CSA Staff Notice 45-323 (Revised) Update on Use of the Rights Offering Exemption in National Instrument 45-106 Prospectus Exemptions

CSA Staff Notice 45-323 (Revised) Update on Use of the Rights Offering Exemption in National Instrument 45-106 Prospectus Exemptions

CSA Staff Notice 45-323 (revised)

Update on Use of the Rights Offering Exemption in

National Instrument 45-106 Prospectus Exemptions

July 26, 2018

Purpose

This notice{1} provides an update by staff of the Canadian Securities Administrators (staff or we) on use of the streamlined rights offering exemption for reporting issuers (the rights offering exemption or exemption) effective in all Canadian jurisdictions since December 8, 2015. It also provides guidance based on our reviews of offerings using the exemption.

Background

The Canadian Securities Administrators (the CSA) adopted a streamlined rights offering exemption as a way of addressing concerns that issuers seldom used prospectus-exempt rights offerings to raise capital because of the associated time and cost. At the same time, rights offerings can be one of the fairer ways for issuers to raise capital as they provide existing security holders with an opportunity to protect themselves from dilution. We designed the rights offering exemption to make prospectus-exempt rights offerings more attractive to reporting issuers while maintaining investor protection. Key elements of the rights offering exemption include:

• a rights offering notice that reporting issuers must file and send to security holders informing them how to access the rights offering circular electronically,

• a simplified rights offering circular in a question and answer format intended to be easier to prepare and more straightforward for investors to understand -- it has to be filed but not sent to security holders,

• a dilution limit of 100%, increased from 25%, and

• statutory secondary market liability.

When we proposed the rights offering exemption, we indicated that staff in certain jurisdictions would conduct reviews of rights offerings for a period of two years after adoption. Staff have now completed those reviews.

Use of rights offering exemption

General

Use of prospectus-exempt rights offerings by reporting issuers has increased significantly Canada-wide since adoption of the exemption. Prior to adoption, there were approximately 13 prospectus-exempt rights offerings by Canadian reporting issuers each year. Between December 8, 2015 and December 31, 2017, 60 issuers used the exemption to raise $535.5 million, as follows:

|

Rights offerings completed and amounts raised |

||

|

|

||

|

Principal jurisdiction |

Number |

Amount Raised |

|

|

||

|

Ontario |

16 |

$ 192,122,322 |

|

|

||

|

British Columbia |

25 |

$ 180,759,899 |

|

|

||

|

Alberta |

16 |

$ 109,159,080 |

|

|

||

|

Manitoba |

2 |

$ 52,432,332 |

|

|

||

|

Québec |

1 |

$ 1,000,239 |

|

|

||

|

Total |

60 |

$ 535,473,872 |

This is an increase of approximately 130% in the use of prospectus-exempt rights offerings by reporting issuers since adoption of the exemption.

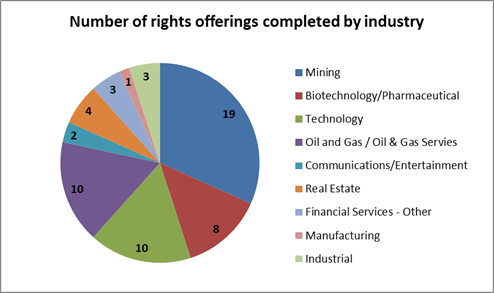

As indicated below, the rights offering exemption was used across all industries.

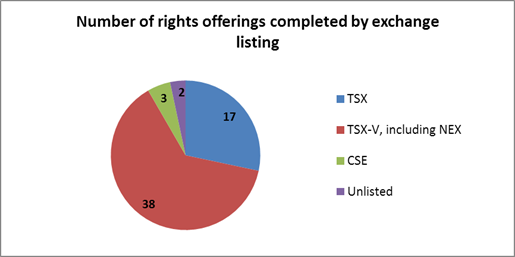

Use of the exemption by exchange listing was as follows:

Time and cost

One of the reasons we adopted the streamlined rights offering exemption was to reduce the time and cost for an issuer to complete a rights offering. Prior to adoption of the streamlined exemption, CSA staff looked at 93 prospectus-exempt rights offerings by reporting issuers over a seven-year time period. During that time, the average length of time to complete a rights offering was 85 days.

Since the adoption of the streamlined exemption, the time to conduct a rights offering has been reduced significantly. Our reviews indicate that the average number of days from filing of the rights offering notice to closing was 41 days.

Dilution and participation by insiders

On average, issuers sought to issue 51% of the outstanding securities of the applicable class through the rights offering and actually issued 40% of the outstanding securities. The percentage of amounts raised from insiders was 47%. In addition, of the 29 rights offerings that had a stand-by commitment, 24 were provided in whole or in part by an insider or related party.

Reviews of rights offerings

We reviewed all 60 rights offerings conducted using the exemption. In general, we found that the offerings met the requirements of the exemption. However, we noted the following areas where compliance and disclosure could be improved:

• stand-by commitments,

• use of available funds, and

• closing news release.

1. Stand-by Commitments

Of the 60 rights offerings that we reviewed, 29 had stand-by commitments. In 14 offerings, the stand-by commitment was provided by multiple parties. We note that the use of multiple stand-by guarantors potentially mitigates any concerns regarding change of control of the issuer provided that the guarantors are not acting jointly or in concert.

When a rights offering has a stand-by commitment, Form 45-106F15 Rights Offering Circular for Reporting Issuers (the Form) requires additional disclosure including the relationship of the stand-by guarantor with the issuer, the security holdings of the stand-by guarantor before and after the rights offering, and confirmation that the stand-by guarantor has the financial ability to carry out its stand-by commitment.

Item 24 of the Form requires the issuer to explain the nature of its relationship with the stand-by guarantor including whether, and, if applicable, the basis on which the stand-by guarantor is a related party of the issuer. As the stand-by guarantor is often a related party of the issuer, we think this disclosure is important information for security holders to have in considering their investment decision.

In some rights offerings, we noted weakness in the disclosure regarding the nature of the relationship between the issuer and the stand-by guarantors. For instance, one issuer did not disclose the relationship at all, although the relationship was disclosed in a separate continuous disclosure document. We note that prior disclosure of a relationship in the issuer's continuous disclosure record is not sufficient to meet the requirements of the Form.

Issuers are also required to confirm in the rights offering circular that the stand-by guarantor has the financial ability to carry out its stand-by commitment. This statement provides clarity to security holders that the stand-by guarantor will be able to fulfill its obligations. We highlight this requirement because providing this statement in the rights offering circular is a condition of use of the exemption.

2. Use of available funds

Two of the key disclosure items in the Form are the available funds after the rights offering and how the issuer will use them. Most issuers we reviewed provided sufficient disclosure in these areas. However, we did note some recurring deficiencies in the areas set out below.

Working capital

As part of disclosing available funds after the rights offering, an issuer must disclose any working capital deficiency. This includes adding the working capital deficiency as a line item in the table of available funds. This disclosure is important because it gives security holders a better picture of the issuer's prospects following the rights offering than if the disclosure of the proceeds were provided without taking into account the working capital deficiency.

Issuers are required to disclose the working capital deficiency as of the most recent month end. If there has been a significant change in working capital since the most recently audited annual financial statements, the issuer must explain that change. We found that some issuers did not explain the change in working capital. In the Form, we provide guidance on what we would consider to be a significant change. Examples are changes that result in material uncertainty regarding the issuer's going concern assumption or a change in the working capital balance from positive to negative or vice versa. We remind issuers that even if the change in working capital is from a negative position to a positive position, it must still be explained.

Liquidity

Issuers whose available funds are insufficient to cover short-term liquidity requirements and overhead expenses for the next 12 months are required to:

• discuss how management plans to discharge liabilities as they become due,

• state the minimum amount required to meet short-term liquidity demands, and

• disclose management's assessment of the issuer's ability to continue as a going concern.

This disclosure is critical to investors because it highlights significant risks that the issuer is facing or may face in the short term. We noted a number of issuers that reported a working capital deficiency without providing meaningful disclosure as contemplated in the Form.

Allocation of Available Funds

Issuers are required to provide a detailed breakdown of how they will use the available funds and to describe in reasonable detail each of the principal purposes. We noted some instances where the level of detail in the breakdown of the use of funds could be improved.

In general, allocating funds simply to working capital is not sufficient to meet the requirement for either a detailed breakdown or reasonable detail. We would generally expect issuers with negative cash flow from operating activities to provide a breakdown of their key expenses for at least the next 12 months. For instance, if an issuer is engaged in mineral exploration, we would expect it to break down the available funds so that investors know how much is allocated to each exploration program as well as how much is allocated to general and administrative and other key expenses.

3. Closing news release

Another requirement of the exemption is that the issuer must file a closing news release disclosing certain details about who subscribed to the rights offering, including the amount subscribed for by insiders and stand-by guarantors, distinguishing between the basic and additional subscription privileges. We found some instances where issuers did not include all of the required information.

We also remind issuers that there is a specific SEDAR document type for closing news releases and that closing news releases should be filed under this document type in the same SEDAR project as the rights offering circular.

Conclusion

Since adoption of the streamlined rights offering exemption in December 2015, the exemption is being used more frequently and is allowing issuers to raise more capital in a shorter time frame. In general, issuers have been using the exemption appropriately and complying with the Form requirements.

Questions

Please refer your questions to any of the following:

British Columbia Securities CommissionLarissa M. StreuSenior Legal Counsel, Corporate Finance604-899-6888 or 1-800-373-6393Anita CyrAssociate Chief Accountant, Corporate Finance604-899-6579 or 1-800-373-6393Alberta Securities CommissionAshlyn D'AoustSenior Legal Counsel, Corporate Finance403-355-4347 or 1-877-355-0585Manitoba Securities CommissionWayne BridgemanDeputy Director, Corporate Finance204-945-4905Ontario Securities CommissionDavid SuratSenior Legal Counsel, Corporate Finance416-593-8052Raymond HoSenior Accountant, Corporate Finance416-593-8106 or 1-877-785-1555Autorité des marchés financiersMarie-Josée LacroixSenior Securities Analyst, Corporate Finance514-395-0337 ext.4415Alexandra LeeSenior Regulatory Advisor, Corporate Finance514-395-0337 ext.4465Nova Scotia Securities CommissionDonna M. GouthroSecurities Analyst902-424-7077

{1} This notice is a revised version of CSA Staff Notice 45-323, as published on April 20, 2017.