Multilateral CSA Notice of Amendments to National Instrument 45-106 Prospectus Exemptions Relating to the Offering Memorandum Exemption

Multilateral CSA Notice of Amendments to National Instrument 45-106 Prospectus Exemptions Relating to the Offering Memorandum Exemption

MULTILATERAL CSA NOTICE OF AMENDMENTS TO NATIONAL INSTRUMENT 45-106 PROSPECTUS EXEMPTIONS RELATING TO THE OFFERING MEMORANDUM EXEMPTION

Multilateral CSA Notice of Amendments

Annex A-1 -- Amending Instrument for National Instrument 45-106 Prospectus Exemptions

Annex A-3 -- Amending Instrument for National Instrument 45-102 Resale of Securities

Annex A-4 -- Amending Instrument for Multilateral Instrument 11-102 Passport System

Annex B-1 -- Changes to Companion Policy 45-16CP Prospectus Exemptions

Annex D -- Form 45-106F16 Notice of Use of Proceeds

Annex E -- Form 45-106F17 Notice of Specified Key Events

Annex F -- Summary of Key Changes to the March 2014 Materials

Annex G-2 -- Local Rule Amendments and Policy Changes

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Multilateral CSA Notice of Amendments

Multilateral CSA Notice of Amendments to National Instrument 45-106 Prospectus Exemptions Relating to the Offering Memorandum Exemption

October 29, 2015

Introduction

The securities regulatory authorities in Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan (collectively, the participating jurisdictions or we) are amending National Instrument 45-106 Prospectus Exemptions (NI 45-106) in respect of the offering memorandum exemption in section 2.9 of NI 45-106 (the OM exemption). We are also making changes to Companion Policy 45-106CP Prospectus Exemptions (45-106CP) and certain consequential amendments to other rules and one policy.

The participating jurisdictions have coordinated their efforts in finalizing the NI 45-106 amendments, related policy changes and other consequential rule amendments (collectively, the final amendments). The final amendments are made or proposed by each participating jurisdiction. In some jurisdictions, ministerial approvals are required for these changes.

Provided all necessary ministerial approvals are obtained, the final amendments will come into force in Ontario on January 13, 2016 and in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan on April 30, 2016.

Substance and purpose of the final amendments

The final amendments modify the existing OM exemption in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan and introduce an OM exemption in Ontario. The final amendments do not modify the OM exemption that exists in any CSA jurisdiction other than the participating jurisdictions.

In Ontario, the introduction of the OM exemption will allow business enterprises, particularly small and medium sized enterprises (SMEs), to benefit from greater access to capital from investors than has been previously permitted under Ontario securities law. We believe the OM exemption will provide business enterprises with a cost-effective way to raise capital by allowing them to distribute securities under an offering memorandum, while maintaining an appropriate level of investor protection.

In Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan, the modifications to the existing OM exemption will introduce new investor protection measures to address concerns observed with the use of the OM exemption in certain of these jurisdictions.

Regulatory framework

The prospectus requirement

Generally, when distributing securities, an issuer must provide investors with a prospectus containing full, true and plain disclosure of all material facts relating to the securities to be issued. Issuers that become reporting issuers are also required to provide prescribed periodic and timely disclosure. This disclosure is intended to provide both existing and potential new investors with the information necessary to make an informed decision regarding whether to buy, sell or hold the security. Due to the availability of ongoing material information, coupled with the initial disclosure provided through the prospectus, the outstanding securities are generally permitted to be freely tradeable. This combination of material information and free-trading securities then allows a market in the securities to develop.

Exemptions from the prospectus requirement

Prospectus exemptions are provided in circumstances where it is determined that the protections of a prospectus are not necessary. For example, certain prospectus exemptions, such as the accredited investor exemption and the family, friends and business associates exemption are based on factors such as:

• investor attributes, such as the investor having a certain level of sophistication, the ability to withstand financial loss and the financial resources to obtain expert advice, and

• the investor's relationship with certain principals of the issuer.

Investors who purchase securities of non-reporting issuers through prospectus exemptions do not generally have the benefits afforded by ongoing disclosure and free-trading securities.

The OM exemption

The OM exemption was designed to facilitate capital-raising by allowing issuers to solicit investments from a wider range of investors than they would be able to under other prospectus exemptions, provided that certain conditions are met. Some of these investors may not have the same level of sophistication, ability to withstand loss or relationship with management as those who qualify to purchase securities under other commonly used capital-raising exemptions, such as the accredited investor exemption or the family, friends and business associates exemption.

In the jurisdictions that currently have an OM exemption, investors are provided with a disclosure document at the point of sale (an offering memorandum), as well as a risk acknowledgement form in respect of their initial investment. However, under the OM exemption, less disclosure is required to be provided to investors by issuers at the point of sale relative to what is required to be included in a prospectus, and currently, no disclosure is required to be provided to investors under securities law by non-reporting issuers on an ongoing basis. In addition, securities acquired under the OM exemption are not freely tradeable. Together, these features of the OM exemption represent potential risks.

In light of the particular risks associated with the OM exemption and based on the experience of certain participating jurisdictions that currently have a version of the exemption in place, we believe that it is appropriate to introduce some new investor protection measures to the OM exemption. These include:

• requiring that non-reporting issuers provide to investors:

• audited annual financial statements,

• an annual notice on how the proceeds raised under the OM exemption have been used, and

• in New Brunswick, Nova Scotia and Ontario, notice in the event of a discontinuation of the issuer's business, a change in the issuer's industry or a change of control of the issuer,

• requiring that marketing materials be incorporated by reference into the offering memorandum to provide investors with the same rights of action in respect of all disclosure made under the OM exemption in the event of a misrepresentation, and

• imposing additional investment limits in respect of both eligible (i.e., investors who meet certain income or asset thresholds) and non-eligible investors that are individuals to limit the risks associated with an investment in securities acquired under the OM exemption.

New key features of the OM exemption

The following is a summary of the new key features of the OM exemption adopted by the participating jurisdictions.

(a) Investment limits

The participating jurisdictions have adopted investment limits for both eligible and non-eligible investors that are individuals (other than those that qualify as accredited investors or under the family, friends and business associates exemption). These limits will not apply to non-individual investors, whether eligible or non-eligible. The final amendments permit a higher investment threshold for eligible investors when a portfolio manager, investment dealer or exempt market dealer has made a positive suitability assessment.

The investment limits will apply to all securities acquired under the OM exemption as follows:

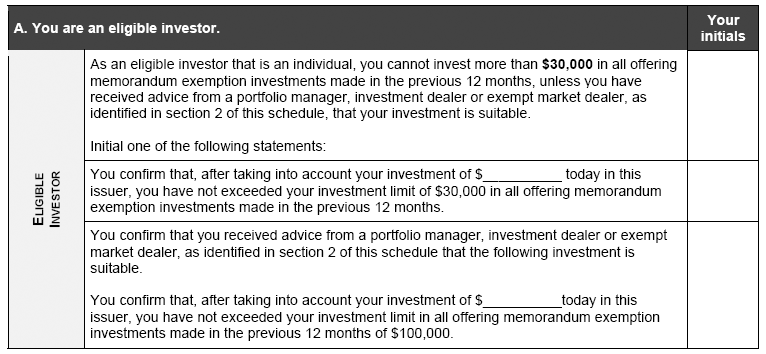

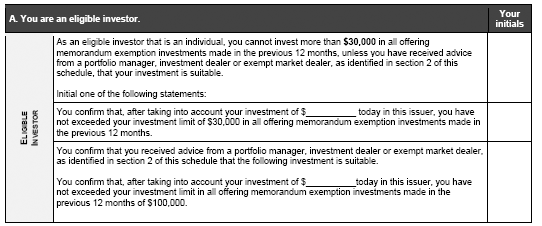

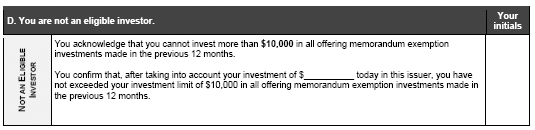

• in the case of a non-eligible investor that is an individual, the acquisition cost of all securities acquired by the purchaser under the OM exemption in the preceding 12 months cannot exceed $10,000,

• in the case of an eligible investor that is an individual, the acquisition cost of all securities acquired by the purchaser under the OM exemption in the preceding 12 months cannot exceed $30,000, and

• in the case of an eligible investor that is an individual and that receives advice from a portfolio manager, investment dealer or exempt market dealer that the investment above $30,000 is suitable, the acquisition cost of all securities acquired by the purchaser under the OM exemption in the preceding 12 months cannot exceed $100,000.

(b) New schedules to the risk acknowledgement form

The participating jurisdictions will continue to require all investors (including those who qualify as permitted clients) to complete and sign form 45-106F4 Risk Acknowledgement, which highlights for investors the key risks associated with investing in securities acquired under the OM exemption.

However, two new schedules have been added which must be completed by each investor that is an individual in conjunction with the risk acknowledgement form. One schedule asks investors to confirm their status, as an eligible investor, non-eligible investor, accredited investor or an investor who would qualify to purchase securities under the family, friends and business associates exemption. The other schedule requires confirmation that the investor is within the investment limits, where applicable. Investors that are not individuals do not have to complete these new schedules.

(c) Disclosure of audited annual financial statements, notice of use of proceeds and notice of specified key events

Non-reporting issuers that use the OM exemption will be required to provide audited annual financial statements to investors, as well as a notice that accompanies the financial statements which describes how the money raised under the OM exemption has been used. A new prescribed form has been introduced for the purposes of this disclosure.

In New Brunswick, Nova Scotia and Ontario, non-reporting issuers will also be required to provide notice to investors of the following events, within 10 days of the event occurring, in a new prescribed form:

• a discontinuation of the issuer's business,

• a change in the issuer's industry, or

• a change of control of the issuer.

(d) Marketing materials

Marketing materials used by issuers in distributions under the OM exemption must be incorporated by reference into the offering memorandum. As a result, the marketing materials will be subject to the same liability as the disclosure provided in the offering memorandum in the event of a misrepresentation.

(e) Other features

Issuers will be prohibited from relying on the OM exemption to distribute specified derivatives or structured finance products. In Alberta, Nova Scotia and Saskatchewan, the OM exemption will continue to be available to investment funds only if they are non-redeemable investment funds or mutual funds that are reporting issuers. In New Brunswick, Ontario and Québec, the OM exemption will not be available to investment funds.

Background

The participating jurisdictions other than the Nova Scotia Securities Commission (NSSC) previously requested comment (the March 2014 materials) on proposals reflected in the final amendments. On March 20, 2014, as part of a broad review of the exempt market, the Ontario Securities Commission (OSC) published a Notice and Request for Comment which included the proposed amendments to the OM exemption and related policy changes (the OSC proposals). On the same date, in response to concerns with the use of the OM exemption, the Alberta Securities Commission (ASC), Autorité des marchés financiers (AMF), Financial and Consumer Affairs Authority of Saskatchewan (FCAA) and Financial and Consumer Services Commission (New Brunswick) (FCNB) published a Multilateral CSA Notice of Publication and Request for Comment regarding proposed amendments to the OM exemption and related policy changes (the MI proposals). The proposals of the ASC, AMF and FCAA were largely aligned, while the FCNB proposal was primarily harmonized with the OSC proposals.

On May 7, 2015, the NSSC published a Notice and Request for Comment (the May 2015 materials) which proposed changes to the OM exemption in Nova Scotia that are similar to the final amendments.

Summary of written comments received by the participating jurisdictions

The comment period for the March 2014 materials ended on June 18, 2014. The participating jurisdictions that published the March 2014 materials collectively received written submissions from 1000 commenters regarding the OM exemption. Comment letters received by the following jurisdictions can be viewed on their websites:

• OSC -- www.osc.gov.on.ca

• AMF -- www.lautorite.qc.ca

• ASC -- www.albertasecurities.com

The comment period for the May 2015 materials ended on July 6, 2015. The NSSC received written submissions from four commenters. These comment letters can be viewed on the NSSC website at nssc.novascotia.ca.

We have considered the comments received and thank all of the commenters for their input.

A summary of the comments submitted to the OSC, together with the responses of the OSC, is included as part of the local notice published in Ontario at Annex G.

A summary of the general themes raised in the comment letters that were received across the participating jurisdictions can be found under the heading "Key themes from the comment letters" below.

Key themes from the comment letters

There were several key themes expressed in the comment letters submitted to the participating jurisdictions. Below is a summary of these key themes.

Harmonization

A significant number of commenters expressed concern about a lack of harmonization in the OM exemption across CSA jurisdictions, with some indicating that harmonization of the OM exemption should be a primary goal of the CSA. Commenters indicated that lack of harmonization could result in:

• increased complexity for issuers in complying with the OM exemption,

• increased time and cost for market participants, and

• increased regulatory burden.

Some commenters suggested that a lack of harmonization could deter issuers, especially SMEs, from using the OM exemption.

As a starting point, we have worked with the version of the OM exemption that currently exists in certain participating jurisdictions, such as Alberta and Québec. Currently, there are two primary models of the OM exemption that exist across the CSA (other than Ontario, which has not previously had an OM exemption).

The participating jurisdictions have endeavoured to harmonize the proposed new OM exemption. While we have not achieved complete harmonization, we believe that, having regard to different local capital markets and experiences, we have achieved substantial harmonization on most of the key aspects of the OM exemption. Further, in relation to the non-participating jurisdictions, there remains harmonization in important areas, such as the forms of offering memorandum and risk acknowledgement.

The participating jurisdictions believe the changes being made to the OM exemption are necessary to address investor protection concerns.

Use of data

Many commenters suggested that securities regulators should gather and publish more data on the exempt market in order to inform policy initiatives. Some commenters expressed concern about whether the participating jurisdictions had access to sufficient data to support the amendments that were being proposed, and indicated that no such data had been published.

We believe that we have access to sufficient information to make the policy decisions that are reflected in the OM exemption set out in the final amendments. At this time, the primary source of data on the exempt market available to securities regulators is the information filed with us through reports of exempt distribution. For example, data on the use of the OM exemption is currently gathered in those CSA jurisdictions that have the OM exemption. The ASC previously published a summary of that data in the MI proposals published for comment on March 20, 2014.

In addition, we considered data or information from a number of sources to support our review:

• the results of a survey conducted by a third party service provider engaged by the OSC as part of its review of new capital raising prospectus exemptions that provided insight into retail investors' views on investing in SMEs,

• household balance sheet data from Ipsos Reid's 2012 Canadian Financial Monitor Survey,

• feedback from investors obtained through consultations and other informal means,

• information regarding complaints and enforcement activity related to the OM exemption in those participating jurisdictions that currently have the OM exemption,

• consultations conducted in certain participating jurisdictions with a variety of market participants, and

• comments received on the proposals published in OSC Staff Consultation Paper 45-710 Considerations for New Capital Raising Prospectus Exemptions.

The CSA recently announced an initiative to modernize and update the reports of exempt distribution in order to obtain more detailed information on activity in the exempt market. A revised report of exempt distribution was published for comment by the CSA on August 13, 2015. The revised report is intended to provide securities regulators with necessary information to facilitate more effective regulatory oversight of the exempt market and improve analysis for policy development purposes.

Investment limits

The March 2014 materials published by the FCNB and OSC included proposed investment limits of $10,000 for non-eligible investors that are individuals and $30,000 for eligible investors that are individuals for all securities acquired under the OM exemption in a 12-month period.

The March 2014 materials published by the ASC, AMF and FCAA included proposed investment limits of:

• $10,000 for all investors that are not eligible investors for all securities acquired under the OM exemption in a 12-month period, and

• $30,000 for eligible investors that are individuals and that are not accredited investors and do not qualify as specified family members, close personal friends or close business associates under the family, friends and business associates exemption in a 12-month period.

Most commenters were opposed to the proposed investment limits, and suggested that they would be overly restrictive and unfair to investors. In particular, the commenters noted the following:

• Investment limits would restrict investor choice and would reduce the ability of investors to appropriately design and diversify their investment portfolios.

• The investment limits are inflexible as they treat all eligible investors the same and do not take into account the particular financial circumstances of each individual investor.

• The investment limits would reduce the amount of capital available to issuers.

• National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations (NI 31-103) provides an appropriate regulatory framework for the exempt market and securities regulators should rely on the know-your-client, know-your-product and suitability obligations of registrants, instead of imposing limits on investors.

• The investment limits would have unintended consequences. For instance, registrants would "sell to the cap" and the sales process would be at risk of becoming a "tick the box" exercise.

• The investment limits would be too small to enable dealers to offer investments under the OM exemption on a cost-effective basis.

• The investment limits do not account for the stage-based nature of private capital.

• The investment limits would result in the redesign of exempt market products in attempts to avoid the limits.

In addition, many commenters noted that there have been significant losses in the public markets, yet investors are not restricted with respect to how much they can invest in those markets. Others were of the view that the proposed investment limits would not address the actual reasons why investors may lose money in investments under the OM exemption, and accordingly would not serve to protect investors. Further, concern was expressed that by setting a limit of $30,000 for individual eligible investors, securities regulators appeared to be suggesting that this amount was an acceptable loss.

We continue to believe that investment limits are a necessary and appropriate investor protection tool that can help to reduce the risk associated with an investment in securities under the OM exemption, while still facilitating capital-raising by issuers.

However, in light of the feedback that we received, we considered different approaches to investment limits under the OM exemption and have made some changes to the investment limits that were proposed in the March 2014 materials. We believe that the revised approach to investment limits is more flexible, given that the category of "eligible investor" may include individual investors with very different financial circumstances, but still provides appropriate investor protection. The participating jurisdictions have also harmonized their positions since March 2014 so that the investment limits for both eligible and non-eligible investors do not apply to non-individual investors, such as corporations, partnerships or trusts. In addition, we have also made changes to the rule to prohibit the creation or use of an entity, such as a corporation or trust, solely for the purpose of relying on the OM exemption.

Disclosure requirements

The March 2014 materials proposed additional disclosure requirements for non-reporting issuers that distribute securities in reliance on the OM exemption. These requirements included the following:

• audited annual financial statements,

• a notice of the use of proceeds raised in reliance on the OM exemption, and

• in Ontario and New Brunswick, a notice of specified key events, to be provided within 10 days of the event occurring.

Commenters generally expressed support for requiring this disclosure to be provided by non-reporting issuers that use the OM exemption. However, some commenters did not support this requirement, on the basis that this would be a significant departure from current expectations for non-reporting issuers and would create additional costs for these issuers.

We believe that requiring non-reporting issuers raising money under the OM exemption to provide these items of disclosure to investors is necessary to provide investors with accurate and transparent information about their investment.

(a) Audited annual financial statements

Commenters generally supported requiring audited annual financial statements to be prepared in accordance with International Financial Reporting Standards (IFRS). However, some commenters suggested that these financial statements should only have to be audited by issuers that raise funds in reliance on the OM exemption above a certain threshold (with different thresholds being proposed by commenters). Some commenters did not support requiring an audit as this would impose an added cost that may be difficult for issuers, particularly SMEs, to bear which would not be justified given the limited utility of the financial statements. Other commenters stated that requiring the audited financial statements to be prepared in accordance with IFRS would also increase issuers' costs.

In considering this requirement, we noted that corporate legislation in many jurisdictions of Canada already requires shareholders to be provided with annual financial statements.

The final amendments retain the requirement for non-reporting issuers that rely on the OM exemption to provide audited annual financial statements prepared in accordance with IFRS. However, we are aware that the audit requirement could impose an additional burden on some smaller issuers, and we will continue to consider this matter during a future phase of our review.

Additionally, certain jurisdictions currently provide relief from the audit requirement as well as the requirement to prepare financial statements in accordance with IFRS in certain circumstances through blanket orders. In appropriate circumstances, securities regulators that do not currently provide relief through blanket orders may consider granting exemptive relief from these requirements, which would be considered on a case by case basis.

The final amendments also provide an extension to the filing deadline in certain limited circumstances for issuers that would be required to file annual financial statements for a financial year that ends prior to the issuer's first distribution under the OM exemption. This would allow issuers to file the financial statements on or before the later of the 60th day after the issuer distributes securities under the OM exemption, and the deadline to file, deliver or make reasonably available the financial statements.

(b) Notice of discontinuation of the issuer's business, change of industry or change of control

Many commenters supported requiring non-reporting issuers to provide notice to investors of specified key events. However, some objected to this requirement because it would not be harmonized across all participating jurisdictions and it might result in increased costs for issuers.

In New Brunswick, Nova Scotia and Ontario, the final amendments require that non-reporting issuers must provide notice of specified key events to investors within 10 days of the event occurring. However, the notice will only be required with respect to the following events, which is a more limited list of events than the list set out in the March 2014 materials:

• a discontinuation of the issuer's business,

• a change in the issuer's industry, and

• a change of control of the issuer.

The FCNB, NSSC and OSC believe that this requirement will impose only a minimal administrative burden on issuers, given that the listed events will occur infrequently. We have also prescribed a form that sets parameters as to the nature and comprehensiveness of the information that will be required to be provided in the notice. At the same time, we believe that information on these key events would be of interest to investors and should be reported to them.

Role of related registrants

In the March 2014 materials, the FCNB and OSC proposed that registrants related to the issuer (i.e., affiliated registrants or registrants in the same corporate structure) would be prohibited from participating in a distribution of securities under the OM exemption.

Commenters expressed significant concern with this proposal. Some of the specific concerns raised by commenters included the following:

• Sales through a related registrant have long been accepted as part of the securities industry in Canada.

• All registrants are subject to the same regulatory oversight.

• There may be valid business reasons for an issuer to distribute securities through a related registrant, such as reduced costs.

• Excluding related registrants may negatively impact the ability of smaller issuers to raise capital under the OM exemption.

• Adequate safeguards relating to risks associated with the exempt market, including conflicts of interest, already exist.

• Excluding related registrants will negatively impact many registrants.

After considering the comments received, the FCNB and OSC have decided to remove the prohibition against related registrants participating in a distribution under the OM exemption. The existing regulatory framework requires registrants to identify and respond to material conflicts of interest that may affect their ability to meet their regulatory obligations, including conducting suitability assessments. We have included companion policy guidance to remind registrants of their responsibilities to address conflicts of interest in accordance with their regulatory obligations under NI 31-103 and National Instrument 33-105 Underwriting Conflicts.

Exclusion of investment funds

Some commenters did not understand the policy rationale for the FCNB and OSC excluding investment funds from using the OM exemption as reflected in the March 2014 materials.

The FCNB and OSC continue to believe that it is appropriate to exclude investment funds from being able to distribute securities in reliance on the OM exemption. Since the end of the comment period on the March 2014 materials, the AMF has also decided to exclude investment funds from relying on the OM exemption.

Investment funds sold to retail investors are subject to significant and robust product regulation in national rules such as National Instrument 81-102 Investment Funds and National Instrument 81-107 Independent Review Committee for Investment Funds, including custodial requirements, voting requirements, conflict of interest provisions and investment restrictions. Mutual funds sold to retail investors are also required to provide investors with summary disclosure in a fund facts document. Additionally, the CSA is currently examining the fee structures of mutual funds sold to retail investors which may result in rulemaking initiatives. To permit investment funds to sell to retail investors under the OM exemption without the benefit of the disclosure and product regulation that applies to retail investment funds would be inconsistent with the principles underlying these existing rules and with three ongoing investment fund policy initiatives: modernization of investment fund regulation; point of sale disclosure for mutual funds; and the review of the cost of ownership of mutual funds. Further, the exclusion of investment funds is consistent with the objective of facilitating capital raising for business enterprises, particularly SMEs.

The ASC, FCAA and NSSC anticipate considering this issue in a later phase of the review of the OM exemption.

Summary of changes to the final amendments

After considering the comments received on the March 2014 materials and the May 2015 materials and consultations with stakeholders, we have made some changes to what was originally proposed. The changes are reflected in the final amendments.

Annex F contains a summary of key differences between the final amendments and the March 2014 materials. In addition to the changes described in Annex F, we have revised the companion policy guidance proposed in the March 2014 materials, as appropriate, to reflect the amendments to NI 45-106.

We do not consider the changes made since the publication for comment to be material and therefore are not republishing the final amendments for a further comment period, except in Québec, where some of the consequential amendments must be published for comment for a 30-day period and Saskatchewan, where some of the consequential amendments must be published for comment for a 60-day period.

Implementation of the final amendments

The final amendments will become effective on different dates in Ontario and the other participating jurisdictions. Subject to Ministerial approval where required, in Ontario, the final amendments will become effective on January 13, 2016 and in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan, the final amendments will become effective on April 30, 2016.

A large majority of the issuers currently using the OM exemption have a December 31 year-end. The April 30, 2016 effective date in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan will allow these issuers to complete any offering that was initiated in these jurisdictions prior to the new requirements becoming effective and to decide whether they wish to continue using the OM exemption in its new form. It will also provide additional time for the non-December 31 year-end issuers that are currently using the OM exemption to transition to the new requirements.

Despite the delayed effective date in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan, issuers must keep in mind that if they initiate a distribution or expand a distribution into Ontario once the OM exemption is available in Ontario, the issuer will be required to comply with all of the requirements of the OM exemption in Ontario, despite the later effective date in the other participating jurisdictions.

Consequential amendments

National and multilateral amendments

We are making consequential amendments to the following instruments:

• National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards, and

• National Instrument 45-102 Resale of Securities.

The ASC, FCNB, NSSC, AMF and FCAA are also making consequential amendments to Multilateral Instrument 11-102 Passport System.

In Québec, the consequential amendments to the above instruments were published for comment on October 22, 2015, for a 30-day comment period. In Saskatchewan, the consequential amendments to the above instruments were published for comment today for a 60-day comment period. The consequential amendments are intended to come into force in Québec and Saskatchewan at the same time as the amendments to NI 45-106 come into force in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan, on April 30, 2016.

We are also making a minor change to National Policy 11-203 Process for Exemptive Relief Applications in Multiple Jurisdictions to reflect the changes being made to the OM exemption.

Local amendments

Any changes to local rules or policies will be identified in a local notice, where applicable.

Local matters

Annex G is being published in any local jurisdiction that is making related changes to local securities laws and sets out any additional information that is relevant to that jurisdiction only, including information about any applicable approval processes.

Questions

Please refer your questions to any of the following:

Annexes to Notice

|

Annex A -- Rule Amendments |

|||

|

|

|||

|

|

Annex A-1 |

-- |

Amending Instrument for National Instrument 45-106 Prospectus Exemptions |

|

|

|||

|

|

Annex A-2 |

-- |

Amending Instrument for National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards |

|

|

|||

|

|

Annex A-3 |

-- |

Amending Instrument for National Instrument 45-102 Resale of Securities |

|

|

|||

|

|

Annex A-4 |

-- |

Amending Instrument for Multilateral Instrument 11-102 Passport System |

|

|

|||

|

Annex B -- Policy Changes |

|||

|

|

|||

|

|

Annex B-1 |

-- |

Changes to Companion Policy 45-106CP Prospectus Exemptions |

|

|

|||

|

|

Annex B-2 |

-- |

Changes to National Policy 11-203 Process for Exemptive Relief Applications in Multiple Jurisdictions |

|

|

|||

|

Annex C -- Schedule 1 Classification of Investors Under the Offering Memorandum Exemption and Schedule 2 Investment Limits for Investors Under the Offering Memorandum Exemption to Form 45-106F4 Risk Acknowledgement |

|||

|

|

|||

|

Annex D -- Form 45-106F16 Notice of Use of Proceeds |

|||

|

|

|||

|

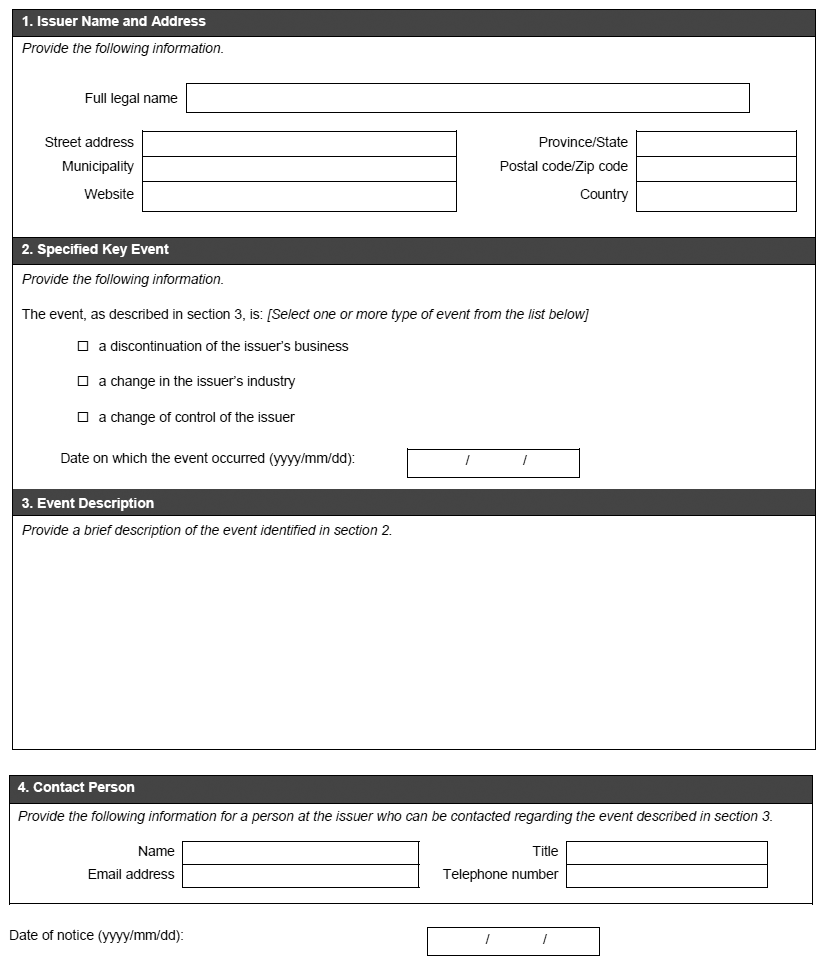

Annex E -- Form 45-106F17 Notice of Specified Key Events |

|||

|

|

|||

|

Annex F -- Summary of Key Changes to the March 2014 Materials |

|||

|

|

|||

|

Annex G -- Local Matters |

|||

Annex A-1 -- Amending Instrument for National Instrument 45-106 Prospectus Exemptions

ANNEX A-1

AMENDING INSTRUMENT FOR NATIONAL INSTRUMENT 45-106 PROSPECTUS EXEMPTIONS

Amendments to National Instrument 45-106 Prospectus Exemptions

1. National Instrument 45-106 Prospectus Exemptions is amended by this Instrument.

2. Section 1.1 is amended

(a) in paragraph (b) of the definition of "eligibility adviser" by deleting "Saskatchewan or",

(b) in paragraph (h) of the definition of "eligible investor" by adding "in Manitoba, Northwest Territories, Nunavut, Prince Edward Island and Yukon," before "a person that has obtained advice".

3. The Instrument is amended by adding the following section:

1.1.1 In this Instrument, in Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan

"date of transition to IFRS" has the same meaning as in National Instrument 51-102 Continuous Disclosure Obligations;

"exempt market dealer" has the same meaning as in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

"first IFRS financial statements" has the same meaning as in National Instrument 51-102 Continuous Disclosure Obligations;

"investment dealer" has the same meaning as in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

"new financial year" means the financial year of an issuer that immediately follows a transition year;

"old financial year" means the financial year of an issuer that immediately precedes a transition year;

"OM marketing materials" means a written communication, other than an OM standard term sheet, intended for prospective purchasers regarding a distribution of securities under an offering memorandum delivered under section 2.9 [Offering memorandum] that contains material facts relating to an issuer, securities or an offering;

"OM standard term sheet" means a written communication intended for prospective purchasers regarding a distribution of securities under an offering memorandum delivered under section 2.9 [Offering memorandum] that

(a) is dated,

(b) includes the following legend, or words to the same effect, on the first page:

"This document does not provide disclosure of all information required for an investor to make an informed investment decision. Investors should read the offering memorandum, especially the risk factors relating to the securities offered, before making an investment decision.",

(c) contains only the following information in respect of the issuer, the securities or the offering:

(i) the name of the issuer;

(ii) the jurisdiction or foreign jurisdiction in which the issuer's head office is located;

(iii) the statute under which the issuer is incorporated, continued or organized or, if the issuer is an unincorporated entity, the laws of the jurisdiction or foreign jurisdiction under which it is established and exists;

(iv) a brief description of the business of the issuer;

(v) a brief description of the securities;

(vi) the price or price range of the securities;

(vii) the total number or dollar amount of the securities, or range of the total number or dollar amount of the securities;

(viii) the names of any agent, finder or other intermediary, whether registered or not, involved with the offering and the amount of any commission, fee or discount payable to them;

(ix) the proposed or expected closing date of the offering;

(x) a brief description of the use of proceeds;

(xi) the exchange on which the securities are proposed to be listed, if any, provided that the OM standard term sheet complies with the requirements of securities legislation for listing representations;

(xii) in the case of debt securities, the maturity date of the debt securities and a brief description of any interest payable on the debt securities;

(xiii) in the case of preferred shares, a brief description of any dividends payable on the securities;

(xiv) in the case of convertible securities, a brief description of the underlying securities into which the convertible securities are convertible;

(xv) in the case of exchangeable securities, a brief description of the underlying securities into which the exchangeable securities are exchangeable;

(xvi) in the case of restricted securities, a brief description of the restriction;

(xvii) in the case of securities for which a credit supporter has provided a guarantee or alternative credit support, a brief description of the credit supporter and the guarantee or alternative credit support provided;

(xviii) whether the securities are redeemable or retractable;

(xix) a statement that the securities are eligible, or are expected to be eligible, for investment in registered retirement savings plans, tax-free savings accounts or other registered plans, if the issuer has received, or reasonably expects to receive, a legal opinion that the securities are so eligible;

(xx) contact information for the issuer or any registrant involved, and

(d) for the purposes of paragraph (c), "brief description" means a description consisting of no more than three lines of text in type that is at least as large as that used generally in the body of the OM standard term sheet;

"portfolio manager" has the same meaning as in National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations;

"SEC issuer" has the same meaning as in National Instrument 51-102 Continuous Disclosure Obligations;

"specified derivative" has the same meaning as in National Instrument 44-102 Shelf Distributions;

"structured finance product" has the same meaning as in National Instrument 25-101 Designated Rating Organizations;

"transition year" means the financial year of an issuer in which the issuer has changed its financial year end;

"U.S. laws" has the same meaning as in National Instrument 51-102 Continuous Disclosure Obligations..

4. Section 2.9 is amended

(a) in subsection (1) by deleting ", New Brunswick, Nova Scotia",

(b) in subsection (2) by replacing "In Alberta, Manitoba, Northwest Territories, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon" with "In Manitoba, Northwest Territories, Nunavut, Prince Edward Island and Yukon",

(c) by adding the following subsections:

(2.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, the prospectus requirement does not apply to a distribution by an issuer of a security of its own issue to a purchaser if

(a) the purchaser purchases the security as principal,

(b) the acquisition cost of all securities acquired by a purchaser who is an individual under this section in the preceding 12 months does not exceed the following amounts:

(i) in the case of a purchaser that is not an eligible investor, $10 000;

(ii) in the case of a purchaser that is an eligible investor, $30 000;

(iii) in the case of a purchaser that is an eligible investor and that received advice from a portfolio manager, investment dealer or exempt market dealer that the investment is suitable, $100 000,

(c) at the same time or before the purchaser signs the agreement to purchase the security, the issuer

(i) delivers an offering memorandum to the purchaser in compliance with subsections (5) to (13), and

(ii) obtains a signed risk acknowledgement from the purchaser in compliance with subsection (15), and

(d) the security distributed by the issuer is not either of the following:

(i) a specified derivative;

(ii) a structured finance product.

(2.2) The prospectus exemption described in subsection (2.1) is not available

(a) in Alberta, Nova Scotia and Saskatchewan, to an issuer that is an investment fund, unless the issuer is a non-redeemable investment fund or a mutual fund that is a reporting issuer, or

(b) in New Brunswick, Ontario and Québec, to an issuer that is an investment fund.

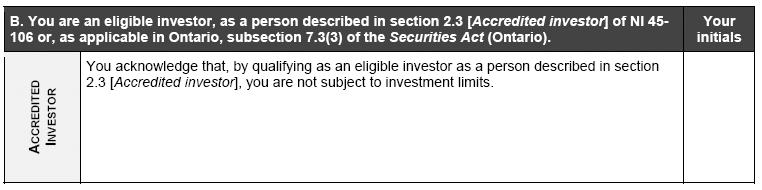

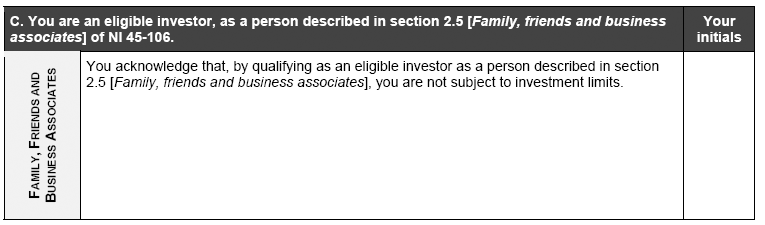

(2.3) The investment limits described in subparagraphs (2.1)(b)(ii) and (iii) do not apply if the purchaser is

(a) an accredited investor, or

(b) a person described in subsection 2.5(1) [Family, friends and business associates].,

(d) in subsection (3) by replacing "In Alberta, Manitoba, Northwest Territories, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon" with "In Manitoba, Northwest Territories, Nunavut, Prince Edward Island and Yukon",

(e) by adding the following subsection:

(3.0.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, this section does not apply to a distribution of a security to a person that was created, or is used, solely to purchase or hold securities in reliance on the exemption from the prospectus requirement set out in subsection (2.1).,

(f) in subsection (3.1) by replacing "Subsections (1) and (2)", with "Subsections (1), (2) and (2.1)",

(g) in subsection (4) by deleting ", Saskatchewan",

(h) by adding the following subsections:

(5.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, an offering memorandum delivered under subsection (2.1)

(a) must incorporate by reference, by way of a statement in the offering memorandum, OM marketing materials related to each distribution under the offering memorandum and delivered or made reasonably available to a prospective purchaser before the termination of the distribution, and

(b) is deemed to incorporate by reference OM marketing materials related to each distribution under the offering memorandum and delivered or made reasonably available to a prospective purchaser before the termination of the distribution.

(5.2) A portfolio manager, investment dealer or exempt market dealer must not distribute OM marketing materials unless the OM marketing materials have been approved in writing by the issuer.,

(i) in subsections (15) and (16) by replacing "(1) or (2)" with "(1), (2) or (2.1)" wherever the phrase appears, and

(j) by adding the following subsections:

(17.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, the issuer must file with the securities regulatory authority a copy of all OM marketing materials required or deemed to be incorporated by reference into an offering memorandum delivered under this section,

(a) if the OM marketing materials are prepared on or before the filing of the offering memorandum, concurrently with the filing of the offering memorandum, or

(b) if the OM marketing materials are prepared after the filing of the offering memorandum, within 10 days of the OM marketing materials being delivered or made reasonably available to a prospective purchaser.

(17.2) OM marketing materials filed under subsection (17.1) must include a cover page clearly identifying the offering memorandum to which they relate.

(17.3) Subsections (17.4) to (17.21) apply to issuers that rely on subsection (2.1) and that are not reporting issuers in any jurisdiction of Canada.

(17.4) In Alberta, an issuer must, within 120 days after the end of each of its financial years, file with the securities regulatory authority annual financial statements and make them reasonably available to each holder of a security acquired under subsection (2.1).

(17.5) In New Brunswick, Ontario, Québec and Saskatchewan, an issuer must, within 120 days after the end of each of its financial years, deliver annual financial statements to the securities regulatory authority and make them reasonably available to each holder of a security acquired under subsection (2.1).

(17.6) In Nova Scotia, an issuer must, within 120 days after the end of each of its financial years, make reasonably available annual financial statements to each holder of a security acquired under subsection (2.1).

(17.7) Despite subsections (17.4), (17.5) and (17.6), as applicable, if an issuer is required to file, deliver or make reasonably available annual financial statements for a financial year that ended before the issuer distributed securities under subsection (2.1) for the first time, those annual financial statements must be filed in Alberta, delivered in New Brunswick, Ontario, Québec and Saskatchewan or made reasonably available in Nova Scotia, as applicable, on or before the later of

(a) the 60th day after the issuer first distributes securities under subsection (2.1), and

(b) the deadline in subsection (17.4), (17.5) or (17.6), as applicable, to file, deliver or make reasonably available the annual financial statements.

(17.8) The annual financial statements of an issuer referred to in subsections (17.4), (17.5) and (17.6) must include

(a) a statement of comprehensive income, a statement of changes in equity, and a statement of cash flows for

(i) the most recently completed financial year, and

(ii) the financial year immediately preceding the most recently completed financial year, if any,

(b) a statement of financial position as at the end of each of the periods referred to in paragraph (a),

(c) in the following circumstances, a statement of financial position as at the beginning of the financial year immediately preceding the most recently completed financial year:

(i) the issuer discloses in its annual financial statements an unreserved statement of compliance with IFRS, and

(ii) the issuer

(A) applies an accounting policy retrospectively in its annual financial statements,

(B) makes a retrospective restatement of items in its annual financial statements, or

(C) reclassifies items in its annual financial statements,

(d) in the case of the issuer's first IFRS financial statements, the opening IFRS statement of financial position at the date of transition to IFRS, and

(e) notes to the annual financial statements.

(17.9) If the annual financial statements referred to in subsection (17.8) present the components of profit or loss in a separate income statement, the separate income statement must be displayed immediately before the statement of comprehensive income referred to in subsection (17.8).

(17.10) The annual financial statements referred to in subsection (17.8) must be audited.

(17.11) Despite subsection (17.10), for the first annual financial statements of an issuer referred to in subsections (17.4), (17.5) and (17.6), comparative information relating to the preceding financial year is not required to be audited if it has not been previously audited.

(17.12) Any period referred to in subsection (17.8) that has not been audited must be clearly labelled as unaudited.

(17.13) In Alberta, New Brunswick, Ontario, Québec and Saskatchewan, if an issuer decides to change its financial year end by more than 14 days, it must deliver to the securities regulatory authority and make reasonably available to each holder of a security acquired under subsection (2.1) a notice containing the information set out in subsection (17.15) as soon as practicable and, in any event, no later than the earlier of

(a) the deadline, based on the issuer's old financial year end, for the next annual financial statements referred to in subsections (17.4) and (17.5), and

(b) the deadline, based on the issuer's new financial year end, for the next annual financial statements referred to in subsections (17.4) and (17.5).

(17.14) In Nova Scotia, if an issuer decides to change its financial year end by more than 14 days, it must make reasonably available to each holder of a security acquired under subsection (2.1) a notice containing the information set out in subsection (17.15) as soon as practicable and, in any event, no later than the earlier of

(a) the deadline, based on the issuer's old financial year end, for the next annual financial statements referred to in subsection (17.6), and

(b) the deadline, based on the issuer's new financial year end, for the next annual financial statements referred to in subsection (17.6).

(17.15) The notice referred to in subsections (17.13) and (17.14) must state

(a) that the issuer has decided to change its financial year end,

(b) the reason for the change,

(c) the issuer's old financial year end,

(d) the issuer's new financial year end,

(e) the length and ending date of the periods, including the comparative periods, of the annual financial statements referred to in subsections (17.4), (17.5) and (17.6) for the issuer's transition year and its new financial year, and

(f) the filing deadline for the annual financial statements for the issuer's transition year.

(17.16) If a transition year is less than 9 months in length, the issuer must include as comparative financial information to its annual financial statements for its new financial year

(a) a statement of financial position, a statement of comprehensive income, a statement of changes in equity, a statement of cash flows, and notes to the financial statements for its transition year,

(b) a statement of financial position, a statement of comprehensive income, a statement of changes in equity, a statement of cash flows, and notes to the financial statements for its old financial year,

(c) in the following circumstances, a statement of financial position as at the beginning of the old financial year:

(i) the issuer discloses in its annual financial statements an unreserved statement of compliance with IFRS, and

(ii) the issuer

(A) applies an accounting policy retrospectively in its annual financial statements,

(B) makes a retrospective restatement of items in its annual financial statements, or

(C) reclassifies items in its annual financial statements, and

(d) in the case of the issuer's first IFRS financial statements, the opening IFRS statement of financial position at the date of transition to IFRS.

(17.17) A transition year must not exceed 15 months.

(17.18) An SEC issuer satisfies subsections (17.13), (17.14) and (17.16) if

(a) it complies with the requirements of U.S. laws relating to a change of fiscal year, and

(b) it delivers a copy of all materials required by U.S. laws relating to a change in fiscal year to the securities regulatory authority at the same time as, or as soon as practicable after, they are filed with or furnished to the SEC and, in any event, no later than 120 days after the end of its most recently completed financial year.

(17.19) The financial statements of an issuer referred to in subsections (17.4), (17.5) and (17.6) must be accompanied by a notice of the issuer disclosing in reasonable detail the use of the aggregate gross proceeds raised by the issuer under section 2.9 in accordance with Form 45-106F16, unless the issuer has previously disclosed the use of the aggregate gross proceeds in accordance with Form 45-106F16.

(17.20) In New Brunswick, Nova Scotia and Ontario, an issuer must make reasonably available to each holder of a security acquired under subsection (2.1) a notice of each of the following events in accordance with Form 45-106F17, within 10 days of the occurrence of the event:

(a) a discontinuation of the issuer's business;

(b) a change in the issuer's industry;

(c) a change of control of the issuer.

(17.21) An issuer is required to make the disclosure required respectively by subsections (17.4), (17.5), (17.6), (17.19) and (17.20) until the earliest of

(a) the date the issuer becomes a reporting issuer in any jurisdiction of Canada, and

(b) the date the issuer ceases to carry on business.

(17.22) In Ontario, an issuer that is not a reporting issuer in Ontario that distributes securities in reliance on the exemption in subsection (2.1) is designated a market participant under the Securities Act (Ontario).

(17.23) In New Brunswick, an issuer that is not a reporting issuer in New Brunswick that distributes securities in reliance on the exemption in subsection (2.1) is designated a market participant under the Securities Act (New Brunswick).

(18) Repealed. [B.C. Reg. 86/2011, s. (e).].

5. Paragraph 6.1(1)(c) is amended by replacing "or (2) [Offering memorandum for Alberta, B.C., Manitoba, New Brunswick, Nova Scotia, Newfoundland and Labrador, Northwest Territories, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon]" with ", (2) or (2.1) [Offering memorandum]".

6. Section 6.5 is amended by adding the following subsection:

(1.1) In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, the required form of risk acknowledgement for individual investors includes Schedule 1 Classification of Investors Under the Offering Memorandum Exemption and Schedule 2 Investment Limits for Investors Under the Offering Memorandum Exemption to Form 45-106F4..

7. Part 8 is amended by adding the following sections:

8.4.1 Transition -- offering memorandum exemption -- update of offering memorandum -- Despite subsection 2.9(5.1), in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan, an issuer is not required to update an offering memorandum that was filed in the local jurisdiction before April 30, 2016, solely to incorporate the statement required under paragraph 2.9(5.1)(a), unless the offering memorandum would otherwise be required to be updated pursuant to subsection 2.9(14) or Instruction B.12 of Form 45-106F2 Offering Memorandum for Non-Qualifying Issuers.

8.4.2 Transition -- offering memorandum exemption -- marketing materials -- Despite paragraph 2.9(17.1)(a), in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan, OM marketing materials that relate to an offering memorandum that was filed in the local jurisdiction before April 30, 2016 and that are delivered or made reasonably available after April 30, 2016 must be filed within 10 days from the earlier of delivery to, or being made reasonably available to, a prospective purchaser..

8. item 10.1 of Form 45-106F2 Offering Memorandum for Non-Qualifying Issuers is amended by adding "Ontario," before "Prince Edward Island".

9. Item 10.2 of Form 45-106F2 Offering Memorandum for Non-Qualifying Issuers is amended by adding "Ontario," before "Prince Edward Island".

10. Item 10 OF Form 45-106F3 Offering Memorandum for Qualifying Issuers is amended by adding "Ontario," before "Prince Edward Island".

11. Form 45-106F4 Risk Acknowledgement is amended

(a) by replacing "In Alberta, Manitoba, Northwest Territories, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon to qualify as an eligible investor, you may be required to obtain that advice" with "In Manitoba, Northwest Territories, Nunavut, Prince Edward Island and Yukon to qualify as an eligible investor, you may be required to obtain that advice", and

(b) by adding the following:

Schedule 1

Classification of Investors Under the Offering Memorandum Exemption

Instructions: This schedule must be completed together with the Risk Acknowledgement Form and Schedule 2 by individuals purchasing securities under the exemption (the offering memorandum exemption) in subsection 2.9(2.1) of National Instrument 45-106 Prospectus Exemptions (NI 45-106) in Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan.

- - - - - - - - - - - - - - - - - - - -

How you qualify to buy securities under the offering memorandum exemption

Initial the statement under A, B, C or D containing the criteria that applies to you. (You may initial more than one statement.) If you initial a statement under B or C, you are not required to complete A.

- - - - - - - - - - - - - - - - - - - -

Schedule 2

Investment Limits for Investors Under the Offering Memorandum Exemption

Instructions: This schedule must be completed together with the Risk Acknowledgement Form and Schedule 1 by individuals purchasing securities under the exemption (the offering memorandum exemption) in subsection 2.9(2.1) of National Instrument 45-106 Prospectus Exemptions (NI 45-106) in Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan.

- - - - - - - - - - - - - - - - - - - -

SECTION 1 TO BE COMPLETED BY THE PURCHASER

1. Investment limits you are subject to when purchasing securities under the offering memorandum exemption

You may be subject to annual investment limits that apply to all securities acquired under the offering memorandum exemption in a 12 month period, depending on the criteria under which you qualify as identified in Schedule 1. Initial the statement that applies to you.

- - - - - - - - - - - - - - - - - - - -

12. The Instrument is amended by adding the following form after Form 45-106F15:

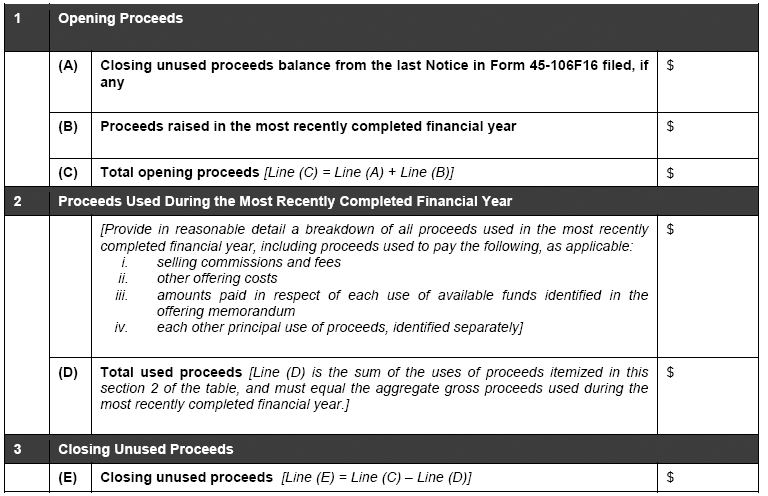

Form 45-106F16

Notice of Use of Proceeds

[Insert issuer name]

For the financial year ended [Insert end date of most recently completed financial year]

Date: [Specify the date of the Notice. The date must be no earlier than the date of the auditor's report on the financial statements for the issuer's most recently completed financial year.]

[Provide the information specified in the following table.]

[If any of the proceeds required to be disclosed in this table were paid directly or indirectly to a related party (as defined in Instruction A.6 of Form 45-106F2 Offering Memorandum Form for Non-Qualifying Issuers) of the issuer, state in each case the name of the related party to whom the payment was made, their relationship to the issuer and the amount paid to the related party.]

Instructions for Completing

Form 45-106F16

Notice of Use of Proceeds

1. The amount for Line (A) is taken from Line (E) in the prior year's Notice of Use of Proceeds (Notice), if applicable. If a Notice was not required in the prior year, then the amount for Line (A) is $nil.

2. The amount for Line (B) is the aggregate gross proceeds raised in all jurisdictions in Canada under section 2.9 [Offering memorandum] of National Instrument 45-106 (the OM exemption) during the most recently completed financial year. If an issuer raised funds in reliance on other prospectus exemptions concurrently with the OM exemption during the year and it is impractical to separately track proceeds raised only under the OM exemption, the issuer can provide the disclosure outlined in the table for the aggregate gross proceeds raised under all prospectus exemptions during the most recently completed financial year.

3. If Line (C) is $nil, then the issuer does not have an obligation to file, deliver or make reasonably available the Notice for that financial year.

4. In Section 2 of the table, the issuer must provide a breakdown in reasonable detail of the uses of the aggregate gross proceeds during the most recently completed financial year. Issuers should ensure that the disclosure is specific enough and provides sufficient detail for an investor to understand how the proceeds have been used.

5. Both direct and indirect payments to related parties must be disclosed. An example of an indirect payment could include repayment of a debt that was incurred for a prior payment to a related party.

6. Proceeds invested on a temporary basis would not generally be considered to have been used.

13. The Instrument is amended by adding the following form:

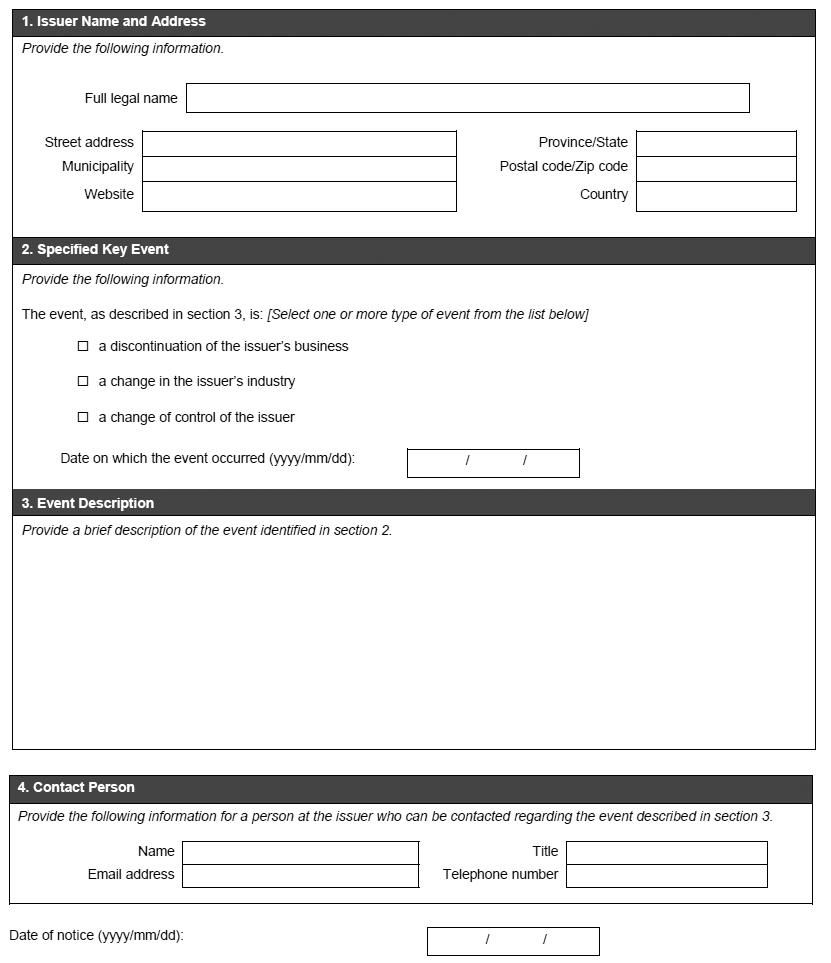

Form 45-106F17

Notice of Specified Key Events

This is the form required under subsection 2.9(17.20) of National Instrument 45-106 Prospectus Exemptions (NI 45-106) in New Brunswick, Nova Scotia and Ontario to make available notice of specified key events to holders of securities acquired under subsection 2.9(2.1) of NI 45-106.

14. This Instrument comes into force in Ontario on January 13, 2016 and in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan on April 30, 2016.

Annex A-2 -- Amending Instrument for National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

ANNEX A-2

AMENDING INSTRUMENT FOR NATIONAL INSTRUMENT 52-107 ACCEPTABLE ACCOUNTING PRINCIPLES AND AUDITING STANDARDS

Amendments to National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards

1. National Instrument 52-107 Acceptable Accounting Principles and Auditing Standards is amended by this Instrument.

2. Section 1.1 is amended

(a) by deleting "except in Ontario, " from paragraph (d) of the definition of "acquisition statements".

3. Subsection 2.1(2) is amended

(a) by deleting "except in Ontario, " wherever it occurs, and

(b) by deleting "and" at the end of paragraph (g), by adding ", and" at the end of paragraph (h) and by adding the following paragraph:

(i) all financial statements

(i) filed by an issuer under subsection 2.9(17.4) of National Instrument 45-106 Prospectus Exemptions,

(ii) delivered by an issuer under subsection 2.9(17.5) of National Instrument 45-106 Prospectus Exemptions, or

(iii) made reasonably available by an issuer under subsection 2.9(17.6) of National Instrument 45-106 Prospectus Exemptions.

4. In the following provisions, "(c) and (e)" is replaced with "(c), (e) and (i)":

(a) subsection 3.2(1);

(b) subsection 3.7(1);

(c) subsection 3.8(1);

(d) subsection 3.9(1);

(e) subsection 3.10(1).

5. This Instrument comes into force in Ontario on January 13, 2016 and in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan on April 30, 2016.

Annex A-3 -- Amending Instrument for National Instrument 45-102 Resale of Securities

ANNEX A-3

AMENDING INSTRUMENT FOR NATIONAL INSTRUMENT 45-102 RESALE OF SECURITIES

Amendments to National Instrument 45-102 Resale of Securities

1. National Instrument 45-102 Resale of Securities is amended by this Instrument.

2. Appendix D is amended in the list preceding "Transitional and Other Provisions" by replacing "section 2.9 [Offering memorandum] (in Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Northwest Territories, Nova Scotia, Nunavut, Prince Edward Island, Québec, Saskatchewan and Yukon);" with "section 2.9 [Offering memorandum];".

3. This Instrument comes into force in Ontario on January 13, 2016 and in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan on April 30, 2016.

Annex A-4 -- Amending Instrument for Multilateral Instrument 11-102 Passport System

ANNEX A-4

AMENDING INSTRUMENT FOR MULTILATERAL INSTRUMENT 11-102 PASSPORT SYSTEM

Amendments to Multilateral Instrument 11-102 Passport System

1. Multilateral Instrument 11-102 Passport System is amended by this Instrument.

2. Appendix D is amended by replacing the following rows

|

Offering memorandum in required form |

s. 2.9(5) of NI 45-106 |

n/a |

|

|

||

|

Requirement to file offering memorandum within prescribed time |

s. 2.9(14) of NI 45-106 |

n/a |

with

|

Offering memorandum in required form |

s 2.9(5) of NI 45-106 |

s 2.9(5) & s.2.9(5.1) of NI 45-106 |

s.2.9(5) & s.2.9(5.1) of NI 45-106 |

s.2.9(5) of NI 45-106 |

s.2.9(5) & s.2.9(5.1) of NI 45-106 |

s.2.9(5) & s.2.9(5.1) of NI 45-106 |

s.2.9(5) & s.2.9(5.1) of NI 45-106 |

s.2.9(5) of NI 45-106 |

s.2.9(5) of NI 45-106 |

s.2.9(5) of NI 45-106 |

s.2.9(5) of NI 45-106 |

s.2.9(5) of NI 45-106 |

s.2.9(5) & s..2.9(5.1) of NI 45-106 |

|

|

|||||||||||||

|

Requirement to file offering memorandum within prescribed time |

s.2.9(14) of NI 45-106 |

||||||||||||

3. This Instrument comes into force in Alberta, New Brunswick, Nova Scotia, Québec and Saskatchewan on April 30, 2016.

Annex B-1 -- Changes to Companion Policy 45-16CP Prospectus Exemptions

ANNEX B-1

CHANGES TO COMPANION POLICY 45-106CP PROSPECTUS EXEMPTIONS

This Annex reflects changes to Companion Policy 45-106CP Prospectus Exemptions that will take effect upon the coming into force of the Rule Amendments set out in Annex A. Additions are represented with underlined text and deletions are represented with strikethrough text.

PART 1 -- INTRODUCTION

1.8 Persons created to use exemptions ("syndication")

Sections 2.3(5), 2.4(1), 2.9(3), 2.9(3.0.1) and 2.10(2) of NI 45-106 specifically prohibit syndications. A distribution of securities to a person that had no pre-existing purpose and is created or used solely to purchase or hold securities under exemptions (a "syndicate") may be considered a distribution of securities to the persons beneficially owning or controlling the syndicate.

For example, a newly formed company with 15 shareholders is set up with the intention of purchasing $150 000 worth of securities under the minimum amount investment exemption. Each shareholder of the newly formed company contributes $10 000. In this situation the shareholders of the newly formed company are indirectly investing $10 000 when the exemption requires that they each invest $150 000. Consequently, both the newly formed company and its shareholders may need to comply with the requirements of the minimum amount investment exemption, or find an alternative exemption to rely on.

Syndication related concerns should not ordinarily arise if the purchaser under the exemption is a corporation, syndicate, partnership or other form of entity that is pre-existing and has a bona fide purpose other than investing in the securities being sold. However, it is an inappropriate use of these exemptions to indirectly distribute securities when the exemption is not available to directly distribute securities to each person in the syndicate.

PART 3 -- CAPITAL RAISING EXEMPTIONS

3.3 Advertising

NI 45-106 does not restrict the use of advertising to solicit or find purchasers. However, issuers and selling security holders should review other securities legislation and securities directions for guidelines, limitations and prohibitions on advertising intended to promote interest in an issuer or its securities. For example, any advertising or marketing communications must not contain a misrepresentation and should be consistent with the issuer's public disclosure record.

3.3.1 Advertising and marketing materials under the offering memorandum exemption

In Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan, an offering memorandum prepared in accordance with the offering memorandum exemption in section 2.9(2.1) of NI 45-106 must incorporate by reference any marketing materials used in relation to a distribution under the offering memorandum exemption. Subsection 2.9(8) of NI 45-106 requires the issuer to sign a certificate that indicates that the offering memorandum does not contain a misrepresentation. As marketing materials are incorporated by reference into the offering memorandum, the issuer must also ensure that the information contained in marketing materials does not contain a misrepresentation.

In these jurisdictions, an issuer or registrant that uses marketing materials as part of an offering made in reliance on the offering memorandum exemption must review the marketing materials to confirm that they are consistent with the offering document and are fair, balanced and not misleading. In addition, these jurisdictions expect an issuer or registrant to determine whether any claims set out in marketing materials adequately refer to information to support these claims and representations. For example, if benchmarks are used for comparison purposes, the issuer or registrant should assess whether the benchmarks are relevant and comparable to the investment in question and confirm the marketing materials:

(a) adequately explain differences between the benchmark and the investment,

(b) make reference to the source of the benchmark and identify the date to which the information is current, and

(c) where relevant, caution purchasers that historical performance is not necessarily indicative of future results.

Issuers that prepare offering memoranda in accordance with Form 45-106F2 Offering Memorandum for Non-Qualifying Issuers, are also required to comply with requirements relating to forward-looking information, which are described in Instructions A.12 and B.14 of Form 45-106F2. Issuers cannot disseminate material forward-looking information unless it is contained within the offering memorandum. Additionally, forward-looking information contained in an offering memorandum must comply with certain requirements in National Instrument 51-102 Continuous Disclosure Obligations. These requirements also extend to marketing materials that are used in connection with a distribution under the offering memorandum exemption.

In these jurisdictions, if an issuer or registrant intends to rely on marketing materials prepared by a third party, such as an analyst report that rates a security or compares a security with securities of other issuers, the issuer or registrant is expected to perform its own assessment of the marketing materials to confirm that they are fair, balanced and not misleading. For example, if the report has been paid for by the issuer, or if there are other relationships between the analyst and the issuer, it would be inappropriate to describe the report as being an "independent" report. The report should also prominently disclose the fees paid and relationships between the analyst and the issuer. An issuer or registrant should not rely on marketing materials prepared by a third party without independently reviewing the materials prior to use.

A registrant should be aware of other CSA guidance on the review and use of marketing materials and reliance on marketing materials prepared by third parties.

3.4 Restrictions on finder's fees or commissions

The following restrictions apply with respect to certain exemptions under NI 45-106:

(1) no commissions or finder's fees may be paid to directors, officers, founders and control persons in connection with a distribution made under the private issuer exemption or the family, friends and business associates exemption, except in connection with a distribution of a security to an accredited investor under the private issuer exemption; and

(2) in Northwest Territories

,and Nunavutand Saskatchewan, only a registered dealer may be paid a commission or finder's fee in connection with a distribution of a security to a purchaser in one of those jurisdictions under the offering memorandum exemption.

3.8 Offering memorandum

(1) Eligibility criteria -- Alberta, Manitoba, Northwest Territories, Nunavut, and Prince Edward Island, Québec and Saskatchewan

Alberta, Manitoba, Northwest Territories, Nunavut, Prince Edward Island, Québec, Saskatchewan, and Yukon impose eligibility criteria on persons investing under the offering memorandum exemption. In these jurisdictions, the purchaser must be an eligible investor if the purchaser's acquisition cost is more than $10 000.

In determining the acquisition cost to a purchaser who is not an eligible investor, include any future payments that the purchaser will be required to make. Proceeds that may be obtained on exercise of warrants or other rights, or on conversion of convertible securities, are not considered to be part of the acquisition cost unless the purchaser is legally obligated to exercise or convert the securities. The $10 000 maximum acquisition cost is calculated per distribution of security.

Nevertheless, concurrent and consecutive, closely-timed offerings to the same purchaser will usually constitute one distribution of a security. Consequently, when calculating the acquisition cost, all of these offerings by or on behalf of the issuer to the same purchaser who is not an eligible investor would be included. It would be inappropriate for an issuer to try to circumvent the $10 000 threshold by dividing a subscription in excess of $10 000 by one purchaser into a number of smaller subscriptions of $10 000 or less that are made directly or indirectly by the same purchaser.

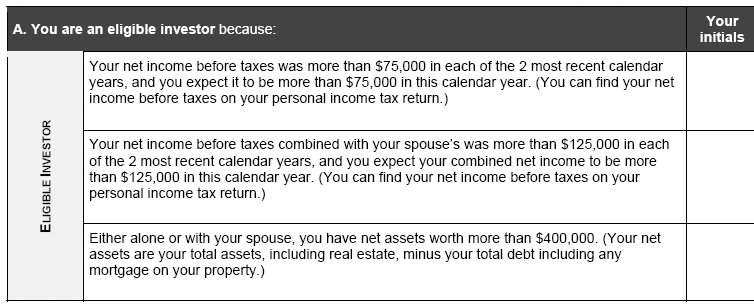

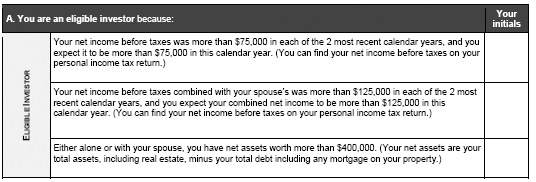

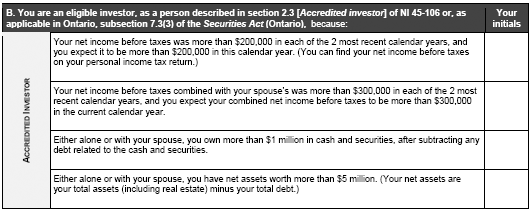

A purchaser can qualify as an eligible investor under various categories of the definition, including if the purchaser has and has had in prior years either $75 000 pre-tax net income or profit or has $400 000 worth of net assets. In calculating a purchaser's net assets, subtract the purchaser's total liabilities from the purchaser's total assets. The value attributed to assets should reasonably reflect their estimated fair value. Income tax should be considered a liability if the obligation to pay it is outstanding at the time of the distribution of a security.

Another way a purchaser can qualify as an eligible investor is to obtain advice from an eligibility adviser. An eligibility adviser is a person registered as an investment dealer (or in an equivalent category of unrestricted dealer in the purchaser's jurisdiction) that is authorized to give advice with respect to the type of security being distributed. In Saskatchewan and Manitoba, certain lawyers and public accountants may also act as eligibility advisers.

A registered investment dealer providing advice to a purchaser in these circumstances is expected to comply with the "know your client" and suitability requirements under applicable securities legislation and SRO rules and policies. Some dealers have obtained exemptions from the "know your client" and suitability requirements because they do not provide advice. An assessment of suitability by these dealers is not sufficient to qualify a purchaser as an eligible investor.

(1.1) Eligibility criteria and investment limits -- Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan

(a) Eligibility criteria

Alberta, New Brunswick, Nova Scotia, Ontario, Québec and Saskatchewan impose eligibility criteria on persons investing under the offering memorandum exemption.