deadline, based on the issuer's old financial year end, for the next annual financial statements referred to in subsections (17.4) and (17.5), and

(b) the deadline, based on the issuer's new financial year end, for the next annual financial statements referred to in subsections (17.4) and (17.5).

(17.14) In Nova Scotia, if an issuer decides to change its financial year end by more than 14 days, it must make reasonably available to each holder of a security acquired under subsection (2.1) a notice containing the information set out in subsection (17.15) as soon as practicable and, in any event, no later than the earlier of

(a) the deadline, based on the issuer's old financial year end, for the next annual financial statements referred to in subsection (17.6), and

(b) the deadline, based on the issuer's new financial year end, for the next annual financial statements referred to in subsection (17.6).

(17.15) The notice referred to in subsections (17.13) and (17.14) must state

(a) that the issuer has decided to change its financial year end,

(b) the reason for the change,

(c) the issuer's old financial year end,

(d) the issuer's new financial year end,

(e) the length and ending date of the periods, including the comparative periods, of the annual financial statements referred to in subsections (17.4), (17.5) and (17.6) for the issuer's transition year and its new financial year, and

(f) the filing deadline for the annual financial statements for the issuer's transition year.

(17.16) If a transition year is less than 9 months in length, the issuer must include as comparative financial information to its annual financial statements for its new financial year

(a) a statement of financial position, a statement of comprehensive income, a statement of changes in equity, a statement of cash flows, and notes to the financial statements for its transition year,

(b) a statement of financial position, a statement of comprehensive income, a statement of changes in equity, a statement of cash flows, and notes to the financial statements for its old financial year,

(c) in the following circumstances, a statement of financial position as at the beginning of the old financial year:

(i) the issuer discloses in its annual financial statements an unreserved statement of compliance with IFRS, and

(ii) the issuer

(A) applies an accounting policy retrospectively in its annual financial statements,

(B) makes a retrospective restatement of items in its annual financial statements, or

(C) reclassifies items in its annual financial statements, and

(d) in the case of the issuer's first IFRS financial statements, the opening IFRS statement of financial position at the date of transition to IFRS.

(17.17) A transition year must not exceed 15 months.

(17.18) An SEC issuer satisfies subsections (17.13), (17.14) and (17.16) if

(a) it complies with the requirements of U.S. laws relating to a change of fiscal year, and

(b) it delivers a copy of all materials required by U.S. laws relating to a change in fiscal year to the securities regulatory authority at the same time as, or as soon as practicable after, they are filed with or furnished to the SEC and, in any event, no later than 120 days after the end of its most recently completed financial year.

(17.19) The financial statements of an issuer referred to in subsections (17.4), (17.5) and (17.6) must be accompanied by a notice of the issuer disclosing in reasonable detail the use of the aggregate gross proceeds raised by the issuer under section 2.9 in accordance with Form 45-106F16, unless the issuer has previously disclosed the use of the aggregate gross proceeds in accordance with Form 45-106F16.

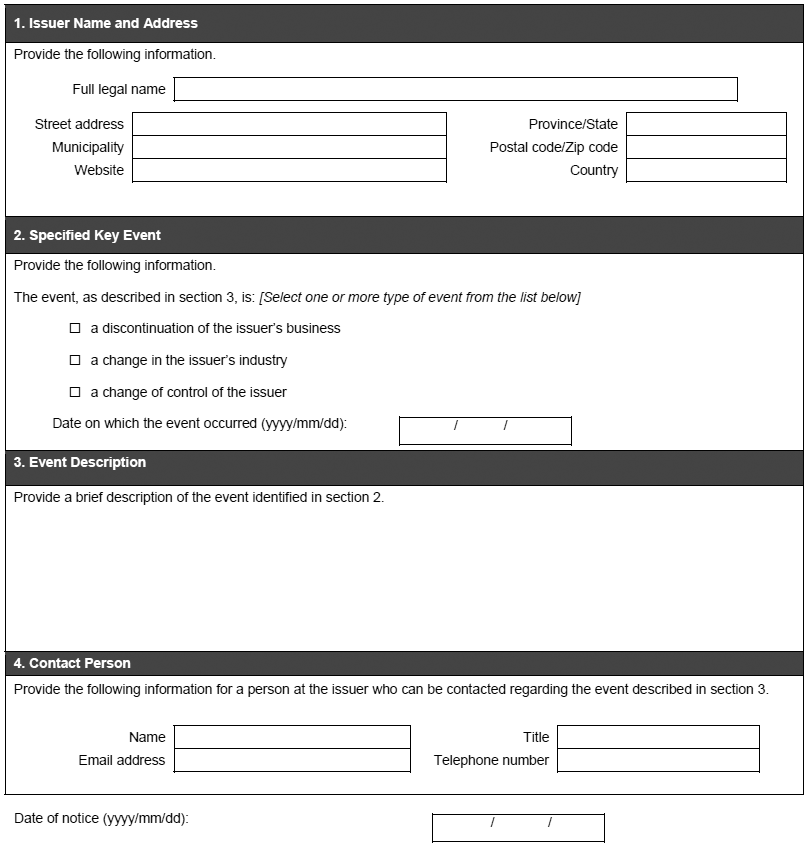

(17.20) In New Brunswick, Nova Scotia and Ontario, an issuer must make reasonably available to each holder of a security acquired under subsection (2.1) a notice of each of the following events in accordance with Form 45-106F17, within 10 days of the occurrence of the event:

(a) a discontinuation of the issuer's business;

(b) a change in the issuer's industry;

(c) a change of control of the issuer.

(17.21) An issuer is required to make the disclosure required respectively by subsections (17.4), (17.5), (17.6), (17.19) and (17.20) until the earliest of

(a) the date the issuer becomes a reporting issuer in any jurisdiction of Canada, and

(b) the date the issuer ceases to carry on business.

(17.22) In Ontario, an issuer that is not a reporting issuer in Ontario that distributes securities in reliance on the exemption in subsection (2.1) is designated a market participant under the Securities Act (Ontario).

(17.23) In New Brunswick, an issuer that is not a reporting issuer in New Brunswick that distributes securities in reliance on the exemption in subsection (2.1) is designated a market participant under the Securities Act (New Brunswick).

(18) Repealed. [B.C. Reg. 86/2011, s. (e).].

5. paragraph 6.1(1)(c) is amended by replacing "or (2) [Offering memorandum for Alberta, B.C., Manitoba, New Brunswick, Nova Scotia, Newfoundland and Labrador, Northwest Territories, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon]" with ", (2) or (2.1) [Offering memorandum]".

6. section 6.5 is amended by adding the following subsection:

(1.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, the required form of risk acknowledgement for individual investors includes Schedule 1 Classification of Investors Under the Offering Memorandum Exemption and Schedule 2 Investment Limits for Investors Under the Offering Memorandum Exemption to Form 45-106F4..

7. Part 8 is amended by adding the following sections:

8.4.1 Transition -- offering memorandum exemption -- update of offering memorandum -- Despite subsection 2.9(5.1), in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan, an issuer is not required to update an offering memorandum that was filed in the local jurisdiction before April 30, 2016, solely to incorporate the statement required under paragraph 2.9(5.1)(a), unless the offering memorandum would otherwise be required to be updated pursuant to subsection 2.9(14) or Instruction B.12 of Form 45-106F2 Offering Memorandum for Non-Qualifying Issuers.

8.4.2 Transition -- offering memorandum exemption -- marketing materials -- Despite paragraph 2.9(17.1)(a), in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan, OM marketing materials that relate to an offering memorandum that was filed in the local jurisdiction before April 30, 2016 and that are delivered or made reasonably available after April 30, 2016 must be filed within 10 days from the earlier of delivery to, or being made reasonably available to, a prospective purchaser..

8. Item 10.1 of Form 45-106F2 Offering Memorandum for Non-Qualifying issuers is amended by adding "Ontario," before "Prince Edward Island".

9. Item 10.2 of Form 45-106F2 Offering Memorandum for Non-Qualifying Issuers is amended by adding "Ontario," before "Prince Edward Island".

10. Item 10 of Form 45-106F3 Offering Memorandum for Qualifying Issuers is amended by adding "Ontario," before "Prince Edward Island".

11. Form 45-106F4 Risk Acknowledgement is amended

(a) by replacing "In Alberta, Manitoba, Northwest Territories, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon to qualify as an eligible investor, you may be required to obtain that advice" with "In Manitoba, Northwest Territories, Nunavut, Prince Edward Island and Yukon to qualify as an eligible investor, you may be required to obtain that advice", and

(b) by adding the following:

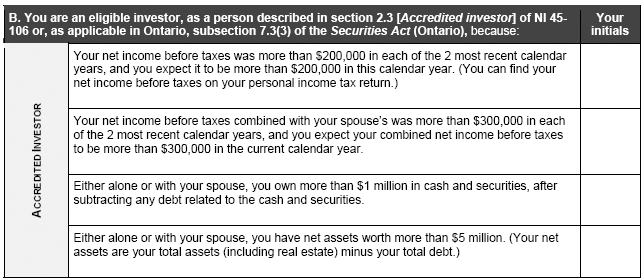

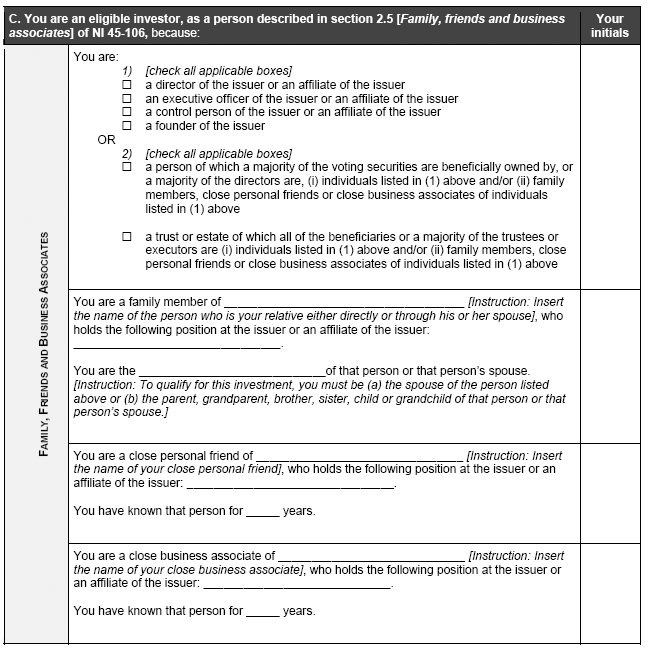

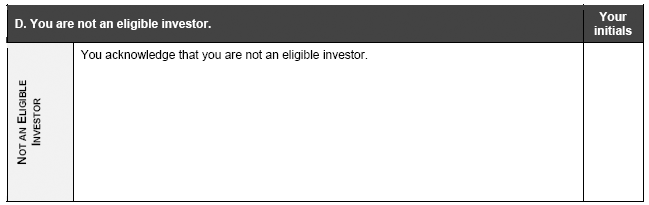

Schedule 1

Classification of Investors Under the Offering Memorandum Exemption

Instructions: This schedule must be completed together with the Risk Acknowledgement Form and Schedule 2 by individuals purchasing securities under the exemption (the offering memorandum exemption) in subsection 2.9(2.1) of National Instrument 45-106 Prospectus Exemptions (NI 45-106) in Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan.

- - - - - - - - - - - - - - - - - - - -

How you qualify to buy securities under the offering memorandum exemption

Initial the statement under A, B, C or D containing the criteria that applies to you. (You may initial more than one statement.) If you initial a statement under B or C, you are not required to complete A.

- - - - - - - - - - - - - - - - - - - -

Schedule 2

Investment Limits for Investors Under the Offering Memorandum Exemption

Instructions: This schedule must be completed together with the Risk Acknowledgement Form and Schedule 1 by individuals purchasing securities under the exemption (the offering memorandum exemption) in subsection 2.9(2.1) of National Instrument 45-106 Prospectus Exemptions (NI 45-106) in Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan.

- - - - - - - - - - - - - - - - - - - -

SECTION 1 TO BE COMPLETED BY THE PURCHASER

1. Investment limits you are subject to when purchasing securities under the offering memorandum exemption

You may be subject to annual investment limits that apply to all securities acquired under the offering memorandum exemption in a 12 month period, depending on the criteria under which you qualify as identified in Schedule 1. Initial the statement that applies to you.

- - - - - - - - - - - - - - - - - - - -

SECTION 2 TO BE COMPLETED BY THE REGISTRANT

2. Registrant information

[Instruction: this section must only be completed if an investor has received advice from a portfolio manager, investment dealer or exempt market dealer concerning his or her investment.]

First and last name of registrant (please print):

Registered as:

[Instruction: indicate whether registered as a dealing representative or advising representative]

Telephone:

Email:

Name of firm:

[Instruction: indicate whether registered as an exempt market dealer, investment dealer or portfolio manager.]

Date:

12. The Instrument is amended by adding the following form after Form 45-106F15:

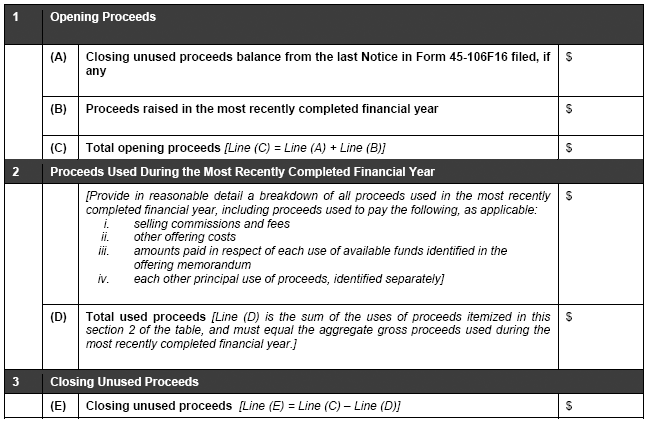

Form 45-106F16

Notice of Use of Proceeds

[Insert issuer name]

For the financial year ended [Insert end date of most recently completed financial year]

Date: [Specify the date of the Notice. The date must be no earlier than the date of the auditor's report on the financial statements for the issuer's most recently completed financial year.]

[Provide the information specified in the following table.]

[If any of the proceeds required to be disclosed in this table were paid directly or indirectly to a related party (as defined in Instruction A.6 of Form 45-106F2 Offering Memorandum Form for Non-Qualifying Issuers) of the issuer, state in each case the name of the related party to whom the payment was made, their relationship to the issuer and the amount paid to the related party.]

Instructions for Completing

Form 45-106F16

Notice of Use of Proceeds

1. The amount for Line (A) is taken from Line (E) in the prior year's Notice of Use of Proceeds (Notice), if applicable. If a Notice was not required in the prior year, then the amount for Line (A) is $nil.

2. The amount for Line (B) is the aggregate gross proceeds raised in all jurisdictions in Canada under section 2.9 [Offering memorandum] of National Instrument 45-106 (the OM exemption) during the most recently completed financial year. If an issuer raised funds in reliance on other prospectus exemptions concurrently with the OM exemption during the year and it is impractical to separately track proceeds raised only under the OM exemption, the issuer can provide the disclosure outlined in the table for the aggregate gross proceeds raised under all prospectus exemptions during the most recently completed financial year.

3. If Line (C) is $nil, then the issuer does not have an obligation to file, deliver or make reasonably available the Notice for that financial year.

4. In Section 2 of the table, the issuer must provide a breakdown in reasonable detail of the uses of the aggregate gross proceeds during the most recently completed financial year. Issuers should ensure that the disclosure is specific enough and provides sufficient detail for an investor to understand how the proceeds have been used.

5. Both direct and indirect payments to related parties must be disclosed. An example of an indirect payment could include repayment of a debt that was incurred for a prior payment to a related party.

6. Proceeds invested on a temporary basis would not generally be considered to have been used.

13. The Instrument is amended by adding the following form:

Form 45-106F17

Notice of Specified Key Events

This is the form required under subsection 2.9(17.20) of National Instrument 45-106 Prospectus Exemptions (NI 45-106) in New Brunswick, Nova Scotia and Ontario to make available notice of specified key events to holders of securities acquired under subsection 2.9(2.1) of NI 45-106.

5

14. This Instrument comes into force in Ontario on January 13, 2016 and in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan on April 30, 2016.